APD - A REIT Vs. A Dividend Aristocrat: One Is A Good Buy The Other A Goodbye

2024-01-18 00:18:33 ET

Summary

- Easterly Government Properties is a high-yield REIT with a stable revenue stream backed by long-term leases with the U.S. Government.

- DEA's dividend growth rate is low and there are concerns about its sustainability, making it a sell.

- Air Products and Chemicals is a global producer of industrial gases with a strong history of dividend growth and positive financial performance.

REITs and Dividend Aristocrats are often the focus of investors' interest. This is particularly true when a company offers a high-yield or a well-respected stock trades near a 52-week low.

With a yield approaching 8%, and nearly its entire portfolio of properties on long-term leases, it is understandable that the REIT highlighted in this article might attract one's eye.

The same holds true of the Dividend Aristocrat I review in this piece. After all, there is ample data showing that collectively, Aristocrats tend to outperform the market over the long haul while also offering reliable dividends.

Add to that an opportunity to acquire one near a 52-week low, and it piques my interest.

However, the developments outlined in this article led me to leave one of these investments on the table and had me initiate a position in the other.

First Up Easterly Government Properties

As its name implies, Easterly Government Properties ( DEA ) is an office REIT specializing in Class A properties leased to the U.S. Government. A micro-cap with 90 properties to its name, the REIT leases to 40 government agencies, with a focus on mission-critical government-leased assets.

DEA's top three tenants are the Veterans Administration, the FBI, and the Drug Enforcement Agency.

DEA investor presentation

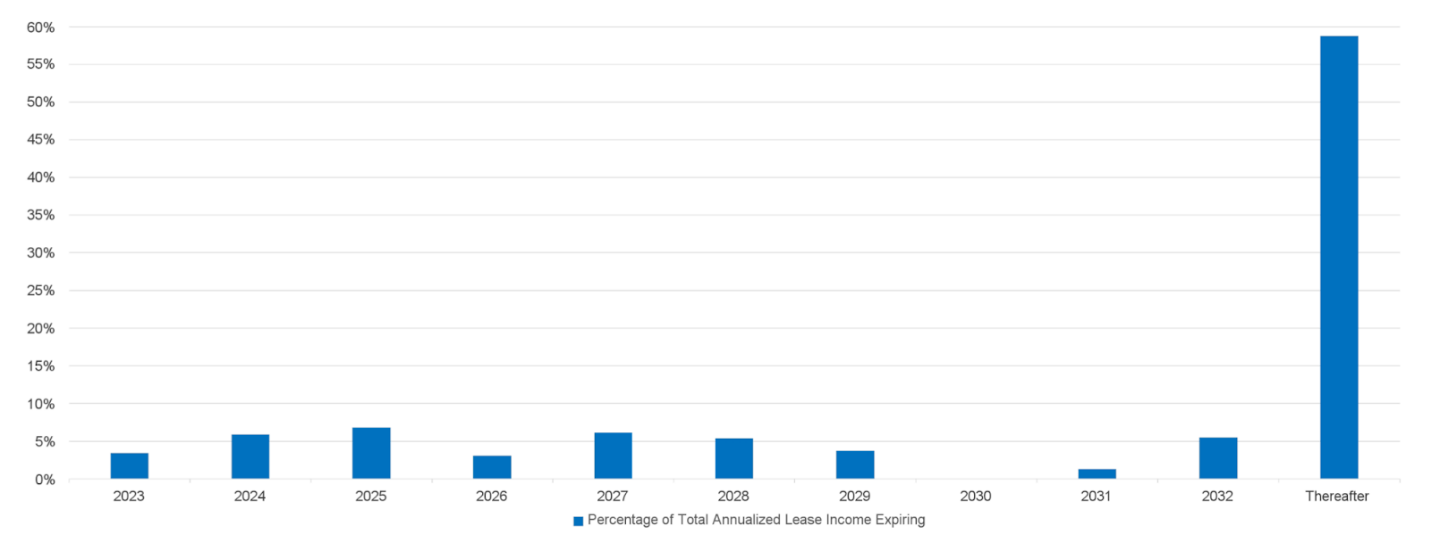

There are several strong positives to consider when evaluating DEA as a prospective investment: 99% of its lease income is backed by the full faith and credit of the U.S. Government, and at the end of the last quarter, 97.5% of DEA's properties were leased with a weighted average lease term of 10.4 years.

This results in a stable revenue stream that is fairly easy to forecast.

The following excerpt from the latest earnings call, describing a recently acquired property that is leased to the federal government, provides an example of the mission-specific nature of many of DEA's properties.

Given the highly sensitive operations housed within the courthouse, the facilities constructed according to the specific requirements of the U.S. Courts and the United States Marshals Service, meaning strict Federal building and security standards, including isolated prisoner movement, a 50-foot perimeter of security setback, progressive collapse construction and blast-resistant exteriors.

Additionally, the company has a reasonable debt load. Last quarter, DEA repaid all of the firm's borrowings under its $450 million revolver credit line. Also, in this high interest rate environment, DEA carries no floating rate debt on its balance sheet.

Less than a week ago, the Kroll Bond Rating Agency rated DEA's credit as BBB/stable (Kroll uses the same rating scale as S&P).

{kind=link}

However, not all are peaches and cream with DEA. While it is true that the company benefits from holding unique assets, that is in itself a two-edged sword.

For example, the property described in the earnings report is not one that most prospective tenants could use. Consequently, this provides bargaining leverage for the federal government when renegotiating expired leases.

Furthermore, the work-from-home trend could provide a headwind for DEA.

Although investors should weigh those negatives, my chief concerns lie elsewhere.

In the second quarter following its 2015 IPO, the REIT paid a dividend of $0.21 a quarter. Roughly nine years later, the dividend is $0.265 a quarter, which represents a rather low rate of growth. Furthermore, the dividend hasn't been increased since the middle of August 2021.

While that payout provides a current yield of 7.86%, the firm's 5-year dividend growth rate stands at an anemic 0.38%.

Count me as a guy who finds big yields attractive, but they must have at minimum a low single-digit percentage annual dividend growth rate to warrant my interest.

Far worse is the following.

During the last earnings call, analysts posed this question:

...I'm curious if you can just comment on the dividend. I mean I know the payout ratio still remains elevated. How should we think about that maybe on a go-forward basis?

And here is the response.

It's certainly our experience that our leases provide unique forward-planning capabilities. We can look out further than the typical -- certainly the typical office REIT today. We're really at a place today a real opportunity, as Darrell and Bill indicated, and growth can be accretive.

Furthermore, our reliabilities are not repricing tomorrow with the swaps we put in place earlier this year. So we're very soon to this issue. We'll stay focused on what's best for shareholders, but that's the backdrop today.

A similar question posed by another analyst elicited an equally ambiguous answer.

Nowhere in management's response was there any assurance that the dividend would remain intact or that the company planned to increase the payout.

As one who has perused scores of earnings calls wherein an analyst posed a question regarding a company's dividend, I can state unequivocally that the near-universal response is to "talk up" the dividend.

From my perspective, management's replies present a red flag.

Of course, a pair of questions and answers on an earnings call are not proof that DEA's dividend is under duress. It does, however, leave me with troubling questions. And digging a bit deeper, I believe my concerns are well founded.

Since 2016, the REIT recorded a negative AFFO growth rate, and analyst's consensus growth rate over the next two years is now -1.59%.

Over the trailing twelve months, DEA has a dividend payout ratio of over 320%, an AFFO payout ratio of just over 113%, and a forward AFFO payout ratio of nearly 108%.

These metrics indicate that a cut in the dividend is possible.

A best-case scenario is that there will be no dividend increases in the foreseeable future and that management will have to curtail growth to support dividend payments.

Weighing the above, I rate DEA as a SELL .

Air Products and Chemicals

With 750 production facilities in 50 countries, Air Products and Chemicals ( APD ) serves over 30 industries. One of the largest global producers of industrial gasses, APD products include oxygen, nitrogen, and argon and process gasses such as hydrogen, carbon monoxide, helium, syngas, and specialty gasses.

A truncated enumeration of the businesses that depend on APD's products includes Aerospace, Automotive, Beverages, Electronics, Food, Medical, Metals and Oil and Gas Production, Pharmaceuticals, Power, Pulp, Paper, Rubber and Plastics, and Water and Wastewater industries.

{kind=link}

While it is true that APD's products are generally commodities, they are absolutely essential to the company's customers and constitute a relatively small fraction of total costs. This means businesses are willing to pay premium prices to ensure needed supplies from a reliable producer.

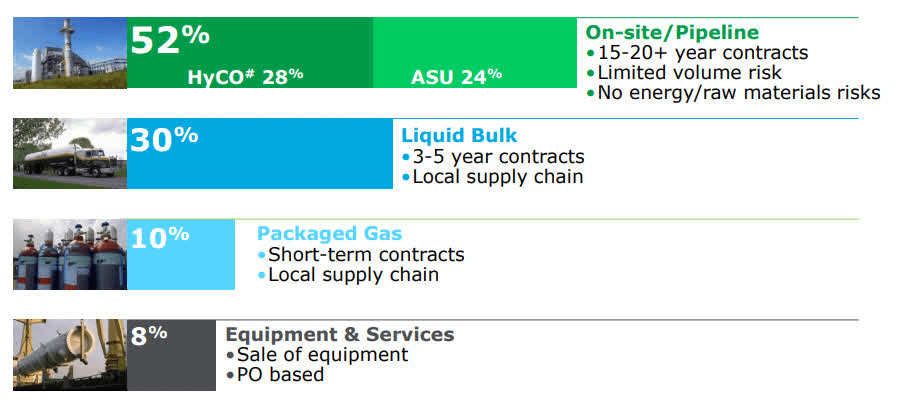

It is also common for industrial gas companies to build plants adjacent to customers' production facilities. Furthermore, prior to building these plants, customers are required to enter into long-term contracts.

Consequently, customers with APD production facilities built on-site contributed approximately 50% of 2022 revenue.

That also means that to switch suppliers, a rival must build a similar plant or pipeline to provide essentially the same products. This dynamic means switching costs can be exorbitant should a client opt to change suppliers.

This results in APD recording customer retention rates that are over 95%.

Additionally, APD is the world's largest supplier of hydrogen and has $19 billion devoted to hydrogen megaprojects in its pipeline.

MarketsAndMarkets forecasts a CAGR for the hydrogen generation market of 10.2% from 2023 to 2028.

And unlike DEA, Air Products and Chemicals has a stellar history of dividend growth.

APD Presentation

With a current yield of 2.65%, a payout ratio of just under 60%, and a 5-year dividend growth rate of 9.73%, APD has a safe dividend that is likely to grow for the foreseeable future.

APD's debt is rated A2/stable by Moody's and A/stable by Standard & Poor's.

The forward P/E of 20.31x compares well to the 5-year average P/E of 28.53x, and the current 5-year PEG of 1.78x is well below the average PEG ratio for the stock over the last 5 years of 2.56x.

Those metrics, coupled with analysts' consensus price target of $307.86 indicate the stock is likely undervalued.

Summation

As outlined in this piece, at best I see stagnant growth for DEA for the foreseeable future. A worst-case scenario includes a possible dividend cut.

While DEA's 7%-plus dividend may seem enticing, there are a number of stocks with dividends at or near a 7% yield that I believe are better investments.

In contrast, despite the recent drop in share price, APD is not stuck in neutral, let alone a company in a state of decline.

Full fiscal year 2023 results recorded adjusted EPS up 12%, EBITDA increasing by 11%, operating income up 14%, and net income growing by 12%.

In Q4, APD posted the 8th highest EBITDA in the last forty quarters and the 2nd highest EBITDA over the last three fiscal years.

Management guides for Q1 adjusted EPS to be up 10% to 16% over last year and for adjusted EPS in FY 2024 in a range of $12.80 to $13.10, a 13% year-over-year increase at the midpoint.

With this Dividend Aristocrat trading near its 52-week low, I initiated an investment in the stock about a month ago and intend to add substantially to my position towards this month's end, as funds become available.

For further details see:

A REIT Vs. A Dividend Aristocrat: One Is A Good Buy, The Other A Goodbye