CA - Agnico Eagle: Another Solid Quarter Despite Detour Downtime

2023-10-26 09:00:42 ET

Summary

- Agnico Eagle Mines reported a solid Q3 with increased production and revenue, despite lower grades at its two highest grade assets and a temporary disruption at Detour Lake.

- Meanwhile, its all-in sustaining costs came in below the industry average, benefiting from higher gold prices and diesel hedges, and it reported 16% higher margins.

- In this update, we'll look at the Q3 results, if whether it can meet guidance at Detour, positive developments across the portfolio, and the stock's updated low-risk buy zone.

The Q3 Earnings Season for the Gold Miners Index (GDX) has finally begun and the first company out of the gate was Agnico Eagle Mines (AEM). Overall, the company had another solid quarter despite headwinds from declining grades at Fosterville and nearly a month of partial disruption to milling at Detour Lake, with output up over 6% year-over-year. Meanwhile, despite rising fuel prices (Agnico benefits from diesel hedges), all-in sustaining costs [AISC] came in well below the industry average, with a 16% increase in AISC margins year-over-year helped by the higher gold price. In this update we'll look at the recent quarter, the bigger picture cost and margin outlook, and recent developments across its assets.

Detour Lake Operations - Kirkland Lake Gold

{kind=link}

Q3 Production & Sales

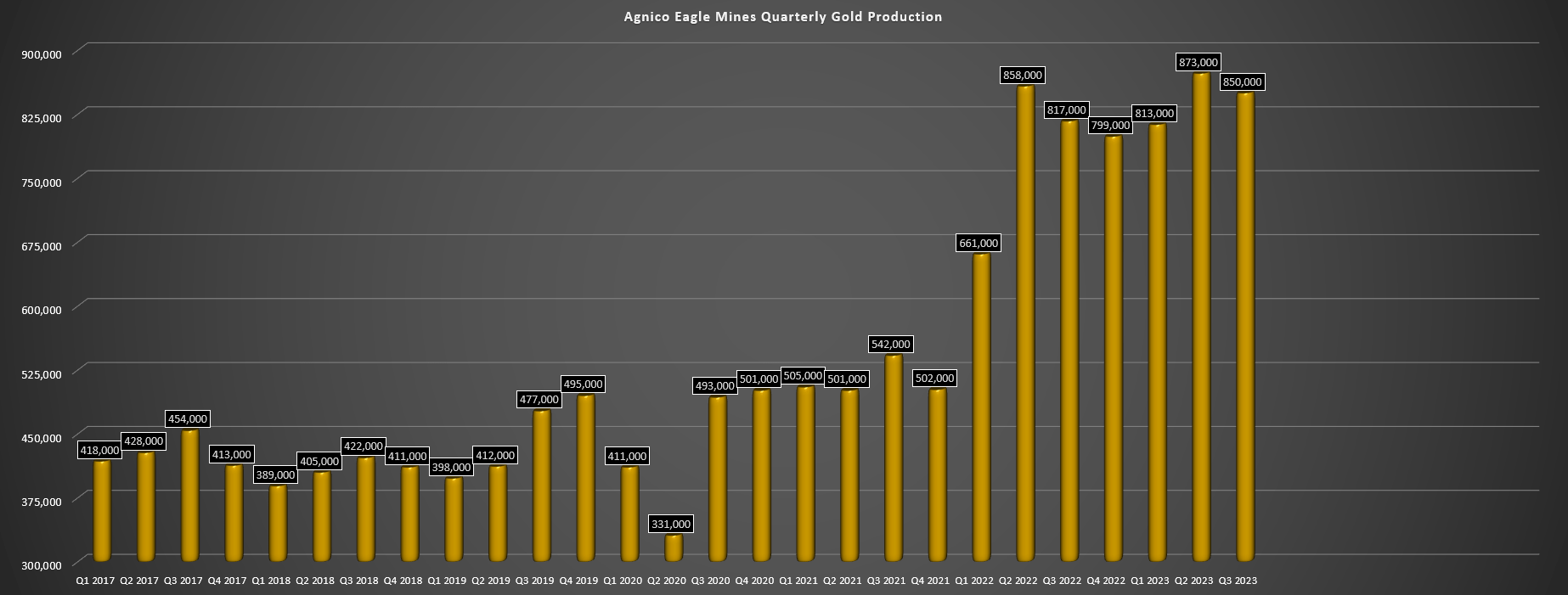

Agnico Eagle released its Q3 results this week, reporting output of ~850,200 ounces (sales of ~843,100 ounces and revenue of ~$1.62 billion), a 6% increase in production and over 13% increase in revenue from the year-ago period. The increased production was primarily related to acquiring the other 50% stake in Canadian Malartic and another huge quarter from Meadowbank, offset by much lower production from LaRonde, Macassa, Fosterville, and Detour Lake. However, it's worth noting that these declines in output were expected because of mill downtime and a planned change in the mining method at LaRonde (manage seismicity), a lower grade profile at Fosterville (honeymoon phase of 25+ gram per tonnes grades from the Swan Zone is over), lower grades related to mine sequencing at Macassa (up-tick in grades expected in Q4).

While Detour's production dip was unexpected (resulting from a transformer powering the SAG mill on one of two grinding circuits failing (since refurbished, with no impact to Q4 output), this is a one-time issue and resulted in ~14,000 fewer ounces assuming throughput was similar to Q3 2022 levels. Agnico noted that to prevent future extended downtime, it has ordered two additional new transformers and is working to improve monitoring of operating and spare transformers through the operation of an internal data acquisition system. The company shared that this will continuously monitor and record key system parameters including current, voltage, and frequency.

Agnico Eagle - Quarterly Gold Production - Company Filings, Author's Chart

{kind=link}

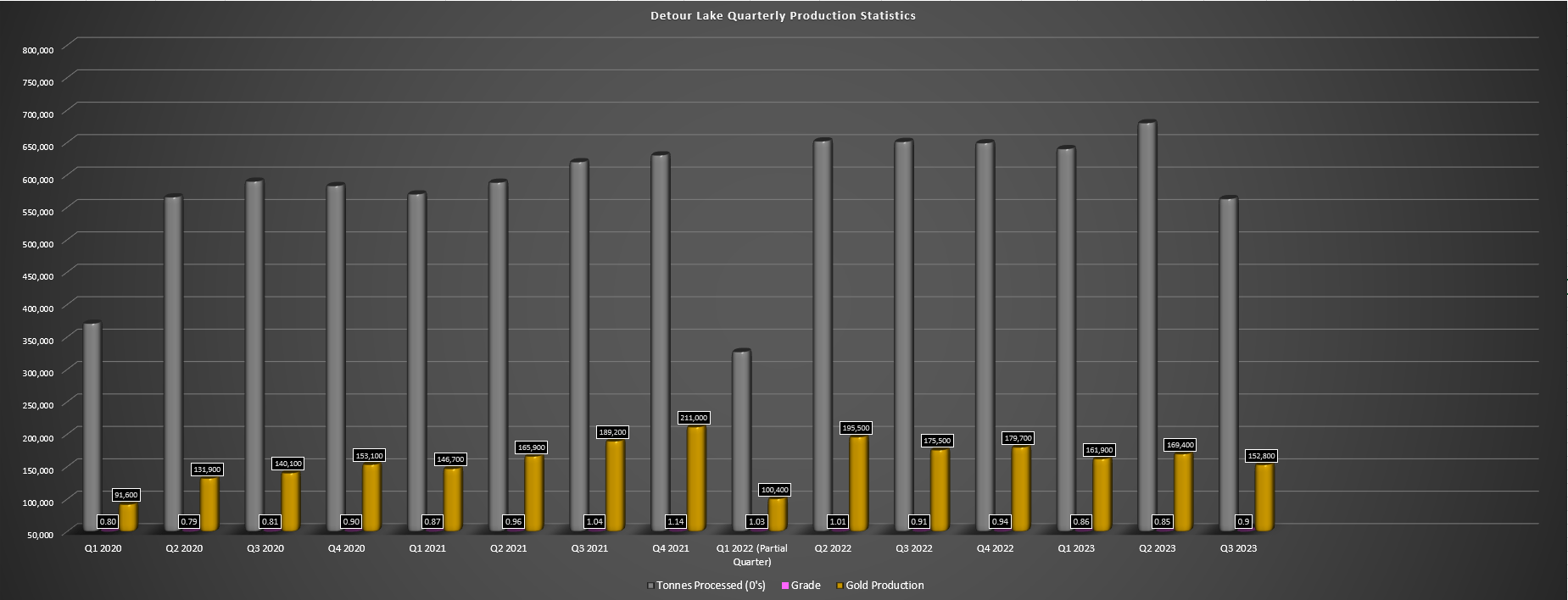

Digging into the results a little closer on a mine-by-mine basis and starting with Detour Lake, Q3 production came in at ~152,800 ounces of gold, impacted by lower throughput (~5.63 million tonnes processed) offset by slightly higher grades. This translated to a ~13% decline in production year-over-year, and has left the mine tracking towards the lower end of its FY2023 guidance of 685,000 to 715,000 ounces, with just ~484,000 ounces produced year-to-date. And while the mine will need a 191,000 ounce quarter to deliver near the low end of guidance, Detour will benefit from higher grades in Q4, with the mining of higher grades. So, assuming ~6.65 million tonnes processed at 0.99 grams per tonne of gold, and a 92.3% recovery rate, Detour could produce 195,000+ ounces and deliver just above the low end of guidance despite the disruption.

Detour Lake - Quarterly Production Statistics - Company Filings, Author's Chart

{kind=link}

Although this setback might be a little disappointing (the mill operated at ~70% of normal rates for 25 days which affected throughput), it's important to note that this is an asset that's expected to produce up to 750,000 ounces of gold in 2025 as throughput increases to the 28.0 million tonne per annum goal, but that will still leave ~4.8 million tonnes of excess capacity (32.8 million tonnes) per annum, providing the opportunity to top up the mill further and push production closer to ~1.0 million ounces per annum. So, while the quarterly miss may be disappointing, this is ultimately an asset that could produce closer to 1.0 million ounces by the end of the decade at sub $850/oz all-in sustaining costs, making it one of the best assets globally. Plus, despite the setback, Agnico still expects to deliver above the mid-point of its company-wide guidance range (3.35+ million ounces vs. 3.24 to 3.44 million ounce guidance).

Detour Drilling Highlights - Company Website

{kind=link}

Some impressive recent intercepts at depth and in the West Pit Extension released to date are shown below and include 2.5 meters at 17.3 grams per tonne of gold, 14.4 meters at 2.8 grams per tonne of gold, 5.4 meters at 7.1 grams per tonne of gold, 15.4 meters at 4.3 grams per tonne of gold, 2.5 meters at 81.4 grams per tonne of gold, and 22.8 meters at 3.7 grams per tonne of gold.

While it's early to speculate on potential mining rates with studies yet to be released, Detour Underground could add ~126,000 incremental ounces assuming 4,500 tonnes per day at Detour Lake Underground at ~2.5 grams per tonne of gold and ~96% recoveries, with the potential to actually come in marginally above 1.0 million tonnes per annum in peak years (higher open-pit grades in 2032 to 2034). That said, pushing the operation to marginally above 1.0 million ounces per annum in peak years would depend on whether the mill can be pushed to run at 31+ million tonnes per annum or if higher-grade feed from underground displaces some open-pit ore.

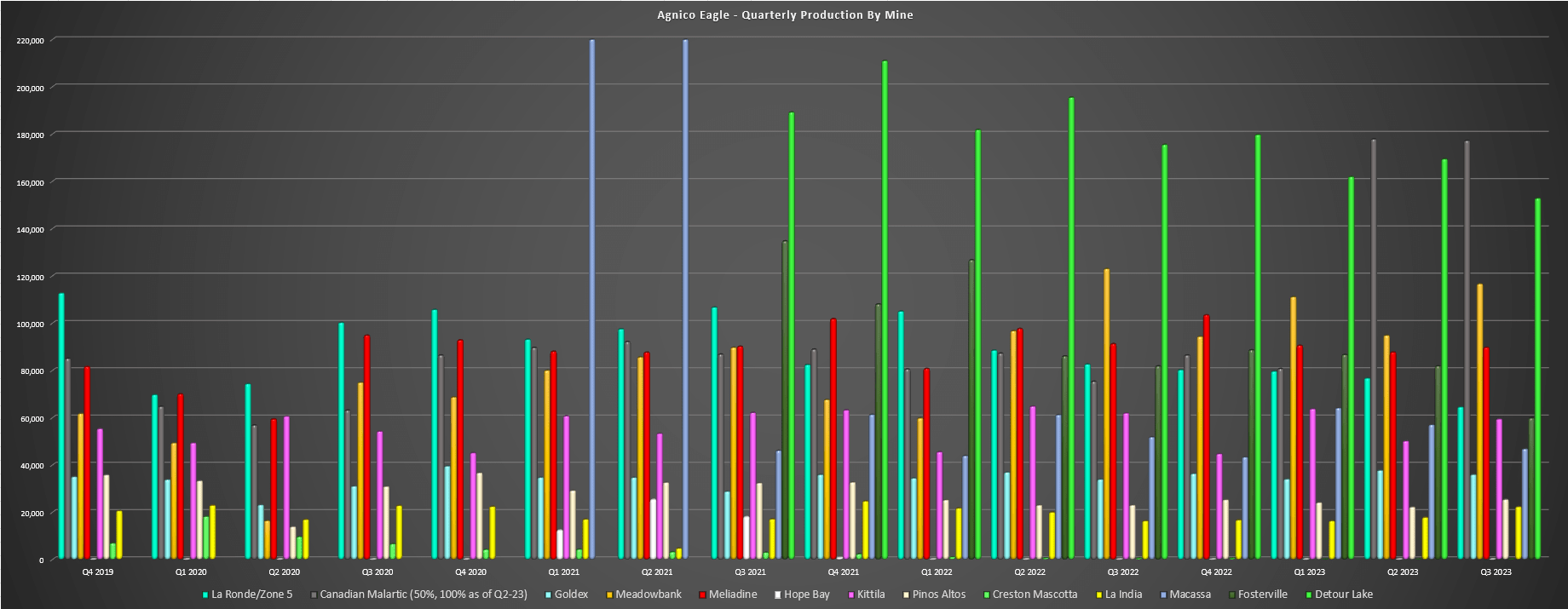

Moving over to Canadian Malartic, the mine produced ~177,200 ounces for Agnico with the benefit of full ownership, a 135% increase year-over-year with the benefit of higher grades. Agnico Eagle noted that throughput levels benefited from softer ore at Barnat and positive grade reconciliation, while costs at Detour Lake and Canadian Malartic benefited from a weaker Canadian Dollar. Given this FX benefit, cash costs at both mines came in at $755/oz and $805/oz, respectively, with Malartic's costs actually lower year-over-year despite the impact of sticky inflationary pressures. This is certainly encouraging given that these are the company's two largest mines and the two largest mines in Canada, and there's certainly room to improve costs at both mines long-term by leveraging existing mill capacity, and with Agnico looking at implementing advanced process control utilizing AI and potential ore sorting at Detour. In fact, once optimized at the end of this decade, Agnico could have nearly 2.0 million ounces combined coming from these two assets alone.

Fosterville Quarterly Production - Company Filings, Author's Chart

{kind=link}

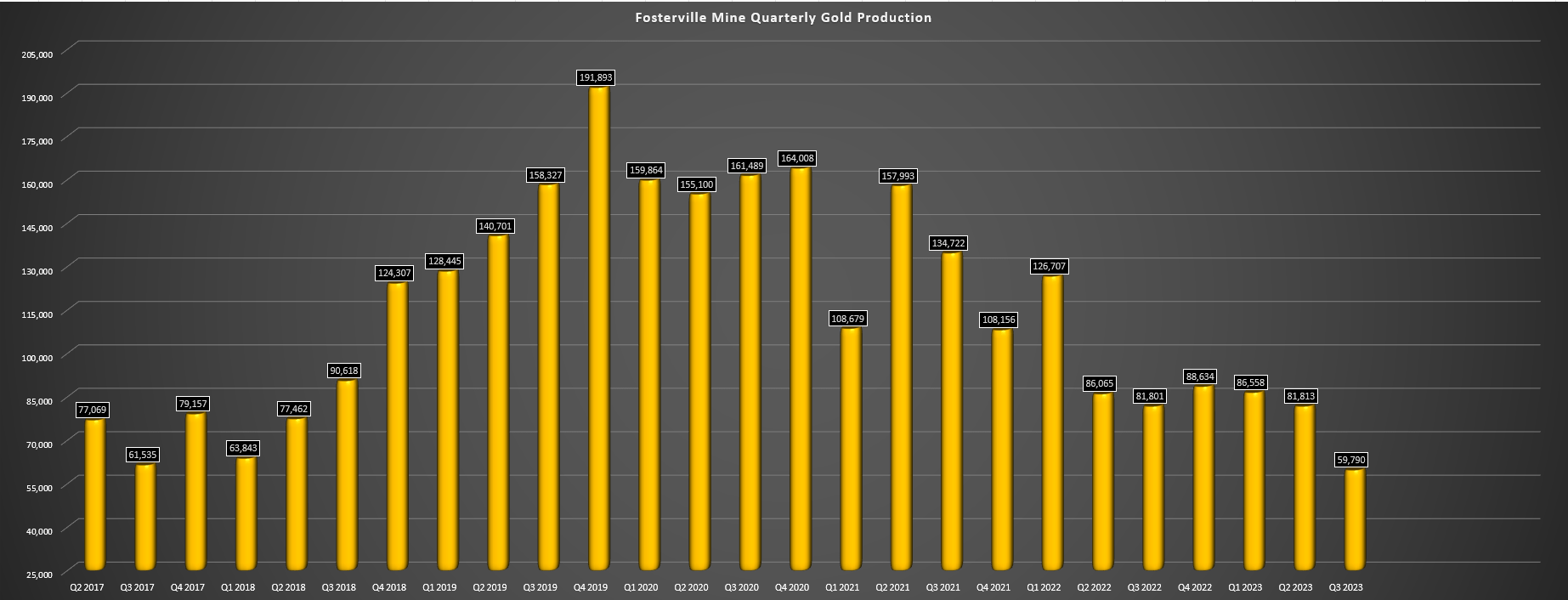

As for the company's smaller operations, Fosterville had a softer quarter which was to be expected given the lower grade profile (13.2 grams per tonne of gold) and lower throughput. However, the ~60,000 ounces of gold produced still came in at industry-leading cash costs of $495/oz and mine-site costs of ~$200/tonne. However, the positive news was that the restrictions related to low-frequency noise that impacted the operation of surface primary fans were finally lifted after 18+ months, allowing the mine to catch up on development and support higher mining rates going forward. Meanwhile, at LaRonde, downtime significantly impacted production which came in at ~64,500 ounces (Q2 2022: ~82,600 ounces), with lower throughput of ~627,000 tonnes at lower grades (3.43 grams per tonne of gold). Still, despite the lower production, cash costs still came in at reasonable levels at $972/oz.

Moving to its Nunavut operations at Meadowbank and Meliadine, combined production for these two assets was ~206,300 ounces (Q2 2022: ~214,200 ounces) despite being up against tough comps with a monster quarter at Meadowbank in Q3 2022 with the asset pushing out ~123,000 ounces. At Meliadine, production was down slightly due to lower grades offset by higher throughput, with work continuing to increase mill throughput to 6,000 tonnes per day by yea-rend 2024. At Meadowbank, production was also impacted by lower grades, but it was still an exceptional quarter given the difficult weather conditions, and annual production will increase materially in 2024 and 2025 to just shy of 500,000 ounces.

Agnico Eagle Mines - Quarterly Production by Mine - Company Filings, Author's Chart

{kind=link}

Finally, as for Kittila, Goldex, Macassa, and its Mexican operations, production was down at Macassa and Kittila year-over-year, partially offset by higher output at its Mexican operations and Goldex which were up against easier comparisons. At Kittila, the asset reported a record monthly throughput of ~195,000 tonnes in July, but production was down due to lower grades. At Goldex, grade and throughput were up year-over-year contributing to the production of ~35,900 ounces of gold at very respectable cash costs ($822/oz). At Macassa production was down to ~46,800 ounces on lower grades, with the asset up against tough comparisons (~22.0 gram per tonne quarter which is above reserve grades in Q3 2022), offset by higher throughput with Agnico reporting productivity gains and improved equipment availability. And in Mexico, Pinos Altos benefited from higher throughput while La India benefited from much higher grades, with both assets combining for ~47,700 ounces in Q3, up 21% year-over-year.

Costs & Margins

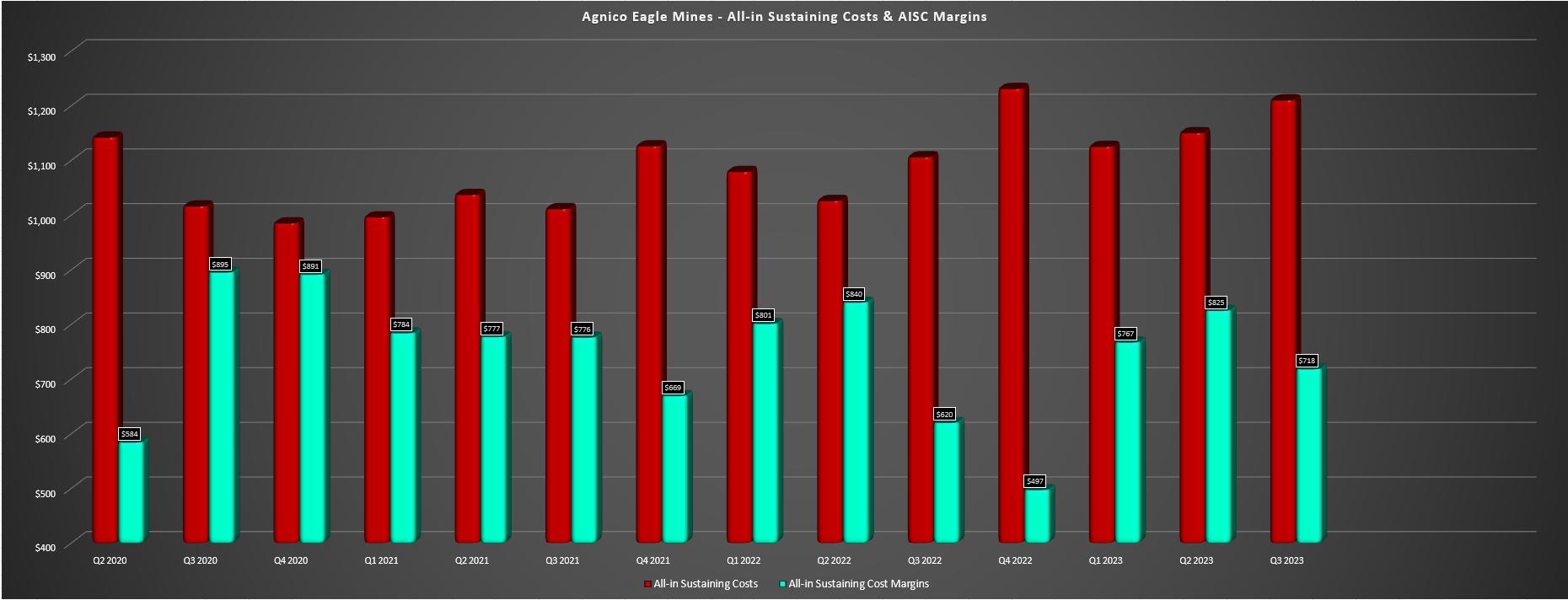

Moving over to costs, Agnico Eagle's cash costs and AISC may have been up year-over-year to $898/oz and $1,210/oz, respectively, but these figures were well below the industry average, with industry-wide AISC likely to come in above $1,360/oz. Besides, while costs were up, Agnico's cost control year-to-date has been solid especially given the lower contribution from two of its highest-margin assets (Detour Lake, Fosterville), with year-to-date AISC coming in at $1,162/oz on ~2.54 million ounces, setting the company up to deliver near its guidance mid-point of ~3.44 million ounces at $1,165/oz. Plus, it's also worth noting that while some producers may see an impact from upside volatility in oil prices in Q4, 72% of Agnico's remaining 2023 diesel is hedged at $0.70/liter vs. a 2023 cost assumption of $0.93/liter, insulating it from any further upside in oil prices if geopolitical tensions escalate.

Agnico Eagle - AISC Margins - Quarterly Filings, Author's Chart

{kind=link}

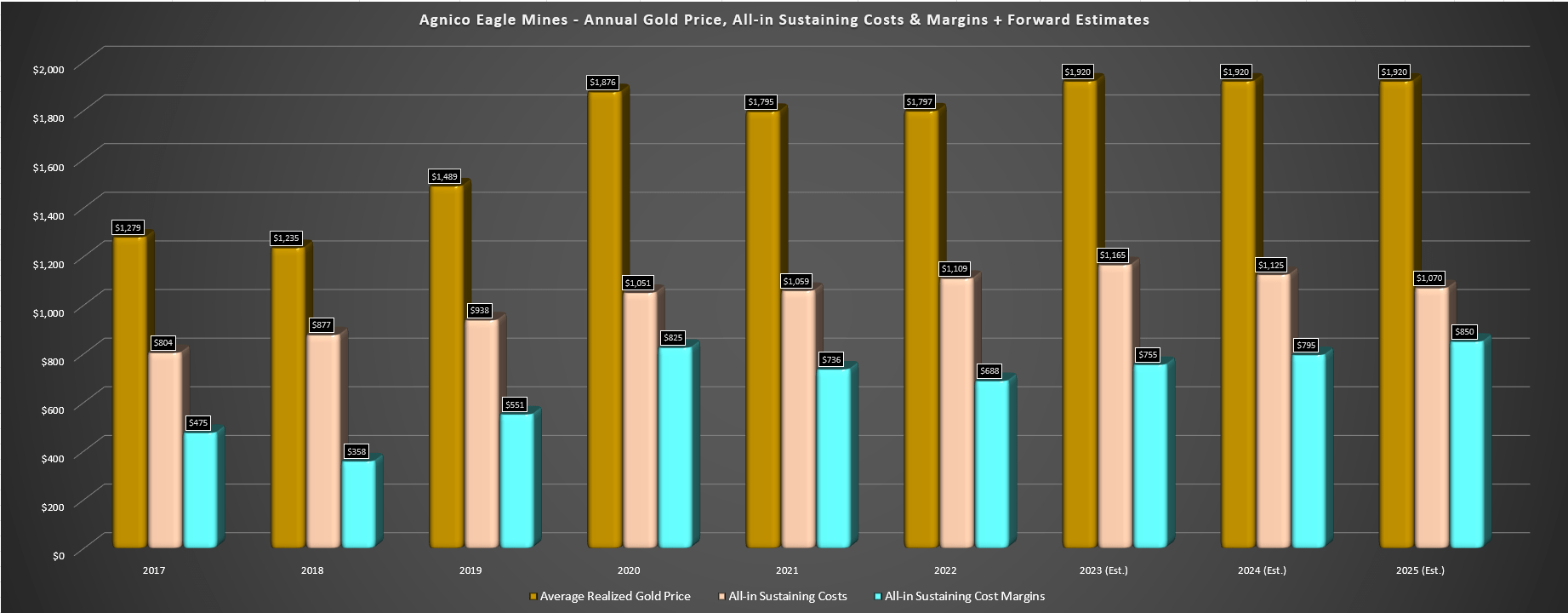

As for the company's margins, even though costs were up year-over-year, AISC margins actually increased to $718/oz (Q3 2022: $620/oz) despite a softer quarter than hoped due to the transformer failure at Detour Lake in August. And even if costs were up, the bigger picture for margins remains quite bullish for Agnico even if one assumes no further upside in gold prices between now and 2025. In fact, as the chart below shows, Agnico should see AISC margins improved 10% year-over-year to $755/oz (assuming $1,920/oz average realized gold price and $1,165/oz AISC), and improve further to $850/oz+ in FY2025. The improvement will be driven by higher production from its lower-cost assets (Detour Lake, Macassa, Kittila, assuming positive SAC decision on operating permit), higher production at Meadowbank which should result in lower costs, and what should be more normalized sustaining capital levels with 2023 sustaining capital being elevated at ~$800 million (FY2022: ~$719 million).

Agnico Eagle - Annual Gold Price, All-in Sustaining Costs & Margins + Forward Estimates ($1,920/oz Constant Gold Price Used in 2023-2025) - Company Filings, Author's Chart & Estimates

{kind=link}

Plus, if one chooses to be more bullish on the gold price and assumes we don't see a constant $1,920/oz gold price out to 2025 to be conservative, Agnico's AISC margins could improve from ~44% ($850/oz) to ~48% ($980/oz) at a $2,050/oz gold price, and I don't think this all that far fetched given that the metal continues to make higher lows on its long-term chart. So, there is certainly an upside to this expected margin profile and I would expect the trend of higher margins (2023 ---> 2025) among the three major producers to help improve sentiment for producers sector-wide which remains in the gutter. Finally, as for Agnico's financial results, the company reported operating cash flow before working capital changes of ~$669 million, free cash flow (defined as cash flow [-] additions to property, plant & equipment) of ~$249 million, and ended the quarter with ~$356 million in cash and just ~$1.59 billion in net debt despite coming off a mid-sized acquisition, giving it a strong balance sheet to support its future growth.

Recent Developments

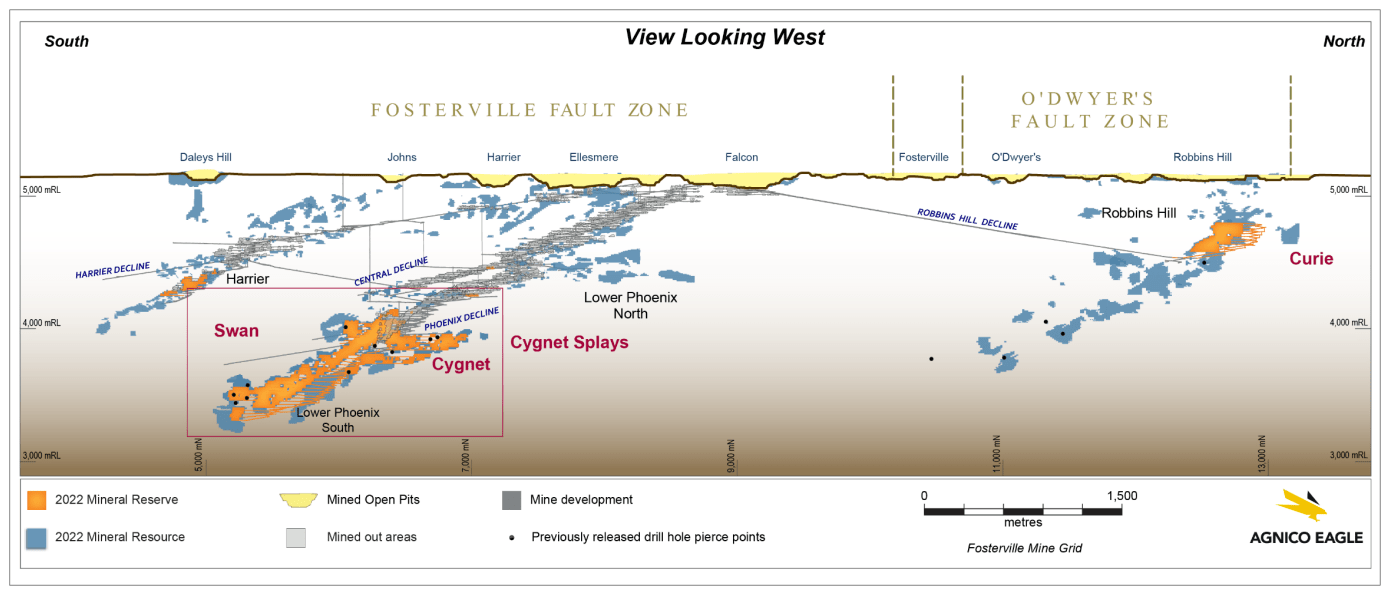

Looking at recent developments, there were several positive ones across the portfolio. For starters, Agnico noted that it is looking at a pilot project for ore-sorting to process 1.5 million tonnes of low-grade material at Detour which will inform the potential design of a full-sized plant to look at a larger ore-sorting operation. Second, the company continues to see exploration success at depth at Lower Phoenix, noting that it hit 10.8 grams per tonne of gold over 10.0 meters in the Cardinal splay at ~1,830 meters depth, 190 meters down-plunge of its current mineral reserve base. For those unfamiliar, the Cardinal Zone was first identified in 2022 by Agnico Eagle in the hangingwall of Lower Phoenix with intercepts of 1.1 meter at 365.5 grams per tonne of gold (1,680 meters depth), 1.4 meters at 226.2 grams per tonne of gold (1,715 meters depth), and 2.9 meters at 168.6 grams per tonne of gold (1,680 meters depth), so this new visible gold intercept is the deepest at Cardinal to date.

Fosterville - Targeting Cardinal Structure - Company Website

{kind=link}

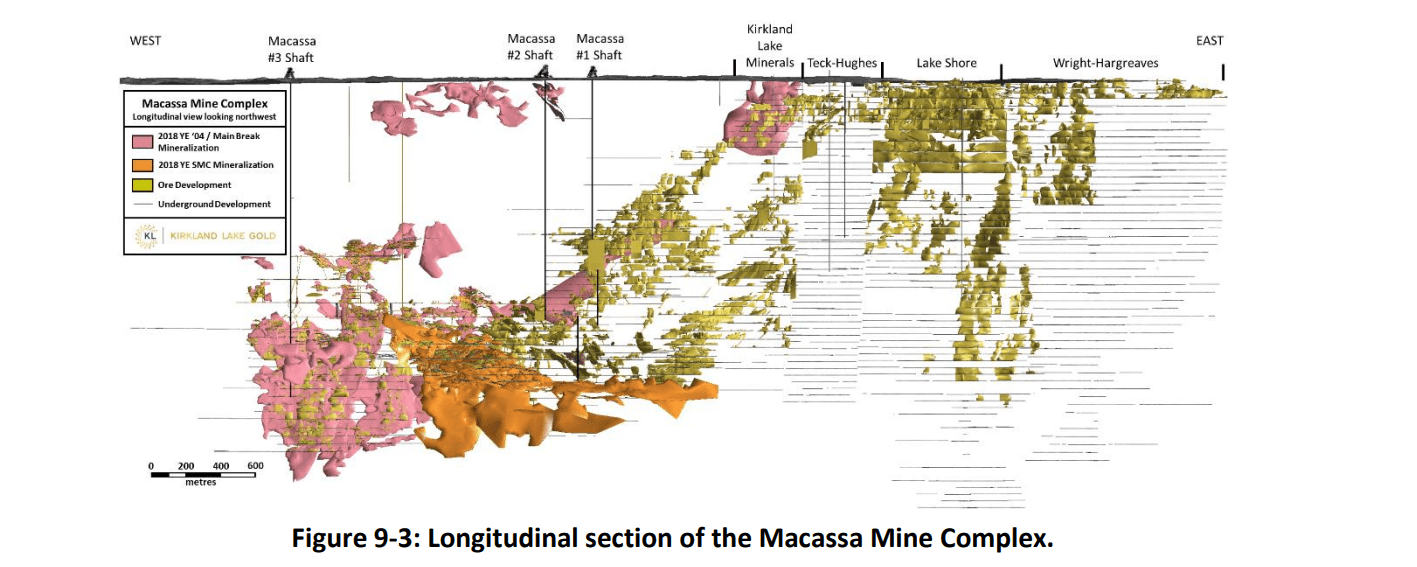

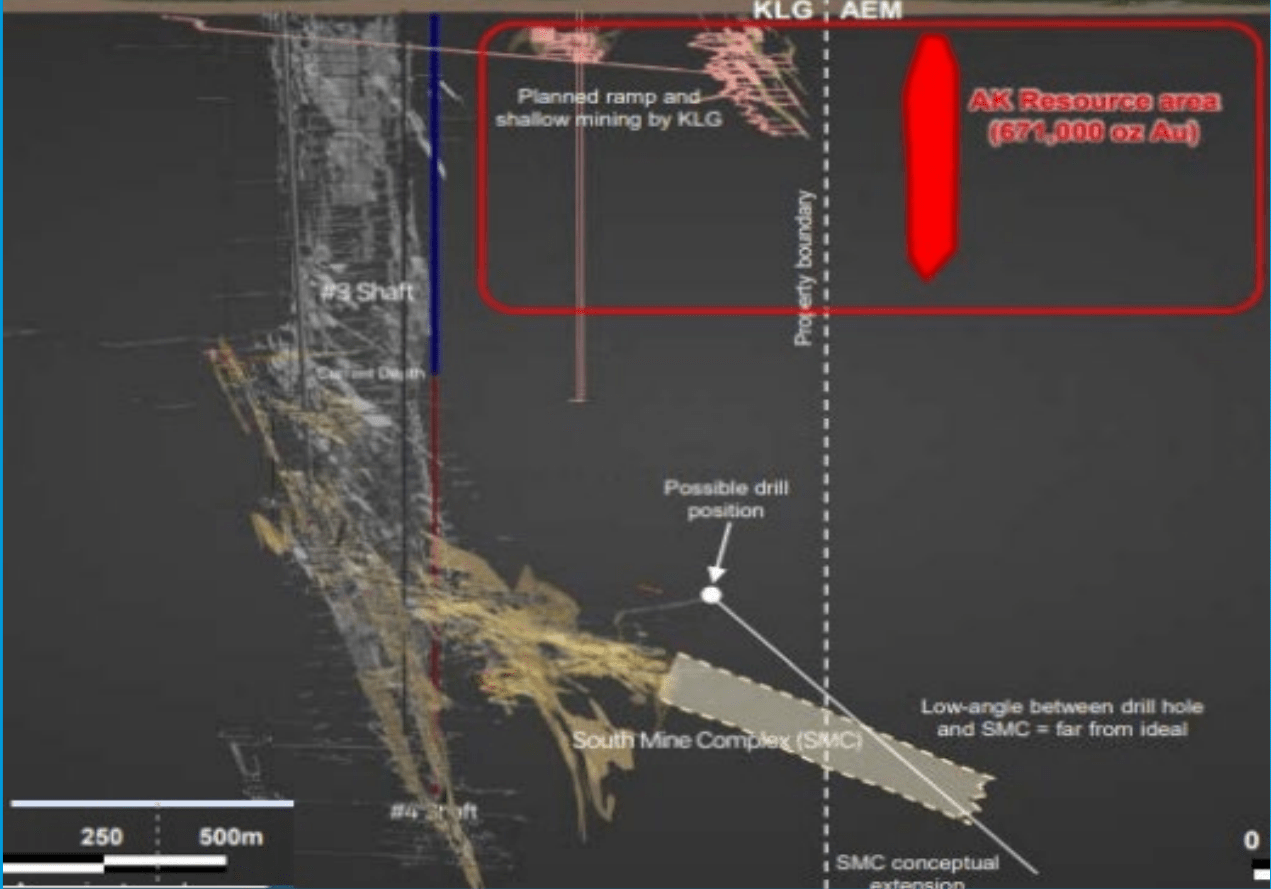

Moving back to Canada, Agnico continues to make progress at Macassa, with higher throughput in Q3 (1,217 tonnes per day), and work is ongoing to increase throughput to 1,650 tonnes per day by mid-2024, with mining rates supported by the commissioning of Shaft #4 and better productivity from Macassa Deep. Notably, development is ahead of schedule at the near surface and Amalgamated Kirkland deposits (being accessed from the surface ramp at Macassa), with ~2,800 ounces produced in Q3, with the potential for these deposits to contribute up to 40,000 ounces in 2024 by trucking ore to the LZ5 plant that is in care & maintenance. Finally, Agnico teased that exploration results to date "confirm gold mineralization east of Macassa, below the past-producing Kirkland Mineral Mine, opening the potential for the discovery of mineralization under five more historical mines of the Main Break further east."

Macassa Mine Complex & Historic Mines To East - 2019 TR Previous Kirkland Lake/Agnico Property Border at Macassa - Company Presentation

{kind=link}

{kind=link}

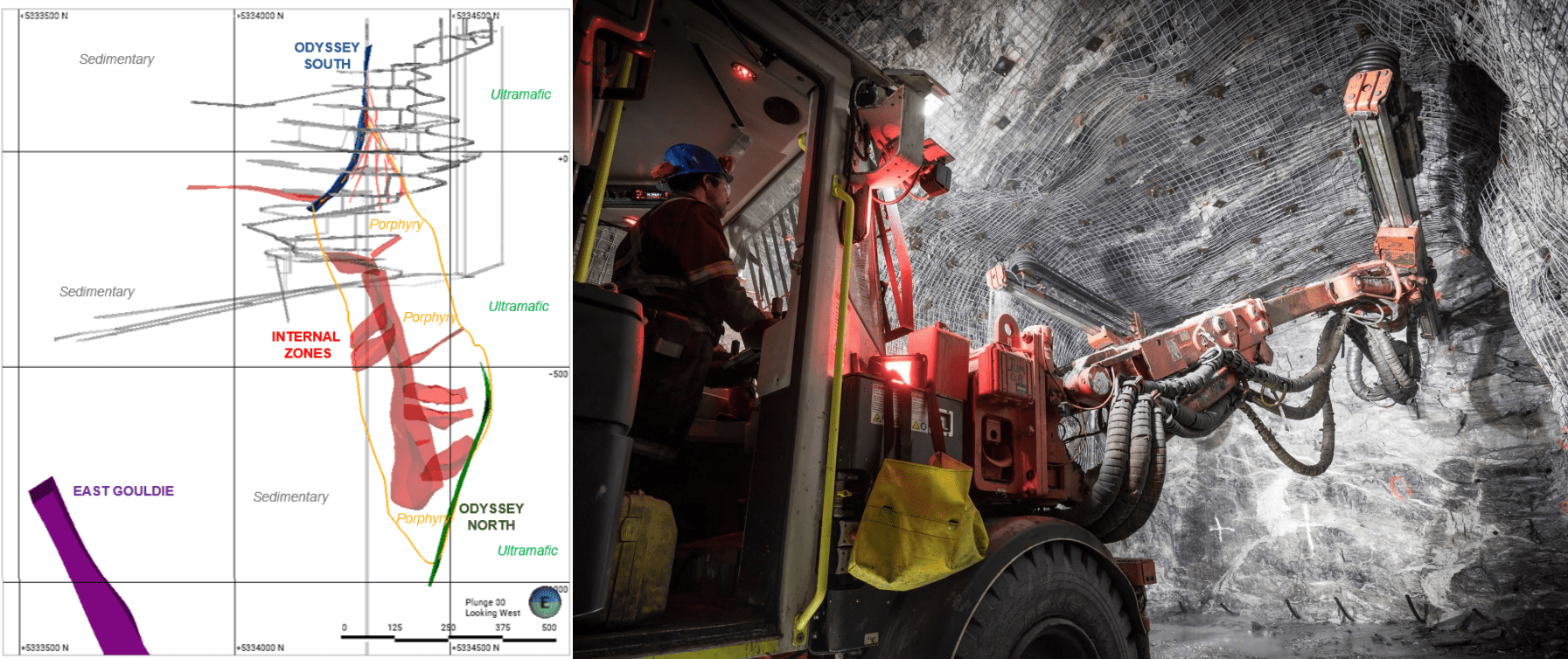

The last positive development worth discussing comes from Odyssey, where production rates improved to 3,300 tonnes per day in September with the commissioning of the paste fill plant, tracking well against planned mining rates of 3,500 tonnes per day next year. In addition, Agnico noted it saw record developer meters of 1,030 in September, and should reach its 1,200 meter per month target in 2024. And in the case of lateral development, rates are also tracking above target, with the company on track to reach the first level at the top of the higher-grade East Gouldie deposit (largest and highest-grade deposit at Malartic Underground or Odyssey) in H1 2024. Finally, the company continues to see positive grade reconciliation like it saw in stope #1 (~44,900 tonnes at 2.95 grams per tonne of gold vs. planned ~29,500 tonnes at 2.65 grams per tonne of gold), with 18% positive reconciliation for ounces to date in its first four stopes, making Agnico quite optimistic about bonus ounces from Odyssey internal zones.

Odyssey Internal Zones & Underground Mining - Company Presentation

{kind=link}

So, were there any negatives?

One minor negative to report was that we still don't have a resolution at Kittila on the operating permit that is pending with the Supreme Administrative Court of Finland [SAC]. And while the SAC has noted that it will issue its decision this month, a negative decision or delayed announcement would mean that Agnico will have to partially suspend activities to stay at the permitted rate of 1.6 million tonnes per annum. However, if the decision is positive, Kittila could produce an additional 30,000 ounces in Q4 2023 vs. the more conservative guidance provided to adjust for the company waiting for this permit. Overall, this is not really a negative, but I was hoping to see a resolution by now on the decision to reinstate the 2.0 million tonnes per annum permit.

Summary

Agnico Eagle had another solid quarter in Q3 and was free cash flow positive despite sticky inflationary pressures, a hiccup at Detour Lake, and a much lower contribution from its lowest-cost Fosterville Mine. Meanwhile, it continues to trade at a massive discount to historical multiples at barely 1.0x P/NAV and ~8.7x FY2024 cash flow per share estimates vs. a 10-year average multiple of ~13.0x cash flow and over 1.40x P/NAV. And given that Agnico has a more diversified portfolio, the best pipeline it's ever had (San Nicolas JV, Detour/Malartic excess capacity with potential for Upper Beaver + Wasamac feed, Hope Bay), and ~95% of production from Tier-1 jurisdictions, I would argue that the stock should trade at the high end of its previous range for multiples given that jurisdiction has never been more important. Hence, I continue to see AEM as one of the top ways to get gold exposure, and I would view any pullbacks below $45.50 as buying opportunities.

For further details see:

Agnico Eagle: Another Solid Quarter Despite Detour Downtime