TWLO - 8x8: Longer-Term Opportunity In A Maturing Market

2023-12-12 01:23:07 ET

Summary

- 8x8 stock has not recovered from the sell-off and is undervalued compared to the IT sector.

- The company has seen declining revenues in a maturing market where there is also tough competition from other providers.

- EGHT's share price is under pressure.

- Its more profitable growth strategy compared to Five9 deserves to be highlighted.

- This remains a long-term opportunity as the management is building up a sales team to drive more product sales.

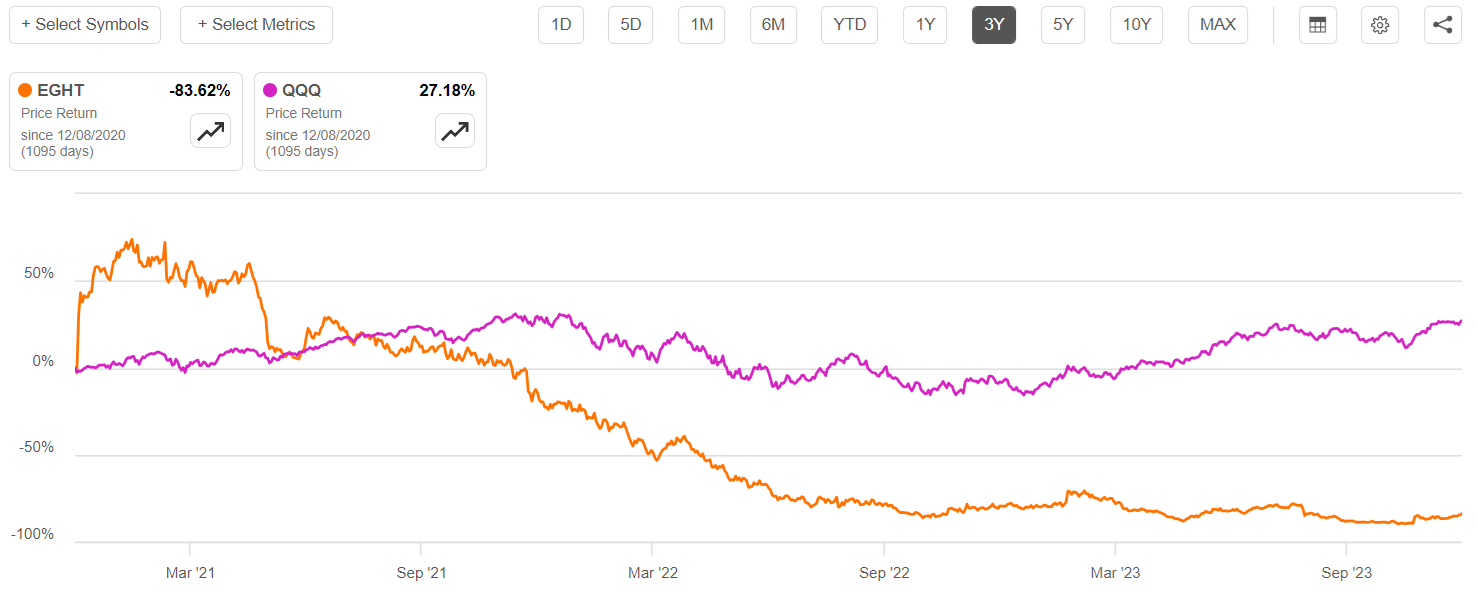

8x8 ( EGHT ) has still not recovered from the sell-off as shown in the orange chart below with its underperformance compared to the Invesco QQQ Trust ETF (NASDAQ: QQQ ) showing the extent of the damage done to its value.

Price Return (seekingalpha.com)

{kind=link}

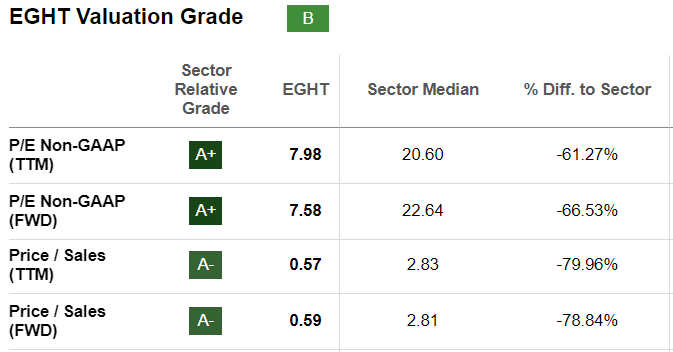

With a market cap of $438.7 million, the company operates a Unified Communications-as-a-Service (UCaaS) platform and is gradually reorienting its operations to be a contact center services provider by leveraging AI. Its trailing price to sales of 0.57x is nearly 80% undervalued relative to the median for the IT sector.

To assess whether 8x8 constitutes an opportunistic buy, this thesis will focus on how revenues and margins are faring in the maturing UCaaS market, and the opportunities lying ahead. Also, to get an industry perspective, I perform a comparison with a competitor.

Facing Revenue Stagnation in a Maturing Market

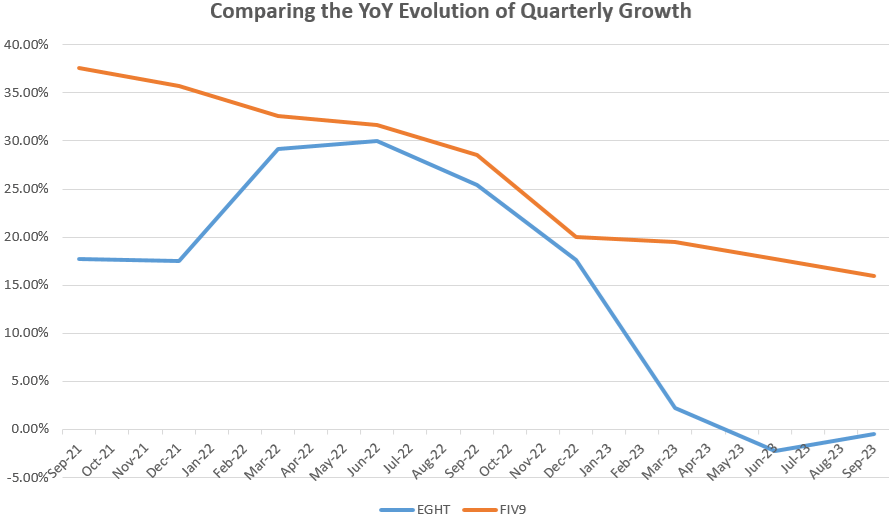

First, there have been YoY revenue declines for both the first two quarters of fiscal 2024 as shown by the blue chart plunging to below the 0.00% level and remaining under. Here, investors will notice that gone are the days when the company enjoyed double digits YoY growth of above 25% driven by the Covid-led digital transformation and remote work.

Charts built using data from (www.seekingalpha.com)

{kind=link}

Now, 8x8 provides a wide range of products ranging from cloud-based voice, chat, and video communications augmented by analytic software and even AI, but, the problem is that the market itself has matured signifying that it is not possible to rapidly gain share as before for all the players.

In response, stakeholders have been rapidly diversifying their product offerings based mostly on transforming their businesses into contact centers or CCaaS providers in an attempt to attract new clients. This involves looking for new ways to improve the customer experience itself instead of purely focusing on the technological convergence of text, voice, and video channels. However, the space is highly competitive with 8x8 pitched against companies like RingCentral ( RNG ), Zoom Technologies (ZTNO), Five9 (NASDAQ: FIVN ), Twilio ( TWLO ), and many others.

Singling out Five9, which I covered recently, it has also suffered from a post-Covid decline in sales as shown in the orange chart above but has managed to do some damage limitation as revenues continue to grow at double digits, or above 15% .

Different Growth-Margin Dynamics

Now there can be several reasons why Five9's products could be seeing more traction. One could be that it may have more innovative products that are better suited to meeting customer requirements. One way to find out is through R&D expenses as companies that spend more on research tend to be more innovative and are also the ones responding more rapidly to customer demands for innovative technologies like Generative AI.

However, it is found that it is 8x8 which has been spending more, or 18.5% to 21% of its revenues on research during the last five quarters compared to only 16.4% to 17.4% for Five9. Now, while Five9 spends more in absolute terms on R&D, this 2.85% difference in favor of 8x8 in relative terms (when considering the mid-points) shows that it dedicates a higher portion of its sales to search. As such, it has rapidly developed conversational IQ and speech analysis tools as well as APIs for integration of Open AI's whisperer for transcription and translation purposes.

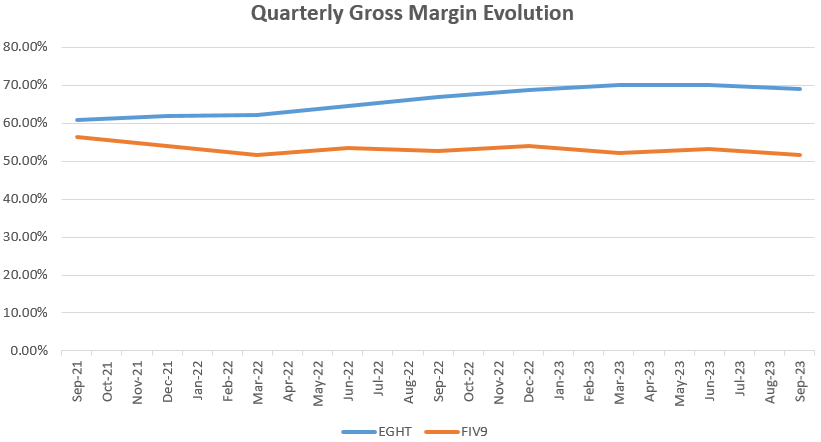

Furthermore, another reason why a company can generate more sales is by luring customers through better product pricing. For this matter, I compared the quarterly gross profit margins of the two companies as shown in the chart below.

Charts built using data from (www.seekingalpha.com)

{kind=link}

Now, gross profits are obtained by subtracting COGS or the cost of goods sold like platform hosting fees (for a typical SaaS play) from revenues. Since margins have been trending higher for 8x8 amid a maturing UCaaS market, this may signify that it has maintained its prices, in contrast with Five9 which may be charging lower as it favors higher sales.

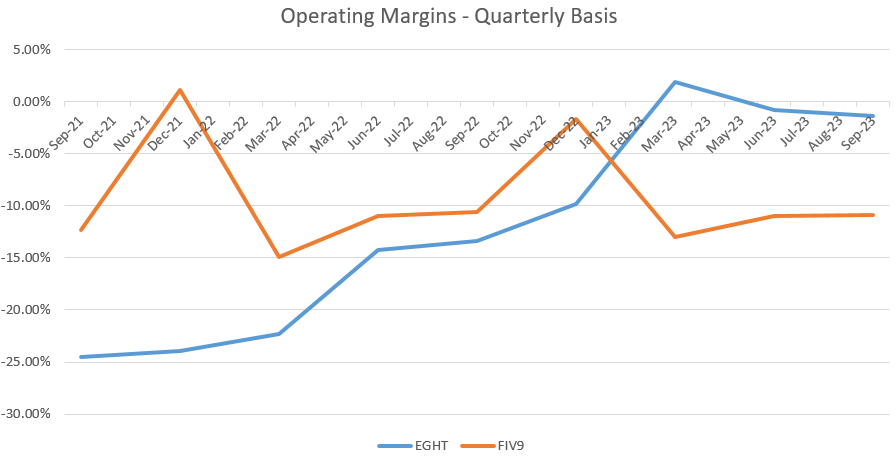

Conversely, 8x8 appears to be more geared toward profitability with this possibility confirmed by the trend in quarterly operating profit margins. First, 8x8's operating loss margin is less than for Five9 as shown in the blue chart below, and, second, while there are certainly variations on a quarter-to-quarter basis, 8x8's margins have shown a net uptrend since the September 2021 quarter.

Charts built using data from (www.seekingalpha.com)

{kind=link}

To this end, during the second quarter of fiscal 2024 (Q2) earnings call, the management emphasized its innovation-led strategy, aimed at driving growth along with improved profitability , as a balanced approach.

Discussing 8x8's Balanced Approach

Now, at a time when spending marketing dollars or even providing discounts to expand a customer base has become important especially when you are facing deep-pocketed competitors like Twilio or Zoom, one starts to wonder whether 8x8's balanced approach to growth is sustainable. For this matter, analysts expect the company to continue to see a revenue decline of 0.37% in the third quarter ending in December. Thereafter, quarterly revenue should expand at a low pace, reaching 0.87% in Q4 and 3.4% by the fourth quarter of fiscal 2024.

Therefore, with such anemic growth compared with historical trends and especially at a time when its competitor can achieve much more, it is likely for the stock price to remain under pressure. This can result in further stock downside risks, which is the reason why despite lower valuations I do not view it as a buy.

{kind=link}

Looking at the momentum, with an RSI of 72.16 , the stock is in overbought territory, and its share price is positioned above the 10-day and 50-day SMAs which tends to show an upside, probably because of investor enthusiasm in anticipation of the company being acquired. This follows unconfirmed news about RingCentral possibly being the subject of a takeover.

This said, the stock could also surge in case it delivers a revenue beat as has been the case during 7 out of 8 occasions, but this should be temporary given the number of downward revisions it has faced in the last one and a half years, unless it opts for inorganic growth. However, there may not be enough appetite for an acquisition as there is only $148.8 million in cash versus debts of $544.3 in the balance sheet, and this is after spending $250 million for Fuze in 2022. Also, $12.9 million had to be paid as cash interest to service debt for Q2 alone. Therefore, because of the lack of a growth narrative, this is not a stock to buy.

Moreover, the Fuze acquisition, while enabling 8x8 to increase its enterprise customer base, has not helped, neither to boost sales as anticipated nor to more rapidly make the company become a $1 billion revenue business . The reason has mostly to do with the inability to retain customers using Fuze products, possibly because they are required to be migrated to 8x8's platform. Noteworthily, attrition linked to Fuze has induced headwinds both in the enterprise ARR metric and customer count. As a result, total ARR of $707 million grew only by 2% YoY.

Therefore, still digesting the $250 million acquisition, and not boasting a cash-rich balance sheet, 8x8 does not have many options to grow revenues rapidly.

A Longer-Term Opportunity

On the other hand, I believe there are opportunities beyond 2024, and, this time thanks to organic growth. In this regard, aware that many potential customers may not be knowledgeable about the company's innovative products, the management is focusing on creating both customer and partner awareness. The related action plan will be carried out by the newly recruited CRO and CMO, both experienced in building sales & marketing teams for contact centers. This should help in more rapidly translating 8x8's sales pipeline into revenues.

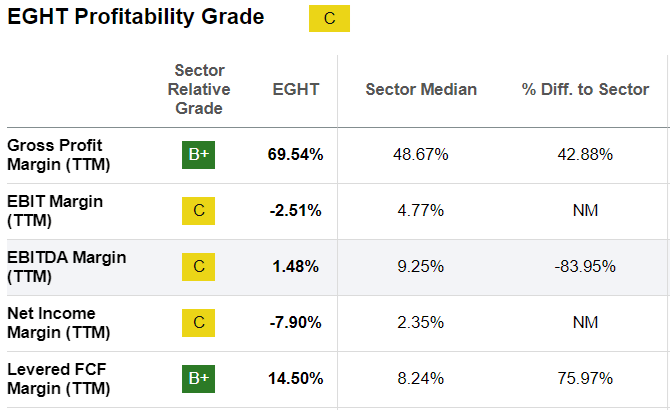

However, the recruitment of additional personnel especially during a period of relatively higher wage inflation entails that operating expenses may go up, in turn impacting margins for this loss-making company (on a GAAP basis). In this respect, non-GAAP operating profits in Q2 were $23.8 million, or a 160% YoY increase. Well, this is a highly commendable figure and certainly shows that the management is abiding by the profitability mandate, but, non-GAAP figures do not enable a like-to-like comparison with peers. Consequently, sticking with GAAP figures, 8x8 still scores a " C " relative to the IT sector as shown below, helped by superior gross margins and levered FCF margins.

{kind=link}

According to me, while growth should take time to pick up, it is on the profitability front that 8x8 should make rapid progress thanks to two factors. First, its multiple-product sales strategy could offset some of the increase in additional employee-related expenses. This involves the sales team aiming to sell eight products (UC, CC, ICA Digital, ICA Voice, Workforce Management, CPaaS, SecurePay, and professional services) at a time, instead of one. Interestingly, this means more upselling opportunities to the same customer instead of spending more marketing dollars to sell one product to eight different customers. This can result in better ARPU and should be more profitable growth.

Second, there are more cross-selling opportunities as a result of Fuze customers being migrated to 8x8's platform. In this way, they are likely to consume other services facilitated by its cloud-based subscription approach, which most corporations are looking for to avoid making big capital expenses, especially in a period where the cost of doing business remains elevated. As per the executives , they have already started to see such opportunities.

In conclusion, this thesis has shown that 8x8's response to the maturing market has been to shift from a UCaaS-led to a contact center-led business while emphasizing portfolio sales instead of selling a single product. This way of proceeding is proving beneficial to the cash flow with the amount of dollars generated from operations more than doubling in Q2 on a YoY basis. However, this approach does not allow for sales to grow rapidly in the short term which is the reason for the Hold position.

For further details see:

8x8: Longer-Term Opportunity In A Maturing Market