CA - Air Canada: Encouraging Earnings Rebound But Watch International Passenger Revenues

2023-10-10 11:12:36 ET

Summary

- Air Canada has seen a significant drop in stock price despite impressive performance in Q2 2023.

- Adjusted diluted earnings per share, operating revenues, free cash flow, and net debt have all shown positive growth.

- I take a bullish view on the stock overall, but investors may remain cautious if Air Canada lags behind its peers in international passenger revenue growth.

Investment Thesis: I take the view that Air Canada has the capacity to see further upside on the basis of strong recovery in earnings and reduction of net debt. However, upside will also significantly hinge on Air Canada's capacity to further bolster international passenger revenues going forward.

In a previous article back in July, I made the argument that Air Canada ( AC:CA ) to continue to see upside going forward, on the basis of strong growth in passenger revenue per RPM.

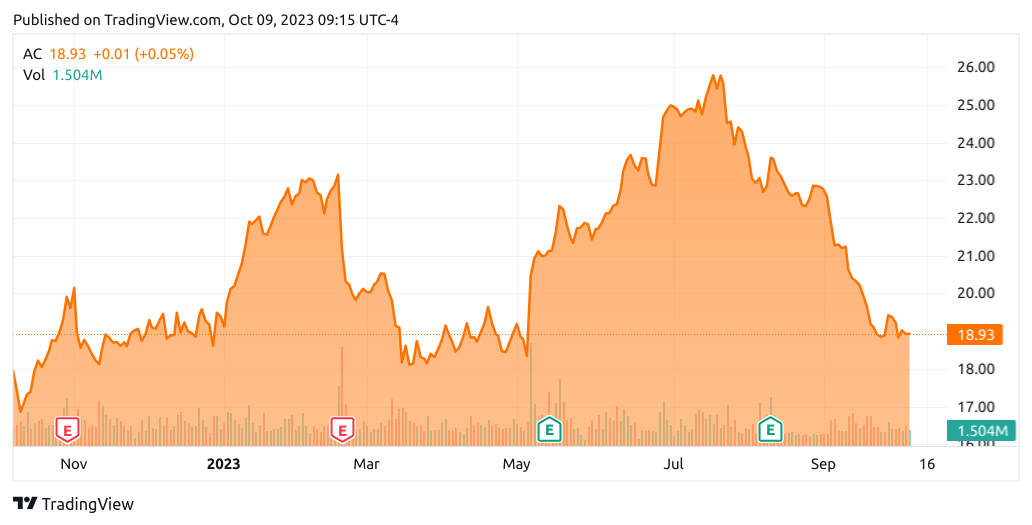

However, the stock has descended significantly to a price of CAD 18.93 at the time of writing:

{kind=link}

The purpose of this article is to investigate why Air Canada has seen such a significant drop over the past three months, and whether the company has the ability to see continued growth from here taking recent performance into consideration.

Performance

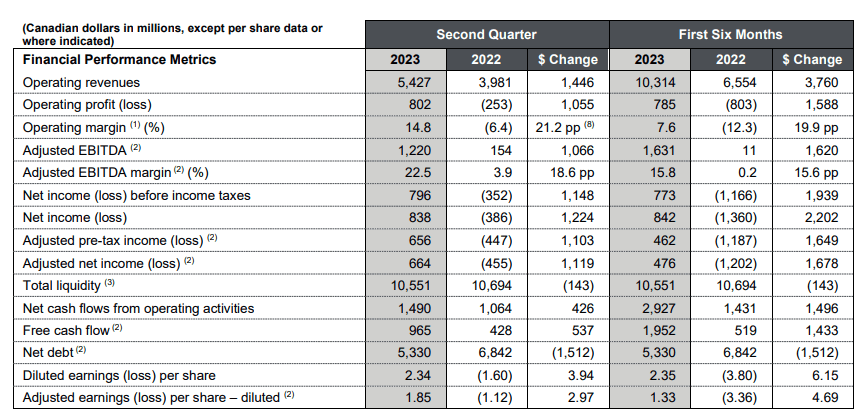

When looking at the most recent earnings results for Air Canada, we can see that performance on the whole has been quite impressive in Q2 2023 as compared to that of Q2 2022.

Air Canada News Release: Second Quarter 2023 Financial Results

{kind=link}

Adjusted diluted earnings per share have rebounded comfortably into positive territory, while operating revenues are up by 36% as compared to that of the same quarter last year. In addition, free cash flow has more than doubled from that of last year, while net debt has decreased from CAD 6.842 billion to CAD 5.330 billion.

Moreover, when we look at the historical trajectory for passenger revenue per RPM, we can see that the same is both higher than that of the last quarter at 22.7 cents, as well as being higher than that of the same quarter in 2022.

Figures sourced from historical Air Canada News Releases (Q1 2019 to the present). Heatmap generated by author using Python's seaborn library.

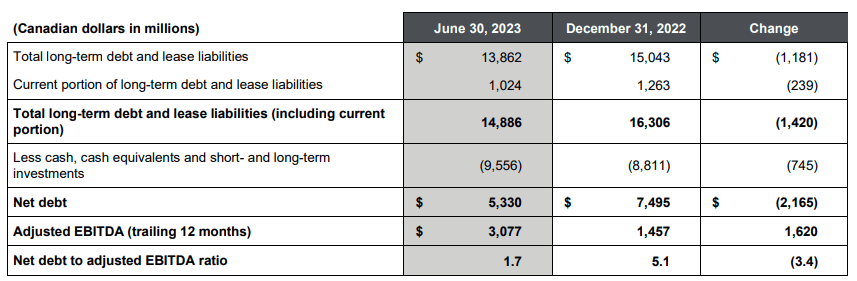

Coming back to the decrease in net debt, we can also see that over the past six months - the company's net debt to adjusted EBITDA ratio has seen a strong decrease over this period, meaning that Air Canada is taking on significantly less net debt relative to its earnings - the latter of which has also seen a strong increase over the period.

Air Canada News Release: Second Quarter 2023 Financial Results

{kind=link}

From this standpoint, I take the view that Air Canada's performance in its most recent quarter has been quite encouraging.

My Perspective

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, I fail to see a rationale for the sharp drop in price that we have seen in the stock given the above results.

In particular, when looking at Air Canada's EV/EBITDA ratio, we can see that the ratio has descended to pre-2020 levels while earnings per share has continued to grow this year and is steadily starting to approach levels seen pre-pandemic.

ycharts.com

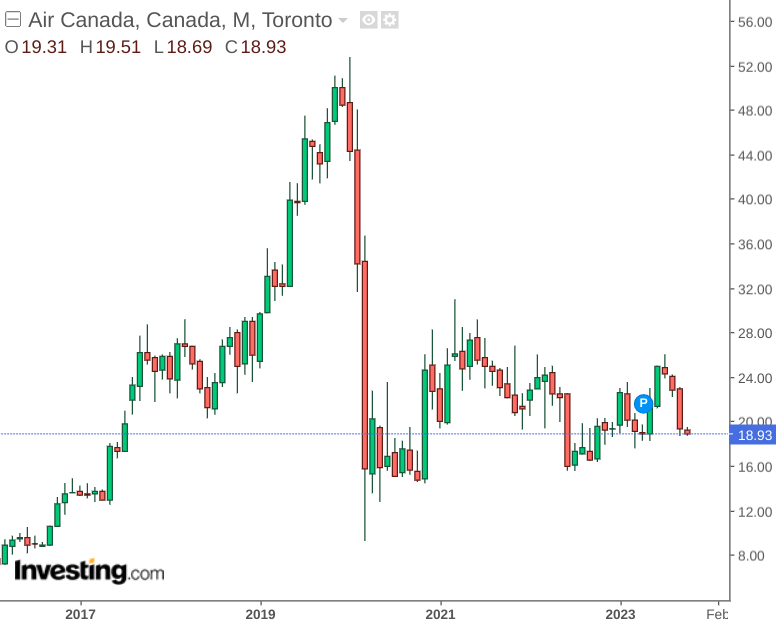

From this standpoint, I take the view that the stock could have room to rise if we see further earnings growth going forward. However, when looking at stock price on a monthly chart - we can see that Air Canada still remains well below 2019 levels:

{kind=link}

In spite of an encouraging rebound in earnings as well as a decline in net debt to adjusted EBITDA - Air Canada's recent improvements have not been reflected in the stock price.

It has been reported that one of the potential reasons for the lag in growth has been a lagging behind in a recovery of passenger miles flown as compared to other global airlines. For instance, while passenger miles flown in Q2 2023 had recovered to 92% of the same period in 2019 for Air Canada - this still lags behind a level of 94% among global airlines.

From this standpoint, while there is the possibility that investors are undervaluing Air Canada given the company's rising earnings growth and decreasing net debt - there is also the possibility that we could see investors remain cautious if Air Canada is perceived to be lagging behind its peers.

Risks and Looking Forward

In terms of the potential risks to Air Canada at this time, I take the view that while the recovery in passenger revenue per RPM along with earnings growth and net debt reduction has no doubt been encouraging, it is likely that growth for Air Canada (as well as the airline sector more generally) will start to plateau going forward, as the recovery in passenger demand post-COVID begins to stabilise.

Moreover, when we look at the percentage share of passenger revenues for each region - we can see that the share for Canada fell from 30% to 26% from June 2019 to June 2023 - while that of the Atlantic rose from 26% to almost 34%.

| Regions |

| June 2019 |

| June 2019 (% share) |

| June 2023 |

| June 2023 (% share) |

| Canada |

| 1338 |

| 30.84% |

| 1282 |

| 26.16% |

| U.S. Transborder |

| 959 |

| 22.11% |

| 1037 |

| 21.16% |

| Atlantic |

| 1159 |

| 26.72% |

| 1665 |

| 33.97% |

| Pacific |

| 621 |

| 14.32% |

| 573 |

| 11.69% |

| Other |

| 261 |

| 6.02% |

| 344 |

| 7.02% |

Source: Figures sourced from Air Canada Q2 2019 and Q2 2023 Consolidated Financial Statements and Notes. Percentages calculated by author.

In this regard, we can see that international revenues have become more important to overall passenger revenue growth post-pandemic. Accordingly, should international passenger miles continue to lag behind that of global carriers, then investors may continue to remain apprehensive of the stock.

Conclusion

To conclude, my own view on Air Canada is that the company has strong potential to see upside on the basis of a strong recovery in earnings growth as well as a reduction in net debt to EBITDA.

However, I caution this with the fact that international passenger revenues have become increasingly important to Air Canada's growth post-pandemic. Thus, in addition to the encouraging performance we have seen to date, investors are likely to want to see further evidence that Air Canada can continue to grow passenger revenue internationally.

In summary, I continue to take a bullish view on Air Canada - but will be paying close attention to the company's trajectory in boosting passenger revenues across international segments going forward.

For further details see:

Air Canada: Encouraging Earnings Rebound, But Watch International Passenger Revenues