CA - Air Canada: There's Light At The End Of The Runway

Summary

- Air Canada reported Q4 and FY2022 results that showcase a robust bounce back in travel spending.

- Consumers are not cutting back on travel as much as other discretionary spending in the short term, while the company is strengthening its presence in Eastern Canada.

- Total debt remains a concern, and elevated oil prices mean elevated fares, which may eventually cut into demand as a minor recession fully reverberates in the global economy.

- I take a cautious stance, but believe it's worthwhile to take a small position in the low 20s range - I forecast a 12-18 month share price of $30.

Introduction & Thesis

Air Canada ( AC:CA ) is a leading Canada-based airline company that has been in operation for over 85 years . The company provides air travel for passengers in the Canadian market, the Canada-United States (U.S.) trans-border market and in the international market to and from Canada. AC:CA also provides cargo services throughout Canada, though it is a minor piece of the revenue mix. AC:CA is the largest airline in Canada and the fifth-largest airline in North America by passengers serviced and is also part of the Star Alliance , the world's largest global airline alliance. The company has several brands, notably Air Canada, Air Canada Rouge, the discount carrier, and Air Canada Vacations, a comprehensive vacation package offering that mostly services the Caribbean. AC:CA owns the Aeroplan loyalty program, which allows individuals to accumulate Aeroplan points through travel on AC:CA and select partners for redemption of travel vouchers, gift cards and other redemption options. As of Jan. 27, 2023, the company operated a fleet of 187 aircraft .

Throughout 2022, Air Canada has been a beneficiary of the post-COVID travel recovery and has posted positive operating income from Q3 onwards. Consumers seem willing to still spend on travel, even as prices remain elevated . Business travel seems to be recovering as well, and Air Canada is bolstering its stronghold on Eastern Canada as they consolidate routes and right-size their operations amidst a push to reduce their debt. While macroeconomic risks, like oil price volatility and COVID flare ups remain, AC:CA seems to have finally turned the corner and may be worth a cautious Buy. I forecast a share price of $30 within a 12-18 month term. All numbers in CAD unless otherwise noted.

2022 Results and Outlook

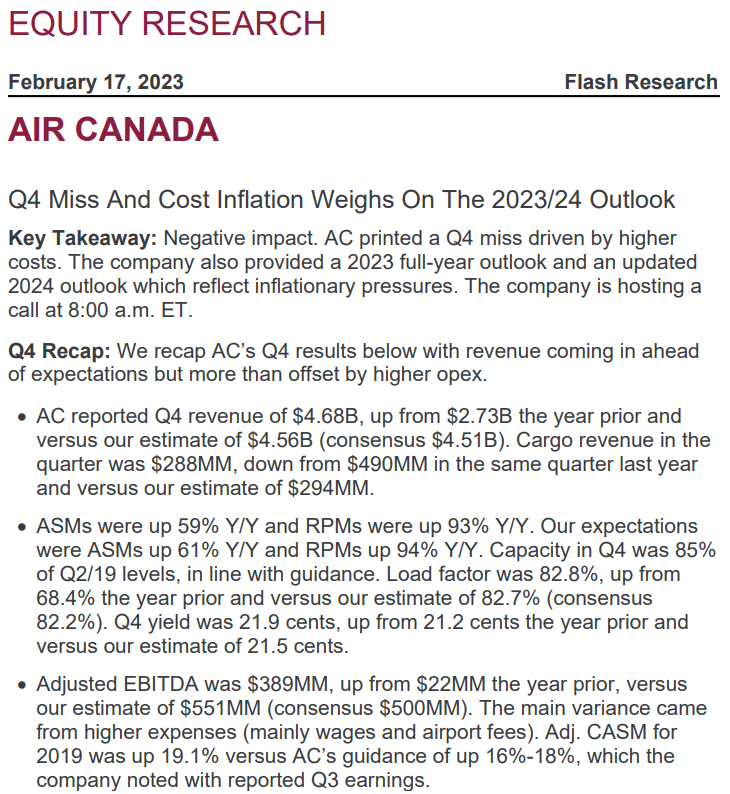

AC:CA announced quarterly and 2022 year-end earnings on Feb. 17, 2023 that missed expectations, as evidenced by a 8% share price drop post release. The company reported record revenue of $4.7Bn and narrowed operating losses to $22MM compared to Q4 of 2021. Compared with Q4 of 2019, revenue increased about 2% on 85% of the capacity and 87% of the traffic. Transborder flight revenues hit $916MM, surpassing Q4 of 2019 by 1% on 7% less capacity. Adjusted EBITDA totaled $389MM in the quarter, a significant increase from the adjusted EBITDA of $22MM in Q4 of 2021, while net cash flow from operations in the quarter hit $647MM. Highlights also included the continued success of diversifying revenue sources, with cargo revenue in Q4 of 2022 55% higher than that in the same period prior to the pandemic. Michael Rousseau, CEO of AC:CA, also noted in the executive call that Air Canada Vacations delivered impressive results, and that Aeroplan's active membership is at an all-time high and continually increasing. From a demand stand point, sticky prices are not scaring consumers, as evidenced by strong load factors amid high prices and less volume of flights.

{kind=link}

Executives also provided cost updates and guidance, along with responses to analyst questions, in the year end executive call. Fuel expenses of around $1.5Bn, which increased $794MM from Q4 of 2021, were mostly due to a modest increase in fuel prices, a 37% increase in liter usage due to more flying and an unfavorable foreign exchange variance. Costs per available seat mile also came within range, with a slight bump mainly attributable to sales and distribution costs, inflationary pressures across all line items, higher weather disruption costs, and employee benefits expenses. The company also announced that previously announced airplane arrivals remain on track and that liquidity totaled $9.8Bn. In the updated guidance outlook, AC:CA provided some further details, as evidenced below.

Air Canada Q4 Results

Analysts grilled executives on several key categories, notably on costs. Kevin Chiang of CIBC noted that some of the CASM targets may appear structural, as those costs would exceed 2019 levels, while volume capacity would only near 2019 levels next year. Executives noted that they wanted to get ahead on labor, procurement and AI, but it will be interesting to see if these costs can fall even as growth ramps up. They cautioned however that ground handling crew and catering costs remain near term pressures. AC:CA released solid results that sets the stage for a strong 2023. Between the new planes coming in 2025, a focus on improving the balance sheet, and strong demand, I think the pieces are in place to bounce back in 2023.

Industry & Competition

Air Canada is a leader in the Canadian air transport industry, a market with an estimated value of $32Bn this upcoming year. AC:CA generates revenue mainly from passenger revenue, which is the key focus of the industry. AC:CA is a global operator, and their network within the Star Alliance allows efficient route sharing across the world. Air Canada operates in two key consumer and geographic segments within consumer aviation. In the consumer category, they operate within leisure and business travel, and geographically they have domestic and international routes, with a focus on direct flights to North/Central America and Europe. While business travel was slow to recover in comparison to leisure travel to start the year, it has roared back post Labor-Day and has sported impressive growth from Q4 onwards. Canada is on track to return to 97% of 2019 available seat miles by the end of Q1 2023, according to American Express Global Business Travel. So while the industry is difficult to predict given various global factors, from inflation, to oil prices, to COVID, at least in the short term, the recovery is clearly underway and is sustaining itself well.

{kind=link}

AC:CA has several main competitors in both Canada and globally. In Canada, WestJet, owned by Onex Corp ( ONEX:CA ) is the closest competitor to a full scale operator. WestJet is the second-largest Canadian airline, and as of 2018 (before they were taken private), was the ninth-largest carrier in North America. AC:CA has subsidiaries that also compete with low-cost carriers, many of whom have popped up within the last few years including Flair, Swoop, Lynx and Canadian Jetliners. Internationally, AC:CA has had a close partnership with United Airlines ( UAL ) for years, and continues to improve its collaboration across the Star Alliance. This should lead to synergies as more countries open up to tourism, specifically in Asia. AC:CA also directly competes with Delta Air Lines ( DAL ) and American Airlines ( AAL ) within North American routes.

Domestically, AC:CA has operated in a position of strength for decades, and surprisingly, the post-pandemic rebound has led to the company to strengthen its position. While low-carriers have eaten into major routes, such as Toronto-Montreal, Toronto-Vancouver, and high demand routes to the U.S., AC:CA has been able to differentiate itself with more convenient scheduling and via a better fleet and service. AC:CA ranks #1 in its employee net promotor score and is able to keep pricing power via these strengths. Additionally, the mid-low demand routes throughout eastern Canada lack any competition, as new competitors only have the scale for high demand routes. This has led AC:CA to box out competition post pandemic, as all airlines deal with staffing shortages and higher fuel costs. WestJet is doing the same thing out west - instead of competing with AC:CA in the east, WestJet has announced that Calgary will be their exclusive hub , further solidifying its own territory. However, with ~70% of Canada's population in east Canada, AC:CA's strategy of solidifying its position around existing hubs should pay dividends into 2023. Given these post-pandemic developments, and a strong demand environment as evidenced in the recent quarterly results, AC:CA is providing increased confidence in its ability to generate a significant amount of cash flow in the near term.

{kind=link}

Risks

There are dozens of risks running an airline, but a few key risks that may impede AC:CA stock from taking flight include: A large pilot shortage in Canada, oil price volatility, and travel restrictions. Canada has seen its new pilot license count drop drastically over the past few years, notably an 80% drop last year from 2019. To combat this, AC:CA has increased its hiring from regional carriers, and has noted that they have been " able to attract pilots " as travel demand has rebounded. But this short-term solution is not viable long term. AC:CA will have to work with regulators to ensure that new licenses are provided to pilots in training to ensure all levels of airlines, which will keep long term labor costs in check and sufficient options for consumers.

Oil price volatility also remains a major cost risk for AC:CA. Jet fuel is made with mostly crude oil, which has had a range from $71.02-$123.70 over the past 12M (as of Jan. 31/23). This extensive volatility leads to uncertainty across setting prices, and can cut into profitability. The final key risk to note is health related - while in North America, restrictions have mostly been done-away with for over a year, in China and other nations in Asia, restrictions just ended recently. As we saw in North America, many consumers still remained fearful of flying even after restrictions ended, so I expect a bumpy return in the far east.

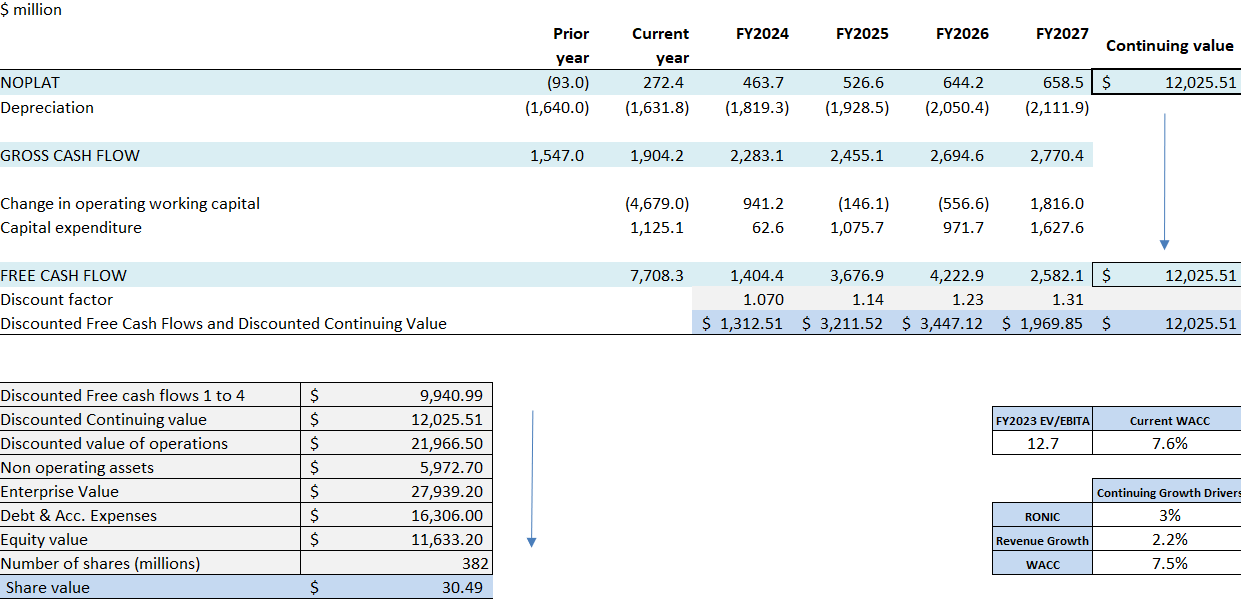

Model Shows Upside

AC:CA has seen share price volatility this year, as the airline sector has rebounded in a choppy fashion. The company's net cash position of almost $10Bn provides sufficient liquidity to fund current growth plans. The model forecasts a current WACC of 7.7%. The weighted average cost of debt of 5.3% and a net debt to EBITDA ratio of 5.1 sting, but a continued focus on cleaning the balance sheet should pay dividends later this year.

Author WACC

I forecast the continuing value of $12.1Bn, given a 14% revenue increase this year and blended revenue growth of ~7% for three years as choppy growth increases eventually flatlines. I anticipate adjusted EBIDTA next year to hit $2.6Bn, within the guided range of $2.5Bn-$3Bn. I see margins holding steady into the end of the year and hold other cost ratios mostly in line with guidance. I see the load factor increasing over time toward 83%, and available seat miles to hit 91% of 2019 figures. Coupled with a terminal WACC above 7% and a terminal revenue growth rate of 2.15%, a $30 share price (see below) can be supported by fundamentals, but the stock will be volatile.

{kind=link}

{kind=link}

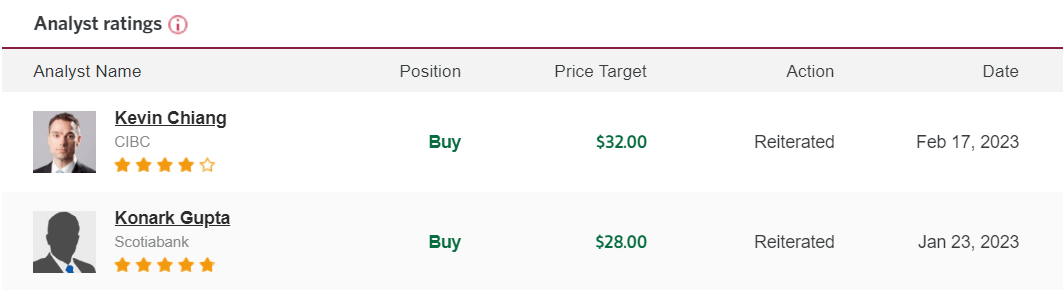

The share price is supported a FY2023 EV/EBITDA ratio of 12.7, in line with industry peers and analyst estimates. I don't think AC:CA will turn a large profit next year, if any, but the building blocks are in place to see the company bounce back and the stock flourish. The $30 share price is in line with analysts across the street.

{kind=link}

Conclusion

AC:CA remains the leader in the Canadian airline industry and is worth a buy at these levels after a big drop post Q4 earnings. The company sports robust operations and continues to expand globally. Management has consistently delivered impressive returns on capital and the company has a history of good CASM rates compared to top competitors . While global oil prices are a key risk, AC:CA is primed to succeed, with blockbuster demand remaining strong across several verticals domestically and internationally. AC:CA is worth a cautious buy at these levels, and I expect a swing back toward $30 before the end of the year.

For further details see:

Air Canada: There's Light At The End Of The Runway