ACMR - ACM Research Shot To The Moon Too Quickly; Not A Good Time To Start A Position

2023-12-01 07:42:27 ET

Summary

- ACM Research's robust growth in China is already priced in, making it unattractive at its current price level.

- The company has strong financials with ample liquidity and low debt levels, reducing the risk of insolvency.

- While the company's efficiency and profitability metrics have room for improvement, its high inventory levels indicate strong demand for its products.

Investment Thesis

After rallying around 100% in the last year, I wanted to take a look at ACM Research ( ACMR ) to see if it is still a good time to start a position. Unfortunately, the robust growth in China is already priced in, in my opinion, therefore, I will be waiting for a pullback. The company has a lot of potential in the long run, however, risk/reward is not enticing at this price level.

Overview of the Company

ACM Research is a global leader in high-performance, cost-effective equipment in the semiconductor sector. The purpose of the company's products is to clean and process technologies that assist in wafer manufacturing. Wafer manufacturing is the core process of creating semiconductors. The equipment is used to remove impurities, polish the wafers to make them a smooth surface, and apply thin films of materials onto them. The company helps to make sure that the components inside the devices are clean, smooth, and function properly.

Financials

As of Q3'23 , ACMR had around $305m in liquidity, against $40m in long-term debt. This is a great position to be in because the short-term investments that the company has more than cover the annual interest on debt, which means the debt levels are not dangerous for the company. As of 9 months ended September 30, interest income was over $6m while interest expense was at around $2m. ACMR can easily take on more debt to fund its operations if it wants, so it is safe to say the company is at no risk of insolvency. There are ways that the company could complement its operations via taking on more debt for strategic acquisitions, however, it is not necessary since the company has a huge pile of cash that is waiting to be utilized for further growth of the company.

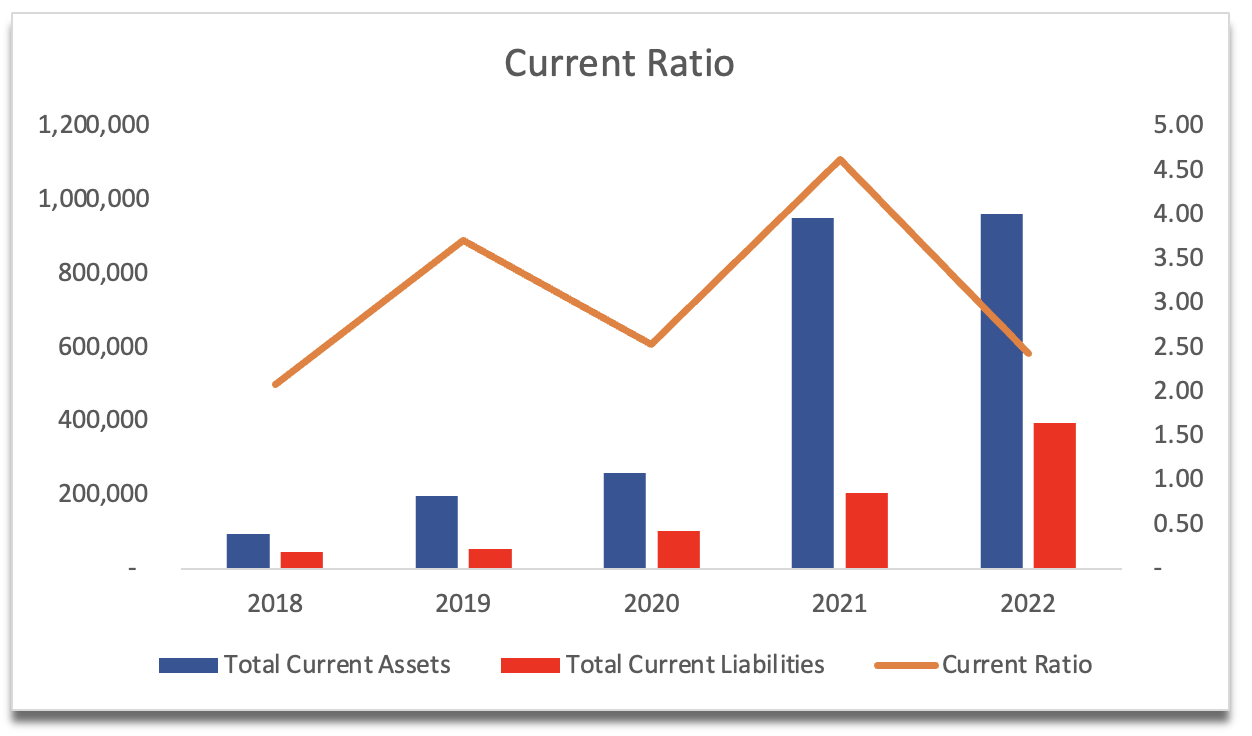

ACMR's current ratio has come down slightly over the last couple of years, which is not a bad thing. I believe has become more efficient at utilizing its assets than it was back when its current ratio stood at around 5 in FY21. I believe that a company should have a current ratio between 1.5 and 2.0 as I believe this is an efficient range. It tells me that the company has plenty of liquidity to pay off its short-term obligations and is not hoarding capital for no reason, that could be used for further growth of the company. As of Q3'23, the company´s current ratio stood at around 2.3, which is slightly above the range I mentioned but it's not a bad thing. It is better to have a strong ratio than below 1.

{kind=link}

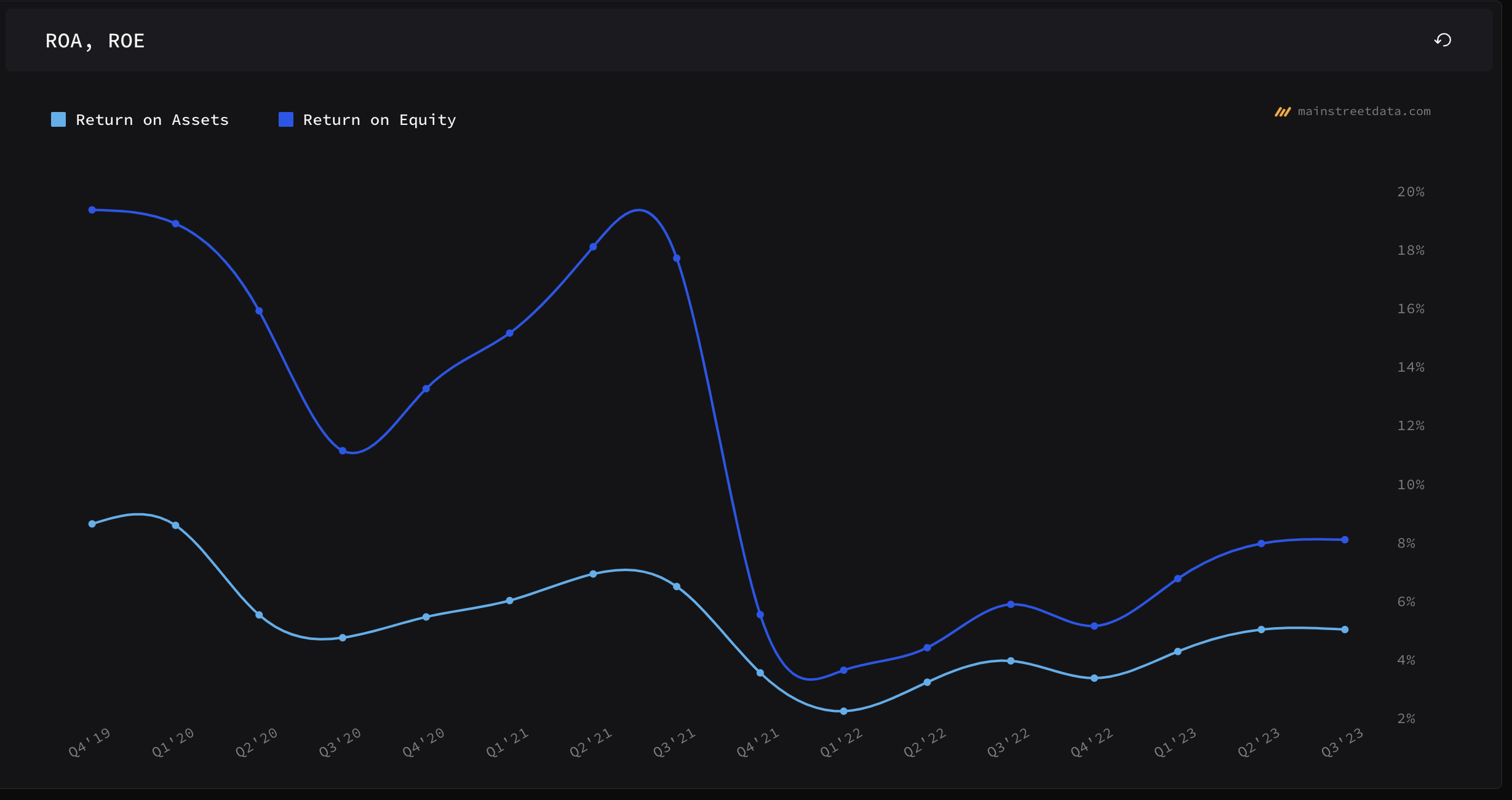

Speaking of efficiency, the company's ROA and ROE have recovered from the bottoms of Q1'22, however, still leave a lot to be desired when looking at what the company managed to achieve in the prior years. For example, FY19 was the height of efficiency for the company, from then on it started to go downhill. This change was driven by the company increasing its inventory levels and its STAR market IPO in Shanghai, which raised around $570m in cash for the company. So, when you look at why the returns have come down, it is not the worst scenario, however, I would like to see the company utilizing the new assets much more efficiently in the future, and hopefully, the company will put the new cash it raised to good use.

{kind=link}

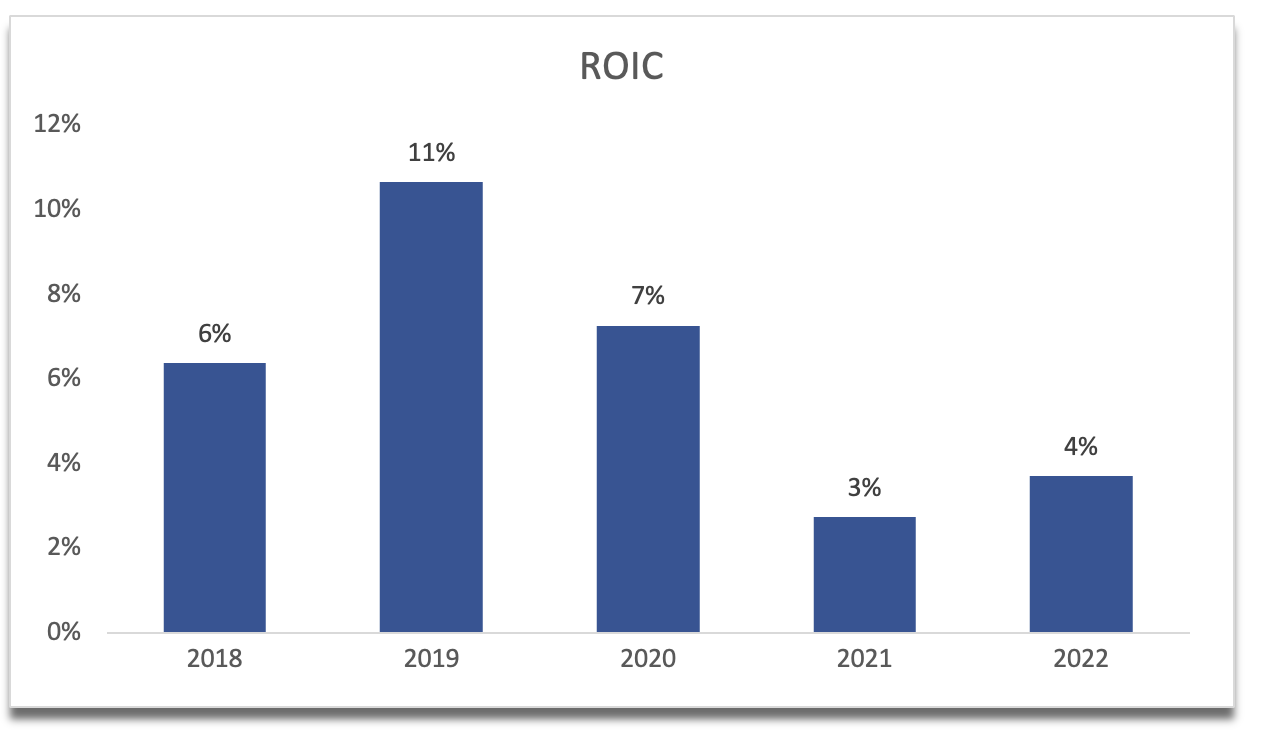

Going over to profitability, the company's return on invested capital has decreased for the same reason as above and is exhibiting the same slight recovery but a far cry from what it used to be. The management will have to try hard to use the available capital it received to good use to improve these metrics going forward, and only time will tell if they are successful.

{kind=link}

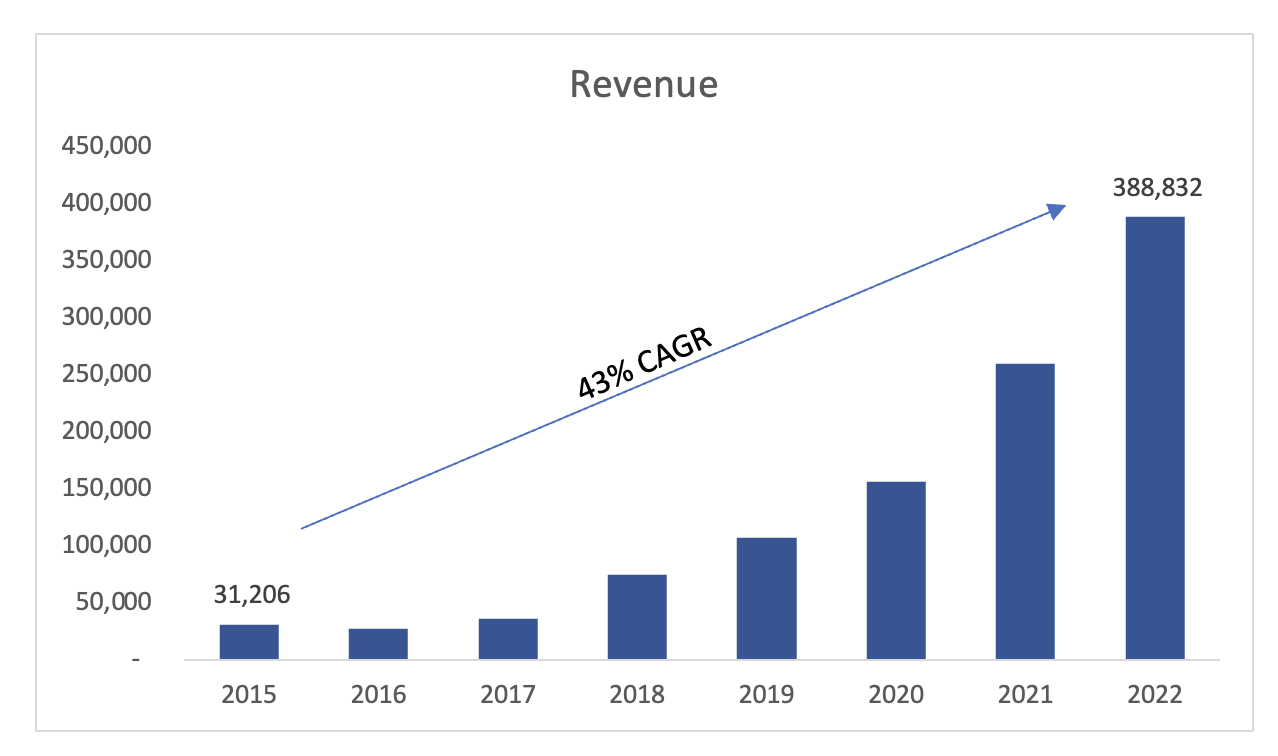

In terms of revenue, ACMR has been performing very well in this area, having achieved around 43% CAGR over the last 7 years, which is very impressive. The demand for the company's products and services is evident, and the increase in inventory levels over the same period is justified. Analysts are estimating a very high growth in the next few years; however, it is not as robust as the company managed to achieve over the last while. I am going to take these estimates with a grain of salt because it is impossible to predict what the company is going to do a year from now, let alone 2+ years as many variables can affect the company's performance. It is not very hard to predict what is going to happen a year from now because the management usually gives us a ballpark of numbers that we can use. So, is the company going to grow at that historical rate for a little while longer, or that stage of growth is gone now? That is what we have to decide in the later section.

{kind=link}

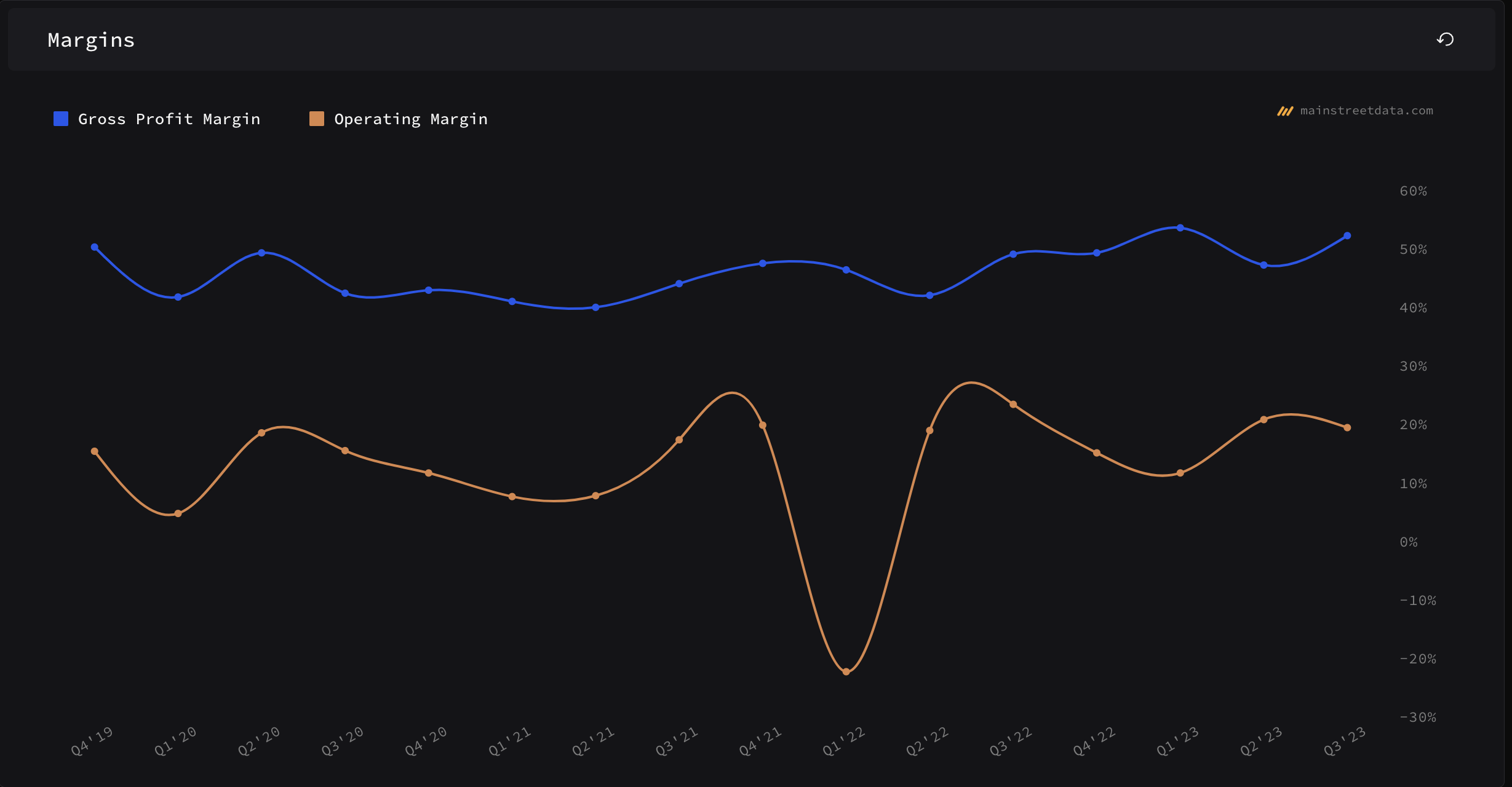

In terms of margins, these have been stable over the last few years, however, FY19 saw the best levels. In more recent years, the company's bottom line has been affected by minority interest, which took around $11m from the bottom line. I would like to see the company improve margins once again, which it seems that it has in the most recent quarters.

{kind=link}

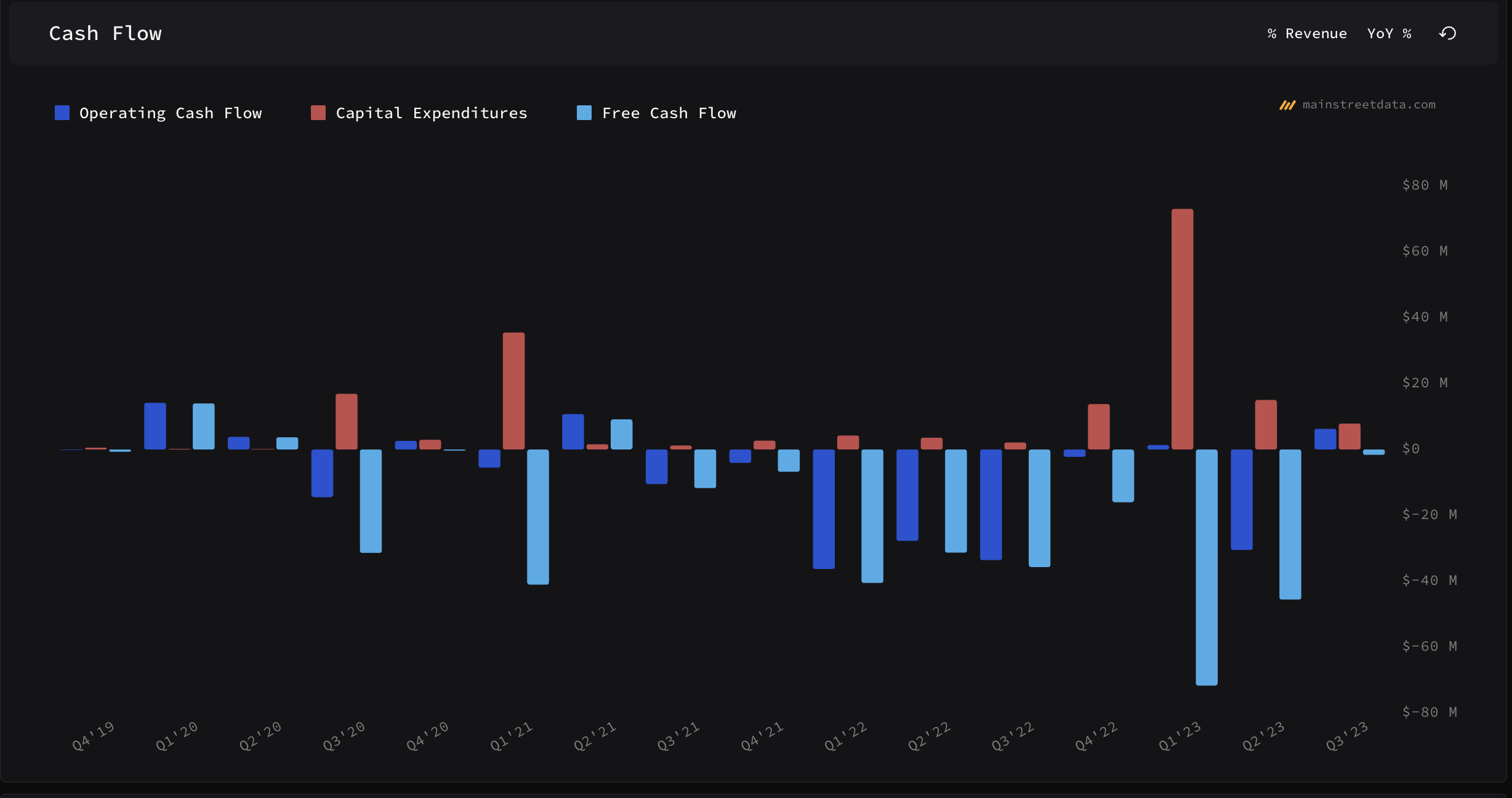

ACMR has been burning through cash right for many years now, which is not ideal, however, the company is still relatively young, and I don't think this is an issue right now, given that the company is still growing at an amazing pace. However, if it continues to operate like this for a very long time, I expect the company to offer more shares to the public, which will dilute shareholders further. If the company can grow at this rate, I don't think the share dilution will affect shareholders too much.

{kind=link}

Overall, I would like to see profitability and efficiency metrics improve in the near future, and I think they will because it is reinvesting back into itself, which I hope will prove to be very profitable, but only time will tell if it is successful.

Comments on the Outlook

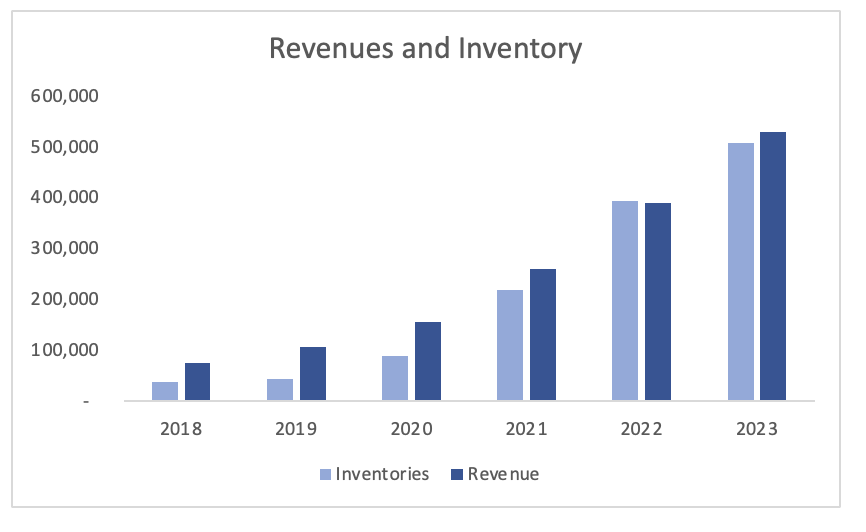

The biggest item I'd like to address is the company's hoarding of inventory, which is a good sign and a potential risk. As of September 30 '23, the company has increased its inventory levels in anticipation of high demand by around 30% from FY22. This is to support " a higher level of expected shipments for the next several quarters, and to reduce the risk of supply chain delays to meet anticipated customer demand for the Company's products. " (as per Q3 10-Q). This seems to be a positive in my opinion. The company expects high demand for the products for the next while, which will generate a decent number of sales and cash flow. It is interesting to note that Inventory has been going hand in hand with sales numbers in recent years, so it is not surprising that the company increased inventory by around 30% while expected sales are around 36%.

{kind=link}

At some point, I believe the management will have to moderate the company's inventory levels especially if the product is not selling as anticipated, which will cost the company a fortune in the future.

Most of the company's revenues come from mainland China, so the risk would come from geopolitics between the US and China, however, I think this is minuscule and the chip ban doesn't affect the company. The company is still headquartered in the US, so it is unknown whether the company will experience any effects from the US ban on semiconductors in China. The company isn't producing any semis, so, the effects will be minimal.

Since most of the revenue is coming from China, and because of these bans and geopolitical instabilities, China is trying to become more self-reliant, which will be beneficial for ACMR as we can see through the robust demand for its products in the mainland. The Chinese government is injecting subsidies, grants, and anything else that could benefit its domestic production of semiconductors and their quality control, which ACMR is feeling the benefits of already. The country's efforts to become self-reliant are just beginning so I would expect a lot of growth in domestic companies that are helping the country advance its semiconductor technology and become self-efficient.

Valuation

In terms of revenue, I believe that focusing on China, which is going to have a big growth in the semiconductor industry for the next decade, will be very beneficial for ACMR. So, I would expect high-double-digit growth in sales for a good few years going forward. However, I do like to take on a conservative mindset when it comes to valuation for that extra margin of safety. Below are my assumptions for revenue growth that I believe are very achievable given the robust demand in China.

{kind=link}

In terms of margins and EPS, I went with slight improvements from FY22, however, very minimal to keep it safe. Below are those assumptions. According to my calculations, the company with such assumptions is trading at a ´23 forward PE ratio of around 13.

{kind=link}

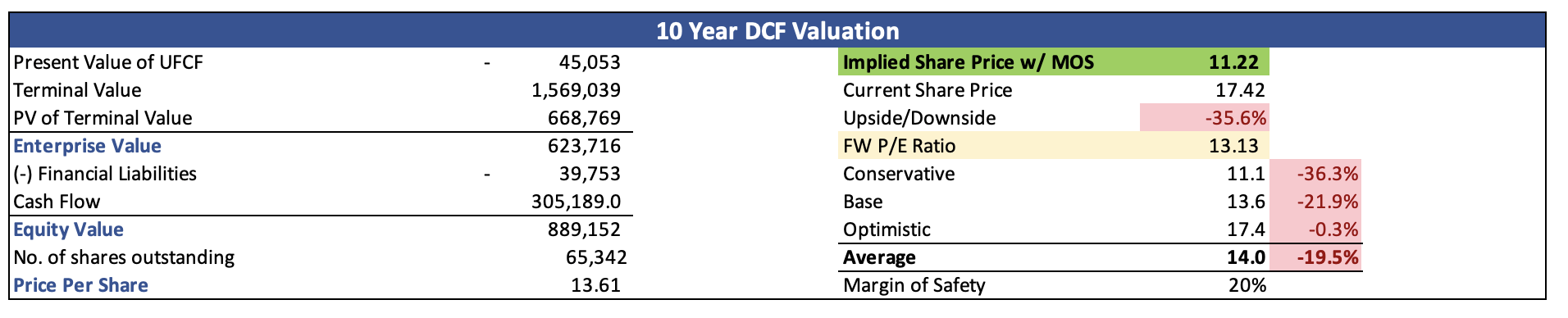

I also went with the company´s WACC of around 9% as my discount factor and 2.5% terminal growth rate. On top of these assumptions, I added another 20% margin of safety to the intrinsic value just to be on the safer side. With that said, the ACMR´s intrinsic value is around $11.22 a share, which means that the company is trading at a premium to its fair value.

{kind=link}

Closing Comments

I am recommending a hold rating because of the company´s elevated inventory levels, which pose a big risk in my opinion, especially if the company may not be able to sell through. I would like to see improvements in the financial metrics mentioned above, as right now it looks like the company is not as efficient as it once was.

On the other hand, the rapid increase in inventory signals that the demand is very high for the company's products and the top-line growth could be phenomenal in FY24 and beyond, however, I would have to wait and listen to a couple more earnings calls to see what the management´s visibility for the future is and whether it demand for the company´s products will continue to increase going forward.

Maybe my revenue assumptions are too conservative, however, seeing the company´s share price has already increased by around 100% in the last year, I don't feel comfortable starting a position at the recent top. $20 seems to be a decent resistance and I wouldn't be surprised if the company continues to trend down to around the $12-$15 range in the next few months, especially if the next earnings are not what everyone expects the company to do.

For further details see:

ACM Research Shot To The Moon Too Quickly; Not A Good Time To Start A Position