CA - 8% Yielding Dividend Aristocrat Bargains You Don't Want To Miss

2023-11-14 07:10:00 ET

Summary

- Even legendary dividend aristocrats can fail, with General Electric and V.F. Corporation being key examples. General Electric investors are down 65% from 2000's highs, and V.F. Corp. investors are 82% underwater.

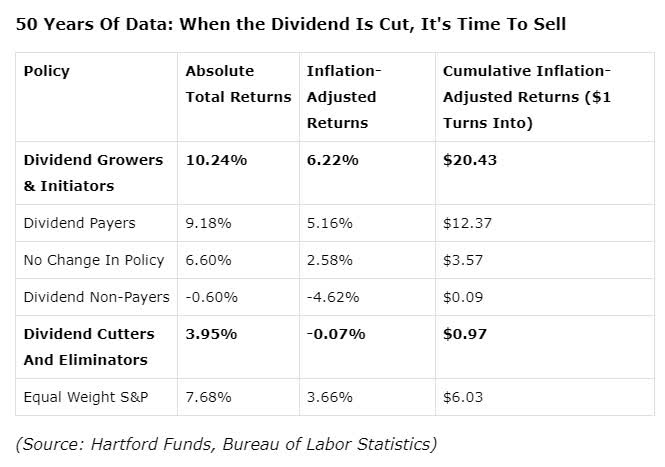

- Short-term price is vanity, cash flow is sanity, and dividends are reality. 50 years of historical data is clear: if the dividend is cut, it's time to sell and move on.

- UGI Corporation is a utility conglomerate that hasn't cut its dividend in 138 years. But its cut risk is rising due to struggles at AmeriGas, which is 40% of sales.

- If UGI Corporation uses its strategic AmeriGas review as an excuse to cut the dividend sell immediately because it effectively means "never in history, not even during the Great Depression, has our business been this terrible."

- Here are three low-risk BBB+ rated Ultra SWAN dividend aristocrats with a 1% risk of a dividend cut even in a Pandemic-level economic recession. They are expected to potentially deliver 330% returns in the next decade, doubling the market's returns. But in the next 2 years, they offer 8X better return potential than the S&P.

At our service, we constantly scan the skies for signs of trouble for income investors.

To paraphrase Thomas Jefferson:

Eternal vigilance is the price of financial freedom."

{kind=link}

Let's not forget that while the U.S. stock market is 97.5% risk-free in the long term (unless the world ends, you can't lose money in U.S. stocks if you buy and hold for long enough), individual companies, even utilities, do fail.

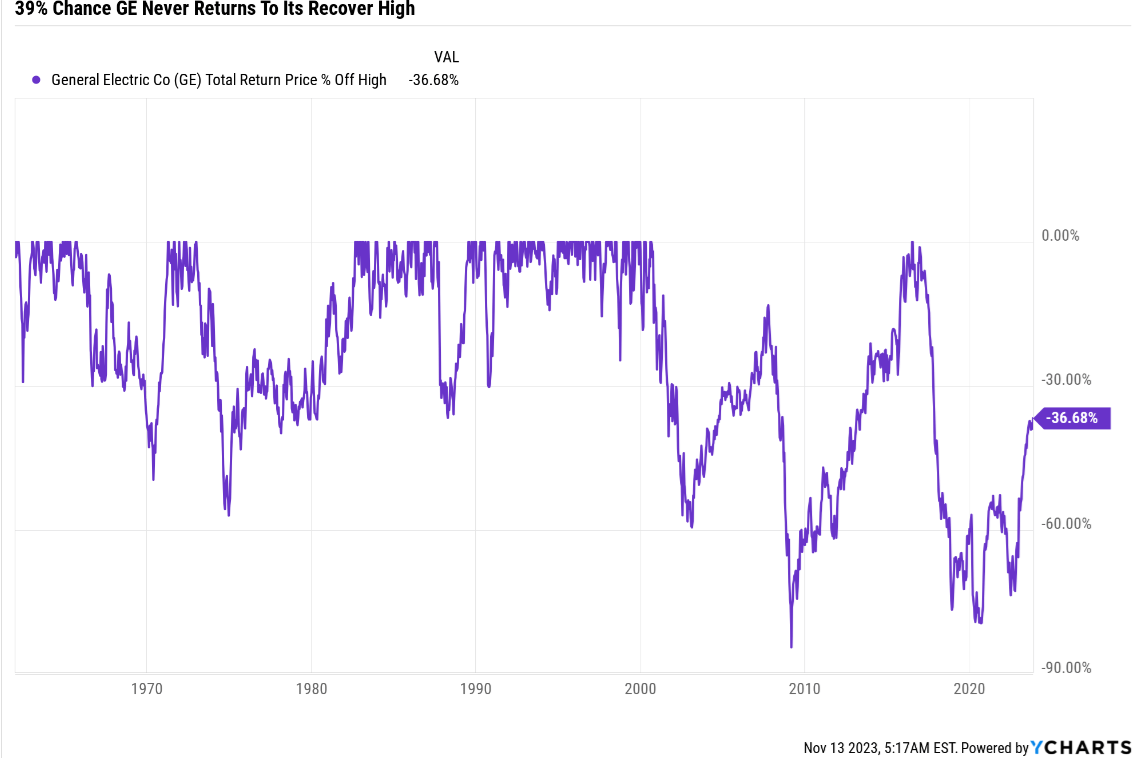

In fact, let's not forget General Electric (GE), the ultimate example of a fallen aristocrat.

- most valuable company in the world in 2000

- run by Fortune magazine's "CEO of the century"

- AAA-rated balance sheet

- dividend aristocrat

- hadn't missed earnings expectations in 10 years.

There was no more SWANier (sleep well at night) Ultra SWAN than GE a quarter century ago.

And then the wheels fell off the bus, and on an annual basis, GE cut its dividend five times.

{kind=link}

When the dividend is cut, management is saying, "things are worse than they've been in years, or even decades."

When a dividend aristocrat or king cuts, it means that never in the last 25 or 50 years or more have the fundamentals of the business been so dire.

The safest dividend is one that's just been raised, and the reverse is also true. A dividend that's been cut is still at elevated risk of another cut.

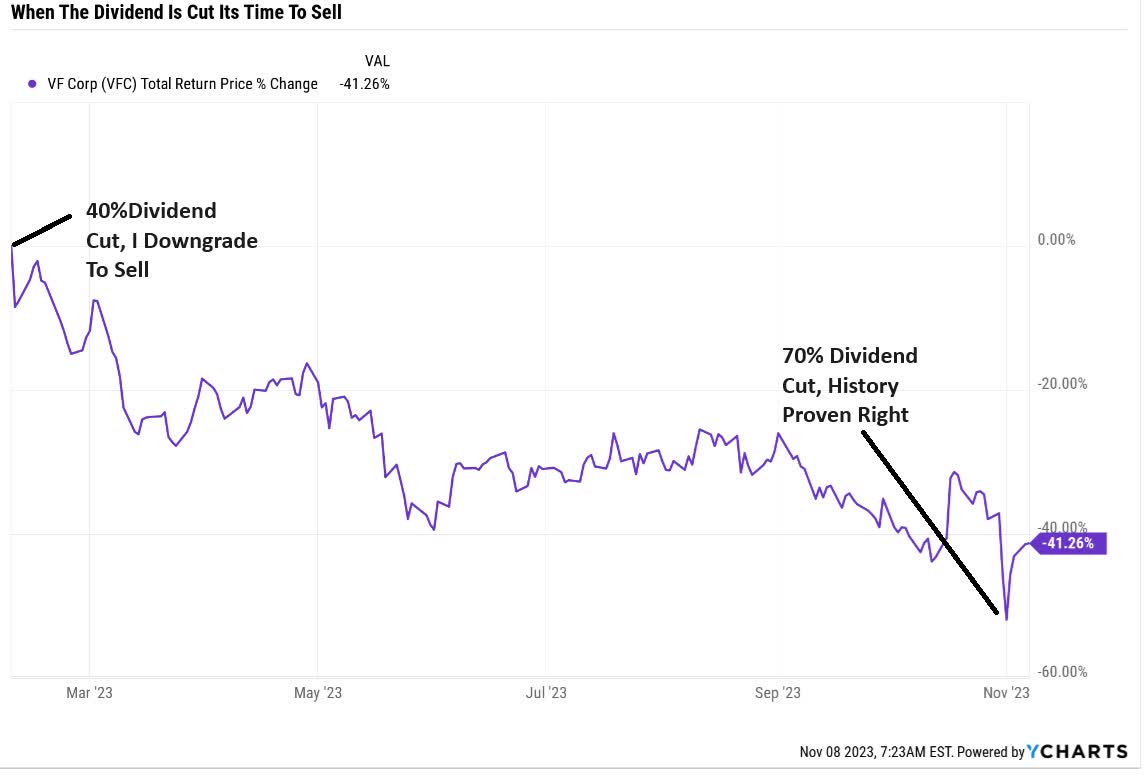

Consider the example of V.F. Corporation (VFC).

I warned Seeking Alpha readers once and our members several times that the VFC dividend cut was a signal to sell and never look back.

{kind=link}

And indeed, the first dividend cut was followed by a 70% cut months later that sent shares plunging.

By the end of that day, VFC had been cut in half even after already falling over 50% by the time of the first cut.

{kind=link}

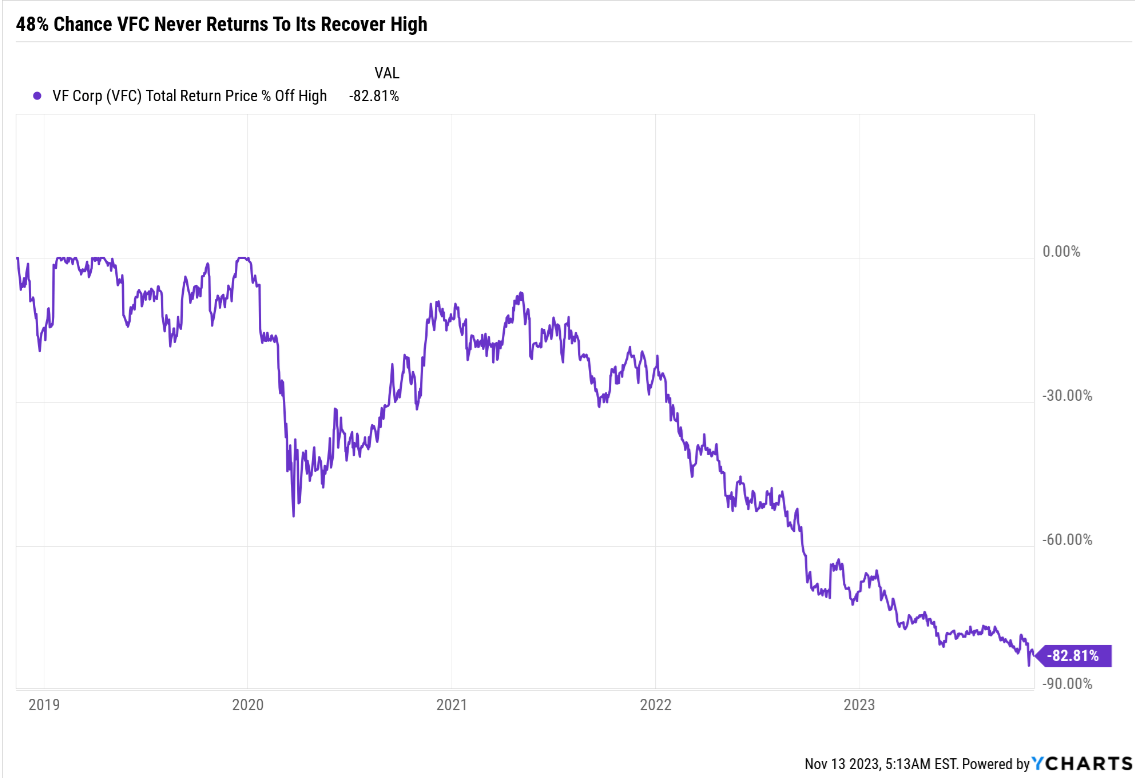

The pandemic hit VFC like so many other clothing companies. But it was well on its way to recovery until Supreme, its multi-billion acquisition announced in November 2020 during the era of free money, started to struggle.

VFC has entered the danger zone, down over 70% from record highs. A level that indicates a 48% chance, a coin flip, as to whether it will ever achieve a new record high again.

{kind=link}

Just consider how GE investors have fared since 2000, when they are down 36%, including dividends and not adjusting for inflation.

- 82% inflation

- 65% inflation-adjusted loss after 23 years.

You can see why dividend cuts are dangerous and why I take the time to warn readers and Dividend Kings members about rising dividend cut risk among aristocrats.

- Walgreens' Dividend Could Be Toast So Buy These 9% Yielding SWANs Instead

- 3M Could Get Cut In Half, So Buy These 8%-Yielding SWANs Instead

And now I've just learned of another potential future fallen aristocrat.

UGI Is The Next Potential Fallen Aristocrat

UGI Corporation (UGI) is a dividend legend most investors have never heard of.

This is a dividend champion (aristocrat not in the S&P) founded in 1885 that is a utility conglomerate primarily focused on Pennsylvania and America's largest propane distributor.

Its claim to fame is the dependability of the dividend, with a 35-year dividend growth streak but an even more impressive 138 years without a dividend cut.

That's right, not even in WWI, WWII, the Great Depression, a flu pandemic that killed 5% of the world, the Great Recession, the COVID Pandemic, or dozens of recessions, crises, and 20% interest rates could cause UGI to cut its dividend.

However, there are some troubling signs that management might cut the dividend in the coming months.

Following the review will also be actions to optimize the company's cost structure and re-align its capital allocation priorities." - UGI press release .

UGI has an A-rated utility business, but 40% of its revenue comes from junk bond-rated AmeriGas, the largest propane distributor in the country.

The weighted credit rating for all its business segments is BB+, and a struggling business is thus harming its cost of capital.

Natural gas is a far better heating fuel than propane in terms of cost and dependability, and the AmeriGas business is primarily in rural areas where gas lines haven't been built.

People are moving to cities over time, and while some businesses (like industrial chicken operations) will always be customers, AmeriGas is struggling with rising winter temperatures and higher driver pay that will not change for the foreseeable future.

So margins at AmeriGas are being squeezed while volumes are in decline, with no end in sight for the secular decline of the propane industry.

{kind=link}

4 analysts cover this small utility for a living, and they aren't able to agree whether UGI will keep the dividend intact.

Most think it will, but there is increased uncertainty.

Don't forget that no dividend is 100% risk-free, even those with 100% safety scores.

| Rating |

| Dividend Kings Safety Score (250 Point Safety Model) |

| Approximate Dividend Cut Risk (Average Recession) |

| Approximate Dividend Cut Risk In Pandemic Level Recession |

| 1 - unsafe |

| 0% to 20% |

| over 4% |

| 16+% |

| 2- below average |

| 21% to 40% |

| over 2% |

| 8% to 16% |

| 3 - average |

| 41% to 60% |

| 2% |

| 4% to 8% |

| 4 - safe |

| 61% to 80% |

| 1% |

| 2% to 4% |

| 5- very safe |

| 81% to 100% |

| 0.5% |

| 1% to 2% |

| UGI |

| 60% |

| 2.0% |

| 4.00% |

(Source: Dividend Kings Research Terminal.)

Our 3,000-point safety and quality model says that UGI's risk of a dividend cut has risen from 3% to 4%. That's not a high risk, but be aware of what a potential cut could mean.

What A Dividend Cut From UGI Would Mean For Investors

If UGI were to spin off AmeriGas, which is currently valued at $0 by the stock market and which it estimates is worth at least $1 billion, then its payout ratio would rise from 45% to 70%.

45% is the upper end of its target payout ratio because the propane business creates much more volatile earnings than most utilities.

Without the propane business, it's perfectly fine for management to keep the dividend intact with a 70% payout ratio in a sector where rating agencies consider 75% safe.

The issue for UGI is that this is a corporate culture and management team that's always run in the range of 40% to 45% payout ratios.

If management wants to cut the dividend, this review is the perfect opportunity.

- UGI might spin off AmeriGas and keep dividend investors whole: 30%

- UGI might spin it off and leave the dividend intact: 66%

- UGI might spin off AmeriGas and might do a stealth cut: 4% probability.

If UGI cuts the dividend, think of what that would signal.

A company that has never cut a dividend since its founding in 1885 would be saying, "things are worse than during the Great Depression."

They wouldn't be that bold and spin any cut as "unlocking value for shareholders."

But remember that short-term stock prices are vanity, cash flow is sanity, and dividends are reality. Follow the money, and you'll find the truth. And the truth is that when a dividend is cut, it's time to sell and never look back.

How To Find 8% Yielding Aristocrat Alternatives To UGI

Here is how I have used our DK Zen Research Terminal to find the best non-speculative 8% yielding dividend aristocrat alternatives to UGI.

From 504 stocks in our Master List to the best blue-chip aristocrat bargains.

All in one minute, thanks to the DK Zen Research Terminal. This is how I find all my investment ideas.

| Screening Criteria |

| Companies Remaining |

| % Of Master List |

| 1 |

| Lists "Dividend Champions" |

| 135 |

| 27.00% |

| 2 |

| BHS Rating "reasonable buy, good buy, strong buy, very strong buy, ultra value buy" |

| 100 |

| 20.00% |

| 3 |

| Non-Speculative (No Turnaround Stocks, investment grade) |

| 92 |

| 18.40% |

| 4 |

| 7.5+% dividend yield |

| 3 |

| 0.60% |

| Total Time |

| 1 minute |

Looking for the safest and most dependable names in ultra-yield? Here they are.

8% Yielding Dividend Aristocrat Bargains You Can Trust

For further research, I've linked articles about these 8% yielding aristocrats and ordered them from highest to lowest yield.

Bottom Line Up Front Fundamental Summary

- Yield: 8.3% (5X S&P 500 and 2X SCHD or VYM)

- dividend safety: 100% very safe (1% dividend cut risk)

- overall quality: 96% low-risk Ultra SWAN dividend aristocrat

- credit rating: BBB+ stable (5% 30-year bankruptcy risk)

- long-term growth consensus: 4.0%

- long-term total return potential: 12.3% vs 10.2% S&P 500

- discount to fair value: 28% discount (potential Ultra Value "fat pitch" buy) vs 8% overvaluation on S&P

- 10-year valuation boost: 3.3% annually

- 10-year consensus total return potential: 8.4% yield + 4.0% growth + 3.3% valuation boost = 15.6% vs 10.1% S&P

- 10-year consensus total return potential: = 326 % vs 164% S&P 500.

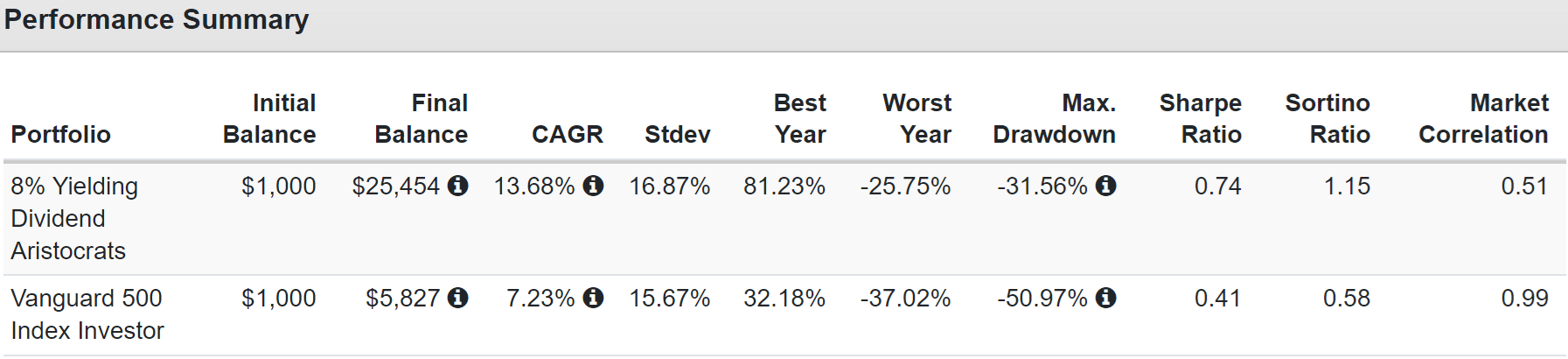

These 8% yielding aristocrats are expected to quadruple in the next decade, doubling the market's returns. And while you wait to see if that bullish consensus forecast comes true, you're locking in a very safe 8.3% yield that's growing at almost 2X the long-term inflation rate.

- 9.7% inflation-adjusted yield on cost over the next 30 years (retirement time frame)

- 9.1% average inflation-adjusted yield over the next 30 years = 273% inflation-adjusted cash return over the next 30 years

{kind=link}

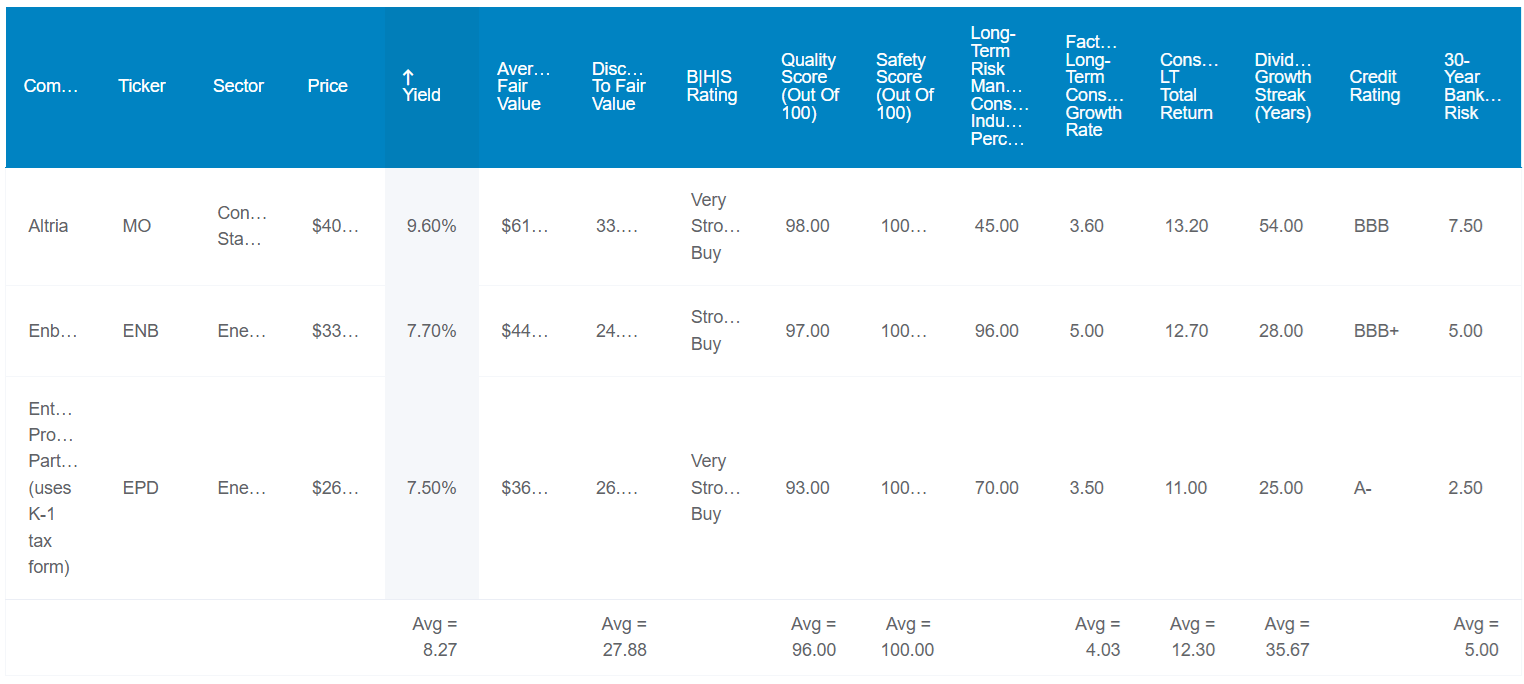

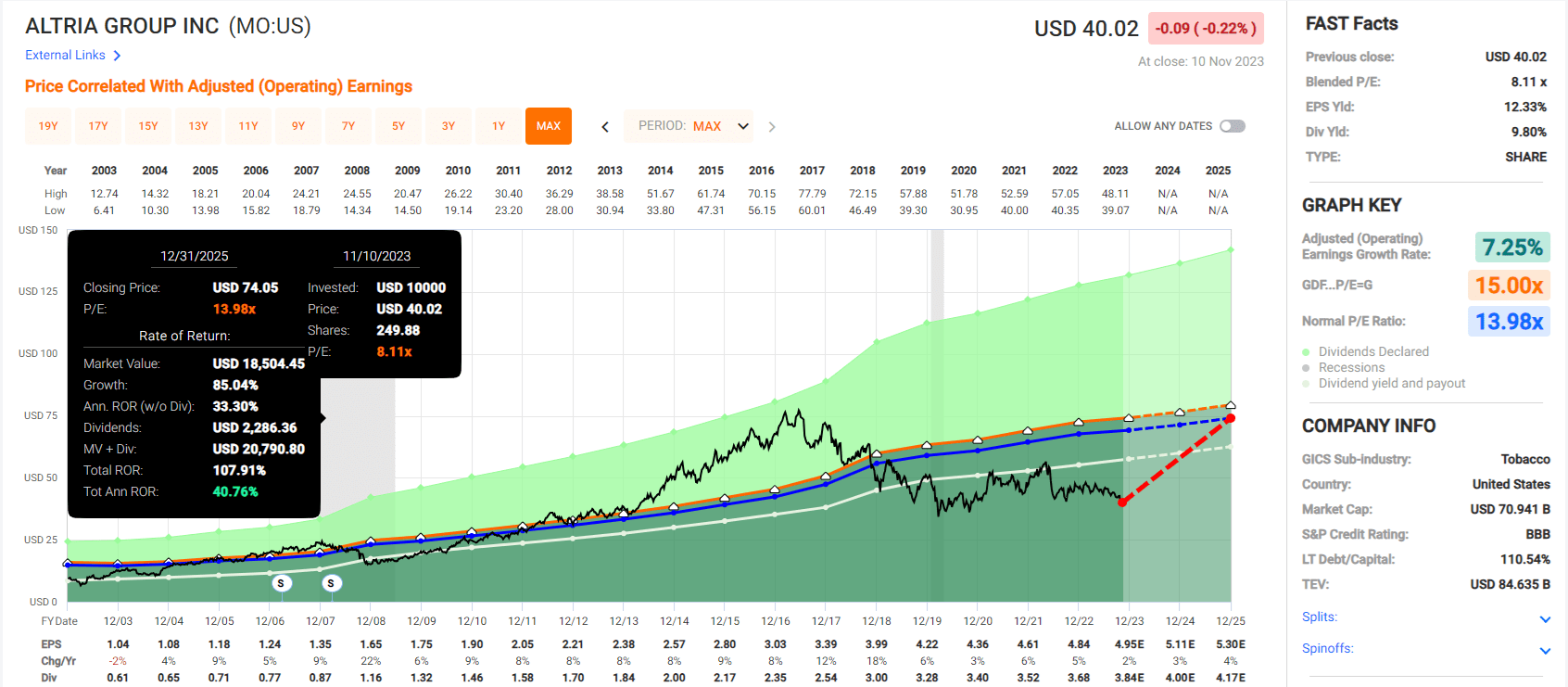

- Altria Group, Inc. ( MO )

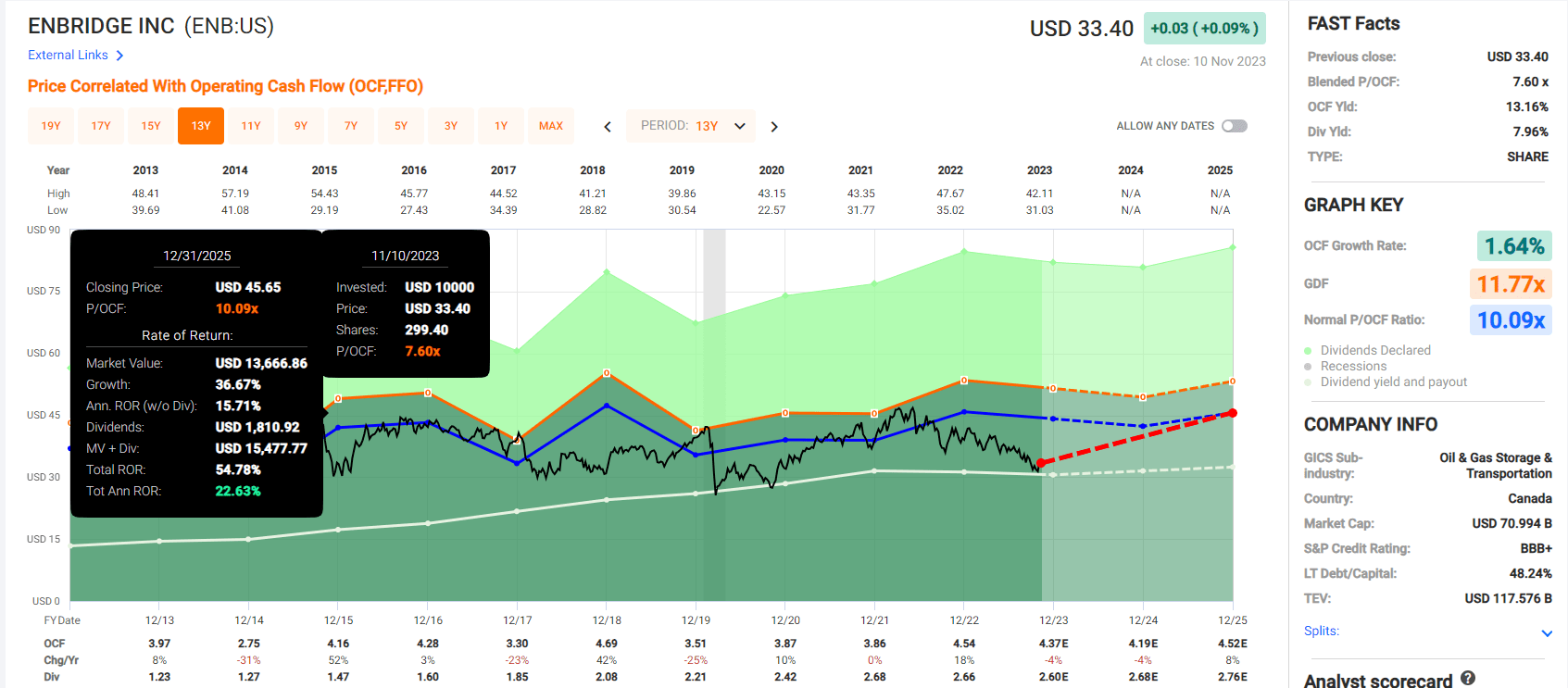

- Enbridge Inc. ( ENB ) - CA company, 15% dividend withholding EXCEPT in retirement accounts

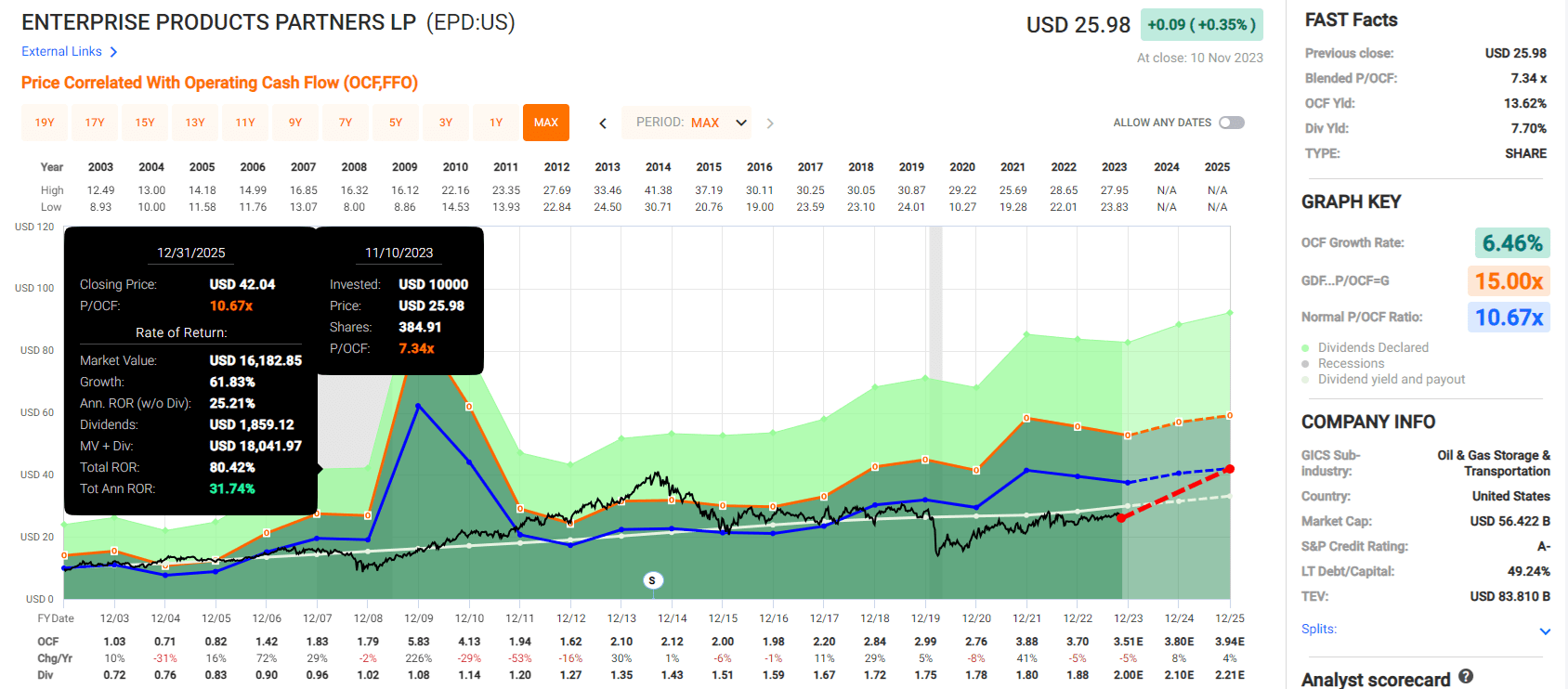

- Enterprise Products Partners L.P. ( EPD ) - K1 tax form.

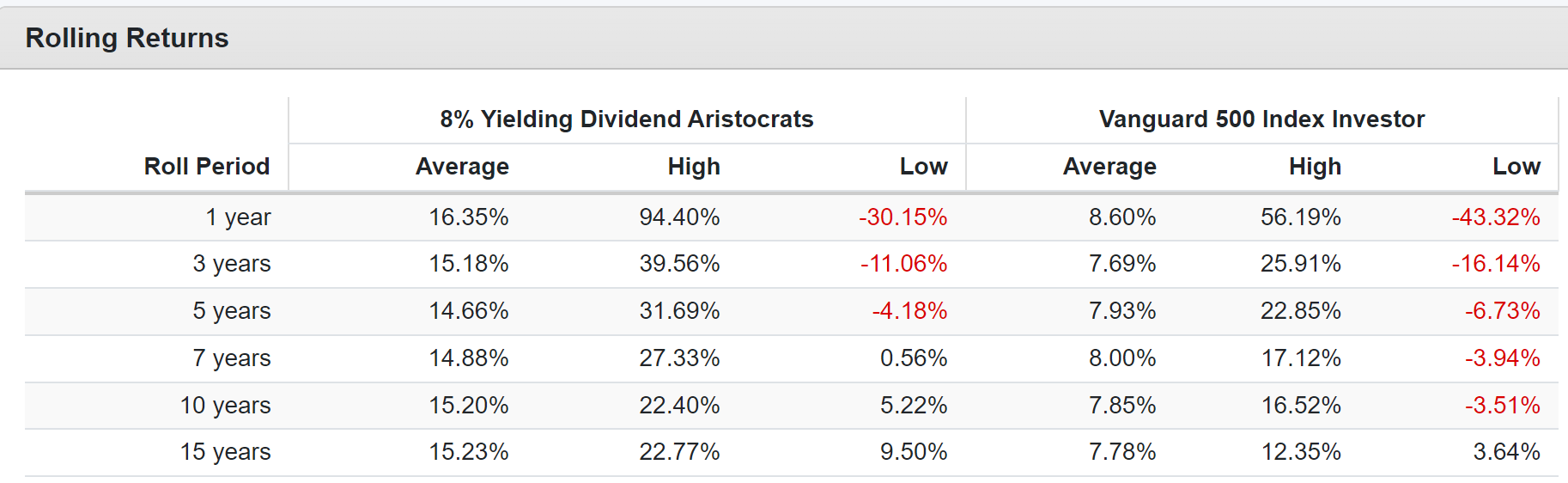

How likely are 12% to 13% future returns from these legendary dividend aristocrats?

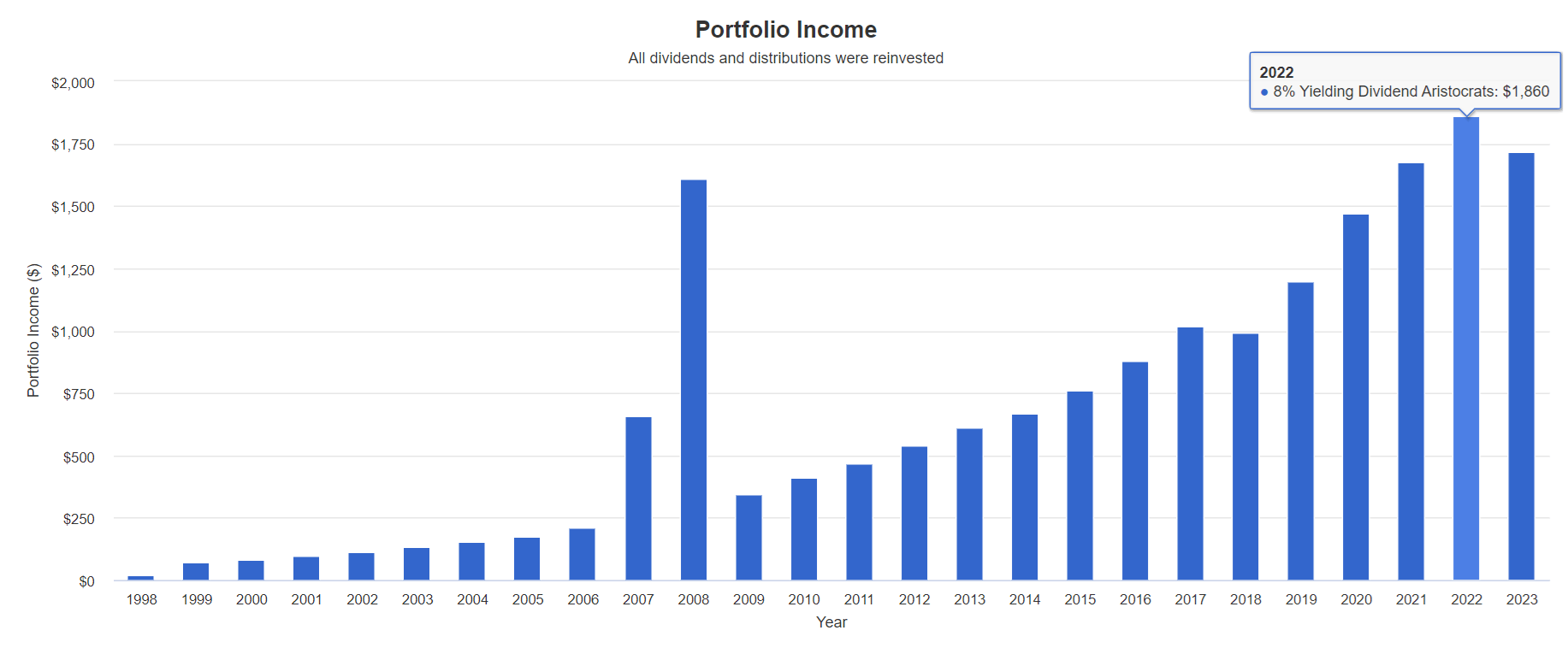

Historical Total Return Since 1998

{kind=link}

{kind=link}

{kind=link}

15.2% annual income growth for 23 years.

- 186% yield on cost if you bought in 1999

- 100% inflation-adjusted yield on cost.

Consensus Total Return Potential Through 2025

- if and only if each company grows as analysts expect

- and returns to historical market-determined fair value

- this is what you will make.

Altria

{kind=link}

Enbridge

{kind=link}

Enterprise Products Partners

{kind=link}

S&P 500

{kind=link}

Paying an 8% historical premium for the S&P 500 (SP500) is not going to lead to good things for investors in the coming 2 years. Not unless you think 12% likely returns with plenty of volatility along the way is a good return.

Or...buy these 8% yielding aristocrat bargains off 81% upside potential over 2 years and 32% annual returns.

- 8X the return potential of the S&P through 2025

Bottom Line: These 3 Dividend Aristocrats Offer The Safest 8% Yield On Wall Street

There is a 1% risk of a dividend cut for MO, ENB, and EPD, which is much lower for all of them together (less than 0.1%).

For context, Goldman estimates a 10% risk of nuclear war right now and 2.5% in any given year, even without the US and Russia in a raging proxy war.

Meanwhile, they are so undervalued and yielding such rich cash streams that they offer 8X the return potential of the S&P through 2025.

The dividends alone could beat the S&P's 2-year returns, never mind the growth and valuation boosts these coiled springs offer.

Is the market overvalued? Yup. Even without a recession, returns will likely be lackluster in the coming years.

But that doesn't mean you can't buy smart things, including alternatives to UGI, potentially the next failed aristocrat (4% risk).

Remember that short-term share prices are vanity, cash flow is sanity, but dividends are reality.

For further details see:

8% Yielding Dividend Aristocrat Bargains You Don't Want To Miss