CCJ - A Study Of Cameco's History Suggests Uranium Bull Market Is Just Getting Started

2023-05-08 16:34:40 ET

Summary

- If you feel like you've already heard enough deductive reasoning about why uranium is entering a bull market, below I offer a fresh perspective for your consideration.

- Examining the operational history of industry leader Cameco throughout past business cycles can reveal where we stand in the current uranium cycle.

- My operational analysis indicates the uranium bull market is still in its early stages. Business is expected to continue to improve in the next few years.

- Investors seeking to profit from the next uranium up-cycle may want to consider Cameco before the stock breaks out of its current range.

Over the past few years, there has been a significant amount of discussion surrounding a potential uranium bull market. Nuclear power has gained increasing acceptance as a carbon-free energy source in the developed world. With China and India expanding their nuclear reactor fleets and Japan reactivating its nuclear power plants, which had been idle since the 2011 Fukushima disaster, uranium demand is expected to continue growing over the next decade and beyond. However, on the supply side, the uranium mining sector has experienced underinvestment for almost a decade, resulting in a decline in reserves and production capacity; there are also various issues with new mine construction, ranging from regulatory hurdles via permitting new mines to the current uranium prices that are still too low to incentivize new western supply. As a result, the uranium market has been unbalanced in recent years, leading to commercial inventory draws. Traders claim that the current uranium market is the tightest it has been in ten years, and the carry trade is no longer a viable option due to the unavailability of spot material and higher interest rates.

Macro analysts have identified near and medium-term catalysts that could significantly boost the price of uranium, potentially surpassing the peak of the last up-cycle in 2006-2007 when it reached US$137/lb U3O8 as shown in Figure 1.

{kind=link}

Fig. 1. Uranium (U3O8) spot and long-term prices (modified from Cameco)

Several factors could significantly impact the price of U3O8 in the near future. Firstly, the introduction of the Sprott Physical Uranium Trust ( SRUUF ) has reduced the supply of uranium in the market since July 2021. As more investors recognize the environmentally friendly benefits of nuclear energy and invest in the uranium market, which currently has a market value of just US$10 billion, the U3O8 price could increase rapidly. Secondly, the Russian invasion of Ukraine has prompted Western utilities to prepare for potential sanctions on Russian nuclear fuel, which could drive up the price of converted and enriched material and, in turn, impact U3O8 prices. Given that Russia plays a significant role in uranium conversion and enrichment, this development could have a major impact. Thirdly, the enrichment segment of the uranium industry is shifting from underfeeding to overfeeding , which may also affect U3O8 prices. This change will result in roughly 30-35 Mlb of additional demand for U3O8 over the next few years, resulting from the cessation of underfeeding (20 Mlb) and the commencement of overfeeding (10-15 Mlb). Lastly, utilities are projected to enter the spot market later in the cycle, as they traditionally did in previous cycles, when the yellow cake is apparently insufficient to meet their requirements.

Despite the positive factors mentioned earlier, the price of uranium has remained stagnant around US$50/lb since early 2022, as depicted in Figure 1. Therefore, it is imperative to conduct a more detailed examination of Cameco Corporation ( CCJ ) to uncover independent clues as to whether a bull market is genuinely underway. Cameco is chosen not only because it is the largest uranium producer in the Western world, but also because as an organization it has such a profound knowledge of the nuclear energy value chain - as I shall discuss in details below - that we can assume it is best-positioned in the industry to make intelligent decisions across the cycles.

An overview of Cameco

Vertical integration

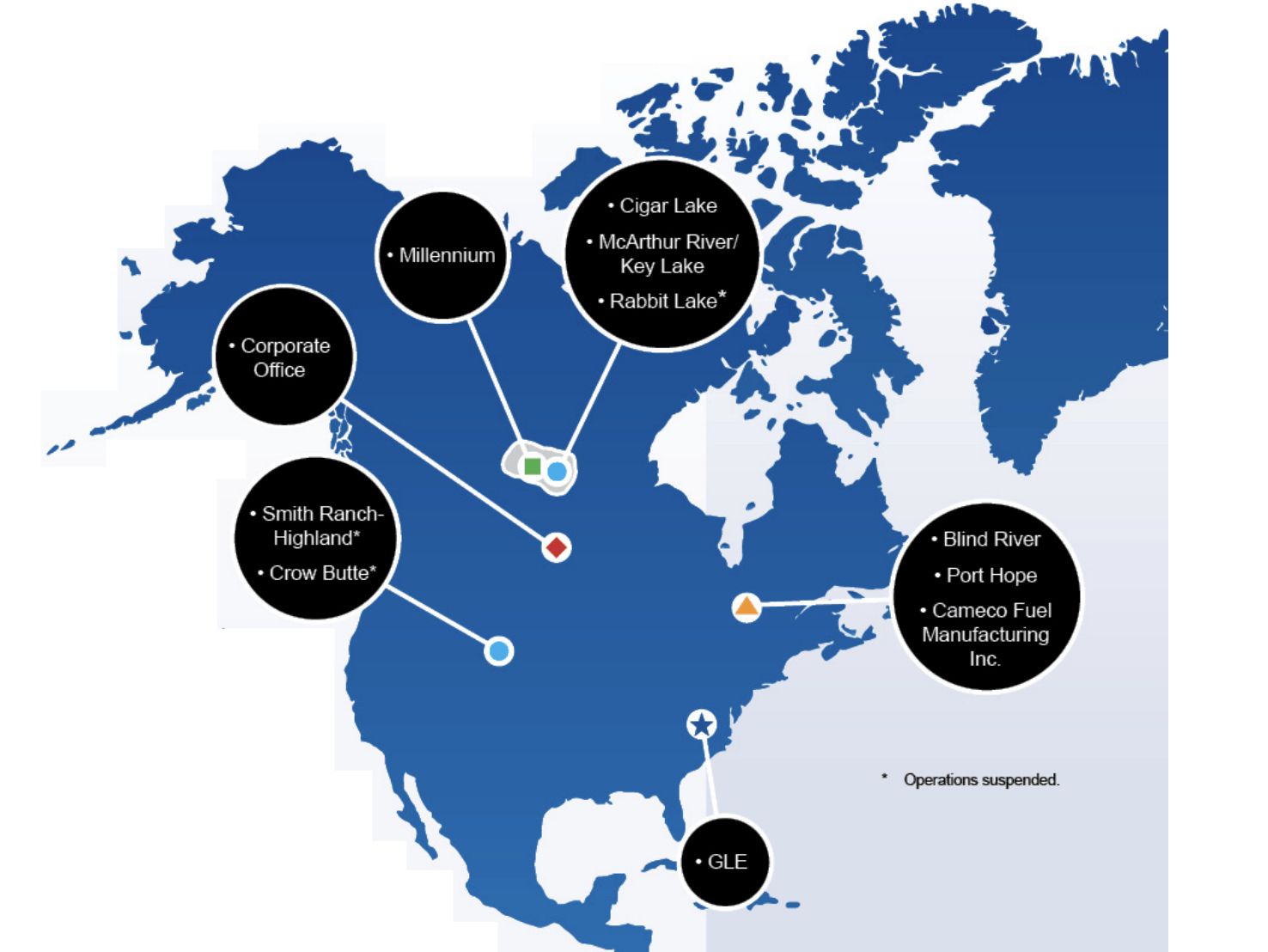

Originally created by the merger and privatization of two Crown corporations, Cameco went public in 1991 only to become fully private in 2002. Cameco pursues a strategy of capturing full-cycle value from upstream (exploration for and production of uranium) to downstream (uranium refining, conversion and fuel fabrication). Following a series of M&A, Cameco is now one of the largest suppliers of uranium fuel to utilities around the world, as illustrated in Figure 2.

- Upstream: Cameco operates several uranium mines in the Athabasca Basin in northern Saskatchewan, including McArthur River-Key Lake (70% and 83%), the world's largest high-grade uranium mine and mill; Cigar Lake (54.5%), the world's highest grade uranium mine; and Rabbit Lake (100%), which is currently in care and maintenance. In addition to these Canadian mines, Cameco owns a 40% interest in Inkai in Kazakhstan, in partnership with Kazatomprom (60%). In the U.S., Cameco has a 100% interest in two uranium mines, Crow Butte and Smith Ranch-Highland, both of which are currently suspended. Cameco also has an interest in undeveloped uranium projects, such as Millennium (69.9%) in the Athabasca Basin, and Yeelirrie (100%) and Kintyre (100%) in Western Australia, as well as several exploration projects.

- Downstream: Cameco operates the Blind River uranium refinery (100%) in Ontario, which is the world's largest commercial refinery. The UO 3 powder produced at Blind River is then transported to Cameco's wholly-owned Port Hope conversion facility in Ontario, where it is used to produce uranium hexafluoride (UF 6 ) and uranium dioxide (UO 2 ). Port Hope has approximately 21% of the world U F 6 prim ary conversion capacity. The UF 6 and UO 2 products are then used in the fabrication of fuel bundles for light-water and CANDU-type, heavy-water nuclear reactors at facilities in Port Hope and Cobourg.

{kind=link}

Fig. 2. The operational footprint of Cameco in North America, with the Inkai operation in Kazakhstan not shown (modified from Cameco)

In addition, Cameco has a 49% non-operating stake in Global Laser Enrichment LLC , in partnership with Silex Systems Ltd. ( SILXY ). Global Laser Enrichment is the exclusive licensee of the SILEX laser enrichment technology, which is a third-generation uranium enrichment technology.

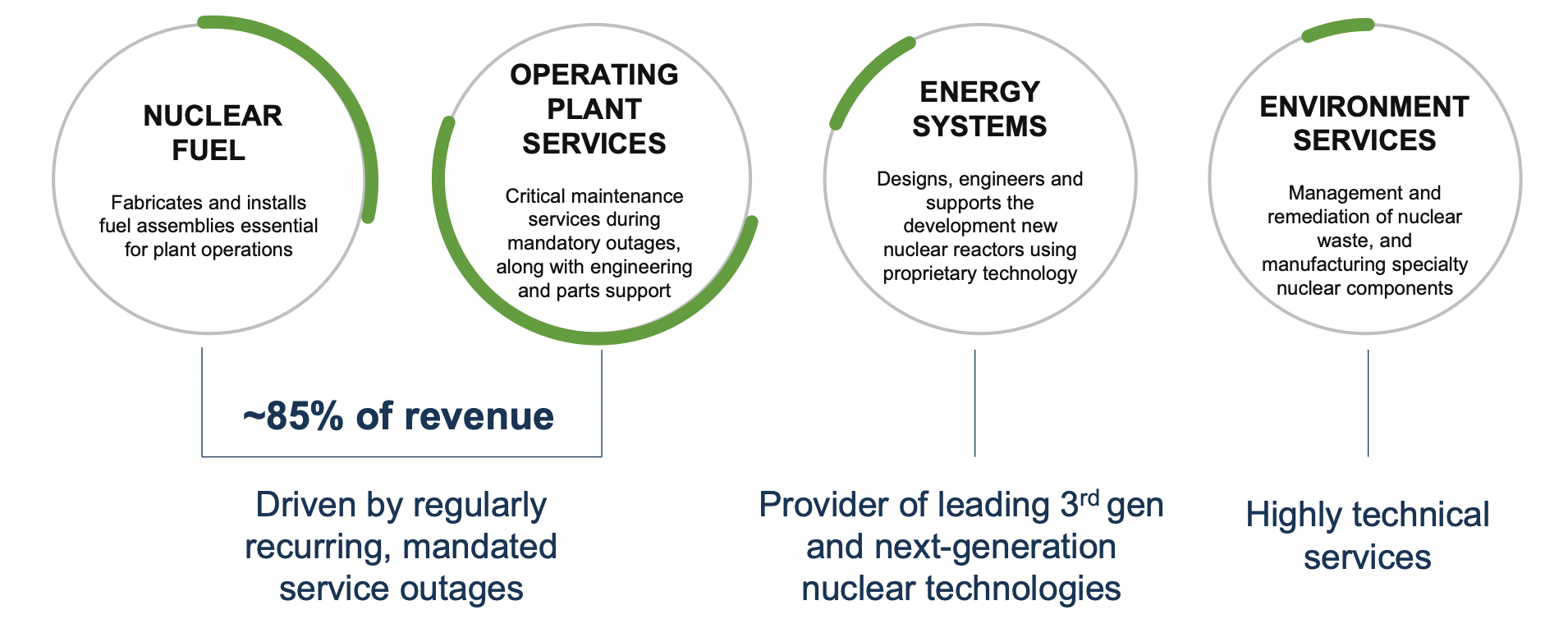

To further expand its participation in the nuclear fuel value chain and acquire long-term customer relationships, Cameco (49%) and Brookfield Renewable (51%) joined hands in October 2022 in the purchase of Westinghouse Electric Company , an established service provider for the nuclear power industry. Westinghouse mainly engages in the manufacturing and installation of fuel assemblies and other ancillary equipment across multiple light-water reactor technologies. Some 85% of its revenue is from long-term contracted or highly-recurring customer service provisions with an almost 100% customer retention rate, as evidenced in Figure 3.

{kind=link}

Fig. 3. Business segments of Westinghouse Electric Company (Cameco)

Uranium pure-play

The uranium industry consists of a quadropoly structure, with Kazakh state company Kazatomprom (KAP.LSE), French company Orano, Cameco, and Russian concerns as the main players. Kazatomprom is exclusively involved in upstream activities like uranium mining, while the Russians are primarily engaged in uranium refining and conversion. Cameco is the largest uranium pure play that participates in the entire value chain of the uranium industry.

- Previously, Cameco owned gold mining operations, including the Kumtor gold mine in Kyrgyzstan, which was later spun off as Centerra Gold Inc. ( CGAU ). In 2009, Cameco divested all of its Centerra holdings.

- Cameco also previously held a 31.6% limited partnership interest in Bruce Power, which generates about 30% of Ontario's electricity from its nuclear power plant. However, in 2014, Cameco sold its stake in Bruce Power for C$450 million. Despite the sale, Cameco remains the exclusive fuel supplier to Bruce Power.

Uranium reserves and resources

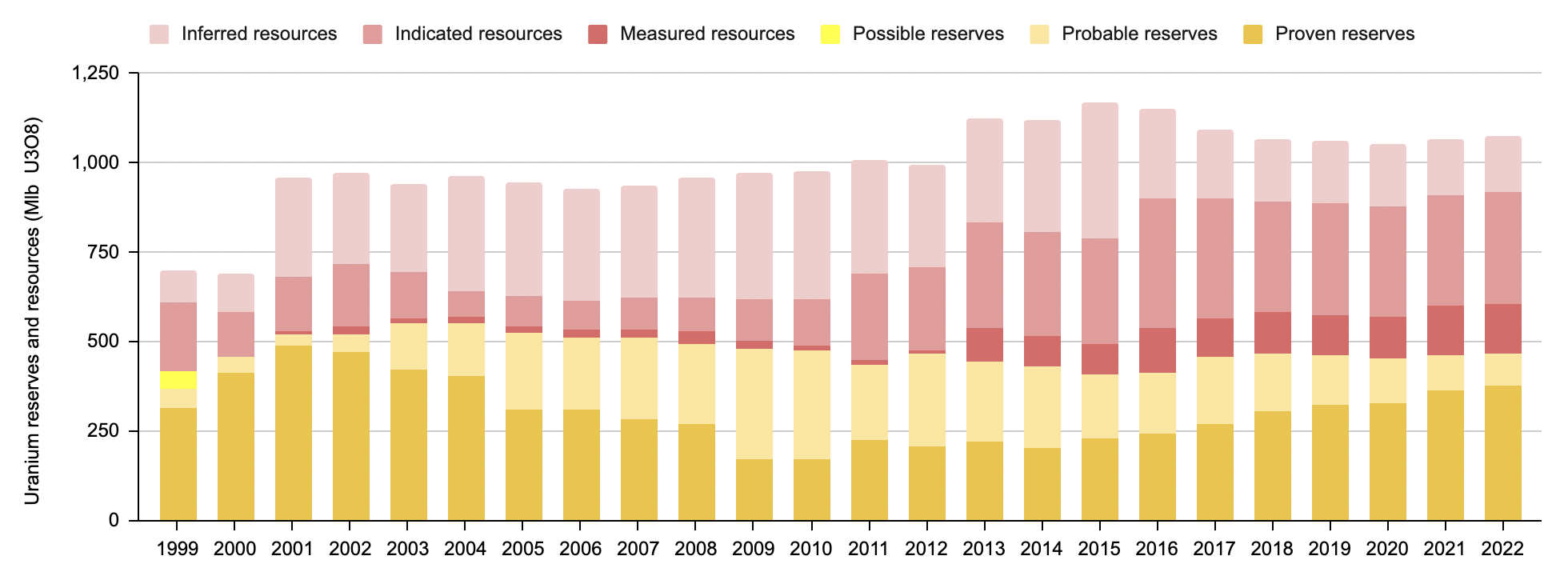

As of December 31, 2022, Cameco's proven and probable reserves of U3O8 amount to 469 million pounds. In addition, the company has approximately 606 million pounds of resources in the measured, indicated, and inferred categories, as illustrated in Figure 4.

{kind=link}

Fig. 4. The uranium reserves and mineral resources of Cameco (Cameco)

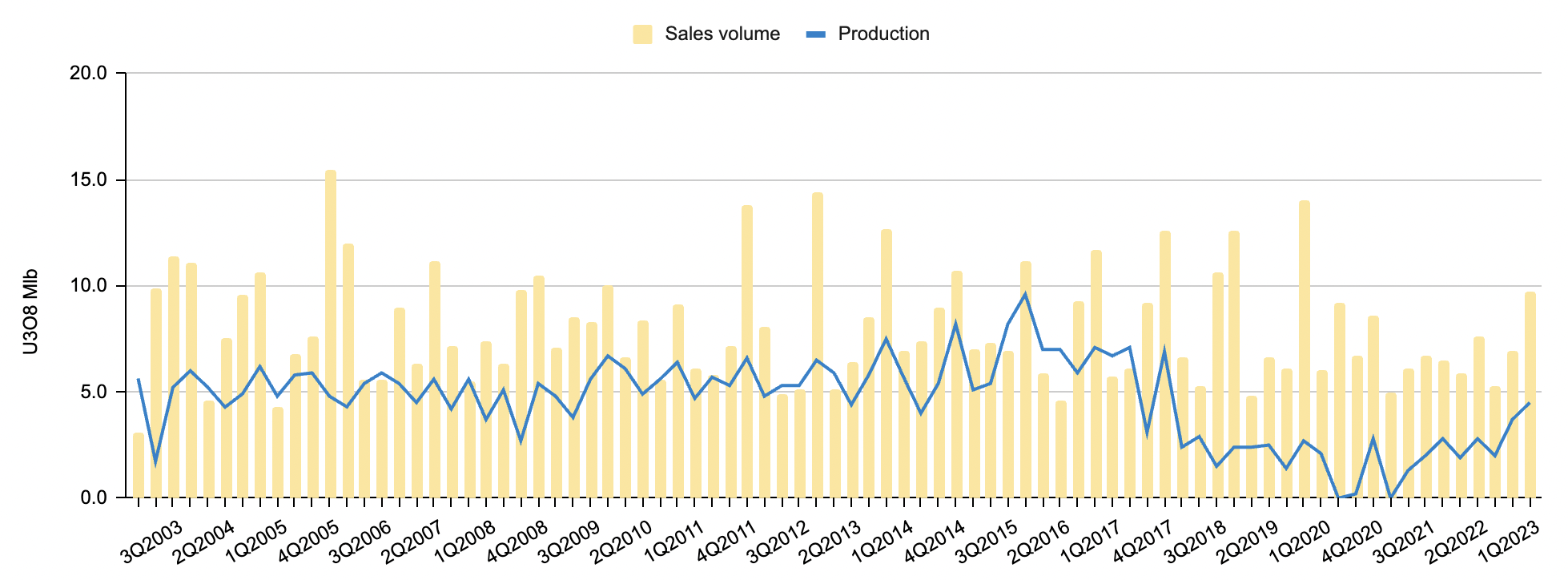

Based on an average production rate of 18.3 million pounds per year from 2000 to date (as shown in Figure 5), Cameco's proven and probable reserves suggest a reserve life of 25.3 years. Over time, Cameco has steadily converted uranium mineral resources to reserves in response to demand, as illustrated in Figure 6. With 606 million pounds of uranium resources available for upgrading, Cameco appears to have sufficient asset backing for many decades to come. The abundance of reserves and resources, however, poses a hidden risk for investors as it allows major producers to increase production and flood the market, ultimately leading to a crash in uranium prices, as observed during the 2006-2007 cycle (Figure 1).

{kind=link}

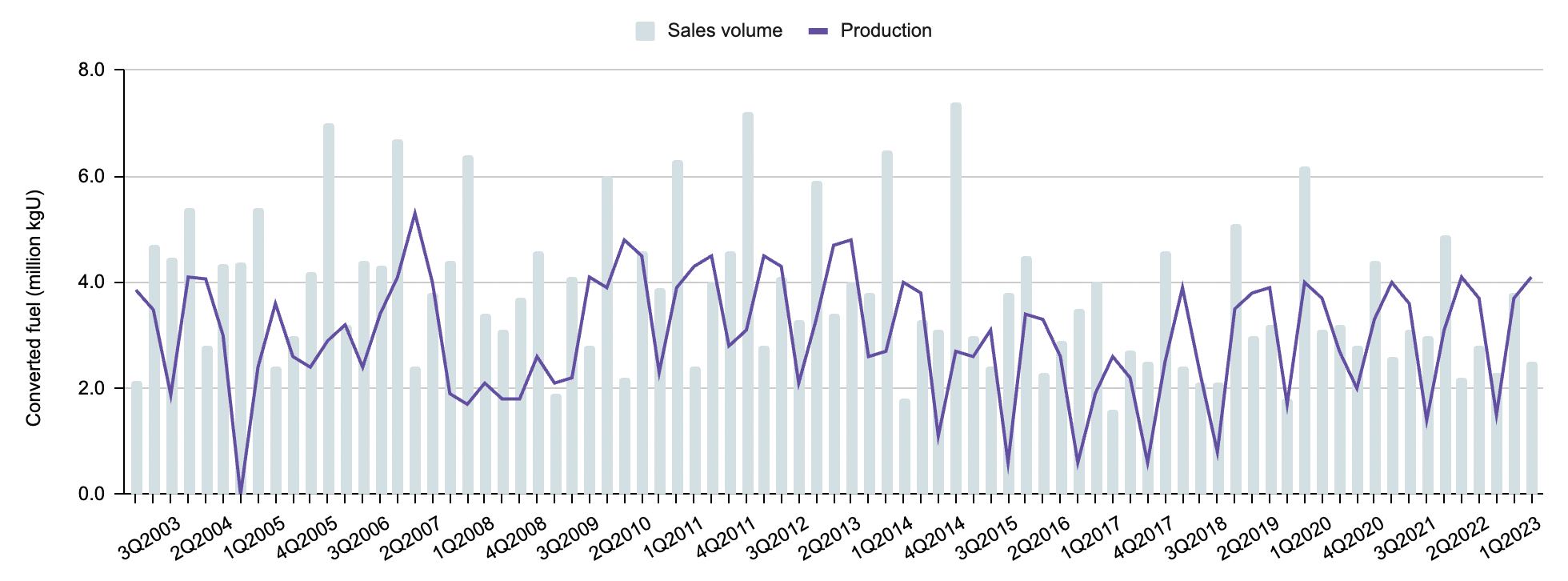

Fig. 5. Cameco's uranium production and sales volumes by quarter. Note sales tend to spike in the fourth quarters (compiled by Laurentian Research for The Natural Resources Hub based on data released by Cameco)

{kind=link}

Fig. 6. The year-end uranium reserves and mineral resources of Cameco (compiled by Laurentian Research for The Natural Resources Hub based on data released by Cameco)

It's worth noting that during the previous uranium bull market, Cameco allowed the proven and probable reserves to decline, a trend that wasn't reversed until the subsequent bear market started in 2017. Since then, the proven and probable reserves have remained relatively unchanged, as shown in Figure 6. If we take the last cycle as a reference point, we can expect to see depleting reserves only when the next bull market reaches full swing.

Operational trends

Production and sales volumes

Figure 5 indicates that the sales volume of uranium remained relatively stable over the years due to long-term contracts with utilities, except for the past two years. Similarly, Figure 7 shows that the production and sales volumes of converted fuel also remained steady for the same reason.

{kind=link}

Fig. 7. Converted fuel production and sales volumes of Cameco. Note sales tend to spike in the fourth quarters (compiled by Laurentian Research for The Natural Resources Hub based on data released by Cameco)

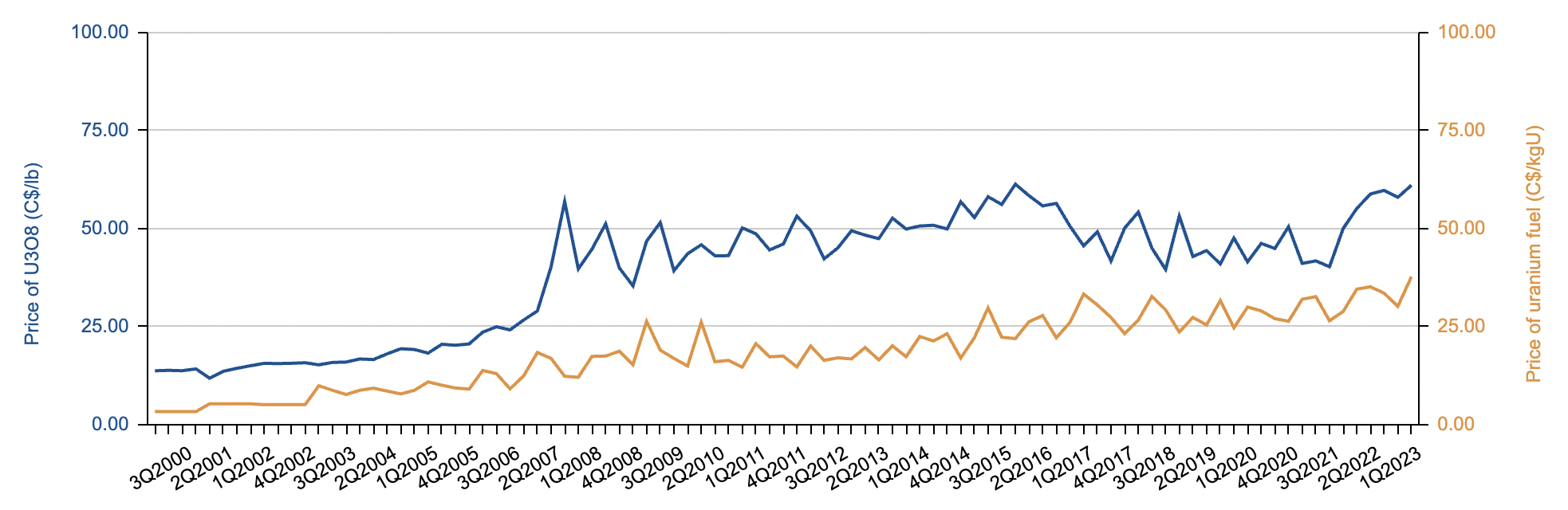

On the other hand, the production volume of uranium is a more accurate reflection of market sentiment. As shown in Figure 8, when the spot uranium price dropped below the break-even point of C$40-45 per pound at the giant McArthur River mine in 2017, Cameco responded by temporarily suspending production . The production volume of uranium has yet to recover to the 2016 levels (Figure 5), indicating that the current cycle may still be in its very early stages.

{kind=link}

Fig. 8. Prices of U3O8 and converted fuel realized by Cameco (compiled by Laurentian Research for The Natural Resources Hub based on data released by Cameco)

Revenue and margins

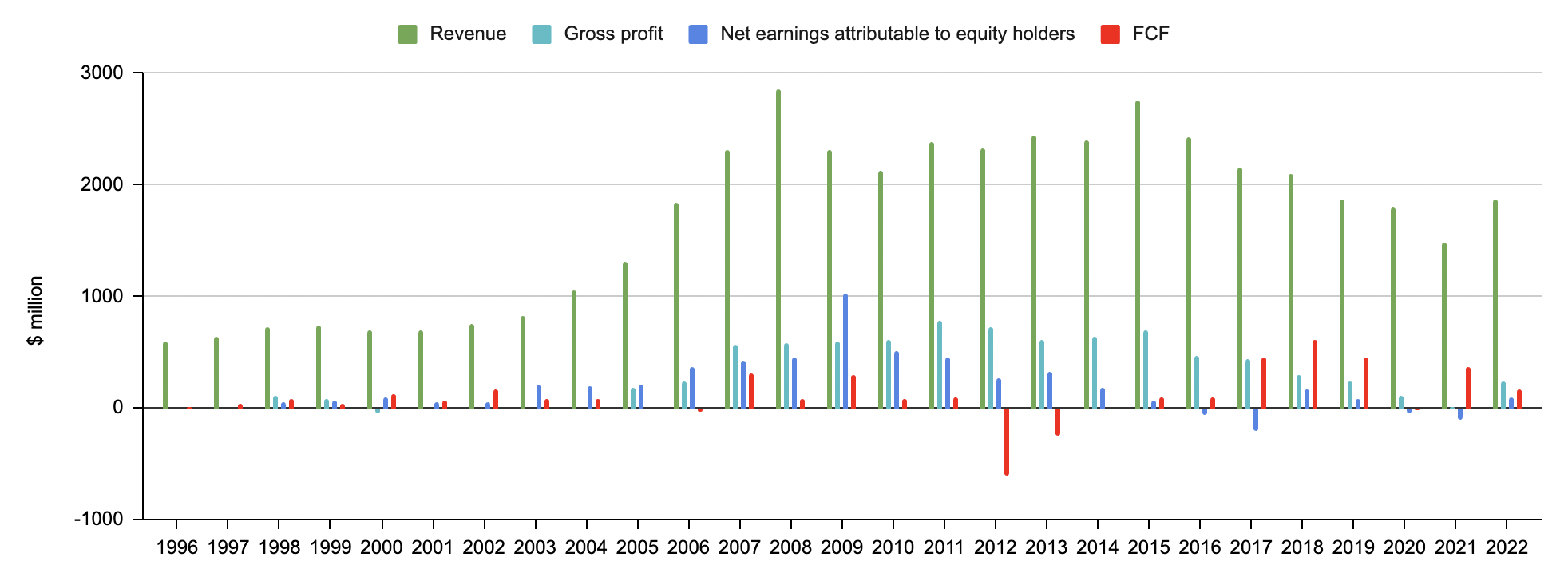

With weakened uranium price realization in 2017, revenue declined, hitting a 15-year low in 2021 before experiencing a moderate recovery in 2022, as illustrated in Figure 9.

{kind=link}

Fig. 9. Annual revenue, gross profit, net earnings, and free cash flow of Cameco (compiled by Laurentian Research for The Natural Resources Hub based on data released by Cameco)

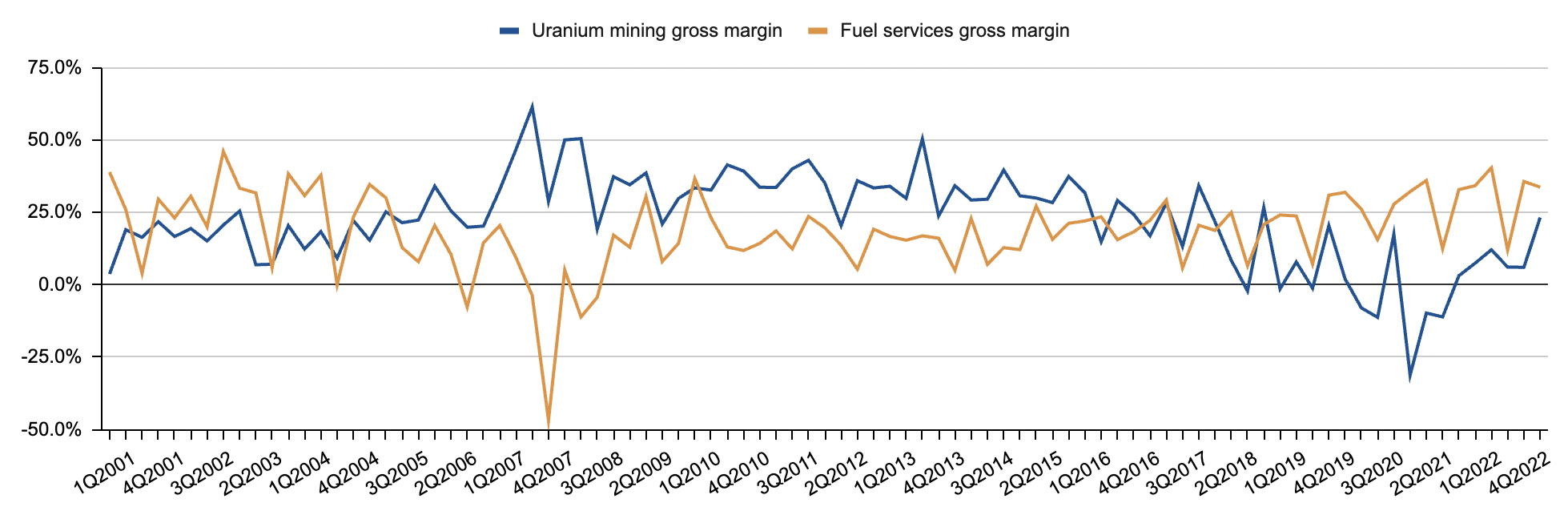

In 2007, the fuel services segment's collapse in operating margin was compensated for by the high operating margins of the uranium segment. However, the uranium segment's consistently low operating margin over the past four years has been too significant for the much smaller fuel services segment to offset, as depicted in Figure 10.

{kind=link}

Fig. 10. Gross margin of the uranium segment and fuel services segment of Cameco (compiled by Laurentian Research for The Natural Resources Hub based on data released by Cameco)

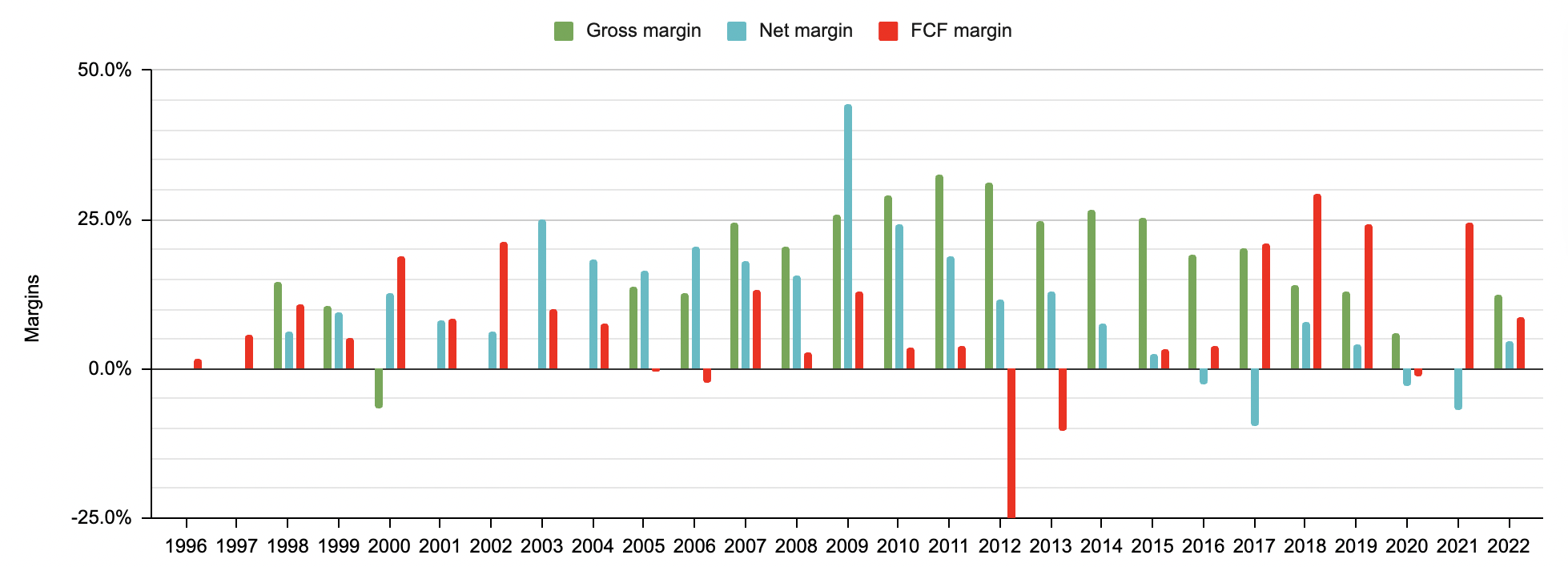

The weak gross margins at the business segment level have led to a low consolidated gross margin over the past few years. In response to declining profitability, Cameco cut capital expenditures, resulting in an expansion of the free cash flow margin, as depicted in Figure 11. In many respects, the margins of the last few years resemble those of the late 1990s and early 2000s, when the previous uranium bear market was at its lowest point and the next bull market was starting to form. If this comparison holds, then we have yet to see the full potential of the current up-cycle.

{kind=link}

Fig. 11. Gross margin, net margin and FCF margin of Cameco (compiled by Laurentian Research for The Natural Resources Hub based on data released by Cameco)

Outlook

Cameco added 35 Mlb in long-term contracts, bringing the total contract book to 215 Mlb of uranium and 70,000tU of UF6 conversion services with deliveries scheduled over the next 10 years. This translates to an average annual delivery of 26 Mlb over the next five years, an increase from the 21 Mlb projected for 2022. With this contract portfolio, Cameco anticipates a rise in sales volume in the coming years.

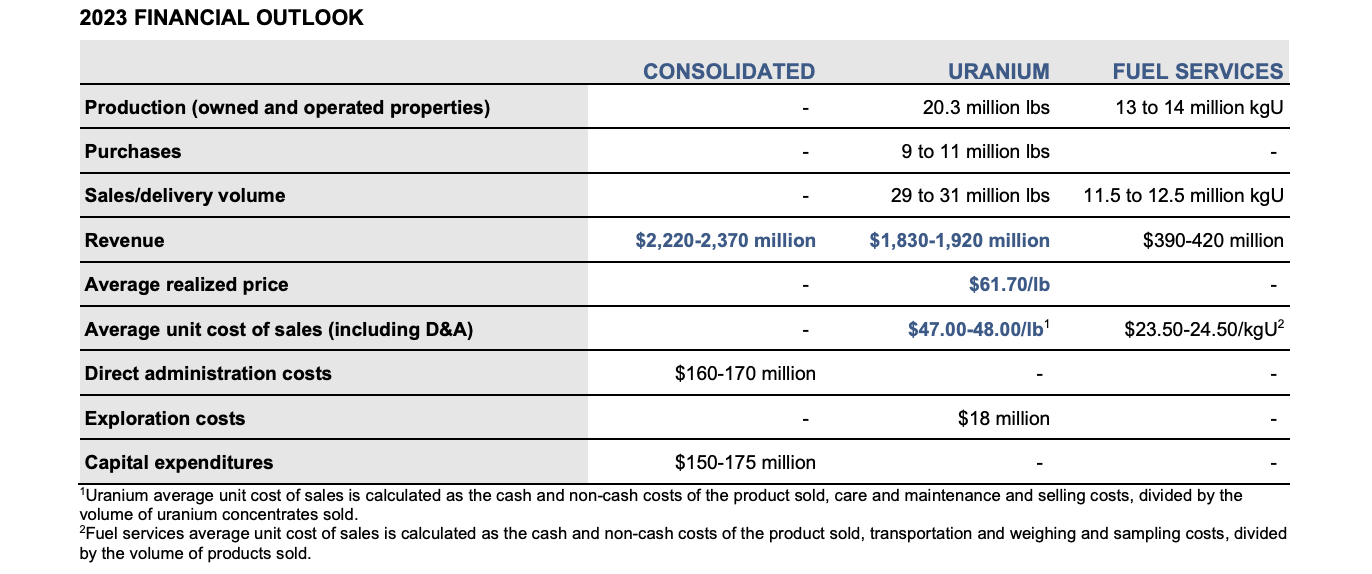

In its first quarter earnings report, Cameco raised its guidance for 2023, as shown in Table 1,

"With our plan to produce 18 million pounds per year (100% basis) at Cigar Lake, 18 million pounds per year (100% basis) at McArthur River/Key Lake beginning in 2024, and increase UF 6 production at our Port Hope conversion facility, we expect to see continued improvement in our financial performance .

...[We expect] consolidated revenue to be between $2,220 million and $2,370 million (previously $2,120 million to $2,270 million). The average unit cost of sales in our uranium segment is now expected to be between $47.00 and $48.00 per pound (previously $46.00 to $47.00 per pound)..."

{kind=link}

Table 1. 2023 financial outlook of Cameco (Cameco)

Investor takeaways

Our comprehensive operational analysis of Cameco suggests that the uranium bull market is still in its early stages. The financial outlook indicates that the company's top line and profits are expected to improve in the coming years. That makes it an opportune time to enter the market.

Cameco is a vertically-integrated uranium fuel vendor in an oligarchic industry, making it one of the best-positioned mining companies to benefit from a uranium bull market. Investors seeking to profit from the next up-cycle may want to consider Cameco as their first choice before exploring alternative options.

Cameco's share price has been hovering around C$33 or US$25 per share since 2022. While estimating the company's intrinsic value is beyond the scope of this article, Wall Street analysts have set a 12-month price target 34% above the current share price, as shown in Figure 12. Interested investors may want to establish a position before the stock breaks out of its current range.

For further details see:

A Study Of Cameco's History Suggests Uranium Bull Market Is Just Getting Started