ACMR - ACM Research: Great Growth Story But Geopolitically Risky

2023-06-08 11:11:50 ET

Summary

- ACM Research is a rapidly growing semiconductor stock with a broad cleaning product portfolio and a serviceable addressable market of $16 billion in 2022.

- The company is investing heavily in production capacity, particularly in China, but faces risks due to geopolitical tensions and country-related concentration risks.

- While ACM's cheaper valuations already account for geopolitical risks, it is not an opportunistic investment at this moment, but worth watching due to its innovation in the semiconductor industry.

As an investor looking to put some money in semiconductor stocks, ACM Research (ACMR) seems to be that rare pearl everyone is looking for, especially during these uncertain times when there are risks of economic slowdowns on both sides of the Atlantic Ocean as central banks tighten monetary policy and China's Covid recovery is proving to be uneven .

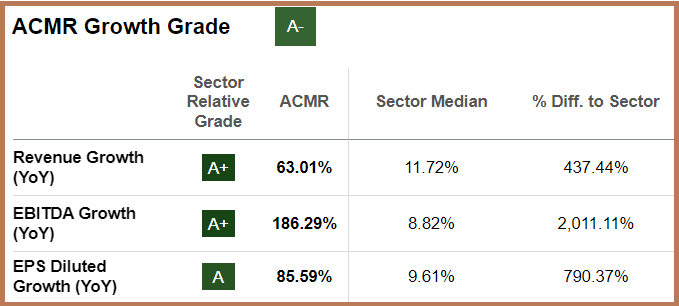

The reason is the company is growing at a frantic pace, not only in terms of sales but also EBITDA and Earnings per Share as pictured below .

{kind=link}

On top of this, with a valuation grade of A-, it is trading at a heavy discount of at least 50% with respect to the IT sector. My aim with this thesis is to understand the reason for this apparent discrepancy and also assess whether the stock could represent an opportunistic investment. For this purpose, I will use data from the first quarter financial results (Q1).

First, I dive into the company's products.

Thriving in Semiconductor Cleaning Equipment

ACM has a broad cleaning product portfolio in the industry, which according to its CEO covers nearly 90% of all cleaning process steps. For investors, cleaning is an essential step in the semiconductor manufacturing process. In this connection, the company has introduced several cleaning tools, like the Bevel Etch tool and high-temperature SPM, which are used for single-wafer applications.

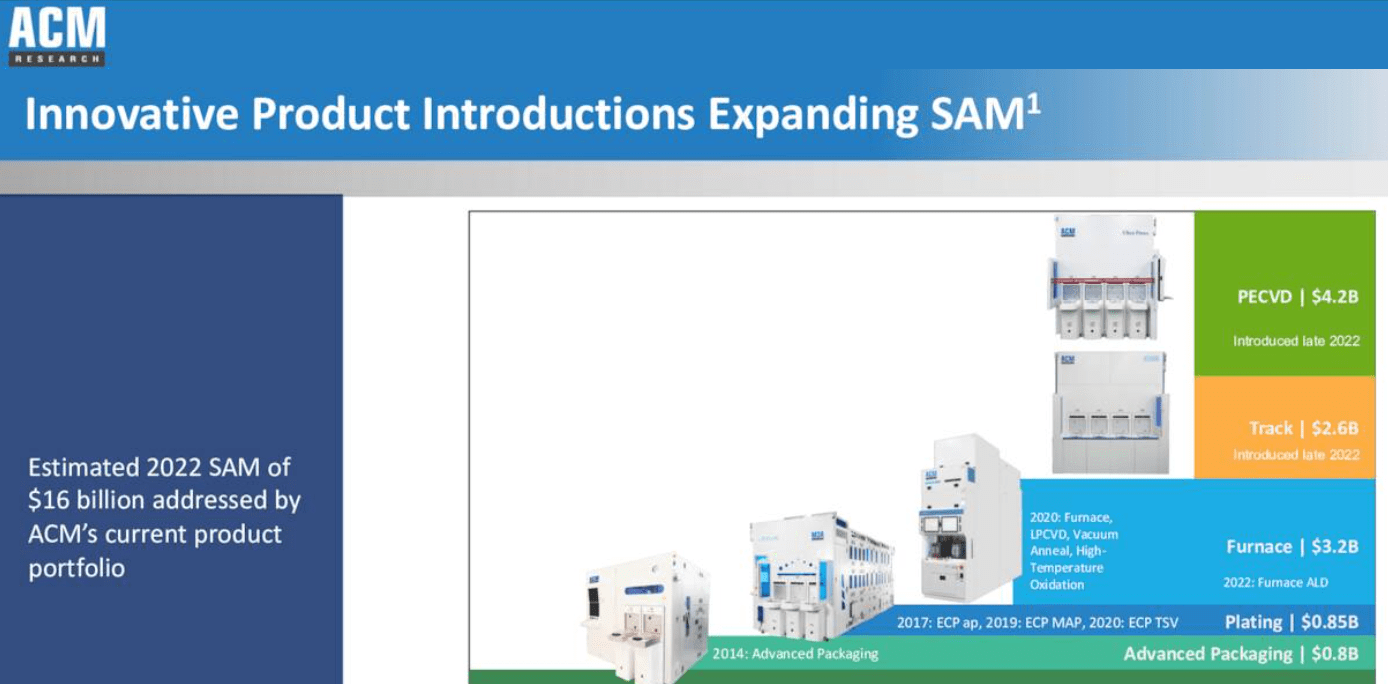

It also has a strong presence in furnace and advanced packaging as pictured below. These all translate to a Serviceable Addressable Market aka SAM of $16 billion in 2022. One point here is that compared to the total addressable market, SAM is more targeted.

{kind=link}

From $389 million in 2022, the company aims to attain $1 billion in sales in the future, and with annual growth averaging 57% from 2017 to 2022, the target could be attained in a matter of years.

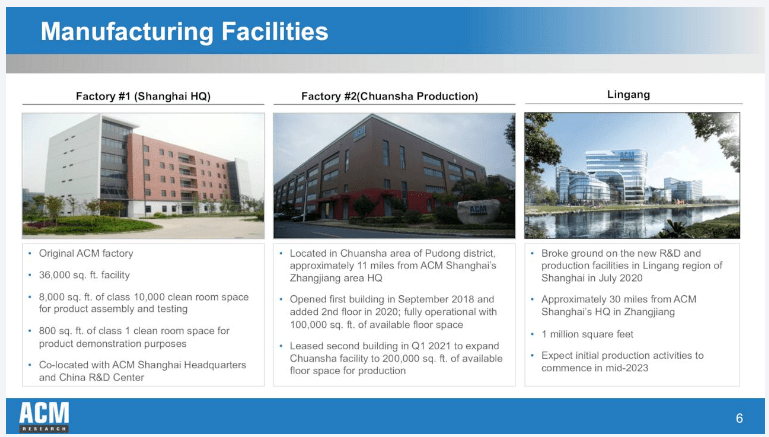

Now, in order to support its growth it has to invest in production capacity like in Lingang, China where it has been expanding. It is also investing in South Korea and the United States, but the bulk of investments are concentrated in China as pictured below.

{kind=link}

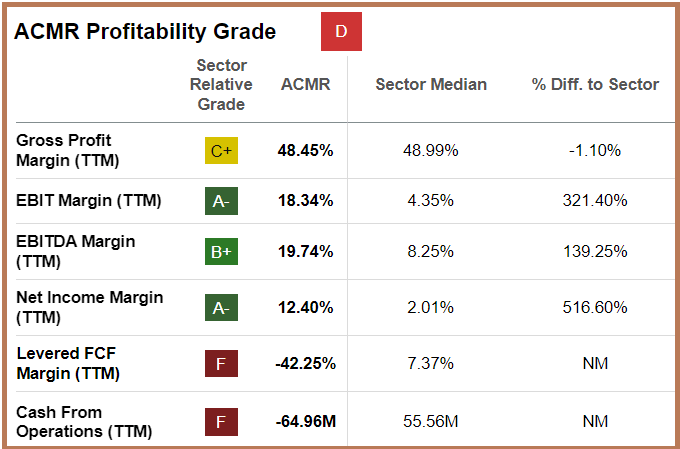

The East Asian country also accounts for its high profitability with its net income margins higher than peers in the IT sector by over 500% . The reason is that with the high demand, it can fetch a high price for its machines which remain superior to peers. This superiority is due to the high degree of innovation as the company has more than 40 patents covering wafer cleaning, electro-polishing, and plating registered in East Asia and the U.S.

ACM can also tap into the vast manpower pool at competitive prices as labor costs are lower than in Taiwan or South Korea where the cost of living is higher. Additionally, with the Semiconductor Industry Association ranking China as the world's top semiconductor market in 2022, the country has a wider choice of suppliers to source raw materials.

However, to bring some realism to the rosy picture painted so far, I also shed light on the investment ACM is making to support such a high growth level.

High Investments and Country Concentration Risks

Talking figures, about $100 million of capital expenditure is planned for 2023. This is not likely to trend lower as projects involving significant spending are scheduled to be completed "in the next several years". Now, Capex growth of 846% is more than 7000 % higher than the IT sector which in itself is something good as it shows that the company is strongly committed to growth. Still, high capital usage has resulted in free cash flow (levered) being -42% compared to 7% for the sector median, as shown below.

{kind=link}

In addition, the company is using up cash from operations instead of generating profit. Well, it did have a positive cash balance of $381.7 million at the end of Q1, or a decrease from the $420.9 million at the end of last year. Moreover, given the relatively modest rate at which it is consuming money (or $30.5 million in its last reported quarter), we can expect the cash to last for another year, unless there is a drastic fall in revenues. This seems unlikely in the short term given the finished goods inventory is sitting at $195.7 million due to some delays in customer uptake due to Covid and the Chinese new year in Q1. Therefore, a rebound can be expected in Q2 as the inventory is converted to sales.

Furthermore, the company is also remodeling its new Shanghai headquarters and expanding production facilities in that country. This comes at a time when geopolitical tensions have escalated around Taiwan and many American companies are thinking twice before investing in that country. Also, the U.S. Department of Commerce has imposed restrictions against exporting high-end chips from Nvidia (NASDAQ: NVDA ) to China as well as the equipment that can produce these devices from suppliers like Applied Materials (NASDAQ: AMAT ) and others.

{kind=link}

Thinking aloud, the tactical move to expand production in China also somehow counters America's strategy to onshore production of chips in light of the CHIPS Act. Therefore, as an American company that is helping China develop its industry through sophisticated equipment, further sanctions may impact ACM's revenues in my view. For this matter, the company has already suffered, albeit indirectly, as a result of current U.S. restrictions impacting its supply chain as per the CFO, with the consequence that this may have delayed certain customer deliveries.

Risks Outweighs Rewards

In these circumstances, an investment in ACM can be rewarding but risky too. On the one hand, you have an undervalued company that is highly profitable and whose products are in high demand in the world's premier semiconductor market. On top, China's uneven recovery has not been contagious to its growth. Furthermore, it may be investing heavily but that does not pose an availability problem for the medium term.

On the other hand, there are country-related concentration risks not only for the customer base but also in terms of manufacturing facilities, and as geopolitical tensions between the U.S. and China keep on deteriorating , this means that there are legitimate concerns about investing.

Now, the semiconductor play has shown a willingness to diversify and is putting more money and effort into South Korea which is a U.S. ally. There are also sales and marketing efforts to diversify the customer base outside Mainland China, but things are still in the market exploration phase. Looking ahead, ACM's strategy is for half of its revenue to come from outside China in an effort to diversify geographically, but no timeline has been provided, and, till these efforts produce concrete results, most of the revenue growth will be coming from that country.

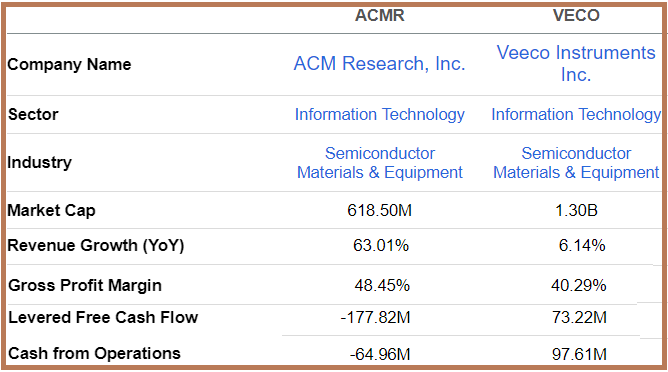

Now, for those looking to invest in semiconductor materials and equipment, another small cap to consider is Veeco Instruments (NASDAQ: VECO ) which also has revenue exposure to China, but only at 40% during its first quarter of 2023. It has a more diversified revenue base with 20% from the U.S., 15% from the EMEA region, and 25% from the Asia Pacific Region excluding China. In comparison, as per my calculation, 97% ($72,458 million out of a total of $74,256 million) of ACM's revenues came from Mainland China in Q1. Still, Veeco is not growing at the same pace but has healthier cash flow metrics as pictured below.

{kind=link}

In conclusion, I believe the company's cheaper valuations already take into account geopolitical risks and it is not an opportunistic investment at this moment. While the management's update as to diversification is certainly welcomed, it is better to wait for a timeline with milestones as to the execution. In the meantime, this is a company to put on your watchlist due to the innovation dimension it brings to the world of semiconductors and its breathtaking growth.

For further details see:

ACM Research: Great Growth Story, But Geopolitically Risky