CA - Alamos Gold: Already Priced For A Bright Future

2024-01-09 07:23:13 ET

Summary

- Alamos Gold is a sound company with no debt and positive cash flows.

- It's making continual improvements to its existing mines and has other properties to explore and develop.

- Despite this, the optimism is already priced into the shares, meaning it's not a bargain anymore.

Alamos Gold (AGI) is a North American gold miner whose primary assets are in Canada and Mexico, with some exploration assets that may yield good results in the future. After a series of M&A activity over the past decade and improving the underlying assets of the prior entities, Alamos has transformed into an entity that is finally producing positive cash flows.

With the share appreciation that has occurred over the past year, some may wonder if the stock still trades at a discount. Having looked at Alamos, I think we have a good company, but one that leans toward overvaluation. As such, I will make the case for why it is a SELL.

Brief History

Alamos amalgamated with AuRico Gold in 2015 and Richmont Mines in 2018. In 2023, it acquired Manitou. The resulting entity, Alamos Gold Inc., has the combined mining and exploration assets of the previous companies and their subsidiaries. From there, the company has been developing its new operation.

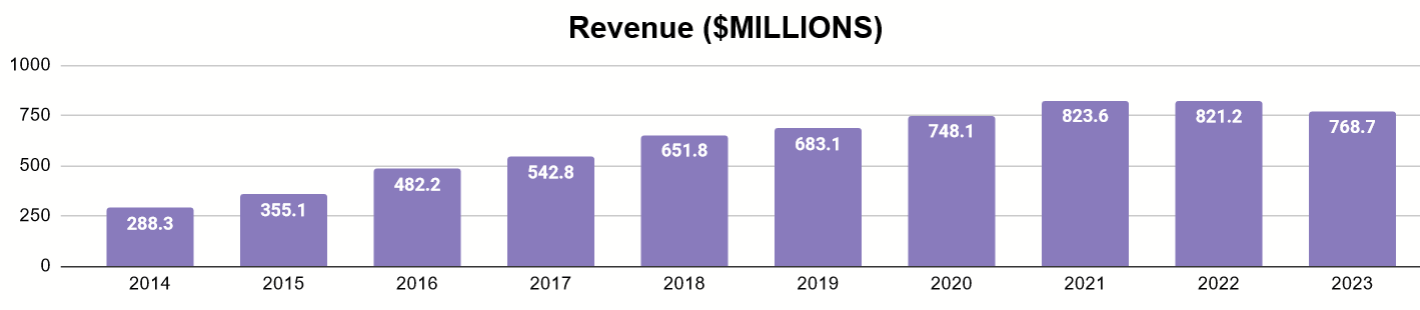

I'll show financial data from the last decade that should illustrate the evolution of the company, and I'll include YTD data for 2023.

{kind=link}

As we can see here, the mergers and natural development of the mining assets led to steady rise of revenues to the present.

{kind=link}

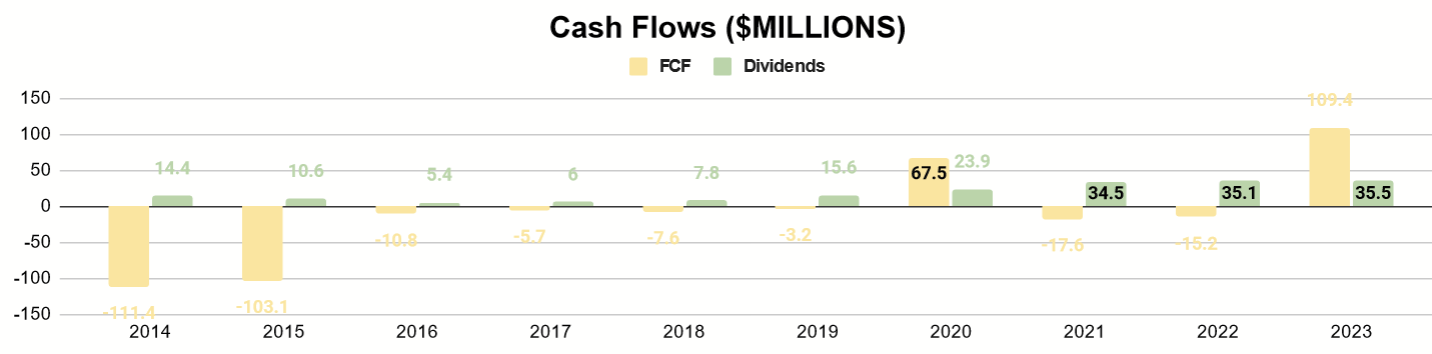

The cash flow history sheds a bit more light. We can see free cash flow was heavily negative at the start of this period. The mergers allowed for some stabilization. Dividend payments continued to be paid, even though free cash flow did not sustain it for a long stretch there.

{kind=link}

Yet, we can see that they had a large cash balance that made such possible and allowed them to get through the period. What kind of company exists now?

Mining Operations

Alamos has three principal assets producing gold for them: Young-Davidson, Island Gold, and the Mulatos District.

Young-Davidson

Young-Davidson is located in Northern Ontario and has been in production since 2013. This mine typically produces around 190K oz of gold per year. In their 2022 annual report , the company reported on-site FCF of $101m. In their Q3 2023 MD&A , they reported $83m in on-site FCF. Additionally, they determined a 15-year mineral reserve life for the mine, meaning it produces cash and has a decent runway of time to continue doing so.

{kind=link}

Island Gold

Island Gold (also in Ontario) has been operating since 2007. It produces around 130K oz per year. The company reported negative $9m in 2022 and further outflow of $34m YTD 2023 for mine-site FCF at Island Gold. The vast majority of the mine-site capex, however, has been for growth, part of the Phase 3+ project on the site. The acquisition of Manitou added new properties in close proximity to this site, adding even more growth potential.

{kind=link}

Mulatos District

This asset consists of the Mulatos mine (operational since 2006) and La Yaqui Grande mine in Mexico. Since La Yaqui Grande is new, the product for the district has been growing fast. Q3 2023 MD&A reported YTD production of a 164.7K oz and mine-site FCF of $114.7m, with capex being very low. Mineral reserve life, however, is reported as five years, but many unexplored reserves exist on both properties that could extend this.

Other Assets

The mine also has exploration assets that have yet to produce gold. They include Lynn Lake, Quartz Mountain, and Turkish assets.

Lynn Lake is in northern Manitoba. The company reports proven and probable reserves at 2.3m oz, with feasibility studies suggesting annual production of 176K oz.

Quartz Mountain is located in Oregon. Much of this asset is still prospective, with 339K proven and probable oz so far.

Turkish assets , naturally, are located in Turkey. About 339K oz are proven and probably so far, but currently the company has been struggling to renew its licenses with the Turkish government, putting this asset into a state of hiatus.

Balance Sheet

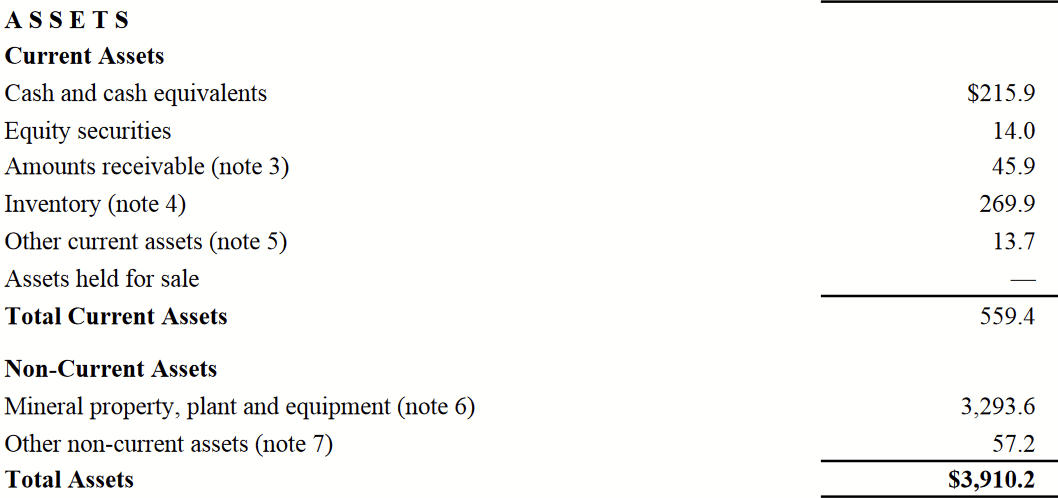

The company shows a strong balance sheet, with $215.9m in cash as of Q3 2023 .

{kind=link}

Total assets are reported at $3.9b, but given the mystery around some of their more exploratory or prospective assets, we ought to treat this as a soft number.

{kind=link}

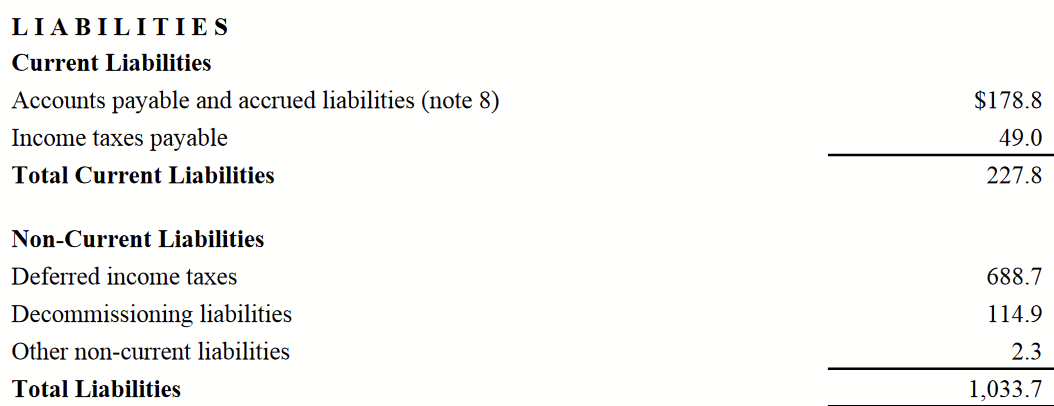

Yet, the good news is that company does not currently have any debt. With positive cash flows, it can finance its own operations and growth.

A Look to the Future

While the company has steadily put itself together over the past decade through its M&A, there are many opportunities for growth and continued production.

Life of Mineral Reserves

For both Young-Davidson and Island Gold, the lives of the reserves are well over a decade with current developments. Mulatos is more concerning with its five-year horizon. Overall, though, this suggest that company-wide levels of cash flow are durable for the foreseeable future.

Phase 3+ Project

The company believes that the Phase 3+ Project, a series of improvements at Island Gold, will increase annual production to 287K oz by 2026, almost doubling current levels at the mine. With recent gold prices, this would add over $300m in annual revenues to the company and reduce growth capex once completed.

{kind=link}

I believe this is the most likely source of major cash flow growth for the company for the foreseeable future.

Turkey

With these assets being outside of NAFTA rules and relations, along with unpredictable nature of Turkish politics since Erdo?an became President it's not clear when the company's licenses will be restored, if ever. The company has been taking legal action against the government, and so I believe assets here can't practically be considered for valuation.

Exploration Assets

Lynn Lake, Quartz Mountain, and adjacent properties to the active sites are areas that maybe explored for much longer but could still engage in productive sometime within the next decade. I believe that one's closer to active mines are more likely to be developed due to their convenience.

{kind=link}

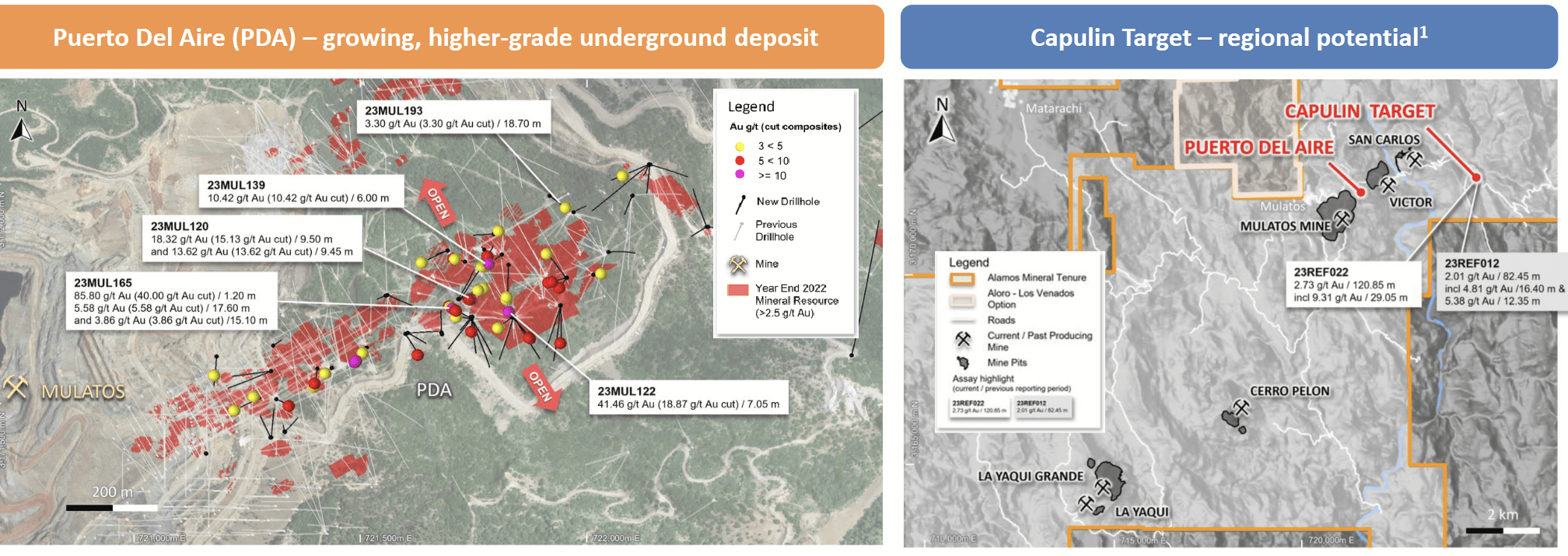

The Puerto Del Aire ((PDA)) and Capulin Targets are both in the Mulatos district and are currently being explored. PDA studies currently indicate over a million oz deposited there.

Valuation

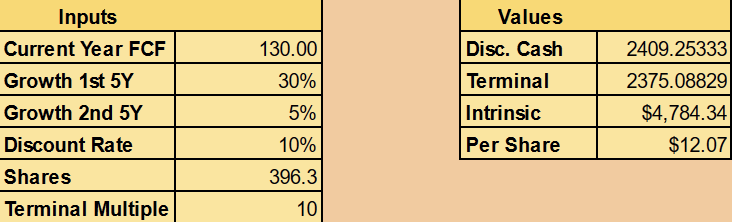

While it will be a developing situation, there is enough information to do a valuation. Using Discounted Cash Flow, we'll make these assumptions:

- Baseline FCF of $130m

- 30% annual growth the first five years

- 5% annual growth the second five years

- Terminal multiple of 10

I believe $130m annually is reasonable, given the reported YTD for 2023 is $109m. 30% as the average annual growth of FCF also makes sense with the jump that will occur starting in 2026. 5% growth for the five years to follow that is to allow for incremental improvements across the company, while lacking obvious sources of major growth. A terminal multiple of 10 allows for exploration assets' more distant value and appreciation by the market to be reflected.

{kind=link}

With this, at a 10% discount rate, a fair value of $12.07 per share. Net cash per share also comes to about $0.73. With that said and at current prices, AGI is leaning toward overvaluation.

There are some things that necessarily blur a valuation for a miner. Fluctuations in the price of gold and higher-quality grades mined than expected could favorably improve financial results beyond what I said. Similarly, some of the exploration assets could materialize into product much sooner. These things could make the shares still somewhat undervalued. Yet, I believe a long-term investor will benefit from entering a position when given a reasonable discount and based on more cautious assumptions. The current price seems to reflect a more optimistic future, one that may not occur.

Moreover, the dividend is currently less than a percent. Even if it could double as revenues increase and capex declines, that's still a low yield on cost, and dividends are typically where we expect to see returns with miners. These things make the share not very good to hold if we want to wait for a higher share price before exiting.

Conclusion

Alamos Gold is a sound company that's assembled itself well after numerous instances of M&A over the past decade. The mines have been able to support each other with their positive cash flows for reinvestment in the business. Going forward, investors will really want to watch the execution of the Phrase 3+ Project and the developments at Mulatos.

Without debt and plenty of assets to explore for the future, I expect this company to continue chugging along for years to come. Yet, investors make money by entering a position with a discount. Current prices suggest more of a premium, and the dividend yield being low doesn't make AGI a great candidate for Hold. With miners being capital-intensive and risky, we want prices that suggest a more pessimistic future that can be proved wrong later on, as opposed to the other way around. For these reasons, I consider the shares to be a SELL for now.

For further details see:

Alamos Gold: Already Priced For A Bright Future