MSFT - Akamai: Now Facing Amazon And Microsoft But In A Differentiated Way

Summary

- Widely known for its CDN, Akamai has embarked on a business transformation process that will see it compete with hyperscalers Amazon and Microsoft.

- The very idea of it facing such a "hyper-competitive" environment has spooked analysts who have downgraded the stock.

- However, a more detailed look reveals that the CDN play which also specializes in cybersecurity exhibits a high level of product differentiation.

- This is the reason why I value the company higher than its market actual price, after moderating to account for risks.

- I clearly substantiate my bullish position using the product differentiation table which also shows the growth potential and opportunities for margin gains.

While everyone is speaking about ChatGPT and AI (artificial intelligence), Akamai Technologies ( AKAM ) has quietly launched its Connected Cloud. As I will elaborate upon later, its scale suggests that it would compete with hyperscalers Microsoft (NASDAQ: MSFT ) and Amazon (NASDAQ: AMZN ) namely for the Compute (cloud computing) business with the Akamai Connected Cloud.

Ironically, despite the announcement only a few days ago, the company's shares dropped by more than 10% at some point, and, the reason for this is analysts at RBC downgrading the company, namely because of the " hyper-competitive " nature of Akamai connected cloud. To provide investors with an idea of the degree of volatility which has impacted the company's stock, I have provided a comparison with the one-year performance of the Invesco QQQ Trust ( QQQ ) in the orange chart below.

However, as this thesis will elaborate upon, the downgrade is not justified, namely because of the differentiation approach involving Akamai's global edge network and security products where it is ahead of the hyperscalers.

I start by providing a brief overview of how the company has evolved from a CDN play to a security one before embarking on the cloud computing transformation.

The Evolution from CDN to Cloud Compute

Akamai is the historical leader in Content Delivery Network ((CDN)) services, which basically encapsulates cache technologies that are responsible for the Internet being fast in the first place. Well, contrary to what you may believe, fast internet does not only depend exclusively on your connection speed but also on the availability of intermediary cache servers which by storing items like frequently-used images or videos, offers a faster user experience, more specifically, by circumventing the need to download the data from the original source. In addition, Akamai also provides features like reliability and security for its customers.

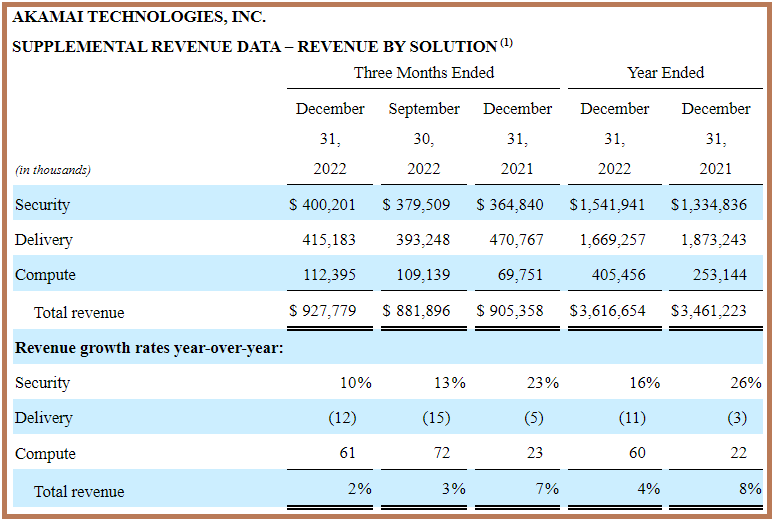

Furthermore, as seen by the revenue by solution table below, the security part of the business has been growing faster than CDN where it faces intense competition not only from pureplay like Cloudflare ( NET ) but also from Amazon's AWS CloudFront, Google's (NASDAQ: GOOG ) Cloud CDN, and Microsoft Azure's CDN. These are hyperscalers diversifying into content caching.

Revenue by Solutions from SEC Filings (seekingalpha.com)

{kind=link}

Coming back to security which constituted 42% of overall revenues in 2022, the company proposes advanced cybersecurity solutions for companies like Zero Trust Protection which, contrary to the outdated parameter defense system, is a strategy whereby all persons or devices outside of a company's network are restricted from accessing corporate computer systems, except in case of explicit need. This is the sort of advanced security mechanism which offers protection against the latest threats.

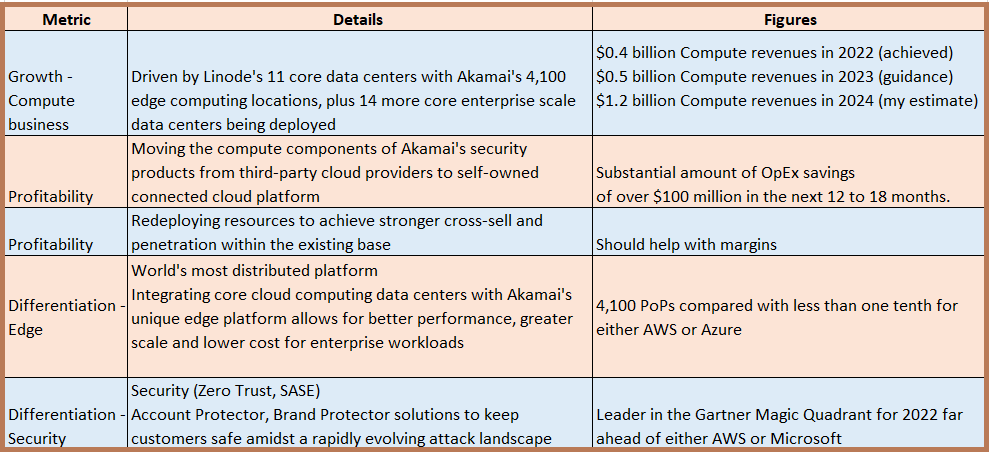

Interestingly, the Compute business which essentially consists of proposing IaaS or Infrastructure-as-a-Service (IaaS) resources, has grown by a whopping 60% from the fiscal year 2021 to 2022, compared to only 16% for Security. The main reason for this growth is the acquisition of IaaS provider Linode, for about $900 million in February 2022, with the deal being expected to add about $100 million to Akamai's revenues.

To have an idea of the scale, $900 million represents around one-quarter of the company's revenues for 2022, which is significant and thus, this acquisition marks a turning point or transformation in Akamai's business strategy whereby it has now started to compete with the hyperscalers in addition to others like DigitalOcean ( DOCN ).

{kind=link}

However, this is not completely true as hyperscalers themselves have already expanded into CDN, which is Akamai's turf, and pursuing further, the company is not competing merely as another cloud computing provider but, also using a differentiated approach, namely as the world's most distributed computing platform.

Distributed Computing Platform and Profitability

In this respect, Akamai's Compute business is seeing traction within the media vertical or companies specializing in the processing of videos and images whose content needs to be cached. In addition, there is interest from other verticals like gaming and commerce where performance at the outskirts or edge of the network is key.

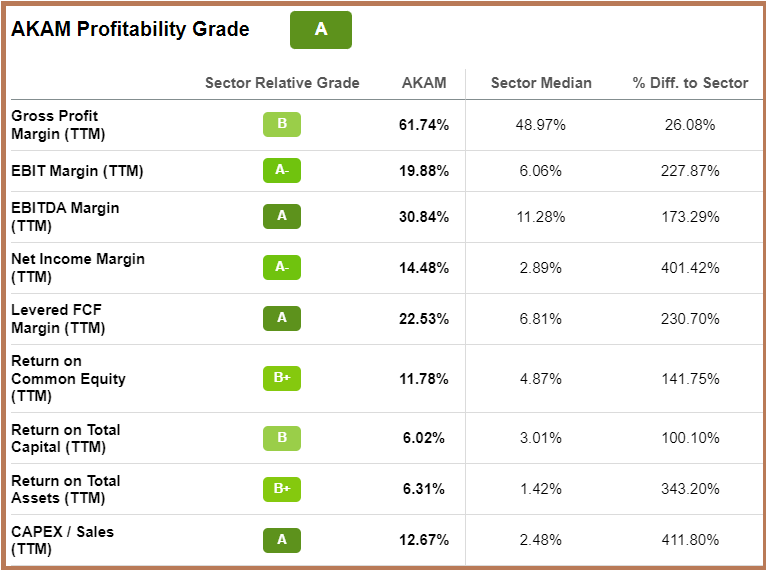

However, the fact that the executives also talk about "better performance at a more competitive price point", suggests that they may have to offer discounts in order to promote the Akamai Connected Cloud as pictured above, and that profitability could suffer. Still, the company's profitability grade as pictured below, suggests that it can tolerate some additional expenses without seeing its position relative to the IT sector median impacted by too much.

AKAM's Profitability Grade (seekingalpha.com)

{kind=link}

Noteworthy, having dedicated cloud offerings also enables Akamai to save on costs, namely, by moving the Compute resources consumed by its security products to its own infrastructure. In this way, some $100 million should be saved from 2023 to mid-2024.

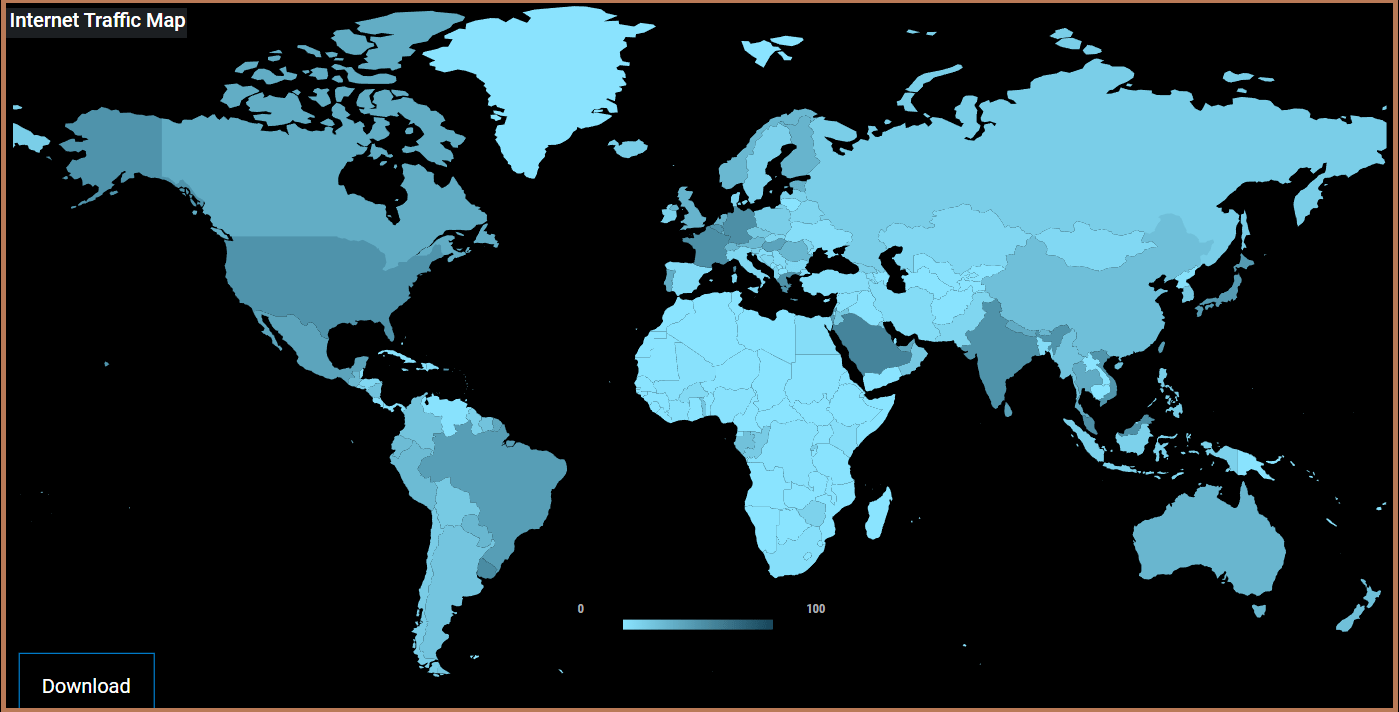

Also, building over its 25 years of experience in caching which has translated into a presence in most of the world's server rooms through PoPs or Points of Presences as per the picture below , the company has developed a unique edge platform. This is basically computing far away from metropolitan centers and enables the company to provide customers with the sort of geographical scale comparable with the likes of the hyperscalers, prompting its executives to term it the world's most distributed computing platform.

Internet traffic Map (www.akamai.com)

{kind=link}

To be realistic, achieving the sort of traction seen by hyperscalers will depend on how Akamai's edge architecture is integrated with its core cloud computing offerings, and, it also has to invest heavily. Thus, in addition to the 11 core data centers obtained through the Linode deal which are now integrated into its 4,100 edge locations, the company is building 14 more enterprise-scale data centers.

Valuations and Risks

This implies heavy Capex usage or 21% of total revenues in 2023 compared to 12.7% last year (above table) as three data centers (out of the 14 planned) are scheduled to come online. Now, based on the eleven Linode data centers costing $900 million, only three data centers will cost $245.5 million ((900/11)x3). Taking into consideration the Capex utilization of 21%, this comes to revenues of about $1.2 billion (245.5 x 5).

Now, the company aims to obtain $0.5 billion from Compute in 2023 against around $0.4 billion in 2022. Therefore, the bulk of the revenue or $0.7 billion ($1.2 - $0.5) should be in 2024. This amount increases the revenue estimate for FY-2024 from $3.99 billion to $4.69 billion, or beefs up the growth from 6.88% to 25.73% ((4.69-3.73)/3.73) as per the table below.

Now, since sales are the denominator in the price-to-sales multiple, the P/S falls to 0.82x, or ((3.05*(6.88/25.73)) instead of the initial 3.05x .

Table built using data from (seekingalpha.com)

With a forward P/S of 0.82x, it means that the stock is significantly undervalued when compared to the sector median of 2.92x by around 72%. Adjusting accordingly, I obtain a target share price of $133 (77.3 x 1.72).

This is a high share price and there are always stock downside risks in a highly competitive marketplace together with unfavorable macroeconomics where the Federal Reserve may continue to tighten monetary supply as inflationary pressures persist. Now, with higher borrowing costs, come fears of a protracted economic slowdown. Hence, moderating my bullish position, I have a lower $90 target which was the support price before analysts' sentiments toward the company started to change.

This said, I remain highly optimistic about the company's Compute business.

Highlighting the Differentiated Approach

The first reason for this is that despite facing some moderation, IT spending should continue to climb in 2023 according to Gartner . Second, according to Uptime , some reported declines have been exaggerated as corporations prefer expanding their IT infrastructure on the cloud rather than on-premises. For this matter, the double-digit growths of Amazon Web Services (20%) and Azure (31%) in their last reported quarters show that amid the slowdown, revenues continue to grow.

Now, when faced with these giants and their ability to cut prices to sustain sales, it is normal for analysts to be skeptical about Akamai's potential. However, the CDN play brings the edge differentiator. In this case, with more data being generated and processed closer to subscribers (mobile users or work-from-homers using their laptops), the edge computing market is expected to grow faster or at 37.9% from 2023 to 2030, compared to only 16.8% for the cloud computing market in general.

Detailing further, with its vast CDN network comprising 4100 PoPs spanning 134 countries and about 365K edge servers, the company has a more distributed edge platform than Amazon with 410 PoPs. In comparison, Azure has about 118 edge locations. Therefore, with enterprises more likely to route their cloud traffic through the edge in order to take the shortest route and optimize costs, it is Akamai that should benefit more from its distributed infrastructure as pictured below.

On top, Akamai's secured access service edge or SASE is key for customers' cybersecurity requirements, and the company has been named as a leader in the Gartner Magic Quadrant for 2022 far ahead of either AWS or Microsoft.

Product Differentiation Table Built using data from (www.seekingalpha.com)

{kind=link}

Thus, one can envision the emergence of another cloud computing play within the highly competitive market, but one which provides for a better and more secure mobile and web experience, and builds on its experience in media delivery and entertainment experiences.

Conclusion

Thus, by considering the product differentiation aspect, this thesis has shown that Akamai should be able to compete with hyperscalers without necessarily using a discount strategy, but rather one which revolves around providing value-added features around edge computing and security.

I also valued the stock accordingly. Still, investors should be aware that, with many analysts focusing exclusively on cloud computing, there can be further downgrades, which can result in further volatility.

Finally, with the integration synergies between Akamai's core data centers and its existing edge platform, together with cross-selling opportunities, there should be margin gains to offset some of the expenses as Akamai executes its business transformation process.

For further details see:

Akamai: Now Facing Amazon And Microsoft, But In A Differentiated Way