TSCO - A Simple Metric To Help Avoid Walmart-Like Stocks In Your Portfolio

- Walmart recently announced disappointing guidance, and its stock has dramatically underperformed the market for over a decade.

- I'm always surprised when I see stocks like Walmart trading at high valuations when there is no rational reason for it.

- In this article, I explore what might cause such high valuation, and I share some very simple metrics that can help retail investors avoid chronic underperformers like Walmart.

Introduction

Walmart ( WMT ) recently announced disappointing guidance that immediately sent the stock price down about -8%. But that is hardly the worst of it for Walmart shareholders. The worst part is that Walmart is likely dead money for years to come for medium and long-term stock investors, just as it has been for many years now. In this article, I'm going to share some basic techniques and metrics that will help long-term retail investors avoid stocks like Walmart and help them achieve better returns.

I always like to begin my articles by reviewing the results of any coverage I've had of a stock in the past. I've only written one previous article on Walmart stock, which was back on November 19th of 2019 titled " Walmart: A 10-Year Full-Cycle Analysis ". In that article, I labeled Walmart as a "Strong Sell" or, "Very Bearish". Here is how Walmart stock has performed since then.

Walmart's severe underperformance was entirely predictable given its fundamentals back in late 2019. But what is remarkable, and remains actionable for investors today is that Walmart stock is still overvalued and likely to produce poor returns in the future.

Walmart's recent underperformance is nothing new. During a decade that included one of the stock market's best bull market runs ever, Walmart returned less than half of what the S&P 500 index returned.

In this article, I want to review and explain in more depth some of the most basic investing principles that I use to value stocks like Walmart with the hope that other investors can use them as well and improve their returns.

Reputation and brand recognition are not sufficient reasons to buy a stock

One thing that continuously boggles my mind is why investors would pay as much money as they have been paying for a slow-growth business like Walmart. The only conclusion that I can come to is that people recognize the brand, they know Walmart has been successful in the past, and it's hard for them to imagine anything seriously damaging happening to the business in the near term. That makes them feel comfortable owning the stock, and so they just ignore the valuation.

Let me explain why this is the wrong way to invest in stocks if an investor wants good returns, but before I do, I want to make a few things clear at the outset. The first is I think Walmart offers a valuable service to consumers, and I am a long-time customer (mostly of Sam's Club). I spend over $10k a year at Walmart and Sam's. I don't have any sort of ax to grind with Walmart. But being a customer of a store and being a passive owner of a store are two very different things. As a potential owner, I need to pay a price for the business that is justified by the likely return on that investment.

So what is the easiest way to think about our likely return on investment?

The way I think about it is if I bought the whole business for $100, how much money would I make from the earnings of that business over the next 10 years? In other words, if I put $100 in, how much do I have 10 years later if I keep all the earnings from the business for myself.

The simplest way to estimate this is to look at the earnings yield, which is the inverted P/E ratio, or E/P. The way to think about the earnings yield is to think about it just like the dividend yield, only, with earnings instead of dividends.

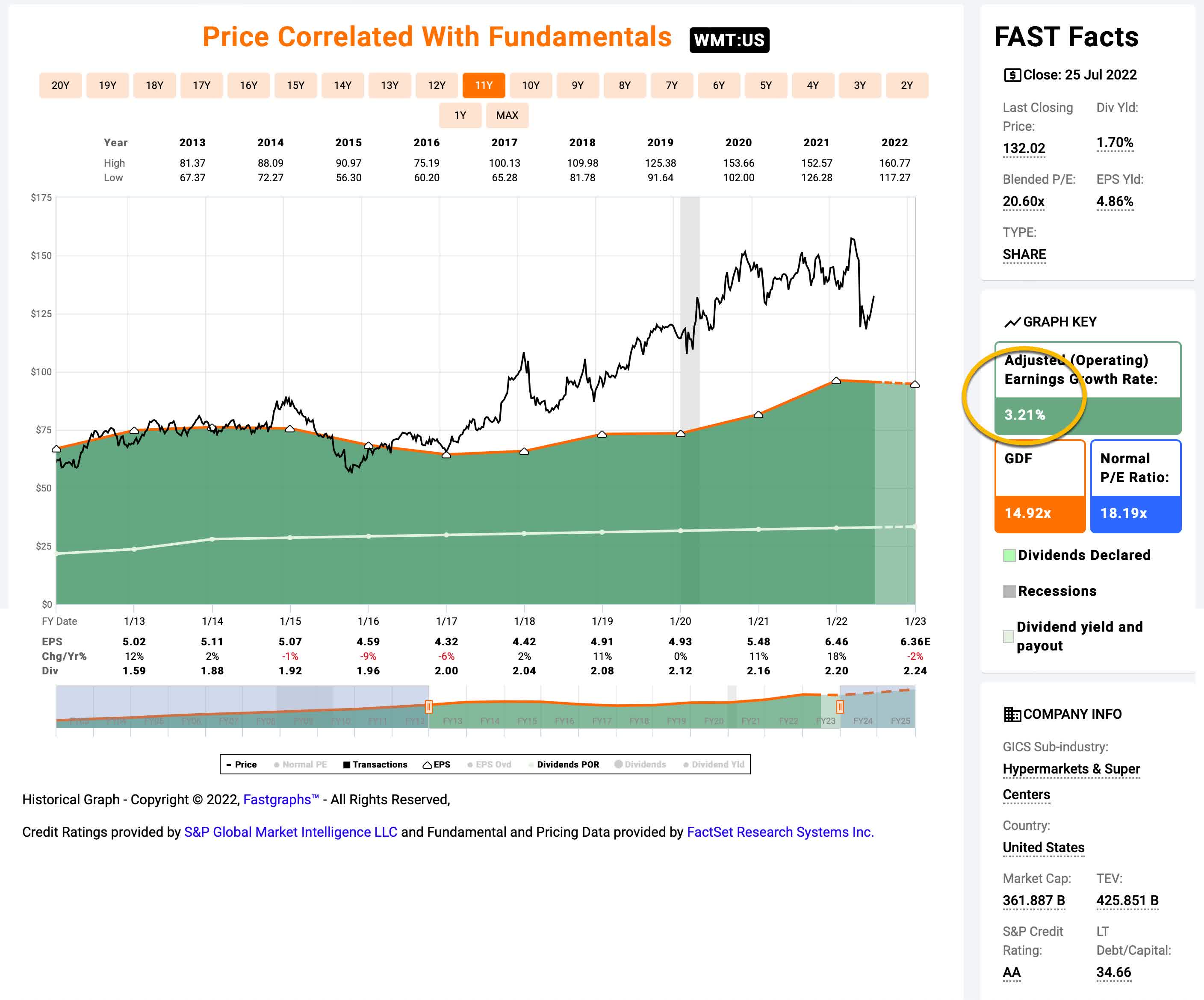

Right now Walmart's forward earnings yield is 5.29%, so if you paid $100 for Walmart, you would earn $5.29 per year on your investment if earnings never grew or shrunk. If you do that for 10 years (10 x $5.29) you get $52.90 worth of earnings you would collect from Walmart's business over that decade. So, we would grow our $100 investment into $152.90 over the course of 10 years. If you plug those numbers into a CAGR calculator, you get a ten-year CAGR of +4.34%. That would be the expected compounded return on your investment if you bought Walmart at today's valuation and kept all the earnings for yourself if those earnings remained the same for ten years.

I don't know about you, but that is a very poor return and not particularly attractive to me. But, fortunately, that's not the end of the story. Higher quality businesses will be able to grow their earnings over time, so each year, in theory, earnings will go up, rather than remain static. For this reason, we need to try to estimate whether earnings will go up, and if they do, how much we think they might go up on average. The way I do this is to look at the past and see what sort of history the business has when it comes to earnings growth.

{kind=link}

I have a few other factors that I typically control for in my standard analysis (and you can read those in my previous Walmart article if you are interested), but in order to keep this explanation simple, I am just going to take Walmart's earnings growth rate over the past decade directly from FAST Graphs, which is circled in gold above. Walmart has grown earnings per share at +3.21% on average since 2013.

Now let's go back to the $5.29 per year we'll earn on our $100 WMT investment and assume that $5.29 grows at +3.21% per year for 10 years. I like to pull the first year's earnings growth forward to be generous. The table below shows how much money we would have accumulated after each year for 10 years.

| Year |

| Cumulative Amount Collected |

| 1 |

| $5.46 |

| 2 |

| $11.09 |

| 3 |

| $16.91 |

| 4 |

| $22.91 |

| 5 |

| $29.11 |

| 6 |

| $35.50 |

| 7 |

| $42.10 |

| 8 |

| $48.91 |

| 9 |

| $55.94 |

| 10 |

| $63.20 |

Okay, whereas before, with no earnings growth we would have earned $52.90 over this time period, because earnings were growing a little bit each year, we earned $63.20. When we assume that $100 grows into $163.20 over the course of 10 years and put that into a CAGR calculator, we get a 10-year CAGR expectation of +5.02%. And that is what one's expected return from Walmart's business is likely to be if the next decade is similar to the last decade.

Investors have to ask themselves if that +5.02% is an adequate return.

For me, I aim for 15% to 20% medium-term annual returns, so a 5% likely return isn't very attractive to me, and at today's price, I would never consider buying a stock with Walmart's valuation. Importantly, as Walmart's stock price goes down, assuming earnings stay the same, the earnings yield will rise and an investor's expected future returns from the business will rise. So, if Walmart's stock price was, say, cut in half, then it would offer much more attractive potential returns.

So, far I've tried to simplify this valuation process in order to get the basics across as much as I can, but this basic valuation can be simplified even more by using a PEG ratio. Popularized by Peter Lynch, the PEG ratio takes the P/E ratio and earnings growth and converts them into one simple ratio. The lower the PEG ratio, the better the valuation, and typically a very good PEG ratio is considered 1 or below. Personally, I would consider a PEG ratio above 2 high, and if a PEG is above 3 that typically corresponds with "sell" for me based on a high valuation (which in turn corresponds to low future returns).

If we take Walmart's estimated earnings for this year of $6.36 (which is probably optimistic given their recent announcement) that produces a P/E of 19.09, and if we divide that by the 3.21 earnings growth rate, we get a PEG ratio of 5.95, which is extremely high, indicating a high valuation (and likely low returns).

For relatively steady-earning businesses like Walmart that have a long earnings history, the PEG ratio is a very quick and easy way to spot over and under valuation. The main thing an investor needs to be careful about is simply making sure their assumptions about earnings and earnings growth are reasonable.

There have been alternative investments available

One excuse for investors owning slow-growing, yet expensive stocks, like Walmart, is that there haven't been alternatives (TINA as it is often referred to). The argument goes, that bond yields have been depressed for the past decade so even if Walmart returns 5%, that's better than bonds and at least Walmart can potentially pass on some inflation to consumers, unlike bonds. On the surface that seems reasonable enough but we also have to consider that, also unlike bonds, there is no guarantee that Walmart will actually achieve that 5% annual return. Sears and K-Mart were similar businesses that couldn't do it. So, we are taking on more risk with Walmart to go along with the potential higher reward and inflation mitigation.

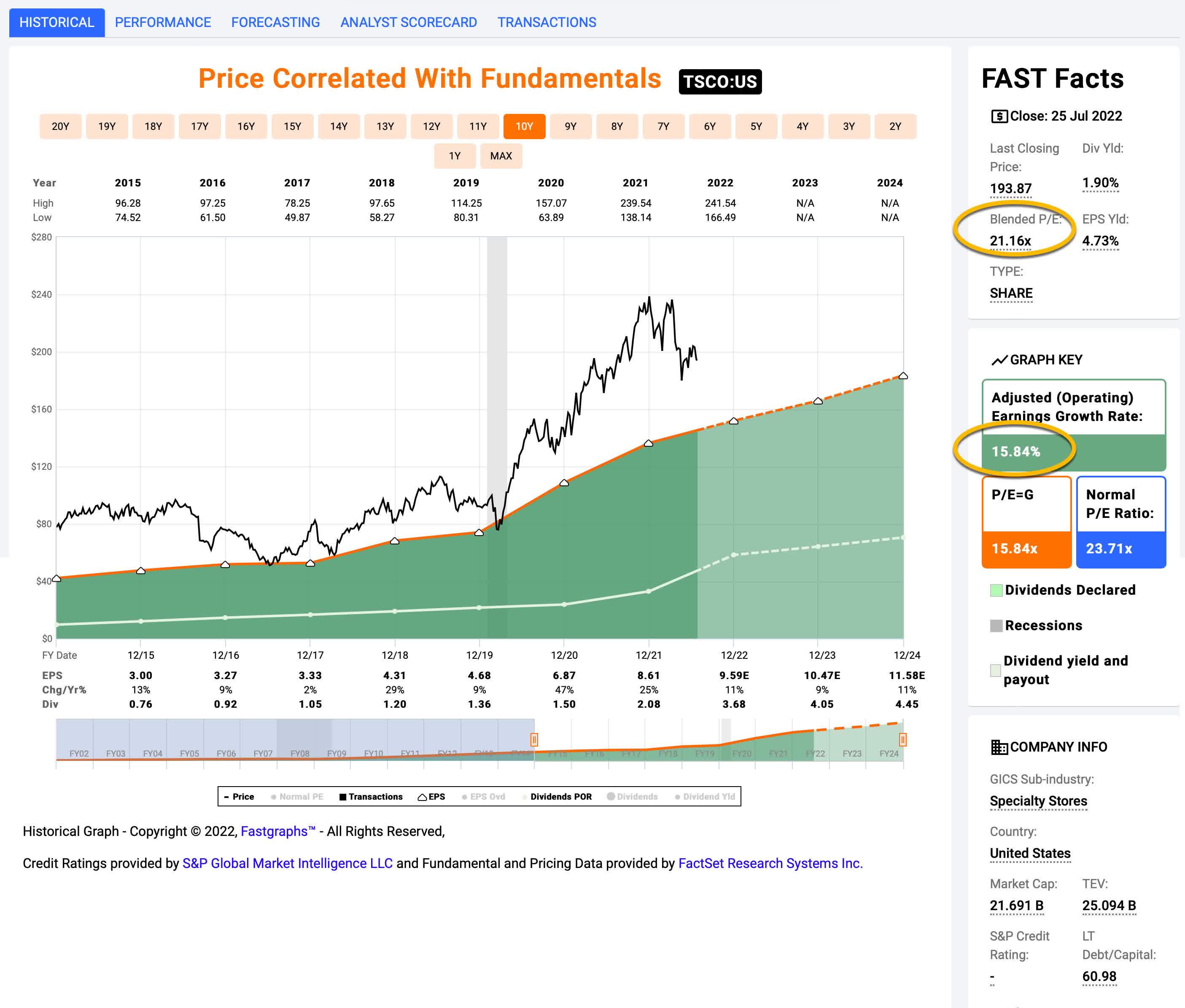

But the better response to Walmart shareholders is that there are similarly priced retail stocks with better earnings growth and, therefore, better PEG ratios. I'll share two that I own. The first is Tractor Supply ( TSCO ).

{kind=link}

Just using the basic information from the FAST Graph without any adjustments we have a P/E of 21.16 (about the same as Walmart) but earnings growth of 15.84%. That's a PEG ratio of 1.34. Perhaps not extremely cheap, like when I bought it back in March of 2020, but a much better deal than Walmart.

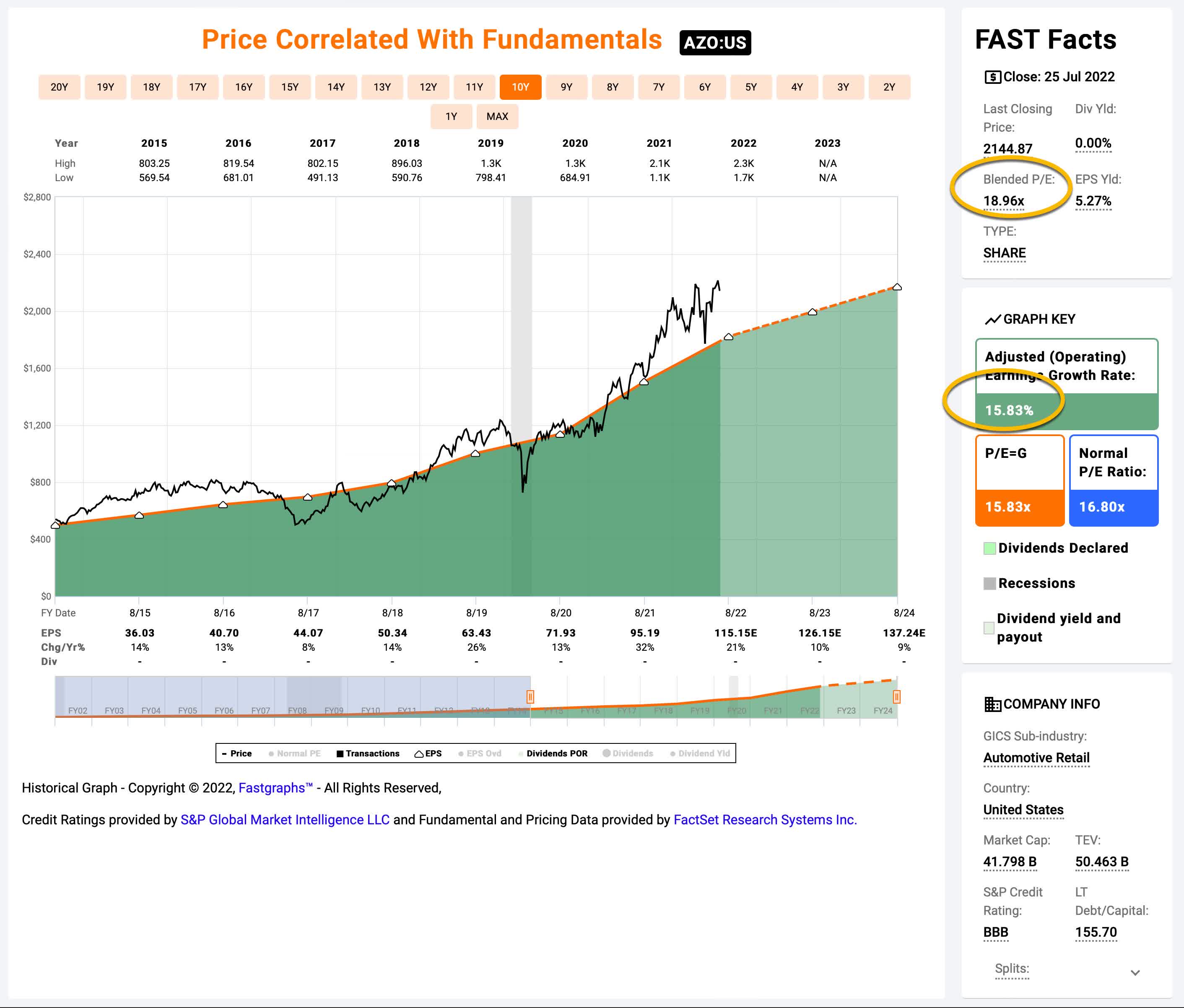

Next, let's look at another one of my holdings, AutoZone ( AZO ).

{kind=link}

In AutoZone's case, it actually has a slightly lower P/E than Walmart, but it also has had 15.83% earnings growth, just using the basic numbers on the FAST Graph. That produces a PEG ratio of about 1.20. Again, perhaps not cheap enough to buy on an absolute basis, but much more attractive as an alternative to Walmart stock.

Conclusion

Brand recognition and a reputation as a winner in distant history are never enough to make up for valuations that are simply too high. Walmart might be around for decades to come, and it might offer a good value to consumers, but that doesn't mean it will be a good investment for investors who are buying or holding the stock today. There really isn't any reason to hold a stock like Walmart at these prices when there are alternatives whose futures are clearly superior and that are trading at better valuations once earnings growth is taken into account. Forgetting name recognition and instead taking a look at the PEG ratio will go a long way to improve the returns of retail investors who own stocks like Walmart.

For further details see:

A Simple Metric To Help Avoid Walmart-Like Stocks In Your Portfolio