LMT - AeroVironment: Strong Order Backlog Is Boosting Growth Prospects In 2024

2023-12-14 06:07:21 ET

Summary

- AeroVironment reported strong Q3 FY24 earnings, beating revenue and earnings estimates and raising its guidance for the third consecutive quarter.

- The company is benefiting from the growing demand for unmanned systems and remotely operated machines in response to increasing geopolitical tensions worldwide.

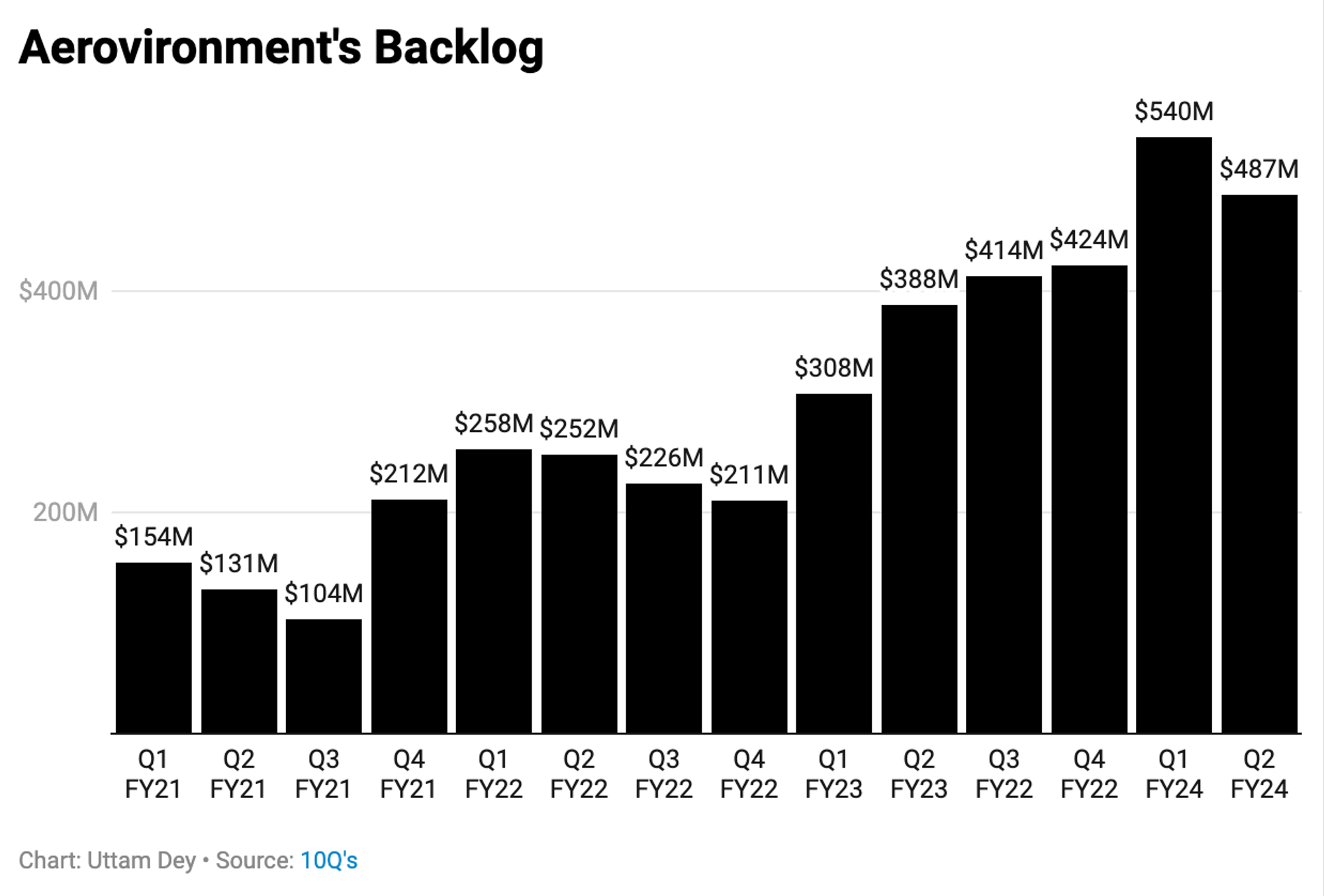

- AeroVironment has a significant volume of order backlog, particularly for its unmanned aerial systems, and is able to recognize a higher portion of its backlog compared to other defense contractors.

- My model suggests the fair value of the stock would be at approximately $165, given the current share count. This represents a 34% upside from current price levels.

Editor's note: Seeking Alpha is proud to welcome Uttam Dey as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

AeroVironment (AVAV) reported Q3 FY24 earnings that impressively beat revenue and earnings estimates. It even raised its FY24 guidance three quarters in a row. However, post-earnings, the stock fell 10% as investors were expecting the company to guide for EPS growth of 116%. Given where the stock is currently trading, while reviewing management's guidance for FY24/25 and beyond, as well as their focus on financial discipline, I believe the stock is undervalued and there is a 34% upside from current levels. In this post, I will walk you through why I think there is still upside in this stock.

Significant Growth in Order Backlog

There have been a growing number of geopolitical tensions rising in different parts of the world after the pandemic. It started with the Nagorno-Karabakh conflict in the Caucasus regions contested between Azerbaijan and Armenia in 2020. Then the world saw how Russia invaded Ukraine in 2022, and later we witnessed the rise of tensions between Israel and Palestine. The frequency with which geopolitical conflicts have been rising has forced many nations to reconsider their military budgets and allocate higher budgets relative to the previous decade. For example, in the USA, the CBO projects that the Department of Defense (DoD) will increase defense spending by ~3.6% every year until 2033. The last time military budgets rose at this pace every year was during the USA's invasion of Iraq.

However, this time around, with technology proliferating in every industry, governments are being selective in the areas in which they allocate specific defense budgets. In my opinion, this is where AeroVironment stands to greatly benefit from the spending patterns of the U.S. government and allied nations. Some of the conflicts that I've highlighted previously, such as the Nagorno-Karabakh conflict and Russia/Ukraine, have provided other nations with conclusive blueprints as to how wars can be fought remotely using unmanned systems and remotely operated machines. For example, Ukraine has been relying heavily on the TB2 Bayraktar drones supplied by Turkey's Baykar Technologies. The same defense company's drones were used by Azerbaijan in its conflict against Armenia in 2020. This created a massive demand for Baykar's drone technology, propelling it into SIPRI's Top 100 Defense Companies of the World as its revenue grew by 94% last year.

I believe much of the momentum in demand for defense drone technology has spilled out into other regions of the world, and AeroVironment is one of the defense companies that is benefiting from this trend. The U.S. defense contractor has seen its funded backlog rise a respectable 25% YoY in the most recent Q2 FY24 quarter. This is after the drone manufacturer's backlog surged 75% YoY in the previous quarter.

{kind=link}

The biggest source of AeroVironment's backlog stems from the demand for their Unmanned Systems (UMS) products, primarily unmanned aerial systems that operate at comparatively lower altitudes and collect tactical information from the skies while also carrying critical payloads for the army. While AeroVironment does not break out its backlog by product vertical, looking at their most recent quarter , one can notice that UMS revenue more than doubled versus the same period last year.

Another advantage AeroVironment has is its ability to recognize a higher portion of its backlog compared to other defense contractors in this space. Usually, large contractors like Lockheed Martin ( LMT ), RTX Corp. ( RTX ) are able to recognize around 1/3 of their backlog in the current financial year while usually leaving the rest of the backlog to be recognized in the following financial year or beyond. For example, Lockheed Martin states that it will recognize just 35% of its backlog in the current fiscal year, as per its most recent quarterly filing . However, in AeroVironment's case, the company is able to ship products to their clients much faster than most other defense companies. Per its most recent Q2 FY24 filings , it will recognize ~60% of their existing backlog of $487 million in this financial year, thereby significantly improving the outlook for shareholder equity.

AeroVironment Stock is a Buy

AVAV is now trading at 62x forward earnings, which I believe will stay at a premium relative to peers as the business continues to ride on the ongoing secular uptrend, driven by demand for higher ammunition inventory restocking cycles. Relative to its peers, AVAV is on track to grow its revenues and earnings at a much faster pace in double digits compared to its peers, which are growing their revenues in single digits.

If we take a more fundamental approach, AVAV is a buy, given my set of assumptions. Let's start with revenue projections. AeroVironment's own management forecasts another strong year of revenue growth of ~28.6%, between $685Mn and $705Mn for FY24. This is quite an impressive growth rate given that AeroVironment is outpacing its 5-year revenue growth rate by 234%. If the company is able to grow its revenue at an average rate of 18% for the next 5 years and then slow down at a pace of 5% after that, while maintaining its EBITDA margin at 18%, aided by operating leverage, and meanwhile growing its capital expenditure in line with the revenue growth rate, the company would be able to generate free cash flow at a 13% margin.

Assuming that AeroVironment's cost of capital remains at 7-8%, the fair value of the stock would be approximately $165, given the current share count. This represents a 34% upside from current price levels.

Risks to the Thesis

Backlog Growth May Slow Down

Like most other defense stocks, AeroVironment to relies on growing military budgets of the U.S. and other foreign allied nations. Any slowdowns in military spending across its clients, will affect the backlog of AeroVironment. However, in my opinion, since AeroVironment largely deals with the supply of emerging defense technologies such as unmanned & robotic systems, I expect sovereign military forces across the world to broaden their ammunition restocking cycles and expand their military budgets to especially focus on emerging technologies such as robotics, AI, intelligence and unmanned systems. This will lead to an expansion of AeroVironment's customer base over the next few years.

Valuation Concerns

AeroVironment is trading 45 times non-GAAP forward earnings, which is 151% higher than the industry average and 144% higher than the forward earnings multiple investors pay to participate in the S&P 500 index. Part of this premium multiple is due to the optimism surrounding its incredible expansion in backlog, suggesting that AeroVironment will continue to see this momentum in subsequent quarters.

However, if the markets were to see a rerating, I would expect AeroVironment to be sold off simply due to its valuation and higher forward multiples. Its forward P/E is at 81.3, which is four times the forward P/E of the S&P500.

Closing Thoughts

As geopolitical tensions rise in different corners of the world, demand for unmanned vehicles and remotely controlled defense systems will increase. AeroVironment has already seen demand for its drone products surge amid the Russia-Ukraine war and the Israel-Gaza conflict. With the US Department of Defense 's military budgets expected to grow over the next decade, expect AeroVironment to continue to see momentum in its drones business. With a target of $165 for this stock per my analysis, there is still enough room for it run and hence it is a buy.

For further details see:

AeroVironment: Strong Order Backlog Is Boosting Growth Prospects In 2024