PLTK - Akatsuki: Negative EV At Odds With Dominant Gacha Game Titles Growth Prospects

2023-06-22 07:00:00 ET

Summary

- Akatsuki Inc. has a massive war-chest of over 45 billion yen in net cash, almost 2x the company's market cap, that can be deployed very profitably into video games and web-comics.

- Currently, Akatsuki is already a dominant player in the Japanese 'Gacha' Game industry (gambling economics), with the massive Dragon Ball Dokkan game under its belt, bigger than Angry Birds 2.

- Akatsuki has also succeeded in developing games based on its own IPs, like Cinderella Nine which was a moderate success, and the newly launched web-comic business should spawn new franchises.

- Comics are at a profit trough as it's a brand-new business, and we should see stabilization in games as ramp up for a seasonally strong Q2 finishes.

- With ample reinvestment opportunities in the anime/manga and Gacha Game spaces, earnings growth is very likely in the longer-term as is stock growth starting at negative EV. Moreover, receive a >3.5% dividend while you wait.

Published on the Value Lab 06/12/23 - Note that we always consider the proposition based on liquidity and market conditions on a stock's domestic market, in this case in Japan.

Akatsuki Inc. ( AKAFF ) is an extraordinarily compelling opportunity. The essence of shareholder value creation is profitable reinvestment to create a value creation engine. Akatsuki not only has 46 billion yen in net cash to invest, incidentally 2x the company's market cap and the reason for a deeply negative EV, but it has a dominant title in the Japanese Gacha Gaming videogame space in Dragon Ball Z Dokkan Battle and ample room to launch more games on its own IPs too, fostered in their newly minted Comics segment which will be another avenue for monetizing Akatsuki's creations. Gacha Gaming is possibly the most profitable videogaming market whose economics are akin to gambling companies, and it's a growing market too. Moreover, dissemination of anime and otaku culture also keep the horizons secular for growth of this home-grown industry as titles increasingly face the rest of the world, and not just the Japanese market.

Akatsuki is seeing a bit of a hit as COVID-19 reversals take hold, as well as one-offs over a recently transferred app have reduced revenues. Ramp-up investment for a seasonally blockbuster Q2 as well as establishment of the Comics segment launched in July 2022 have kept SG&A stubborn as well, so earnings have taken a hit. Akatsuki stock prices are at long-term lows.

However, comics is already turning around from a profitability trough, and the gaming segment is also going to settle down next year as a new title called TRIBE NINE nears release probably in a couple of quarters. At historically low 2016 prices and a deeply negative EV, Akatsuki offers investors imminent stabilization if not possible turnarounds in profits in a growing and highly profitable industry that can be a sink for value generating growth CAPEX. Moreover, heightened interest in Japanese markets and efforts by exchanges to promote more shareholder-friendly behavior create promise for recognition of the value gap from the N.O assets that drive the EV into an unreasonable negative territory. Private equity are also homing in on the mobile gaming space.

Finally, while investors wait, they get paid a relatively generous 3.8% dividend by Japanese standards. An extremely compelling opportunity in terms of upside with very pronounced downside protection to boot - plus there's an income proposition and finally no real liquidity worries with more than $600k in daily liquidity as reported on Saxo Bank. A no-brainer buy.

Primer on Akatsuki's Market

Akatsuki develops Gacha Games, which is a relatively infamous term for those who are in the gaming space. They are present in a meaningful way on mobile platforms.

For the layman, Gacha Games should be understood from its analogue roots, which are capsule toys, where at a station or in an arcade you put in a quarter and out comes a random capsule with a random toy. Sometimes you get a dupe toy, same as last time, but sometimes you get a rarer toy. Trading card games like Magic: The Gathering, Yu-Gi-Oh! and Pokémon trading cards all work off a similar concept with booster packs too, where some cards are stronger than others when you duel other players, and you never know what a booster pack will bring. In the videogaming context, Gacha Games are just games where key elements that are used within the game come from some sort of random process, and the games are monetized in that to get the chance to receive these random drops you have to pay. What elevates it from a trading card game is the virtual experience - gameplay and animations - that lets you experience your collection in a more interactive way.

Just like the trading card games, LiveOps are required to maintain engagement and drive revenues into a property. With MTG it would be the release of new expansions, like the Egypt-inspired Amonkhet, to bring back players to explore the new cards and come up with new decks. Gacha Games do the same thing, which is introduce new expansions of items, content and/or story that bring players back into the game. These spikes in engagement around periodic LiveOp releases are very common among Gacha Games. LiveOps tend to be relatively cheap compared to the value that you get from the idling engine that is the Gacha Game property, that revs up every time there's a new release, patch or update. For Akatsuki's Dokkan there was the anniversary event in January 2023 that brought Dokkan to #1 in store sales in Japan that month, and a few months later there was a Saiyan Day that similarly created large amounts of engagement. EBIT margins easily keep in the 30% area for this industry, and economics are not typically lumpy, excepting perversions around COVID-19.

The infamy of Gacha Games comes from the random process and the fact that certain finds from booster packs and loot boxes are more effective (or overpowered) for winning the game than others, therefore those who put more money into booster packs are more likely to get powerful elements to outcompete other players with in online gameplay - so these games are usually pay-to-win (P2W). There is a gambling loop to the booster packs, and this is also where the engagement, pricing power and retention comes from. The upside is that while there is a gambling loop, in major Asian markets where Gacha Games are the primary games on offer, there are no regulatory concerns, and these games have lead these markets for decades.

But how big is this market? Focusing on Gacha Games that Akatuski makes, which are generally mid-core games, so not quite for hard-core gamers but not in the typical casual segment that dominates the mobile gaming landscape, the biggest title is Genshin Impact, which was launched in the pandemic year, one of the best ever years for gaming. As of the end of 2022 it had managed over $4 billion in lifetime gross. Every month it easily creates more than $100 million in revenue for miHoYo as people pay for loot boxes for cosmetic upgrades and unlocks of their anime-styled characters.

Akatsuki is one of the main players in the Gacha Games market, a market that often leverages established IPs and is closely associated with anime and otaku culture. In Akatsuki's case it's been leveraging Dragon Ball Z as an IP for its game Dokkan Battle, which has more than $3 billion in lifetime gross since its 2015 launch. To Akatsuki's credit, the market was smaller then so it's difficult to compare with the lightning in a bottle moment for Genshin which has been more of a success, but this whole time Dokkan's been a very steady player and grossing around a quarter of Genshin's sales per month . By relatively recent accounts, it didn't lose its audience to Genshin after its launch in 2020, still grossing at pretty similar run-rates as before of around $500 million per year . The industry segment that Akatsuki is part of is well into the billions (~$10 billion) of dollars annually thanks to large Asian markets, and this is focusing just on the mid-core, mainly anime-styled Gacha Games, which is a subset (possibly around 10%) of the billions of downloads in the mobile gaming panorama and the $100 billion or so of revenues across mobile gaming, an industry growing at around 5% CAGR.

Another major title is Uma Musume Pretty Derby, which is a Gacha Game that involves a horse-racing concept except with female anime characters combining it with some idol elements, getting similar numbers to Genshin but still a hefty $1 billion in gross in its first year of operating (2021), with $2 billion lifetime mostly collected in Japan. In addition to being a major success, it's interesting in that unlike Dokkan with DBZ, Uma Musume leverages its own IP. This is what Akatsuki did with its own property, Cinderella Nine, to a lesser but still good effect, and is why they are also launching a manga reading app as another avenue to monetise its IPs than just in games.

The Uma Musume anime was somewhat of a cultural phenomenon some years ago, and the Gacha Game leverages otaku culture but also a pretty large horse racing industry in Japan with the anime and the game both published by Cygames' manga arm Cycomics, all part of CyberAgent ( CYAGF ). But the relationship to a pretty niche Japanese industry, as well as a Japanese idol angle which is perplexing and pretty off-putting for Western audiences, despite the phenomenal marketing. Other games have a lot of potential in the West too, which has been a major growth factor for Dokkan.

Akatsuki's Roadmap and Business Proposition

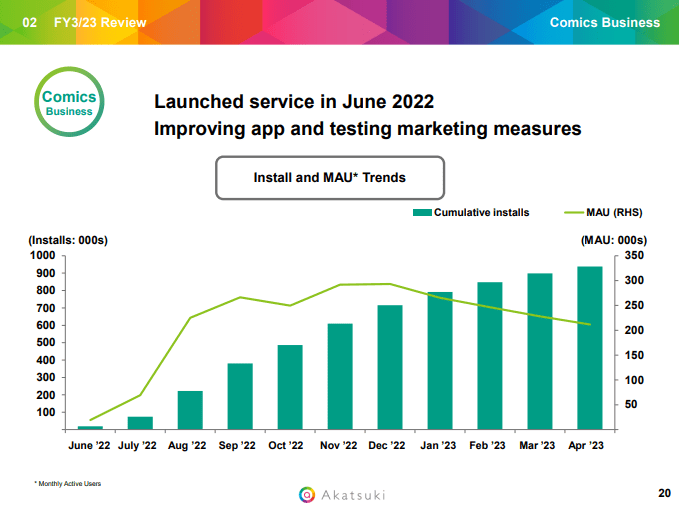

Uma Musume is probably the closest template for Akatsuki's new commercial strategy. Both Cygames and Akatsuki have their own manga arms. Akatsuki's is very new, launched in mid 2022 . Cinderella Nine was Akatsuki's first foray with the anime/manga + Gacha Game strategy, except here Kadokawa ( KDKWF ) published the manga. Now with Akatsuki's own manga arm, they can publish their own manga and incubate new franchises. A lot of the titles offered on the HykeComic app are their own properties, including Demon's Crest which is made by the Author of megahit Sword Art Online . They have a couple of 100ks in MAUs. The model is that periodically comics are readable for free, but for more complete access to binge-read users have to pay for each new chapter of a manga series. Also the manga there are in full color, which is not typical. The business model is still being verified and could be subject to change, but the model is typical for the industry.

HykeComic Engagement (FY 2023 Pres)

{kind=link}

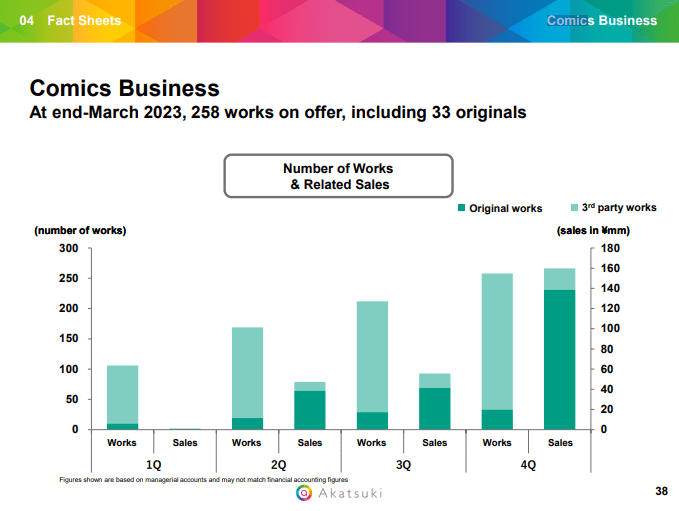

Composition of Manga (FY 2023 Pres)

{kind=link}

Currently, the new comics business is a major loss-maker (segment losses in magnitude of around 20% of Akatsuki profit), but as the concept becomes established and generates scale we should see smaller losses. In fact, and come-down of investment into the HykeComic launch is already visible in the trajectory of results for the segment, which is seeing sequential shrinkage in losses.

Comics Still Unprofitable (FY 2023 Pres)

{kind=link}

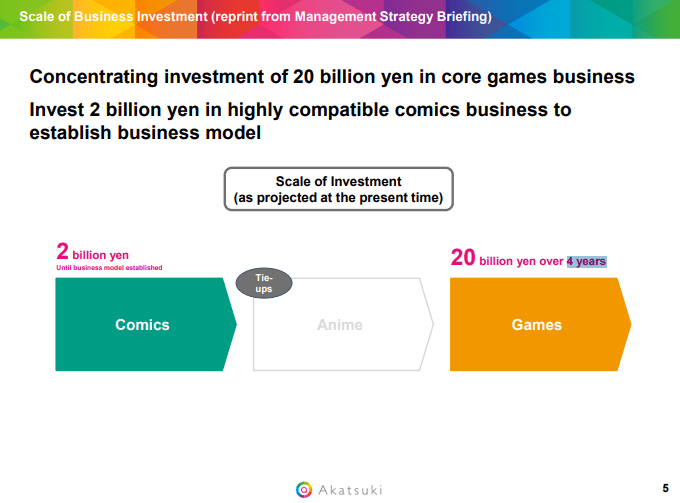

The immediate business roadmap involves spending the 40 billion yen or so in the war-chest over the next few years on games and comics that could have both a domestic and international appeal, just as Dokkan has. Around 20 billion yen is earmarked for games and 2 billion for comic investment over the next four years. Still, 22 billion yen is just a little over half of the total net cash in the company's balances. The investments should yield results and help grow Akatsuki's asset value.

{kind=link}

More concretely, the roadmap sees TRIBE NINE as the new title coming out in the games business likely in the latter half of the coming fiscal year, another title connected to a recent new anime and investment in which is the reason for some of the profit headwinds of around -24% that we are seeing for FY 2023. Akatsuki is taking care of the actual development, and Too Kyo Games are the ones who are responsible for the story elements since they own the IP in this case.

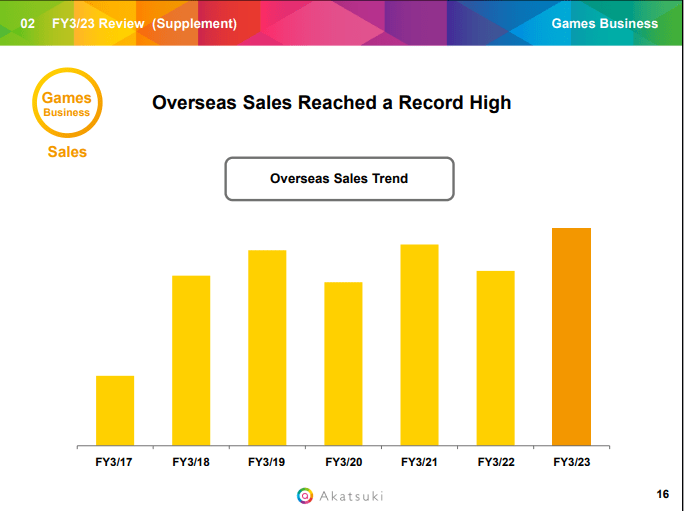

Otherwise, the management plan puts a lot of value on fostering the flagship title of Dokkan Battle, which thanks to the global appeal of the Dragon Ball Z IP and support in lots of languages is growing nicely with the influx of international revenues.

Overseas Driving Games (FY 2023 Pres)

{kind=link}

The 2022 release of Toei's ( TOEAF ) Dragon Ball Super: Super Hero, a DBZ IP movie also helped drive some enthusiasm for the game.

Akatsuki also announced co-development of another title, still no details.

Recent Financials

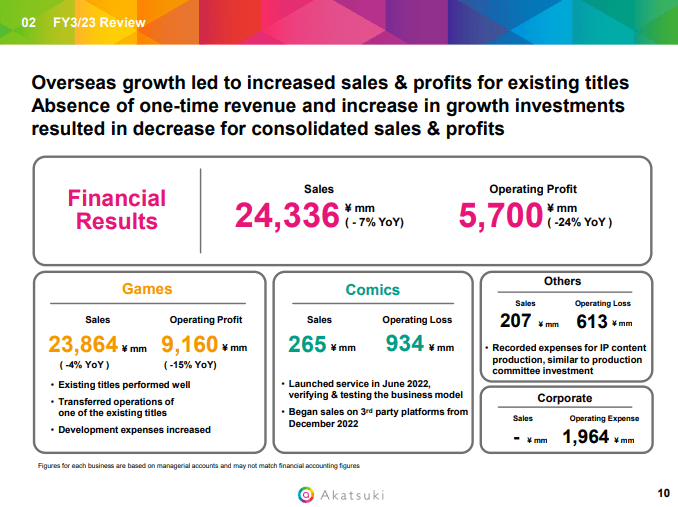

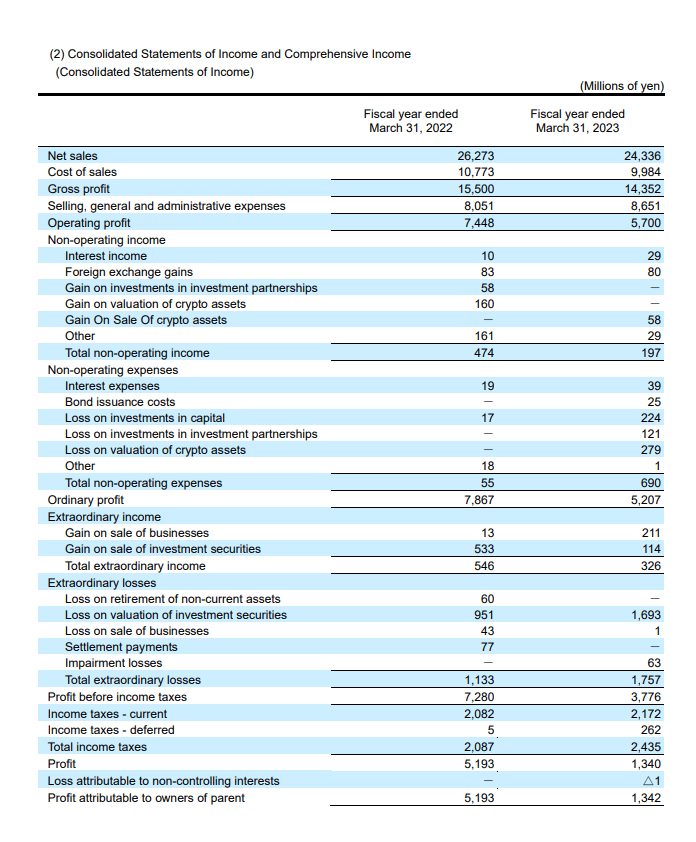

As said, the operating income is down 24% for the FY, and revenues are down 7%. There are a couple of idiosyncratic reasons for that, and the underlying growth in the Dokkan flagship, and considering some elevated expenses around the comic book business launch as well as the ramp up for the TRIBE NINE release, actually indicate general earnings growth and not decline as the baseline case.

Financial Highlights (FY 2023 Pres)

{kind=link}

While the reversal in COVID-19 videogaming has really hurt casual gaming segments, mid-core, which is where Dokkan and lots of its anime-styled Gacha Game competitors lie, is actually pretty resilient. Dokkan, Genshin and others are either keeping their run-rate revenues or growing.

The real hits to the Akatsuki revenues have been from the fact that they ceded control of an app that they developed called UNI'S ON AIR, which is a rhythm game that leverages some known idol groups, but the effects seem to be mainly accounting effects around joint control accounting. But on a more real basis there were associated one-time licensing revenues that didn't get repeated related to UNI'S, and this shortfall explains the revenue decline and comes through in the 'others' segment, which is the segment that used to be Akatsuki's reported IP segment.

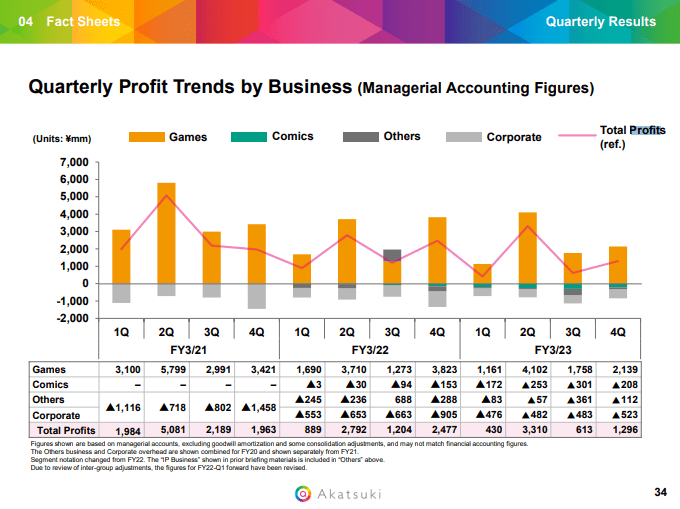

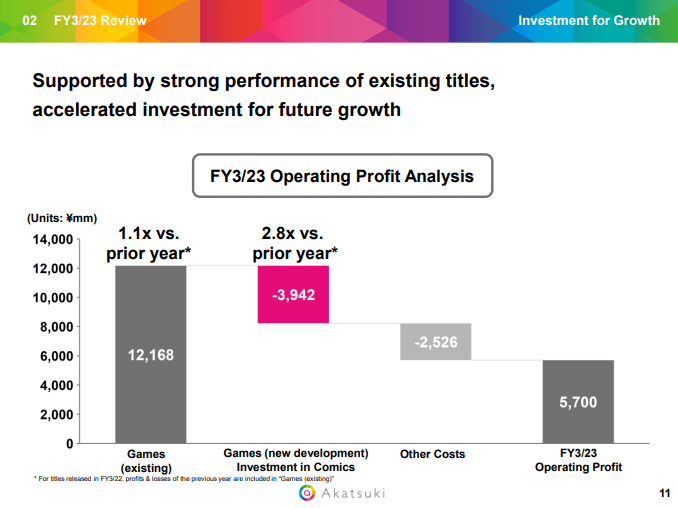

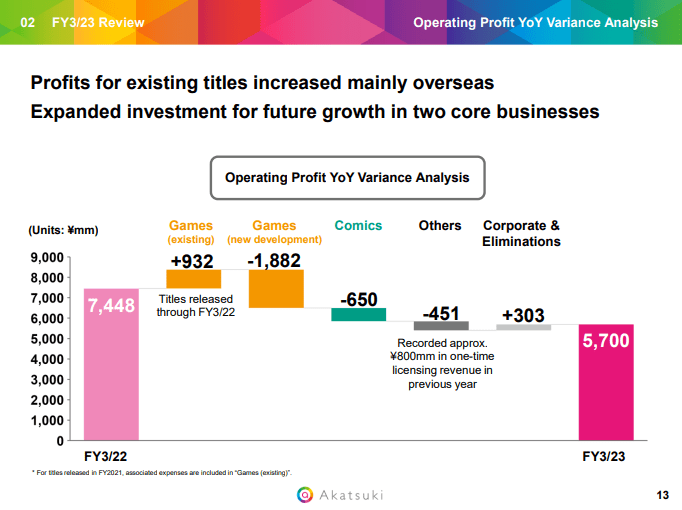

On an expenses and operating profit basis, there's been some increases in headcount and costs associated with the development of new games. Existing games contributed more profit YoY thanks to growth driven by overseas sales for Akatsuki's Gacha Games. However, substantial 3x growth in expensing on new games is the source of the majority of operating profit declines.

Profit growth from existing games (FY 2023 Pres)

{kind=link}

Otherwise, the other profit detractor was the ongoing losses in the comics segment as it ramped up in the current fiscal year. But sequential losses have come down for the comics segment and spells less negative contribution in the coming FY.

Developing new games bringing down profits (FY 2023 Pres)

{kind=link}

On the very bottom line, there were some capital losses in their cash balances due to some ill-fated crypto investments but mostly general equity market declines that hit them this year. This actually mattered a lot, and account for around a 1.6 billion yen differential in profits in addition to the declines in operating profit. The fact that these won't repeat in the coming fiscal year, which has been excellent year so far for Japanese equity markets, will be really important to restore net profits to a normalized level. With new launches this year as well there is a fair chance that we see run-rate profits grow before the FY is out.

IS - showing non-operating hits (FY 2023 Report)

{kind=link}

Valuation

As far as the business is going, they are going to release TRIBE NINE soon, as well as another TBD title, and the existing franchises are seeing growth thanks primarily to overseas revenues. On top of that, the new comics initiative is scaling, monthly active user figures look alright, and the losses should be contracting as expected expenses reduce to about 500 million yen per year, where losses are for the moment 900 million. In all, underlying growth is continuing, it's just that cost ramp-ups are happening ahead of some pretty important launches for the company, including of their entire comics segment.

The fact that this is not a declining company is important firstly because we don't want to be valuing tenor of declines, but also because now we have to build the valuation with suitable comps. We already know that Akatsuki is extremely undervalued due to the 40 billion+ yen in non operating assets that they have that bring their EV into deeply negative territory - so the multiple we apply to Akatsuki doesn't matter than much.

However, we think that in terms of peers and comps, there is no major reason to not compare them to other major casual and mid-core gaming companies, especially with the longstanding popularity of Dokkan. Chosen peers have substantial mobile gaming exposures, where NetEase ( NTES ) has RPG mobile exposures and NEXON ( NEXOF ) has some pretty prominent games such as Maplestory, as well as a relevant mobile gaming presence with Blue Archive. The following is our valuation of Akatsuki.

Akatsuki Valuation (VTS)

Risks and Conclusions

The potential upside is massive, and there's nothing untoward about Akatsuki that would disqualify it from having a multiple that stands up to peers. Even assuming a 0 EV would be appropriate for the company (obviously it isn't), there'd still be almost a 100% upside from the current price.

The only reason why markets might not rate this sector highly, and leave opportunities like Akatsuki undiscovered, may be the rising competition in the Gacha Game space. There are new entrants, and companies across the industry, even Western gaming companies, are beginning to try some Gacha Game monetization schemes. To the extent that East and Western audiences aren't being competed for, there is still competition within the Asian markets, since the anime world is already competitive which can make original IPs to connect to a game difficult to develop, and without a compelling IP a game would be unable to penetrate a pretty saturated market.

However, game development is capitally intensive. If it weren't for the LiveOps and recurring nature of Gacha Game economics, it would be extremely visible as it is for companies like CD Projekt ( OTGLF ) which has very lumpy economics because of the massive outlays for game development that don't see returns for years. There are barriers to new entrant companies for this reason, even if incumbents are able to saturate the market.

However, even if the market is saturated, the pricing power and the fact that there isn't really much price-based competition since these games are ultimately non-commodity products (a long-time Genshin player will have no interest in beginning investing in another Gacha) mean the economics remain superb for these companies, with operating margins easily in the high 30% area when they have titles running and mainly have LiveOps costs, rather than new development costs.

The industry is growing, the margins are stable and can be grown if the IPs are powerful enough. Gacha Gaming is much like gambling - this is an industry you'd want to be in, hence the private equity interest in Playtika ( PLTK ) which is more casino oriented and more familiar to PE investors, but very much in the same universe as other Gacha Games. There isn't any noticeable sign that competition is beginning to erode the economics in a permanent way, although the occasional blockbuster like Genshin can eat away at the opportunities of others.

As far as Akatsuki is concerned, to the extent that the market is competitive, they are going to be relatively insulated since DBZ is an internationally beloved IP and Dokkan is a cash cow game that has proven its resilience for almost a decade now. They have one of the most reliable titles in the Gacha space. Their IP strategy isn't assured to work, but the strategy of developing a manga platform and incubating new IPs that could potentially become relevant is sensible, and as a company with game development expertise they will continue to find engagements with other IPs looking to make a connected Gacha game, like TRIBE NINE most recently and the other new mystery project.

The valuation effects on securities that have hurt the very bottom line are not repeat effects, especially considering the monster year for Japanese equities, and they are definitely in the investment stage of their various new projects, where profits trough. In that respect, they are a bottom-of-the-cycle buy since profits are much more likely to go up than down with TRIBE NINE about to release and the comics segment only a year old and not at critical mass yet in terms of offered content. Their industry is growing overall, and as a subset of videogaming it has some of the best economics possible due to the gambling angle. With Akatsuki, you are paid to get these exposures since the EV is negative - an entirely no-brain valuation that cannot be explained by some terminal concerns around the industry at all.

Foreign money is pouring into Japan now, so the possibility of price discovery in the mid-cap space is higher than it's been in decades, especially as the TSE pushes corporate governance reforms. Akatsuki is already shareholder friendly, too, so while you wait for catalysts, at least of earnings growth or eventually of price discovery by sophisticated buyers, you get paid to wait with a 3.8% dividend yield. Negative EV in a growing industry with top tier economics makes Akatsuki a high conviction, no-brainer buy.

For further details see:

Akatsuki: Negative EV At Odds With Dominant Gacha Game Titles, Growth Prospects