XOM - A Big Move By Occidental Petroleum Should Boost Cash Flows For Shareholders

2023-12-13 09:14:37 ET

Summary

- Occidental Petroleum has entered into an agreement to acquire CrownRock in a $12 billion deal, boosting overall profitability and allowing for a significant increase in distribution.

- The acquisition is part of a trend of major movements in the energy market, with other companies making large deals in the Permian basin.

- Occidental Petroleum plans to finance the purchase with $9.1 billion of new debt and aims to reduce debt through asset sales and cash flow in the first 18 months following the transaction.

December 11 ended up being a very interesting day for shareholders of energy giant Occidental Petroleum ( OXY ). Shares of the company closed up about 1% after news broke that the company entered into an agreement to acquire privately owned CrownRock in a deal valued at $12 billion. According to management, this liquids-heavy transaction brings on significant amounts of resources that have low break-even prices. Even without synergies, the anticipated free cash flows associated with this deal will help to boost overall profitability for the company as a whole and have allowed it to confidently raise its distribution rather meaningfully. While debt will initially be higher, the extra free cash flows generated by the business, combined with a major asset divestiture program that has now been launched by management, will help to bring this under control in relatively short order. Based on what terms are available at this time, this deal does make sense for shareholders and it's logical for investors to be optimistic at this time.

Another mega-deal in the Permian

This year has, in many respects, been defined by some rather major movements in the energy markets. In July of this year, for instance, Exxon Mobil ( XOM ) announced that it was acquiring Denbury ( DEN ) for $4.9 billion. This transaction was dwarfed by the one that Exxon Mobil announced in October for Pioneer Natural Resources ( PXD ) in exchange for $59.5 billion. But Exxon Mobil hasn't been the only company moving in this market. In May of this year, for instance, Chevron ( CVX ) stated that it was acquiring PDC Energy for $7.6 billion. And in October, Chevron decided to acquire Hess Corporation ( HES ) for $53 billion. And there have been rumors recently that privately held Endeavor Energy Partners might be pushing to sell as much as $30 billion worth of assets that it owns. But nothing concrete has been decided on that front.

With all of this activity going on, one of the earliest signs that something might be occurring with Occidental Petroleum came about late last month when, on November 27, a private jet owned by Occidental Petroleum flew into Eppley Airfield in Omaha, Nebraska, where it remained grounded for approximately three hours. This is noteworthy because Warren Buffett controlled Berkshire Hathaway ( BRK.A ) ( BRK.B ) currently owns about 25.4% of all basic shares outstanding of Occidental Petroleum, with that number reducing to about 23.3% if we look at it through the lens of diluted shares. In addition to having this stake valued at about $12.8 billion, Berkshire Hathaway owns just under $8.5 billion worth (face value) of preferred units that should have a liquidation preference of around $8.9 billion.

Even though the preferred ownership that Berkshire Hathaway has in Occidental Petroleum has declined by about $1.5 billion this year because of mandatory redemptions triggered by common share buybacks that Occidental Petroleum has engaged in, the common ownership interest is at an all-time high, reflecting the optimism that Mr. Buffett has in the company. Frankly, that meeting could have been over anything. But it would be absurd to make such a large transaction without confronting such a significant shareholder. This does seem to fly in the face of indications from the third quarter of this year when, in its earnings call, Occidental Petroleum, through its CEO Vicki Holub, stated that it did not need to make any big deals. But clearly, competitive pressures and the attractiveness of certain opportunities out there ultimately prevailed.

An interesting purchase

{kind=link}

Occidental Petroleum

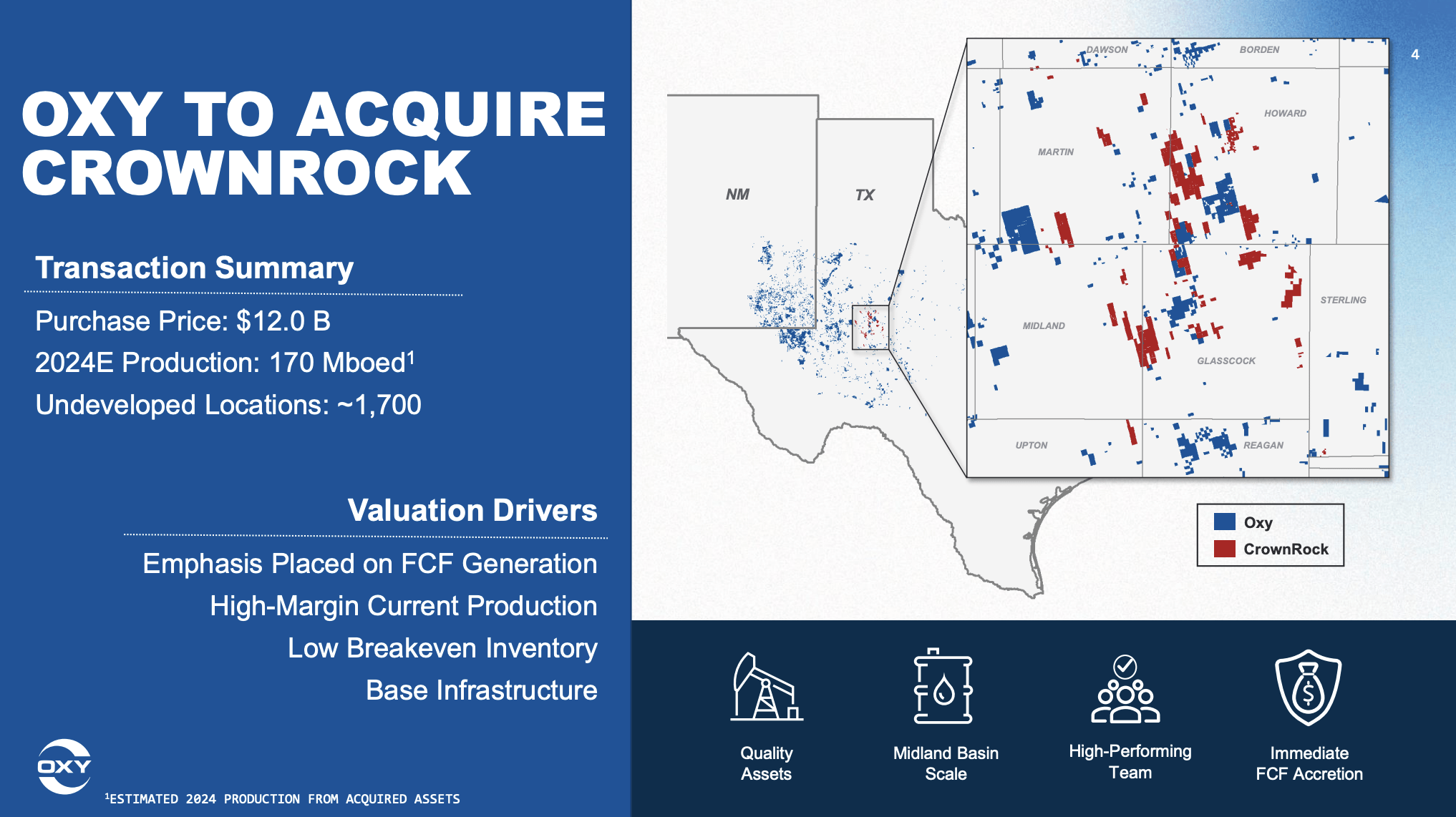

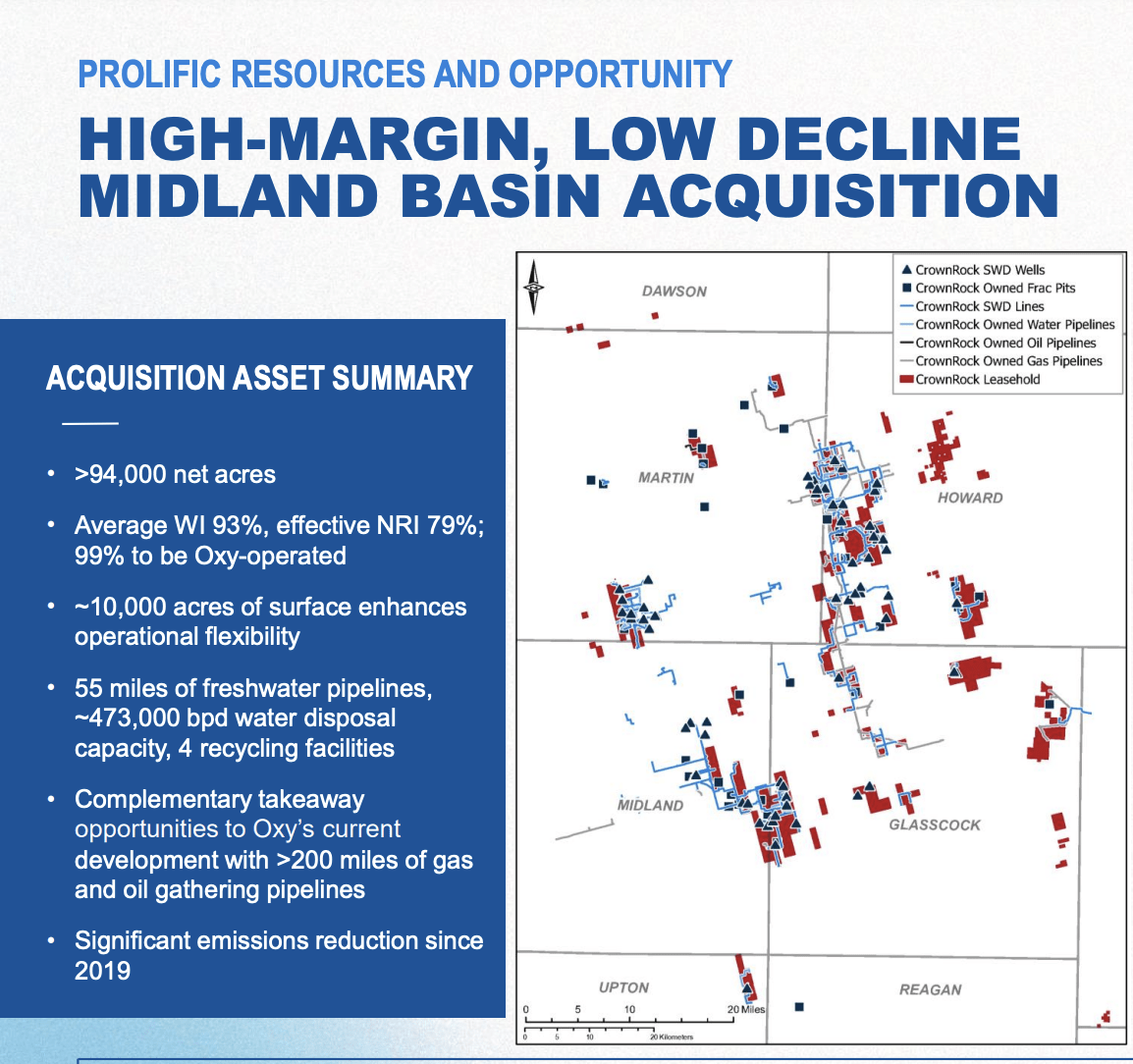

According to the management team at Occidental Petroleum, the company has agreed to acquire privately owned CrownRock in a deal valued at $12 billion. This is a rather significant transaction, bringing over assets to Occidental Petroleum that consist of 1,700 undeveloped locations, 1,250 of which are development ready. The current developed assets are estimated to result in 170,000 boe (barrels of oil equivalent) worth of output per day, about 80% of which is in the form of liquids. All of this is spread across approximately 94,000 net acres of land that, as the image above illustrates, shares close proximity to land currently owned by Occidental Petroleum.

{kind=link}

Occidental Petroleum

In addition to energy producing assets, this purchase brings with it 55 miles of freshwater pipelines that have around 473,000 barrels per day worth of water disposal capacity. Included with that would be four recycling facilities and take away opportunities associated with over 200 miles of gas and oil gathering pipelines that Occidental Petroleum currently owns. Management claims that these assets have a low breakeven point, with prices for WTI crude less than $60 per barrel sufficient to keep shareholders from losing money. All combined, this move will actually increase Occidental Petroleum’s sub-$40 breakeven energy inventories by 33% because of the fact that an estimated 750 of the 1,250 development ready locations are believed to have break even points of less than $40 per barrel.

{kind=link}

Occidental Petroleum

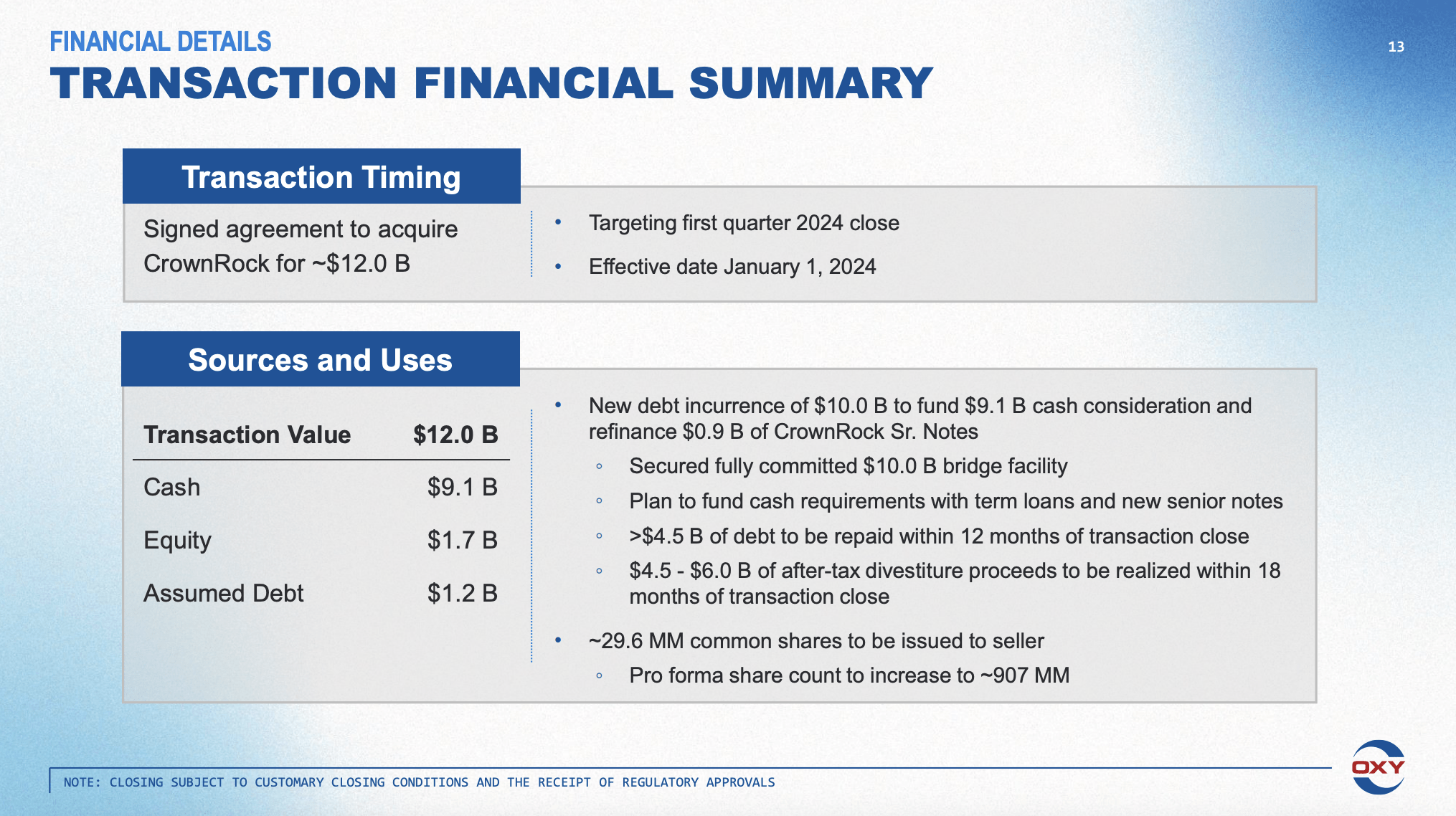

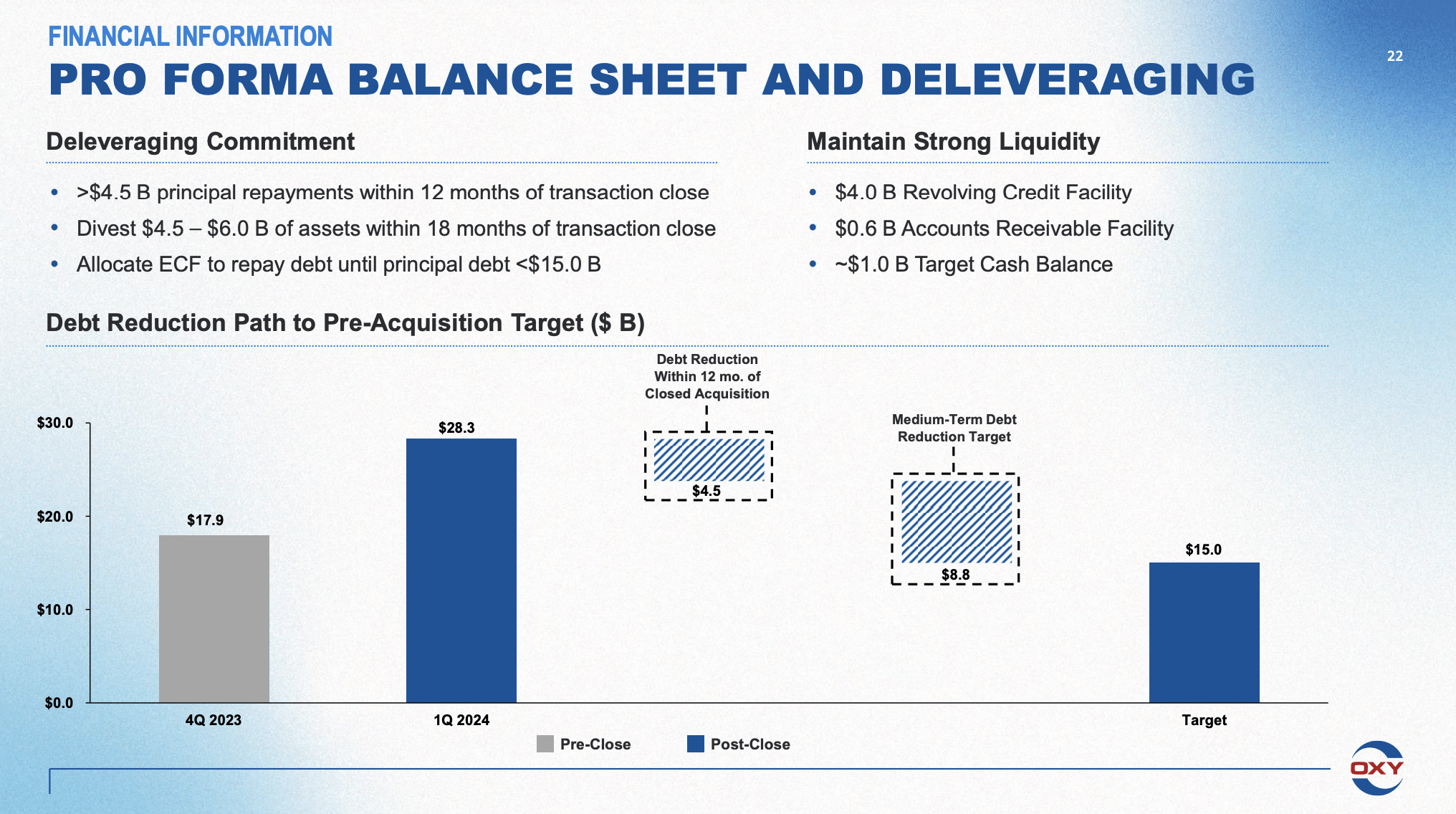

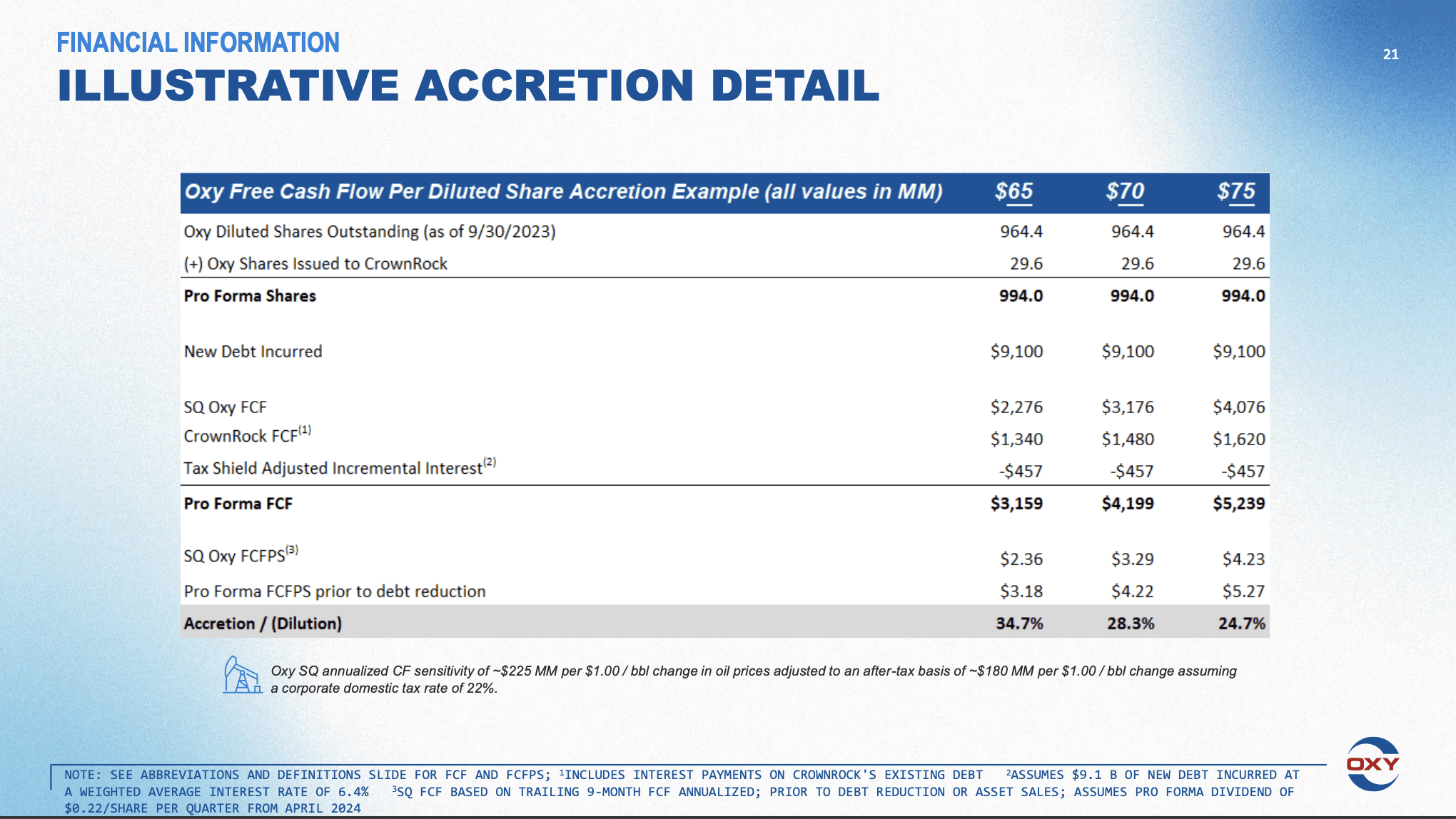

Management has said that they intend to finance this purchase by bringing on $9.1 billion of new debt. The company is also absorbing $1.2 billion of existing debt that CrownRock currently has on its books. That brings the purchase price up to $10.3 billion. The deal will also include the issuance of another $1.7 billion of common shares, increasing the company's share count by 29.6 million up to 907 million on a basic basis and 994 million on a fully diluted basis. Many investors might take issue with this. However, management intends to significantly reduce debt during the first 12 months following the closure of this transaction. You see, as of the end of the 2023 fiscal year, Occidental Petroleum believes that it will have about $17.9 billion in debt on its books. This would increase to $28.3 billion in the first quarter of the year when the deal closes. Having said that, management plans to launch an asset sale program that it expects to bring in between $4.5 billion and $6 billion. When you add on top of this additional initiatives such as the ability to use extra cash flows to reduce debt, the firm believes that it can bring total debt down to $15 billion in about 18 months following the completion of the transaction.

{kind=link}

Occidental Petroleum

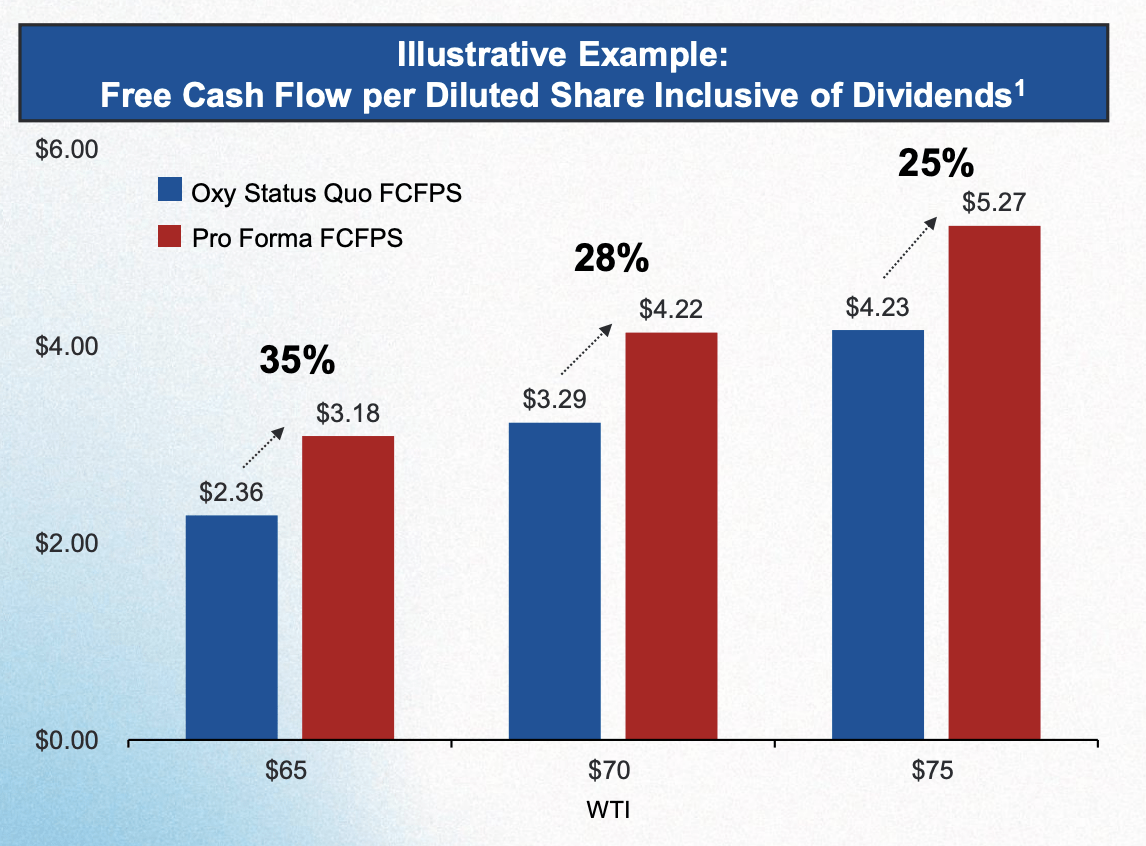

Speaking of cash flow, the current expectation Is for these new assets to add on around $1 billion of free cash flow to the company on an annualized basis. Personally, I don't like using free cash flow as the only metric of profitability because it is so easily manipulated. Companies that are investing heavily in growth initiatives are punished from a free cash flow perspective, while those that aren't growing might look more appealing when they aren't. But we have to work with what we're given. This free cash flow expectation assumes WTI crude of $70 per barrel. However, management was kind enough to give us some additional data in order to evaluate this transaction. For instance, even though the company’s share count is expected to rise because of this transaction, the extra cash flow coming on board should result in free cash flow per share of $4.22 if we assume that oil prices average $70 per barrel. That's up from the $3.29 per share if the transaction is not done.

{kind=link}

Occidental Petroleum

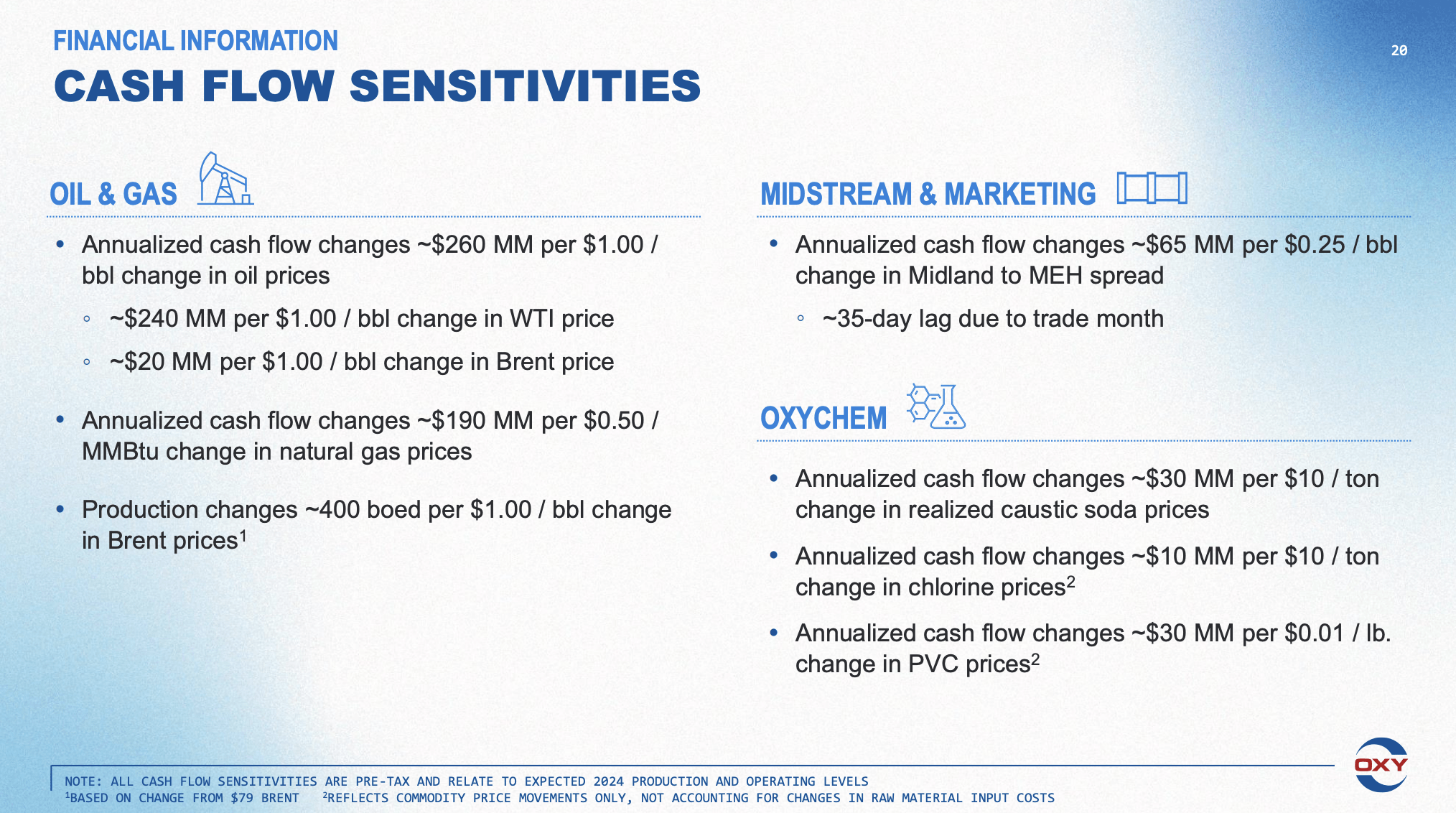

Naturally, this will also fluctuate based on energy prices. Management did offer up some cash flow sensitivity data to show, for instance, that a $1 change in the price of oil for both WTI crude and Brent crude would change annualized free cash flow to the tune of $260 million. There are also other estimates for natural gas and other important metrics. If we use management’s base forecast for this, and we assume $70 per barrel for WTI crude, then the company, on a pro forma basis, should be trading at 12.2 times free cash flow.

{kind=link}

Occidental Petroleum

That's actually down from the 15.6 times that the company is trading at otherwise, with much of the benefit in between driven by a rather hefty tax shield associated with the interest paid on the debt it is accruing for this acquisition. This massive improvement has also allowed management to increase the dividend by 22% to $0.22 per share from $0.18 per share. Although this may not sound like much, this translates to an extra $166.5 million in cash that the company is distributing to its common shareholders each year. Although not terribly material for Berkshire Hathaway, it will be an extra $35.9 million that the company will receive in the form of distributions per annum.

{kind=link}

Occidental Petroleum

Takeaway

Based on the data provided, I must say that I am, conceptually speaking, in favor of this transaction. If the numbers are as attractive as management has laid out, the purchase makes Occidental Petroleum look even cheaper than it would be otherwise. It is a deal that is highly accretive to the company from a cash flow basis and the growth in the distribution and free cash flow per share is undeniably appealing. What’s really awesome to point out is that this transaction assumes no material synergies are realized from the combination. If any synergies do come about, which I think would be fairly likely, it could make the picture even more appealing than it currently is.

For further details see:

A Big Move By Occidental Petroleum Should Boost Cash Flows For Shareholders