ETNB - Akero Therapeutics: Contrarian Buy Opportunity As Stock Tanks On 'NASH Dash' Data

2023-10-10 13:28:32 ET

Summary

- Akero Therapeutics' share price is tanking after biotech's NASH drug fails to meet its primary endpoint in a Phase 2B study.

- Despite the setback, AKRO stock is still trading higher than it was in September 2022, before another Phase 2 study succeeded in earlier stage fibrosis.

- Akero may have set its primary endpoint bar too high in this latest study, and results could still improve at 96 weeks.

- Despite the fail, Akero is still in possession of some arguably "best-in-class" NASH data and there is substantial funding for a pivotal study program.

- Acknowledging the substantial risks, that would likely put anyone but a contrarian trader off of buying Akero stock, but I wonder if today's selloff is an overreaction.

Investment Overview

Forget the "NASH Dash" - the race to be the first biotech or pharma company to secure a drug approval in the indication of nonalcoholic steatohepatitis - Akero Therapeutics, Inc. ( AKRO ) - once considered a frontrunner in this race - is experiencing a "NASH Crash" in trading today.

At the time of writing, Akero's share price has lost >65% of its value in the opening hour of trading, after the market interpreted what Akero has called "encouraging 36 week analysis" from its 96 week Phase 2B SYMMETRY study of lead candidate Efruxifermin ("EFX") in patients with NASH, much more negatively than the biotech itself.

SYMMETRY is a Phase 2b study of 182 patients with cirrhotic NASH, otherwise known as stage 4 NASH - the latest stage, most severe form of the damaging liver disease. The primary endpoint of the study was defined by Akero as:

The proportion of subjects who achieve ? 1 stage improvement in fibrosis with no worsening of NASH at week 36.

The headline news - at least as far as the market is concerned - is that the study missed its primary endpoint, failing to show a statistically significant difference between either the high dose, 50mg, or low dose, 25mg arms and placebo. The data showed that, according to an Akero press release:

22% (28mg EFX) and 24% (50mg EFX) of patients experienced at least a one-stage improvement in liver fibrosis with no worsening of NASH by week 36, compared to 14% for placebo

SYMMETRY Study Fail Wipes Out Years' Worth Of Excellent Progress

Despite today's selloff, Akero stock is still trading at a higher value today than it did in September 2022, when the market held out little hope that the San Francisco-headquartered biotech could succeed in NASH with EFX.

EFX is described, in Akero's latest quarterly report , as:

an analog of fibroblast growth factor 21 ("FGF21") which is an endogenously expressed hormone that protects against cellular stress and regulates metabolism of lipids, carbohydrates and proteins throughout the body.

It is the same mechanism of action as 89bio, Inc.'s ( ETNB ) Pegozafermin, and neither of these relatively small companies looked likely to succeed in an indication as challenging as NASH - in which no drug has ever been approved within or outside the U.S., despite scores of attempts by biotechs and Pharmas attracted by a ~17m patient population (expected to rise to ~27m by 2030), and a double-digit billion market opportunity.

That is, until Akero shared data from its Phase 2b HARMONY study of EFX in patients with pre-cirrhotic nonalcoholic steatohepatitis ((NASH)), fibrosis stage 2 or 3 (F2-F3) in September last year. As per Seeking Alpha :

The study met its primary goal for both the 50mg and 28mg EFX dose groups, with 41% and 39% of EFX-treated patients, respectively, seeing at least a one-stage improvement in liver fibrosis with no worsening of NASH by week 24, compared with 20% for the placebo group.

The study also met a key secondary goal with 76% of patients treated with 50mg and 47% of those on 28mg, achieving NASH resolution without worsening of fibrosis, compared to 15% for placebo, the company noted .

Akero added that 41% of patients on 50mg and 29% on 28mg, achieved both goals (NASH resolution and fibrosis improvement ?1 stage), compared to 5% on placebo.

As I commented in a note on 89bio for Seeking Alpha in October last year, when discussing these results:

Given that the FDA's approval criteria for a NASH drug is improvement of ?1 stage in fibrosis with no worsening of NASH, or improvement in NASH resolution with no worsening of fibrosis, hopes are high that Akero could wind up winning the "NASH Dash," the race to be the first drug approved to treat the disease

After Akero shared the HARMONY data, its stock price took flight, jumping from ~$11 per share, to an all-time high of $54 by the end of December 2022 - a gain of nearly 400%.

Digging Into The SYMMETRY Data - Are There Any Reasons For Optimism?

Although it missed the primary endpoint, the SYMMETRY study did meet several secondary endpoints - as per Akero's press release:

Statistically significant rates of NASH resolution in 63% and 60% of patients at week 36 were observed for the 28mg and 50mg EFX-treated groups, respectively, compared with 26% for placebo, representing the highest response rates reported to date for NASH resolution in this patient population. Statistically significant improvements were also observed for both EFX groups in non-invasive markers of liver injury and fibrosis, insulin sensitization and lipoproteins.

Stephen Harrison, M.D., the SYMMETRY study's principal investigator also stressed that these were "the strongest data set reported to date in a placebo-controlled trial in the difficult-to-treat population of patients with cirrhosis due to NASH," adding that he was:

encouraged that statistically significant improvements on multiple measures of NASH pathogenesis were observed in EFX-treated patients. EFX shows promise for stabilizing and improving liver health for patients with cirrhosis.

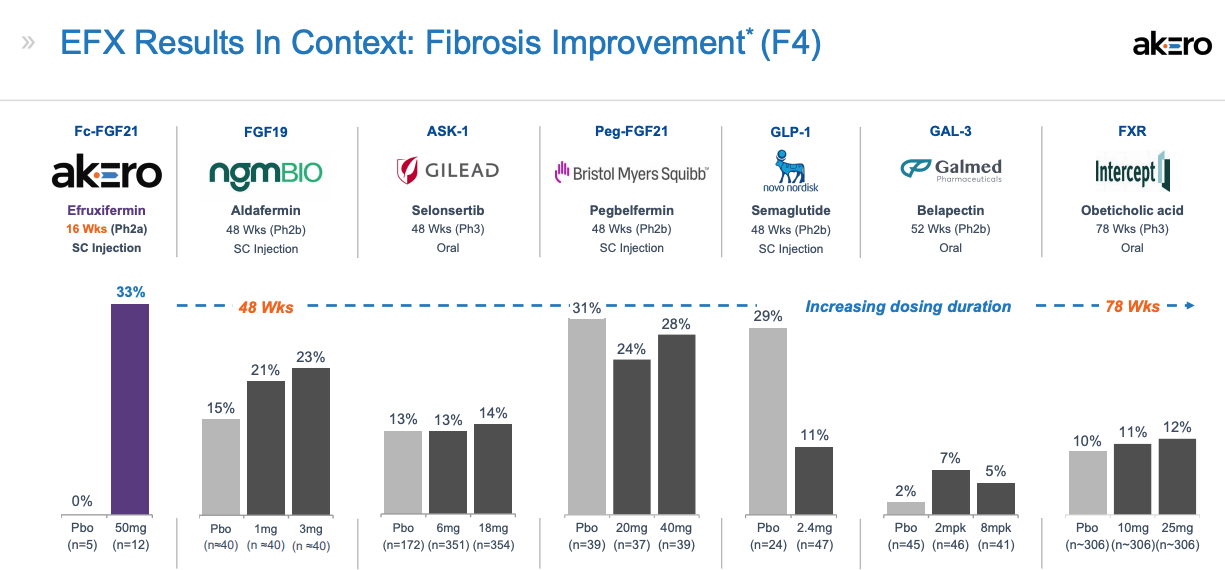

Akero had been confident in the success of SYMMETRY based on encouraging 16-week data in patients with stage 4 Fibrosis from cohorts in its other studies - HARMONY and the Phase 2a BALANCED study - which showed 33% of patients experiencing fibrosis - potentially best-in-class data when compared across a selection of "NASH Dash" challengers, as per a slide shared in a recent Akero presentation.

Akero best in class fibrosis improvement (Akero presentation)

{kind=link}

As recently as late September, the investment bank Cantor Fitzgerald initiated coverage of Akero with a "BUY" rating, suggesting that EFX had "stronger efficacy than competitors across several relevant endpoints," giving the SYMMETRY study a 60% chance of success, and setting a peak sales target of $10bn for the drug, with $2bn in stage F4 in the U.S. alone.

In short, the market had placed a significant amount of faith in Akero, but, based on a single missed endpoint, now seems to be dumping stock as fast as it can. Akero management has suggested that it may have set a "high bar" when selecting statistical significance at just 36 weeks as its primary endpoint.

Akero remains committed to initiating a Phase 3 study of EFX, and it has plenty of cash available to do so, having raised $335m in net proceeds last quarter, according to an earnings press release . Cash position as of Q2 2023 stood at $639m, while net loss for the quarter was $32m.

The company had apparently been waiting for the SYMMETRY results to arrive before planning the design of its 3 Phase 3 studies, SYNCHRONY HISTOLOGY, SYNCHRONY REAL WORLD, and SYNCHRONY OUTCOMES.

SYNCHRONY Phase 3 programs overview (corporate presentation)

{kind=link}

The missed SYMMETRY primary endpoint must have significantly muddied the waters for the company however - does management abandon the stage 4 cirrhosis approval shot, and aim for F2-F3 NASH, where it has already obtained data apparently strong enough for approval? Or would the FDA refuse to approve a subcutaneously administered drug in this earlier stage indication, arguing that patients would be better served by lifestyle changes, or other drugs?

A Quick Look At The Competition - Does Rise Of GLP-1 Agonists Mean "NASH Dash" Has Lost Relevance?

Shortly after Akero's stock skyrocketed in September last year, a rival NASH drug developer - Madrigal Pharmaceuticals ( MDGL ) - saw its stock pop even higher after announcing positive Phase 3 data for its NASH targeting drug Resmetirom. The study involved >1,000 patients with liver biopsy confirmed NASH, and according to Madrigal's latest quarterly report:

The dual primary surrogate endpoints on biopsy are NASH resolution with ?2-point reduction in NAS (NAFLD Activity Score), and with no worsening of fibrosis OR a 1-point decrease in fibrosis with no worsening of NAS. Resmetirom achieved both primary endpoints with both daily oral doses, 80 mg and 100 mg, relative to placebo

Madrigal's stock price jumped from $63, to $290 overnight. Madrigal has now completed its rolling submission of a New Drug Application, although its share price has fallen >50% year-to-date, to $145 per share, and until Akero's selloff today, the two companies had enjoyed a similar value market cap - Madrigal's currently stands at $2.8bn, while Akero's has sunk from $2.7bn, to ~$760m in trading today.

It seems that Madrigal's pivotal study may suffer from a similar issue to Akero's successful HARMONY study in that most patients were suffering from stage 3 fibrosis or below, whereas the FDA is apparently looking to approve a drug that can address stage 4 cirrhosis, and in the former indication, Akero appears to be confident that its own data is superior, as we can see in the slide below.

Akero - best in class in pre-cirrhotic NASH (corporate presentation)

{kind=link}

It's worth noting that, after its Ocaliva lead candidate was firmly rejected by the FDA for approval in NASH in June, Intercept ( ICPT ) opted to sell its business to Italian Pharma alfasigma rather than make another attempt to obtain market approval in this extremely lucrative, but apparently doomed indication. Meanwhile, 89bio stock is also tanking today, given that its lead drug, Pegozafermin, has the same MoA as EFX.

The asset to pay closest attention to in the above table is Novo Nordisk's ( NVO ) GLP-1 agonist, incretin mimetic Semaglutide. The drug that "makes you feel full", and is already marketed as Wegovy, to treat obesity, and as Ozempic, to treat diabetes, is arguably now the runaway leader of the "Nash Dash," alongside Eli Lilly's ( LLY ) tirzepatide, approved as Mounjaro in diabetes and soon to be approved in weight loss.

These 2 drugs are amongst the most hyped in history, with peak sales expectations between them in excess of $100bn. Their unique characteristics - the ability to help people lose weight with minimal side effects - make them strong candidates to gain approvals in NASH also. Although treating cirrhosis may be beyond them, preventing it occurring in the first place is where their strengths lie.

Akero adapted its BALANCED study to include a cohort using both EFX and semaglutide, stating that results showed "significantly greater reduction in liver fat for EFX combined with GLP-1 than GLP-1 alone. Perhaps Akero could respond to the new reality in NASH by pivoting towards gaining an approval for EFX as an adjunctive therapy for be used alongside semaglutide / tirzepatide?

Concluding Thoughts - Reaction To Akero Data Understandable: Could It Make AKRO A Contrarian Buy Opportunity?

Before yesterday's study failure, any discerning biotech investor ought to have considered buying Akero stock as a substantially risky opportunity, but has today's sell-off made the stock attractive at an almost 70% overnight discount?

It does seem possible that Akero can use its significant financial resources to continue the SYMMETRY study and perhaps hope that after 52-weeks, patients' conditions are improving and the gap between the high and low dose treatment arms and the placebo arm is sufficiently wide for the study to be considered a success.

Even if that does not happen, Akero seems to have achieved some undeniably strong results in earlier stage fibrosis, so perhaps a Phase 3 study could be designed to cater for that patient population - after all, that seems to be what Madrigal has done. Akero even has data suggesting EFX could work in tandem with semaglutide - likely to become one of the world's all-time best-selling drugs (sales last year of Wegovy and Ozempic exceeded $8bn).

All three of these opportunities might imply that Akero as a company deserves a valuation of >$1bn, whilst any form of approval in NASH would likely send the company valuation >$2.5bn, given peak revenues would surely exceed $500m (I apply a rule of thumb that commercial stage biotechs trade ~5x sales) even if the approval was limited.

Akero does have a significant problem in that it has no other drugs of note, so if EFX proves to be a busted flush - as so many other drugs targeting NASH have proved to be - the company becomes essentially valueless, apart from its cash reserves. Unlike e.g. Intercept, bought out for ~$800m based on a prior approval of Ocaliva in Primary Biliary Cholangitis ("PBC"), and revenues >$100m per annum, EFX is not a revenue generating asset

Even so, whilst acknowledging the substantial risk involved in making any investment into Akero, my conclusion would be that after today's selloff, I would sooner buy the company's stock than short it, because I don't think Akero's race is run yet, and listed biotechs developing NASH drugs are characterized by wild share price swings, therefore it would not surprise me if investors changed their minds about the potential of EFX a couple more times before the biotech's race is run.

There is a very real threat that Akero's management team - who have apparently been involved in >20 FDA drug approvals - kick EFX to the sidelines and dissolve the company if they face further setbacks, however, meaning investors buying today still have a great deal of downside risk. Arguably, however, Akero, with its "best in class" NASH data - even in relation to its SYMMETRY cirrhosis study - has a few more major share price peaks and troughs to experience before its race is run.

For further details see:

Akero Therapeutics: Contrarian Buy Opportunity As Stock Tanks On 'NASH Dash' Data