CA - Agnico Eagle: Why This Gold Miner Is A Top Pick

Summary

- AEM is as inexpensive as it's been on a P/S and P/CF basis since the bear market of the early 2010s.

- What makes AEM so special.

- Detour Lake could be producing 1 million ounces of gold.

- Fosterville: The X-Factor.

- A few key technical events are happening at the moment, as the stock is: 1) breaking above overhead resistance at the 200-week, and 2) close to breaking out above the top of the multi-year downtrend channel.

As the rebound in gold and the miners gains steam, I'm seeing more pro-gold articles across various financial websites that are recommending investors buy Newmont ( NEM ) and Barrick Gold ( GOLD ). These are the two largest gold producers in the world—both in terms of output and market cap—and they are the go-to names for most investors because of their familiarity and size. Rarely in these articles is there in-depth, compelling analysis of these companies that explains why NEM and GOLD should be purchased, both in general terms and over every other gold miner.

I don't want to call it lazy analysis; I'm quite bullish on Barrick, and Newmont's relative value is now lower after its waterfall decline since last spring. But gaining exposure to rising gold prices isn't about buying the two largest gold mining companies in the world and calling it a day, as that's a plain vanilla strategy and overlooks critical elements that might act as bearish catalysts, leading to underperformance.

I will just say this, any top 2-3 list of large-cap gold miners that doesn't include Agnico Eagle ( AEM ) is suspect. AEM is one of my top picks.

I discussed AEM in great detail just over a year ago ( Agnico Eagle Is A Must-Buy Gold Stock ) and I explained why its underperformance over the prior few years would not last, as with "this team and these assets, I'm confident that outperformance will return."

AEM is up 16% since then, while the HUI (an index of gold miners) is higher by 3%. The S&P and Nasdaq are down 19% and 34%, respectively, during that time, as the gold miners have notably outperformed the stock market. I expect that trend to continue for several more years, and AEM is just as compelling today, especially given the bullish news over the last several quarters. Let's review in greater detail.

In A Gold Bull Market, But Has A Bear Market Valuation

For the last decade, AEM has been one of those stocks where the fundamentals remained exceptionally bullish, but the valuation was hard to justify. I've been a fan of management and the company for a long time, but the stock was always too expensive and the risk/reward was unfavorable.

However, over the last few years, it was the combination of valuation, a few minor operational challenges at some assets, and the Kirkland Lake Gold merger that led to AEM lagging well behind the group. It's been one of the worst-performing seniors in the sector and was back to mid-2019 levels.

Yet all the while, AEM was becoming a bigger and more diversified Au producer. It's now the best-positioned gold miner on the planet, and unlike NEM and GOLD, AEM keeps growing, as apparent by the trend in cash flow over the last few years (which is trending up for AEM and down for GOLD and NEM). Both NEM and GOLD generate more cash flow, and last quarter was an anomaly for NEM as it had a sizable negative working capital adjustment, but AEM is quickly closing the cap. With a $25 billion market cap, on a P/CF basis, AEM is a much better value compared to NEM.

This has created an opportunity to buy the premier gold miner in the sector at the cheapest relative valuation I've seen in many years, and it's why I've been so bullish on the stock lately.

While Agnico's valuation isn't dirt cheap, it's as inexpensive as it's been on a P/S and P/CF basis since the bear market of the early 2010s. You pay a premium for quality, and as long as the company continues to deliver, one can never expect AEM to trade at the same discount to fair value as lower-quality producers. That will never happen; smart money won't allow it.

What Makes AEM So Special

To become the best of the best in this sector, it's a simple equation:

Low-risk jurisdictions

+

Low-cost mines

+

Top-shelf management team and board

+

Diversified portfolio of producing assets

+

Solid balance sheet

+

Strong growth pipeline

=

Best Of The Best

But it's a complex process to reach that upper echelon.

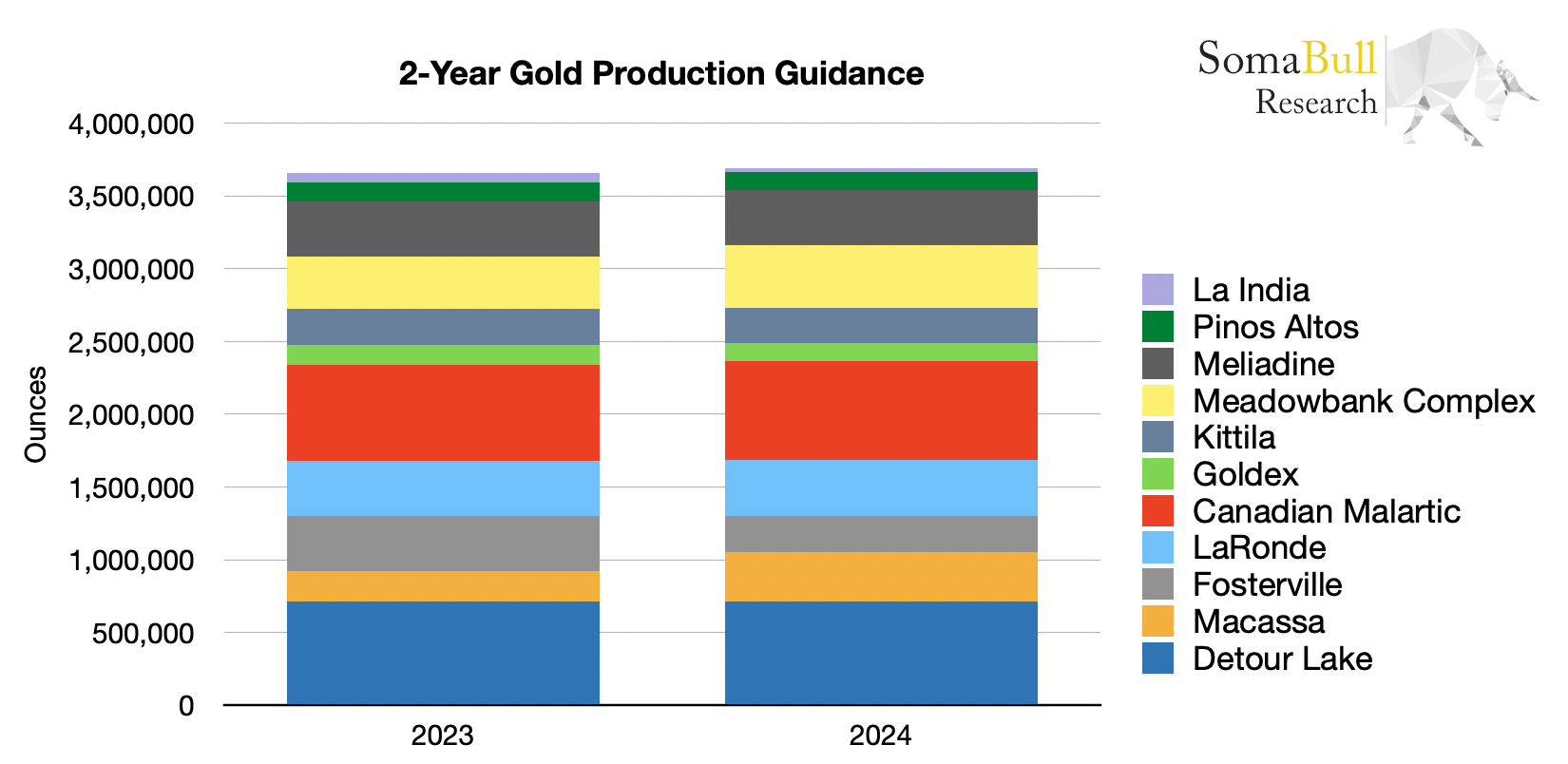

AEM has all parts of the above equation, and it's been methodical in getting to this point, at least until it stepped on the accelerator in the last year as the acquisition of Kirkland Lake Gold, and now Yamana Gold's ( AUY ) Canadian assets, have resulted in gold production more than doubling since 2019 (from just under 1.8 million ounces, to almost 3.7 million ounces going forward). That includes the other 50% of the Canadian Malartic mine, which I've shown in the 2-year production guidance below (based on estimates from earlier in 2022). While Barrick and Newmont still have the higher-quality assets overall, many of Agnico's mines are exceptional. Detour Lake and Malartic would count as Tier 1 mines in the eyes of Barrick, and if the latest study on Detour Lake is close to accurate, it's truly a world-class mine. Macassa, LaRonde, the Meadowbank Complex, and Meliadine are solid Tier 2 operations. Fosterville is a wildcard as it had the potential to be a Tier 1 asset if there were more ultra-high-grade reserves (more on this in a bit). Rounding out the portfolio are dependable mines such as Kittila (which could become a Tier 2 operation), Goldex, and Pinos Altos. When judging the entire portfolio, what sets Agnico apart from NEM and GOLD is the lower jurisdictional risk and higher margin mines. Barrick and Newmont have many key operations in Tier 1 regions, but they don't account for 93% of their portfolio as they do for AEM. AEM is also still producing gold at an average AISC of $1,000-$1,100, while its two larger peers' AISC is in the $1,150-$1,200 per ounce range.

{kind=link}

SomaBull

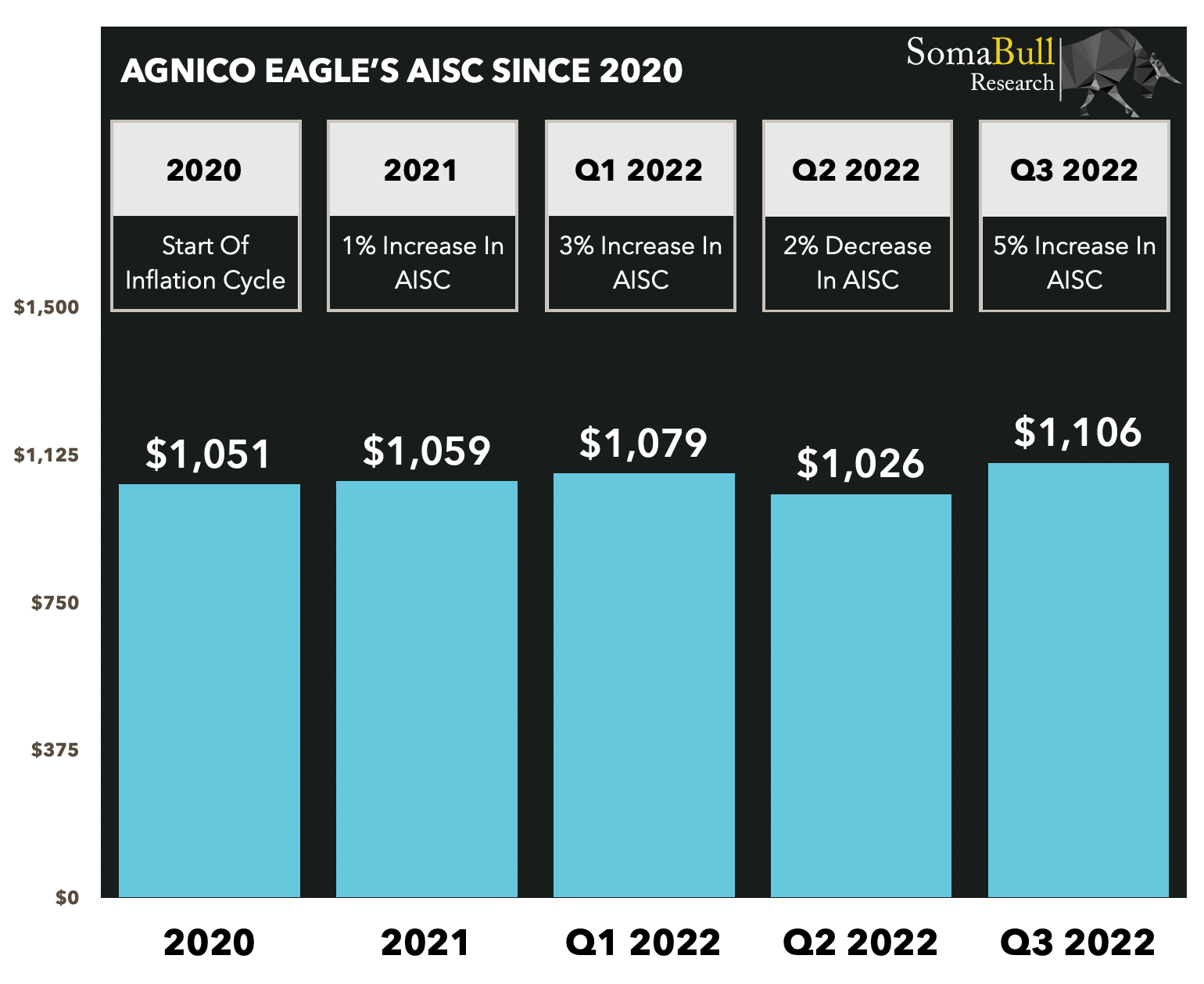

The fear in the sector is the impact that inflationary pressures will have on costs, but Agnico Eagle is doing an amazing job managing the situation.

The company reported AISC of just $1,026 per ounce in Q2 2022, a 2% decrease compared to 2020 AISC, which was the start of the current inflationary cycle. The company has been able to largely offset cost pressures via better operational performance, cost savings initiatives from the Kirkland Lake merger, the weaker Canadian dollar, and currency and fuel hedges. AISC increased to just above $1,100 per ounce in Q3 2022, but that's only a 5% increase compared to 2020, and AEM reiterated the $1,000 – $1,050 per ounce AISC guidance for the year. Although they expect to come in at the higher end of the range due to the still challenging inflationary environment. That implies AISC below $1,100 last quarter (Q4 2022). At $1,800 gold, margins are phenomenal, even if there are increasing cost pressures in 2023. Few companies in this sector have been able to keep costs flat since 2020, and no senior producer other than AEM has either.

{kind=link}

What's even more appealing about AEM are the sizable growth opportunities in its portfolio. The production estimates above don't include the Hope Bay project (also in Canada), which I'm quite intrigued with, or smaller projects like the Amalgamated Kirkland deposit at Macassa.

The mega potential is at Detour Lake, as AEM is analyzing whether to take the mine to 1 million ounces per annum.

Detour Lake Is Turning Into A Monster Deposit

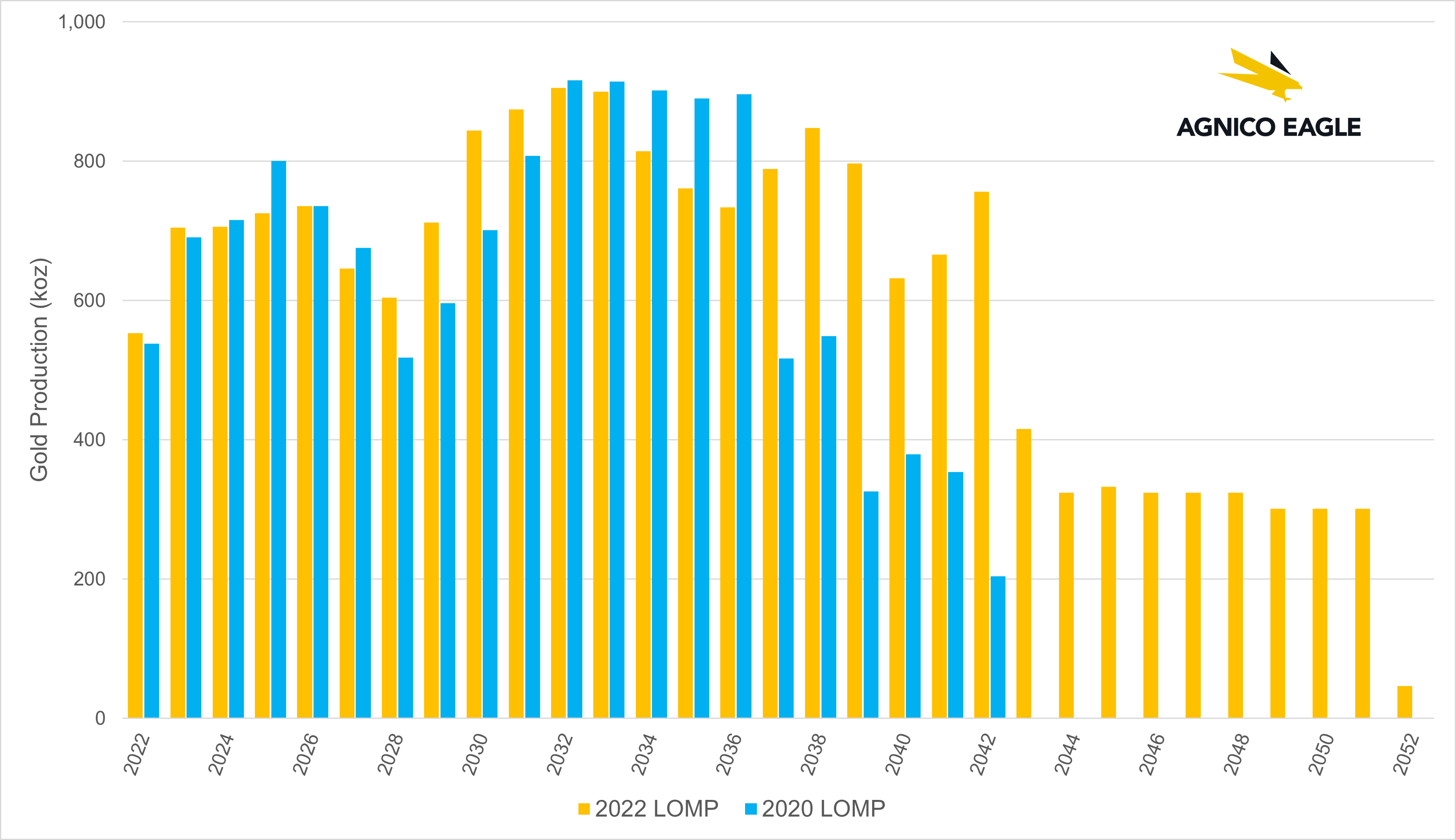

AEM gave shareholders a bonus last summer as they announced a 38% increase in reserves at Detour Lake and extended the mine life by 10 years to 2052.

Detour Lake now contains 20.4 million ounces of gold compared to 15.0 million ounces at the end of 2021. Grade dropped to 0.76 g/t in the latest resource update but it doesn't negatively impact the outlook as the mine plan has higher average grades and lower average costs from 2022 through 2042, and then lower grade ounces at the backend of the mine plan.

{kind=link}

Agnico Eagle

You can see this in the next slide, as there isn't too much difference over the next 5 years compared to the 2020 life of mine. However, there is a much more noticeable jump in production later this decade as the company reduced the dip in output that was previously expected, and then post-2036, they added a significant amount of production. The last ten years are mostly mining/processing lower grade stockpiled ore, but that still amounts to over 3 million ounces of gold production. That shows you how good Detour Lake is—when the "worst" material is still 20 years out, and there are 3 million ounces of it.

{kind=link}

Agnico Eagle

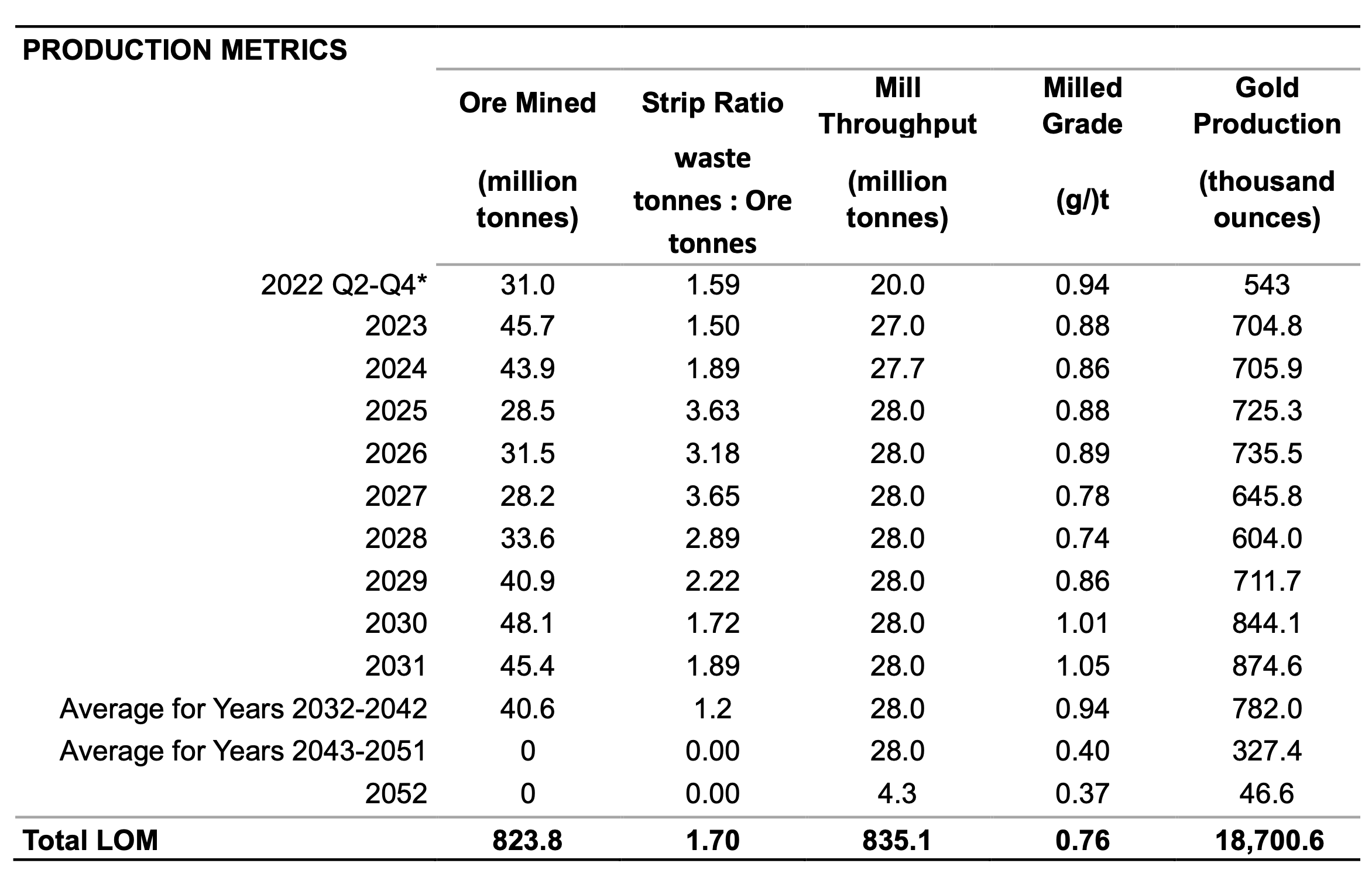

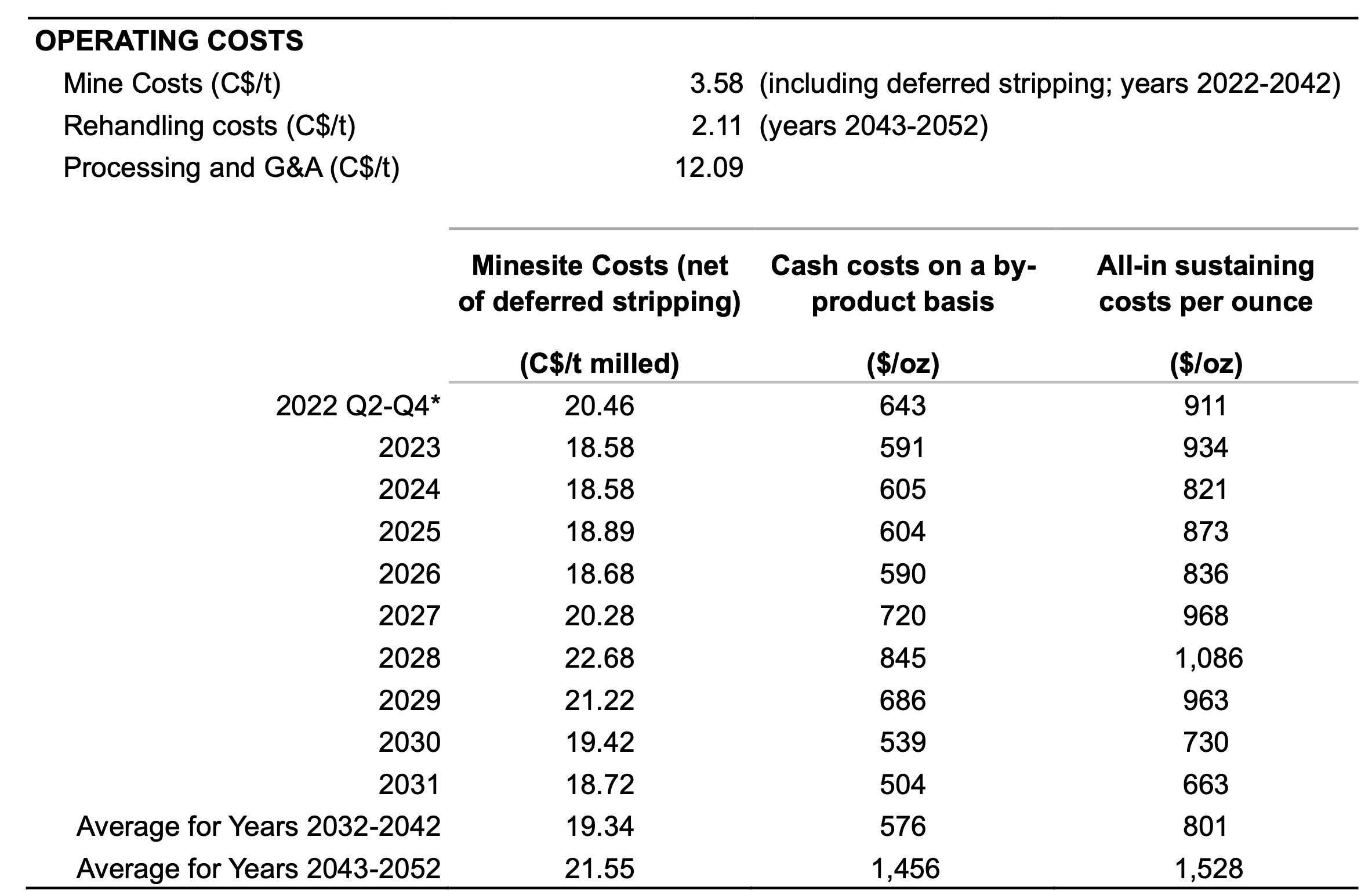

A more complete breakdown of production and other operational metrics such as strip ratio and grade are contained below, with production by year in the far right column. For the next 20 years, Detour Lake will be a 700,000 to 800,000-ounce per year gold mine, which would be one of the top 10 largest gold mines in the world based on 2021 rankings. Two things I want to point out are, 1) the strip ratio increases dramatically from 2025 to 2029, and 2) the grade declines during those years, both of which will increase cost temporarily. However, once Agnico is through the waste stripping, then they get down to the higher grade portions of the deposit, which is when production rises above 800,000 ounces.

{kind=link}

Agnico Eagle

The average cash cost per ounce for the life-of-mine is now US$730, only a $60 per ounce increase over the 2020 mine plan estimate. While the average AISC is now estimated at $920 per ounce, which is an increase of ~$85 per ounce vs. 2020. It's the last decade of the mine life that is raising the overall AISC, as from 2022-2042, AISC will average under $850 per ounce. You can also see the impact of the higher strip ratio and lower grade on the cost side during years 2027-2029.

{kind=link}

Agnico Eagle

Agnico is assessing the potential to increase production at Detour Lake to 1 million ounces or more per year and expects to have this analysis complete by late 2023.

It's not just the increased reserves that support higher throughput at the mine, as the company also announced some exceptional exploration results 2km to the west of the pit, which potentially supports an underground operation later in the mine life.

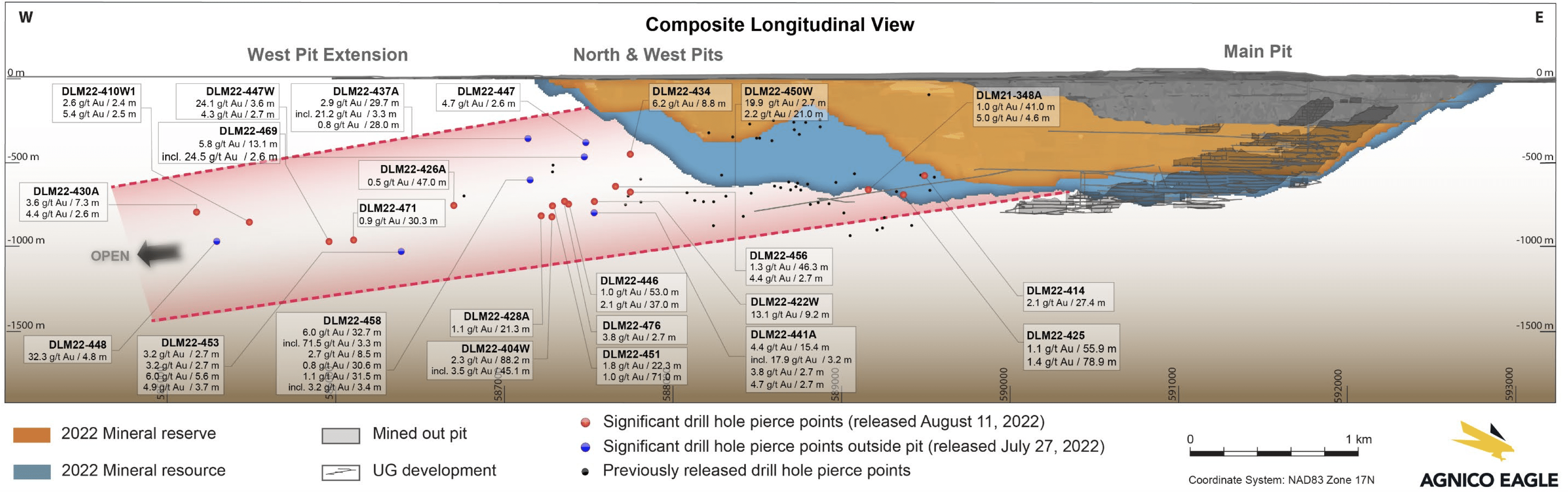

Below is a composite longitudinal view of Detour Lake. I want to focus on three aspects: 1) The mined-out pit (shaded in grey) is small in relation to the overall size of the orebody, which is a good visualization of the remaining mine life. 2) The heart of the main pit (i.e., where the higher grade mineralization resides, but not reflected in the diagram) is still towards the middle to bottom of the deposit and hasn't been mined yet. Hence, the best is still to come. 3) Drilling along strike toward the West Pit Extension shows there is even more upside to the mine, either as a larger open pit and/or low-grade, bulk tonnage, underground operation (as widths are phenomenal). Highlights include 32.3 g/t gold over 4.8m at 955m depth, 2.9 g/t gold over 29.7m at 305m depth, 6.0 g/t gold over 32.7m at 481m depth, and 2.3 g/t gold over 88.2m at 806m depth. All intercepts are estimated true width.

{kind=link}

Agnico Eagle

Given the size of the resource and recent exploration results, Detour Lake could be producing for 30-40 years at the current run rate. That's why AEM is looking to increase output and bring forward a substantial amount of production.

A 1 million-ounce Detour Lake operation would put Agnico Eagle's total gold production at ~4 million ounces, which is knocking on the door of Barrick Gold.

I've been stating for years that Detour Lake is a truly exceptional asset and how the best was still to come. Most investors who complained when AEM bought KL didn't understand the potential of this mine because they were looking in the rear-view mirror—as the operation was struggling in the early years of its mine life and costs were higher—instead of looking at what was ahead.

By no means is Detour Lake at 1 million ounces priced in.

The X-Factor

AEM has a substantial drill program in place this year, which was recently increased by $30 million to just over $350 million in total, and includes approximately $57.3 million of drilling at Fosterville.

I'm curious about the results from this mine, as it has the potential to move the needle in a major way.

When Fosterville was at its prime a few years ago, infill drilling at the Swan zone was hitting anywhere from ~200 g/t to ~1,000 g/t and over 6-8 meters. Recent drill results show some similar grade intercepts (hole UDH413 hit 365 g/t and included 1,075.8 g/t), but widths are only around 1 meter. These results indicate that Fosterville isn't about to return to its previous form, but 1) that's not required, 2) there is more exploration to go, and 3) these drill holes show that Fosterville could see additional high-grade, low-cost mine life, which isn't currently priced in.

Agnico Eagle

I'm not suggesting that another major discovery will occur at Fosterville and the mine will return to world-class status again, but with the aggressive drill campaign and some promising recent drill results, Fosterville is just a bonanza-grade drill hole or two away from becoming a momentous bullish catalyst.

So, keep an eye on what's happening at this asset, as it could add more value to AEM.

Gripes

While I wouldn't call them concerns (minor complaints, perhaps):

1) I don't believe the Yamana acquisition is a home run, as while it's highly strategic, AEM isn't getting a bargain, they are taking on 100% of the project risk and CapEx, and the underground mine at Malartic likely won't be as robust (on a production and cash flow basis) as the open pit.

2) The announcement back in September 2022 in which Agnico Eagle agreed to purchase a 50% interest in the San Nicolás copper-zinc project in Mexico was out of left field and a real departure from the norm for AEM. San Nicolás is an extraordinarily high-grade project (~2% CuEq) and will be developed with the Teck, but this is still a base metal mine, and AEM is a gold producer. It's not a mega-sized project, and I don't believe it detracts from the gold operations, but it's not something I would like AEM to pursue further, or maybe I should say, build upon. When I survey the landscape and look at all of the undervalued gold projects available, that's where I would like AEM to focus.

Overall, there isn't much to dislike.

Technicals Show A Potential Breakout Above The Multi-Year Downtrend

Let's now turn to the technical side of AEM.

A few key technical events are happening at the moment, as the stock is: 1) breaking above overhead resistance at the 200-week, and 2) close to breaking out above the top of the multi-year downtrend channel. I can't tell you what AEM will do over the next several days or weeks, but I will make a few observations about the chart, its structure, and how it relates to the valuation of AEM. I felt back in September that sub-$40 wasn't sustainable as Agnico Eagle was firing on all cylinders and still had exceptional margins even with gold at $1,600. At some point, downtrends end because valuations begin to support price levels. We are at that point with AEM. The stock could very easily fall back down to ~$45 if there is a sharp correction in the sector over the next few weeks (not a forecast), but I believe the path of least resistance is higher. Once $55.00-$57.50 is cleared, then momentum will build further. I do believe that AEM has upside even if gold is flat over the next 6-12 months, and a retest of the 2020 highs—which is a 50% increase from current levels—should easily occur if gold breaks out.

StockCharts.com

In Summary

Agnico Eagle is firing on all cylinders right now. Maybe that changes in the short-term, but that's the whole point of buying AEM. They are so well diversified and have such an exceptional team leading the company that they can withstand setbacks.

Case in point is their Goldex mine in Canada, which was shut down and written off in 2011 due to unstable rock conditions and flooding, which decimated the stock. But AEM worked the problem and eventually got Goldex back into production. It's still in production today and is expected to continue to produce until at least 2030.

We can never be sure what will happen with these assets, but I have a very high level of confidence in this team and its ability to overcome obstacles.

The drop since April 2022 was extreme for a stock like AEM, especially absent a market crash. But since the July bottom, AEM has formed a higher low, and the technicals are definitely indicating a possible bullish reversal is occurring.

Even if gold is range-bound, there is the potential for AEM to outperform and see its stock price appreciate 20-25%. There are so many positives about the company—extremely well diversified, incredibly low jurisdictional risk, managing through this inflationary environment as margins remain stellar, fantastic management team and Chairman that are proven mine builders and operators, and cheap valuation—that AEM is a must-own stock at these levels, even if gold does nothing.

For further details see:

Agnico Eagle: Why This Gold Miner Is A Top Pick