SPY - ADX: 4 Reasons To Be Cautious Despite Recent Outperformance

2024-01-02 00:30:11 ET

Summary

- Adams Diversified Equity Fund seeks long-term capital appreciation and dividend income by investing in large-cap US companies.

- ADX has a very long history and has outperformed the S&P 500 over the past 10 years.

- The fund charges a high management fee and has a fixed distribution policy, which creates a potential tax drag.

- I am initiating ADX with a hold, but would turn more bullish if the discount to NAV were to widen moderately from current levels.

The Adams Diversified Equity Fund ( ADX ) is a closed end fund ("CEF") which seeks to deliver long-term capital appreciation by investing in a blend of high quality, large-cap U.S. companies. The fund seeks to beat its benchmark, the S&P 500, and consistently distribute dividend income and capital gains to shareholders.

The fund is committed to an annual distribution rate of at least 6% and currently is not levered.

ADX has a very long history and traces its roots all the way back to 1929. The fund has delivered strong performance in recent years. Over the past 10 years, ADX has delivered a total return of 233% vs a total return of 210% delivered by the S&P 500 during the same time.

While this fund has certainly stood the test of time and has delivered solid recent results, I believe there are 4 reasons why investors should be cautious CEF right now:

1. High Management Fee

2. Research suggests historical outperformance does not have predictive power for future outperformance

3. Sector neutral approach makes it more difficult to generate alpha

4. Distribution policy creates a potential tax drag

1. High Management Fee

ADX charges a total expense ratio of 0.62%. This compares to an average equity mutual fund expense ratio of 0.44% and an average equity ETF expense ratio of 0.11%. Comparably, the SPDR S&P 500 ETF Trust ( SPY ) charges a total expense ratio of 0.0945% while the iShares Core S&P 500 ETF charges a total expense ratio of 0.03%. In terms of active fund comparisons, the T. Rowe Price Capital Appreciation Equity ETF ( TCAF ) charges a total expense ratio of 0.31% while the EA Bridgeway Blue Chip ETF ( BBLU ) charges a total expense ratio of 0.15%.

While I am generally skeptical of high fee products, I do believe active funds can earn their fees under certain circumstances. For example, I recently initiated BBLU with a Buy rating in my piece EA Bridgeway Blue Chip ETF: A Solid Low Fee Active ETF .

That said, the U.S. Large Blend market category has proved challenging for active managers historically. As shown by the table below, just 9.8% of active U.S. Large Blend funds have outperformed their respective benchmarks over the past 10 years. Furthermore, active U.S. Large Blend funds in the lowest fee quintile tend to have a somewhat better chance of outperforming vs active funds in the highest fee quintile.

For these reasons, I view ADX's 0.62% total expense ratio as a key negative when evaluating the fund.

{kind=link}

2. Research suggests historical outperformance does not have predictive power for future outperformance

Recent research published by Yale SOM professor James Choi suggests that historical mutual fund outperformance does not have predictive power regarding future outperformance. Additionally, a recent study published by Standard & Poor's also argues that there is no evidence of persistence in terms of active mutual fund outperformance.

My view is that one of the reasons for this is a tendency for different strategies to outperform over different time periods. For example, funds focused on growth may experience a period of outperformance only to see value titled funds outperform in the following period.

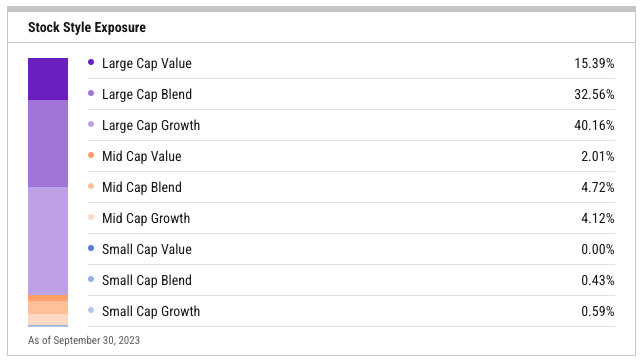

In the case of ADX, I believe the tilt is to focus on larger companies as the fund is focused on large cap equities. Currently, ADX has 11.9% exposure to mid and small capitalization companies. Comparably, the SPY has total exposure of 18.6% to mid and small capitalization companies. This tilt towards larger capitalization companies has likely been a positive performance driver for ADX. However, it is highly uncertain that this phenomenon will continue going forward.

{kind=link}

3. Sector neutral approach makes it more difficult to generate alpha

ADX follows a sector neutral strategy. This means that sector exposure for ADX is roughly inline with the S&P 500. I believe this strategy will make it challenging for ADX to deliver outperformance going forward as it eliminates one key driver of potential alpha, which is sector weights. Over or under weighting various sectors allows an active manager to take active risk vs the benchmark in addition to differences in stock selection within each sector.

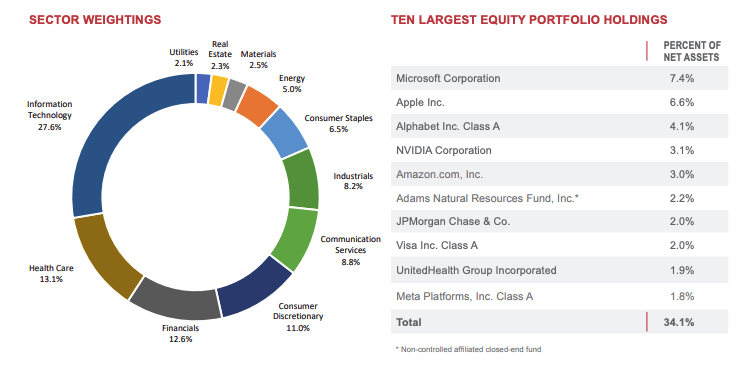

Additionally, many of ADX's top holdings are also top holdings in the S&P 500 suggesting the fund is taking fairly limited active risk. As shown by the table below, it should be noted that ADX's top 5 holdings are also the top 5 holdings in the S&P 500. While the weightings are slightly different, the overall composition suggest that ADX is currently keeping exposures fairly close to its benchmark. I view this as problematic in terms of go forward outperformance potential given the fund's relatively high fee makes it challenging to add value.

{kind=link}

{kind=link}

4. Distribution policy creates a potential tax drag

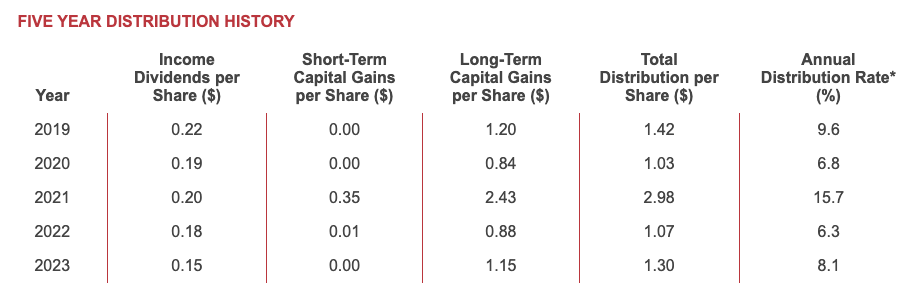

ADX has a stated minimum distribution policy of 6% each year. I view this as a negative as it is very tax inefficient relative to low distribution products. Furthermore, as shown by the table below ADX has actually distributed much more than 6% on average over the past few years.

I view ADX's high levels of distributions as problematic as investors are forced to pay tax on these distributions when the occur. This means that long-term ADX holders face a tax drag in terms of compounding their investment compared to passive low distribution products such as SPY. Moreover, the high level of distributions also gives ADX holders less control of the timing of tax realization. This is particularly relevant for investors who plan to hold ADX until death and might otherwise benefit from a step up in basis which leads to no tax on the capital gains. Moreover, other investors may be in a high tax bracket today but will be in a lower tax bracket in the future. Thus, these investors would be better off realizing capital gains once they are in the lower tax bracket.

{kind=link}

What Would Make Me More Positive on ADX

Currently, ADX is trading at a 13.9% discount to NAV. While this may be attractive on an absolute level, I do not view it highly attractive relative to ADX's average historical discount of 14.4% over the past 10 years. Thus, one thing that would make me more positive on ADX is if the discount to NAV were to widen closer to 17% or 18%.

Another thing that would make me more bullish on ADX is if the fund were to announce actions intended to close the discount to NAV. Potential actions include a more aggressive share repurchase program or conversion into an open ended funds structure.

ADX has an active repurchase program in place and is able to repurchase shares when they trade at a discount to NAV of 10% or more however ADX is not mandated to repurchase shares until the discount exceeds 15% for 30 consecutive trading days. Moreover, the fund will engage in a proportional tender offer to repurchase shares when the discount exceeds 19% for 30 consecutive days (limited to once per 12 month period.)

Thus, if ADX were to trade at a discount of 17%-18% to NAV I would become more bullish given the potential catalysts of more aggressive repurchases or a tender offer if the discount widened further from there.

Conclusion

ADX has delivered solid performance over the past 10 years and has outperformed the S&P 500. However, I am not confident that outperformance will continue going forward.

ADX has a fairly high expense ratio and is part of a market segment which has proved extremely challenging for active managers historically. Moreover, recent research suggests that prior outperformance by an active fund is not an indicator of future outperformance.

I believe the sector neutral strategy employed by ADX makes it more difficult to generate alpha, as it means there is one less lever for fund mangers to take active risk vs the benchmark. Furthermore, ADX's largest holdings are fairly close to the S&P 500 which may make it difficult to generate alpha in the near-term.

ADX's fixed distribution policy gives investors less control over the timing of capital gains realizations. Moreover, the high distribution also creates a tax drag in terms of compounding.

One thing that would make more bullish on ADX is if the discount to NAV were to widen closer to 17% as the fund would likely get more aggressive in terms of repurchasing shares.

For further details see:

ADX: 4 Reasons To Be Cautious Despite Recent Outperformance