ACMR - ACM Research: Remains A Buy

2024-01-15 06:27:01 ET

Summary

- ACM Research's stock price increased over 20% last week after updating its revenue outlook for 2023 and providing positive guidance for 2024.

- ACM Research is positioned to reach $1 billion in revenue by 2026, driven by China's accelerating semiconductor investments and its portfolio expansion into new markets.

- The market is cautious about ACMR's future prospects due to the US-China chip war. We agree that this is a real risk, but not as severe as the market valuates.

ACMR Stock Soars on Updated Guidance

After announcing an improved revenue outlook for 2023 and a positive guidance for 2024, ACM Research ( ACMR ) saw its stock price increase by over 20% last week. The company now anticipates revenue of $530 million to $545 million for 2023, an increase from the previous estimate of $520 million to $540 million. For 2024, the company forecasts revenue of $650 million to $725 million, indicating its strong growth momentum in the semiconductor market.

Since our last coverage of the company 3 months ago, not much has changed in terms of company fundamentals. We reiterate our buy rating for ACM Research, as we are confident in the company's growth potential and attractive valuation. The company has a strong customer base in China, which is projected to continue its accelerated spending on mature node capacity. Furthermore, the company is advancing in broadening its product range and planning to penetrate new markets outside of China.

We also recognize the October 2023 US chip control expansions and their possible negative impact on ACMR’s business. We agree that the company deserves a lower valuation than the market average due to this risk, but not to this extent. The stock trades at a steep discount to its US competitors, who are still struggling with the semi downturn. Even with a very conservative valuation, we believe that ACMR is undervalued and has the ability to generate significant returns in the long run.

This article does a revaluation of the company, taking into account the latest revenue guidance for FY 2023 and 2024, as well as the impact of the expanded US-China chip restrictions.

We Expect $1B Revenue by 2026

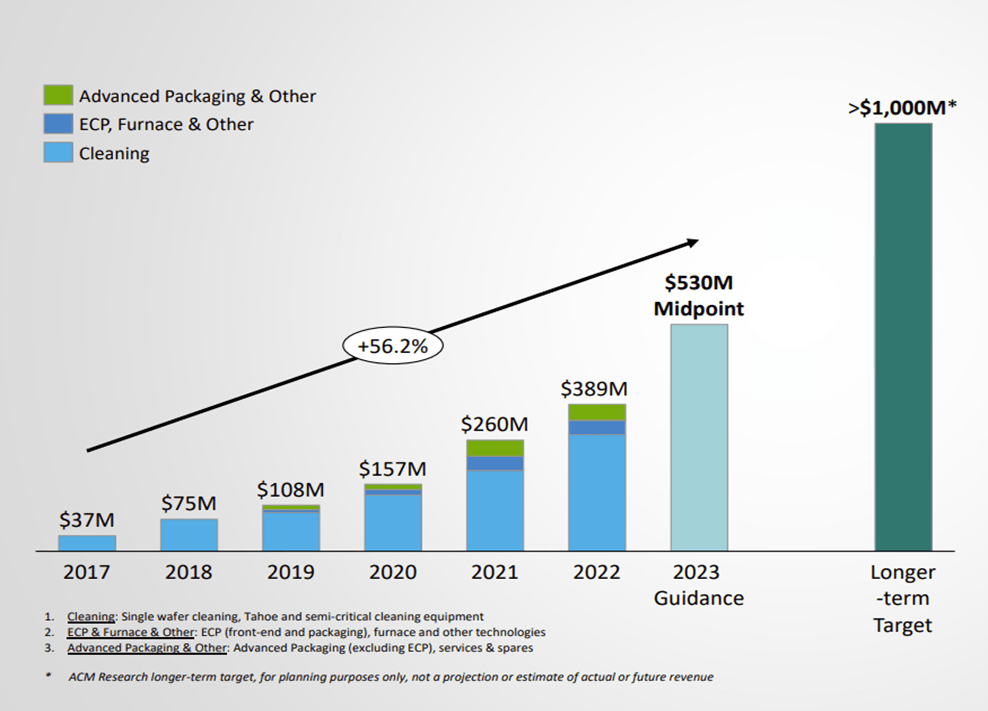

ACM Research, has been delivering strong revenue growth in the past few years, driven by its growing China customer base, and rapidly expanding portfolio. The company has been growing very fast at a 56% CAGR and is aiming to reach $1B revenue in a few years (see below)

ACMR Revenue Trajectory (ACMR Investor Presentation)

{kind=link}

Based on it its latest revenue outlook, we are projecting that ACMR will keep its growth momentum and achieve $1 billion revenue by FY 2026 easily (at a 3 year 25% CAGR), based on the following factors:

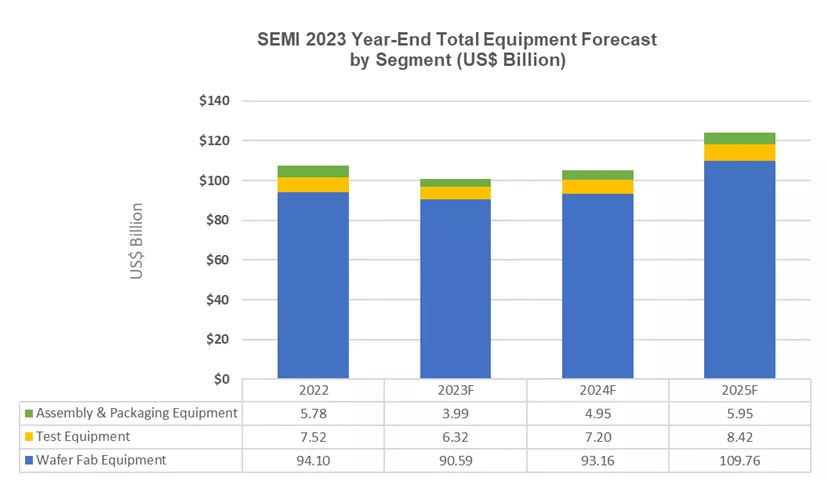

- China's accelerating semiconductor investments: China is the largest and fastest-growing market for ACMR, accounting for 97% of its revenue as per its 10-K . China is investing heavily in its domestic semiconductor industry, aiming to reduce its reliance on foreign imports and achieve self-reliance by 2030 as part of its Made in China plan . Global Semiconductor equipment sales is forecasted to reach record $124 billion in 2025 as per the Semi association report and China is projected to maintain the top position over the forecast period. This creates a huge opportunity for ACMR, as it leverages its strong relationships with leading Chinese chipmakers, and benefits from the increasing demand for its advanced cleaning and packaging solutions.

Global Semi Equipment Forecast (Semi Association)

{kind=link}

- ACMR's portfolio expansion : ACMR is not only focused on its core product line of single-wafer cleaning equipment, but also expanding its portfolio to address new and emerging market segments. The company has launched several new products in recent years, such as the Ultra C Tahoe system which is showing significant sales growth, contributing to a broad portfolio addressing nearly 90% of all cleaning processes.

- Expansion plans beyond China : ACMR is also pursuing growth opportunities in markets beyond mainland China, which will diversify its revenue sources and reduce its geopolitical risks. The company has established a sales facility in Oregon, US to provide sales and product demonstration capabilities in the region. The company has also secured an order from a large U.S. manufacturer in November 2023, marking its entry into the U.S. market. Also in Europe, company received an order for an Ultra C cleaning tool from a major European semiconductor manufacturer. In addition, the company has been making progress in Korea, where it has more than 150 employees and three facilities including sales, R&D labs, and small-scale production capabilities.

The US-China Chip War Risk

ACMR is a US-based company that operates in China, so it faces a significant risk from the ongoing US-China chip war. ACMR gets almost all its revenue from China and also relies on China for its supply chain, as it sources most of its raw materials, components, and equipment from Chinese vendors. Moreover, ACMR's main customers are Chinese semiconductor manufacturers, such as SMIC, Hua Hong, and Yangtze Memory, which are subject to US export controls and sanctions.

The US-China chip war poses several challenges and uncertainties for ACMR, such as:

- The US Chip controls could limit ACMR's ability to sell its products and services to its Chinese customers, as it may require additional licenses or approvals from the US government, or face potential penalties or fines for violating the US export regulations. In its 10-Q , ACMR states that these factors had a negative impact on its sales in the nine months ended September 30, 2023, and anticipates these factors will continue to have an adverse impact in future periods.

- It could disrupt ACMR's supply chain and increase its costs, as it may face difficulties or delays in obtaining the necessary materials, components, and equipment from its Chinese vendors, or have to seek alternative sources from other countries.

- It could damage ACMR's reputation and relationships, as it may be perceived as a hostile or unreliable partner by its Chinese customers, vendors, and regulators, or face political or legal pressures from the Chinese government.

ACMR has acknowledged the risk of the US-China chip restrictions in its SEC filings, and stated that it is monitoring the situation closely and taking appropriate actions to mitigate the impact. ACMR has also expressed its commitment to comply with all applicable laws and regulations, and to maintain its high standards of quality and service. However, ACMR also admitted that the US-China chip war could have a material adverse effect on its business and that it cannot predict the outcome or duration of the conflict.

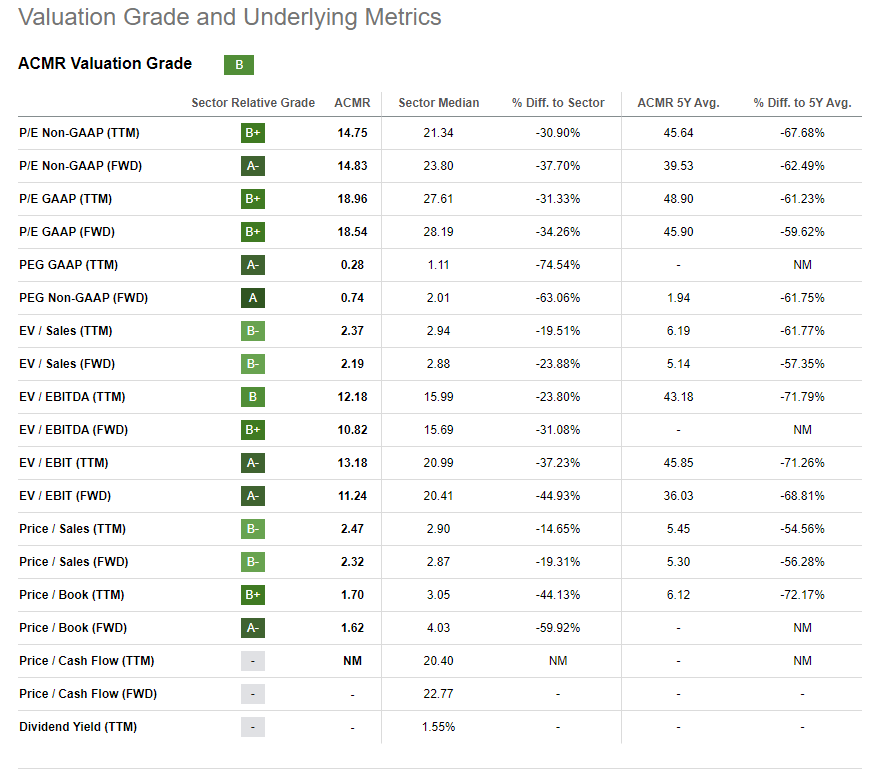

We acknowledge that investors have a valid reason to worry about the risk of the US-China chip war, which is reflected in the low valuation multiples of ACMR’s stock. The multiples (see below) indicate that the market is cautious about ACMR's future prospects. We agree that this is a real risk, but not as severe as the market thinks.

ACMR Valuation Grades (Seeking Alpha)

{kind=link}

Valuation Still Favorable

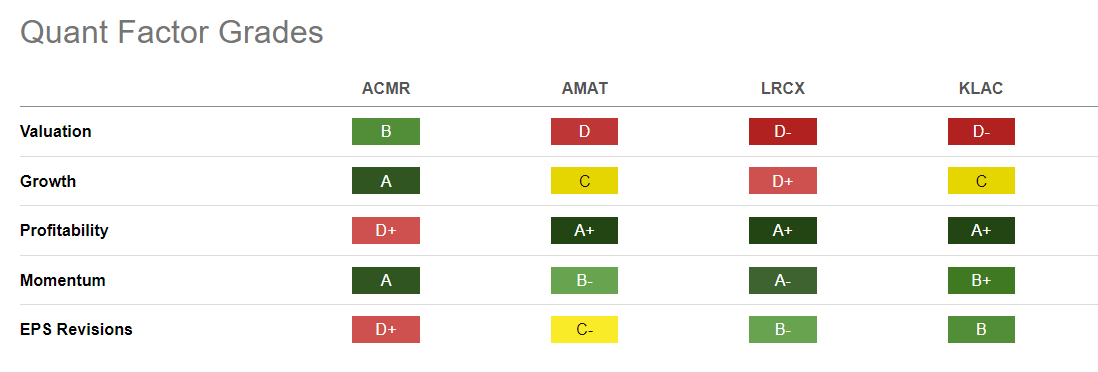

We think that ACM Research remains a good investment option, even after the recent rise in its price and the threat of the US-China chip war. Using Seeking Alpha's Quant grades, we can see how the big players of this industry are still struggling because of the semiconductor market downturn. Their growth has stalled and valuations have become expensive. ACMR is the only company that is growing double digit (38% YoY) and still has an attractive price valuation.

Peer Quant Grades (Seeking Alpha)

{kind=link}

The only downside for ACMR is its profitability grade, but this is understandable for a company that is growing fast and investing its cashflow in expanding its business by building R&D centers and factories. ACMR is on its way to match the profitability of its peers, and we can see the results of its efforts. In Q3, gross margin increased to 52.9% from 49.4% a year ago.

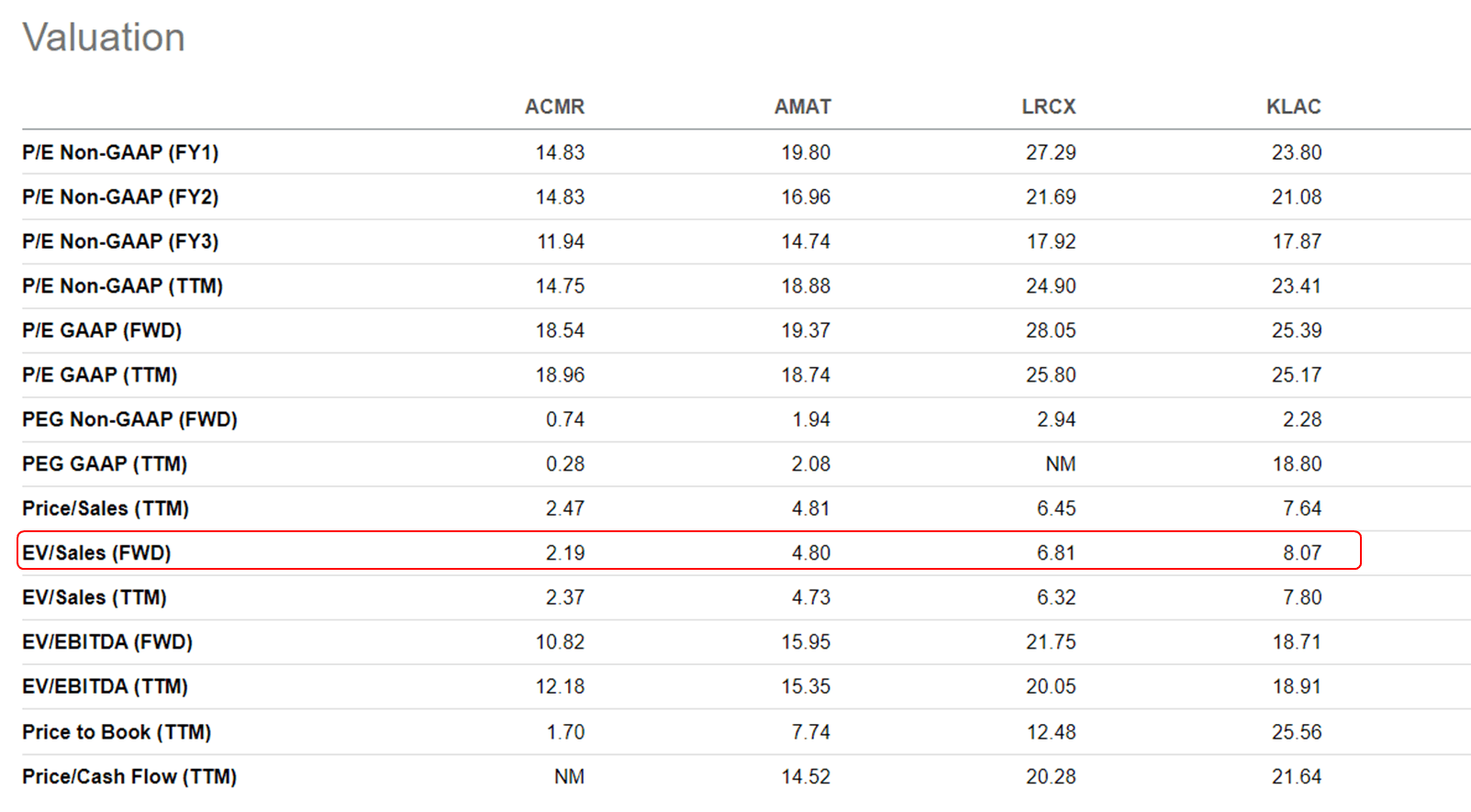

In terms of valuation, we want to look at the forward EV/Sales multiple. As we can see below, ACMR's forward EV/Sales is 2.19x, lowest among its rivals. Its closest rival, AMAT, is at 4.8x.

Peer Valuations (Seeking Alpha)

{kind=link}

As per the latest revenue outlook update, ACMR sales for FY24 are expected to be $690 million (midpoint guidance). If we use a conservative sales multiple of 2.5x and apply it to the current EV, we get a 1 year price target of $32.

This low 2.5x sales multiple is only about a third of the average of its rivals (6.6x). In our previous article , we used a 3x sales multiple, which we are reducing further to 2.5 because of the expanded chip export restrictions imposed by the US government in October 2023.

Conclusion

ACM Research is a promising investment in the semiconductor equipment industry, which is constantly evolving. The company has a diverse product range, a strong presence in the fast-growing Chinese semi market, and a plan to expand globally. Based on its recent revenue forecast, we expect ACM Research to sustain its growth and reach its $1 billion revenue goal by FY 2026.

We also recognize the US-China chip war risks that could have a negative impact on its business. However, we believe that the market has already priced in this risk, as the company’s stock valuation is very low relative to its peers.

Therefore, we reiterate our Buy rating for ACM Research and maintain our 1 year price target of $32.

For further details see:

ACM Research: Remains A Buy