ADDYY - adidas AG: Inventory Reduction Encouraging But Challenges Remain

2023-11-10 10:39:01 ET

Summary

- adidas AG has successfully reduced its excess Yeezy inventory, but earnings have yet to recover.

- Q3 2023 earnings show a decline in gross profit and net sales in Europe and North America.

- In spite of the company's resilience over the past year, I do not take a bullish view on adidas AG at this time.

Investment Thesis: Earnings growth needs to see a substantial improvement to justify the upside in adidas AG's (ADDYY) stock. As such, I do not take a bullish view of adidas at this time.

In a previous article back in August, I made the argument that while adidas AG has seen an encouraging recovery in stock price, it was my view that operating profit needs to see a significant recovery to justify further upside.

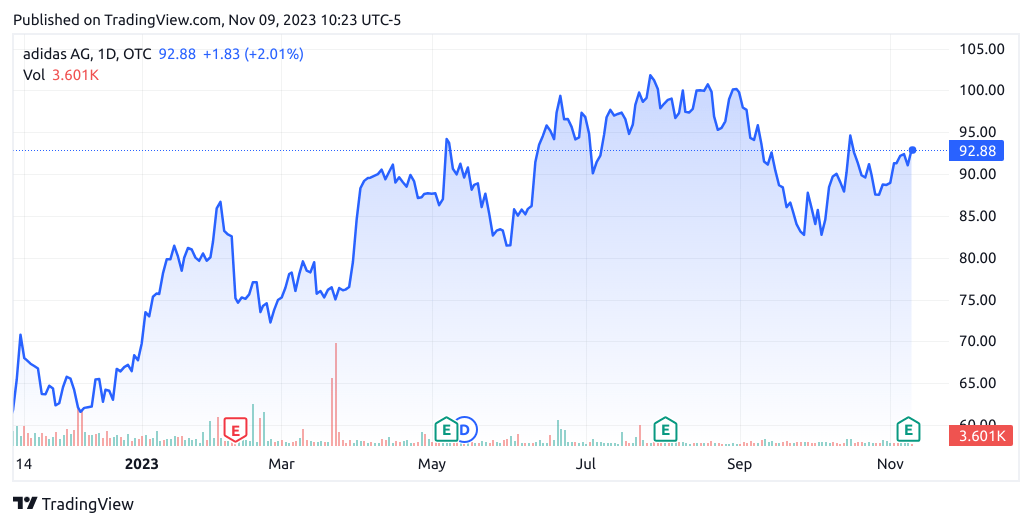

Since then, the stock has descended to a price of $92.88 at the time of writing:

{kind=link}

The purpose of this article is to assess whether adidas AG has the ability to see continued growth from here taking recent performance into consideration.

Performance

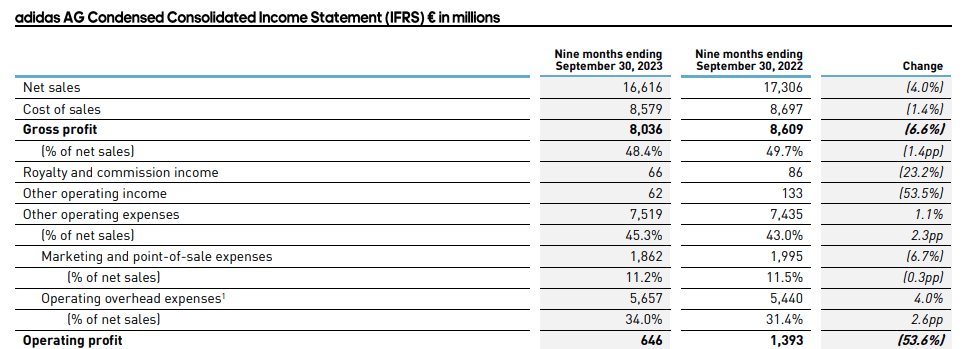

When looking at Q3 2023 earnings results for adidas AG (as released on November 8), we can see that gross profit is down by just over 6% from that of last year - while after deducting for expenses - operating profit is down by €747 million from that of the same period last year.

{kind=link}

Additionally, when we look at net sales by region for Q3 since 2019 (with 2020 excluded due to the effects of the COVID-19 pandemic), we can see that net sales are down across both Europe and North America - but the drop across the latter region has been more stark at 15% as compared to just under 3% for Europe.

Figures sourced from Q3 2019 and Q3 2023 adidas AG Press Releases. Heatmap generated by author using Python's seaborn library.

I had previously made the argument that one of the main factors behind whether adidas AG would see a rebound in growth going forward would be the extent to which the company was able to reduce its excess inventory following the fallout with Ye late last year. Given that Yeezy sneakers had formed a key part of the company's offering in North America, simply writing off such inventory would have come at too high a cost and adidas had to sell off its existing inventory to bolster operating profits once again.

With regards to short-term liquidity, we can see that the quick ratio of adidas AG (calculated as total current assets less inventories all over total current liabilities) has seen a slight increase from that of the June quarter, and we can also see that inventories are down by just over 23% from that of the same quarter last year.

| Sep 2021 |

| Sep 2022 |

| Jun 2023 |

| Sep 2023 |

| Total current assets |

| 14142 |

| 13217 |

| 11151 |

| 10520 |

| Inventories |

| 3664 |

| 6315 |

| 5540 |

| 4849 |

| Total current liabilities |

| 8517 |

| 10605 |

| 8726 |

| 8178 |

| Quick ratio |

| 1.23 |

| 0.65 |

| 0.64 |

| 0.69 |

Source: Figures sourced from adidas AG Q2 and Q3 2023 Press Releases. Figures are provided in € millions, except the quick ratio. The quick ratio was calculated by the author.

While a contributing factor to a lower quick ratio has been lower total current assets - the fact that inventories have seen a significant decrease over the past year (and are approaching 2021 levels) is encouraging. This is an indication that adidas has continued to reduce its excess Yeezy stock and while gross profit had seen a decline of 6.6% as compared to the same quarter last year - this would have been significantly greater had adidas not been able to reduce its Yeezy inventory.

From a longer-term standpoint, we can see that while long-term debt relative to total assets is higher than that of last year, long-term debt is also down from that of the last quarter.

| Jun 2022 |

| Sep 2022 |

| Jun 2023 |

| Sep 2023 |

| Long-term debt |

| 2459 |

| 1958 |

| 2938 |

| 2434 |

| Total assets |

| 21324 |

| 21750 |

| 19338 |

| 18720 |

| Long-term debt to total assets ratio |

| 11.53% |

| 9.00% |

| 15.19% |

| 13.00% |

Source: Figures sourced from the adidas AG Q2 and Q3 2023 Press Releases. Figures provided in € millions, except the long-term debt to total assets ratio. Long-term debt to total assets ratio was calculated by the author.

My Perspective

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, the fact that adidas has continued to reduce its inventory levels has been encouraging in spite of sales and gross profit remaining lower than that of the same period last year.

The big fear among investors concerning adidas late last year was that the company would not be able to sell its inventory of Yeezy sneakers following the public fallout with Ye and that the company's sales and gross profits would take a big hit as a result.

However, we see that while there has been a decline in these metrics - adidas has managed to significantly reduce its inventory to keep sales and profit levels reasonably stable. Additionally, the fact that adidas has also managed to increase its quick ratio and decrease its long-term debt from that of the last quarter is also encouraging and signals that the company has not had to incur higher debt loads to mitigate the initial issue of excess Yeezy inventory.

Risks

In terms of the potential risks to adidas AG at this time, the fact remains that in spite of the company's progress in reducing its inventory over the past year - adidas may still be looking at a €300 million write-off of remaining Yeezy inventory while also incurring one-off costs of €200 million in relation to the company's strategic review.

As such, earnings growth has remained negative, and we see that the company's EV to EBITDA ratio remains near a 10-year high while EBITDA per share remains at a 10-year low:

YCharts

As such, I take the view that adidas will need to demonstrate a substantial recovery in earnings growth before we can see further upside in the stock and this is unlikely to happen until such time that the company has gotten over hurdles relating to its Yeezy inventory issues as well as other one-time costs.

Conclusion

To conclude, adidas AG has shown resiliency over the past year by reducing its inventory and also reducing its long-term debt in the past quarter despite challenging circumstances.

With that being said, earnings growth needs to see a substantial improvement to justify an upside in the stock. As such, I do not take a bullish view of adidas at this time.

For further details see:

adidas AG: Inventory Reduction Encouraging, But Challenges Remain