CA - Alamos Gold: Another Beat On Annual Guidance

2024-01-19 14:28:37 ET

Summary

- Alamos released its Q4 and FY2022 results last week, reporting record annual production of ~529,000 ounces, a 6% beat vs. guidance.

- Meanwhile, the company expects to maintain industry-leading costs next year despite the strength in the MXN/USD, with further margin expansion post-2024.

- In this update we'll dig into the Q4 results, the company's updated outlook, and why Alamos' continues to be one of the sector's best buy-the-dip candidates.

While the S&P-500 ( SPY ) has held onto its Q4 gains, the Gold Miners Index ( GDX ) has given up the bulk of them, down 11% year-to-date in what's typically its best month of the year from a seasonality standpoint. This can be attributed to underwhelming guidance from some companies like Fortuna Silver ( FSM ), mediocre production results from Barrick ( GOLD ), and a ~6% pullback in the gold price from its most recent new all-time high of ~$2,140/oz.

Fortunately, Alamos Gold ( AGI ) was one company with Lundin Gold ( OTCQX:LUGDF ) that bucked the trend, beating its annual guidance and unveiling robust guidance for 2024, with costs expected to be well below the sector average. The company also reported more solid exploration results in H2 from its Mulatos Complex in Mexico, paving a path for significant mine life extension with the high-grade PDA deposit just in time to offset LYG production that is expected to wind down in 2027. In this update we'll dig into the Q4 results, the company's updated outlook, and why Alamos continues to be one of the sector's best buy-the-dip candidates.

{kind=link}

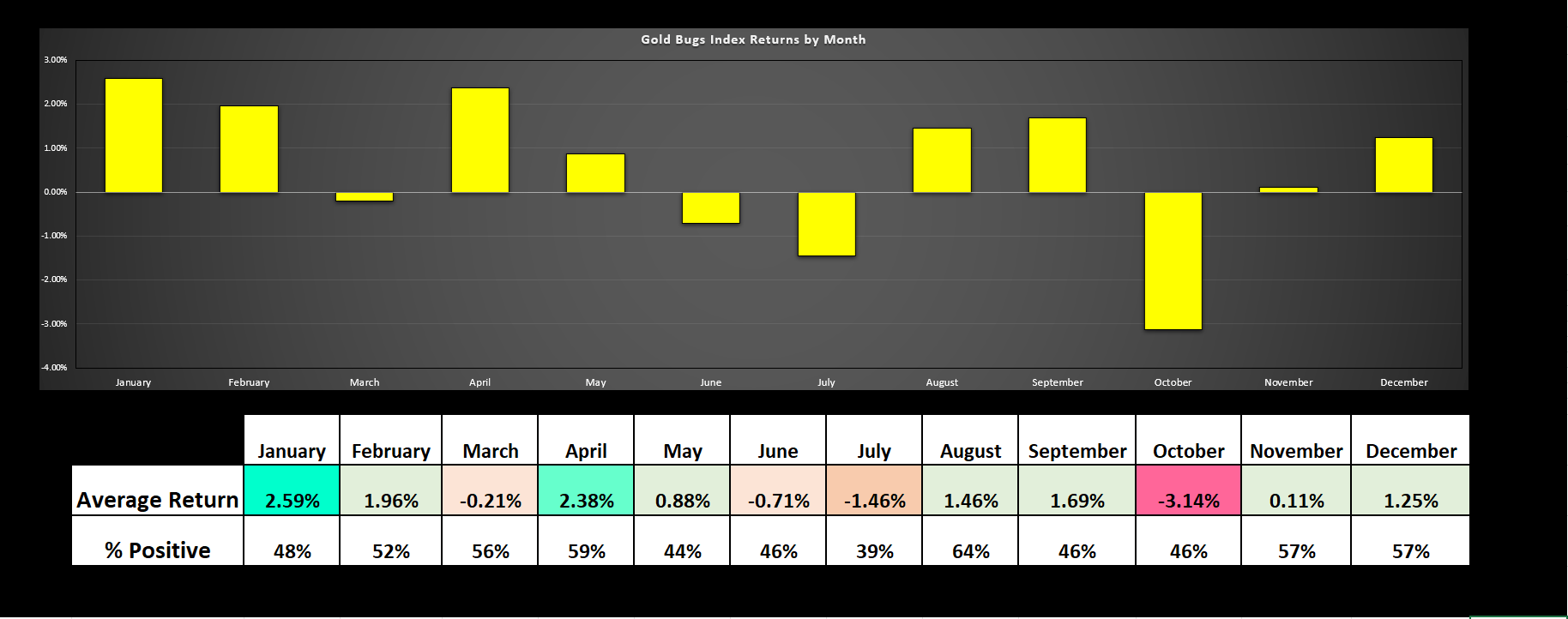

Gold Bugs Index Seasonality - Author's Data & Chart

Q4 and FY2023 Production

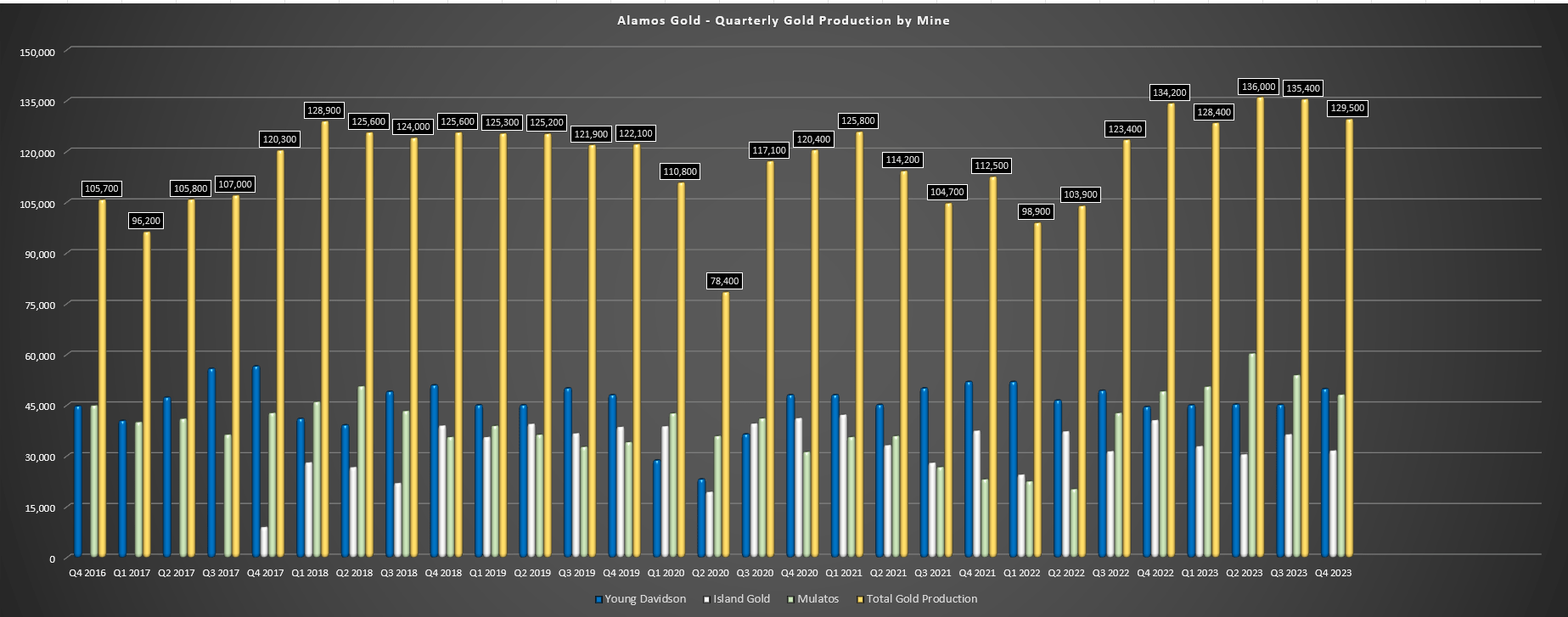

Alamos Gold released its Q4 results last week, reporting quarterly production of ~129,500 ounces of gold, translating to a ~3% decline over the year-ago period. The dip in year-over-year production was largely because of lapping difficult comparisons, with Q4 2022 being a near record quarter, but the annual results were phenomenal with Alamos' gold production hitting a new all-time high of ~529,300 ounces. Notably, this figure was a 6% beat vs. its initial guidance midpoint of 500,000 ounces in FY2023 and translated to 15% growth year-over-year despite a lower grade year at Island Gold with grades below the average reserve grade of ~10.8 grams per tonne of gold. Not surprisingly, this translated to record annual revenue for the company when combined with a higher gold price, with Q4 revenue of ~$255 million and annual revenue of ~$1.0 billion.

{kind=link}

Alamos Gold Quarterly Gold Production - Company Filings, Author's Chart

Digging into the results a little closer, Young-Davidson had a solid Q4 with production of ~49,800 ounces but came in near the low end of guidance at ~185,100 ounces (guidance midpoint: 192,500 ounces). Fortunately, this was more than offset by its Mulatos Complex where production surged to ~48,100 ounces in Q4 and ~212,800 ounces for the year. This figure trounced its FY2023 guidance midpoint of 180,000 ounces with help from much higher grades at La Yaqui Grande. Finally, the company's Island Gold produced ~31,600 ounces of gold in Q2, down year-over-year because of difficult comparisons after lapping elevated grades of 12.1 grams per tonne of gold in the year-ago period. Still, the mine had a solid year with the production of ~131,400 ounces and beating the guidance midpoint of 127,500 ounces by over 3%.

{kind=link}

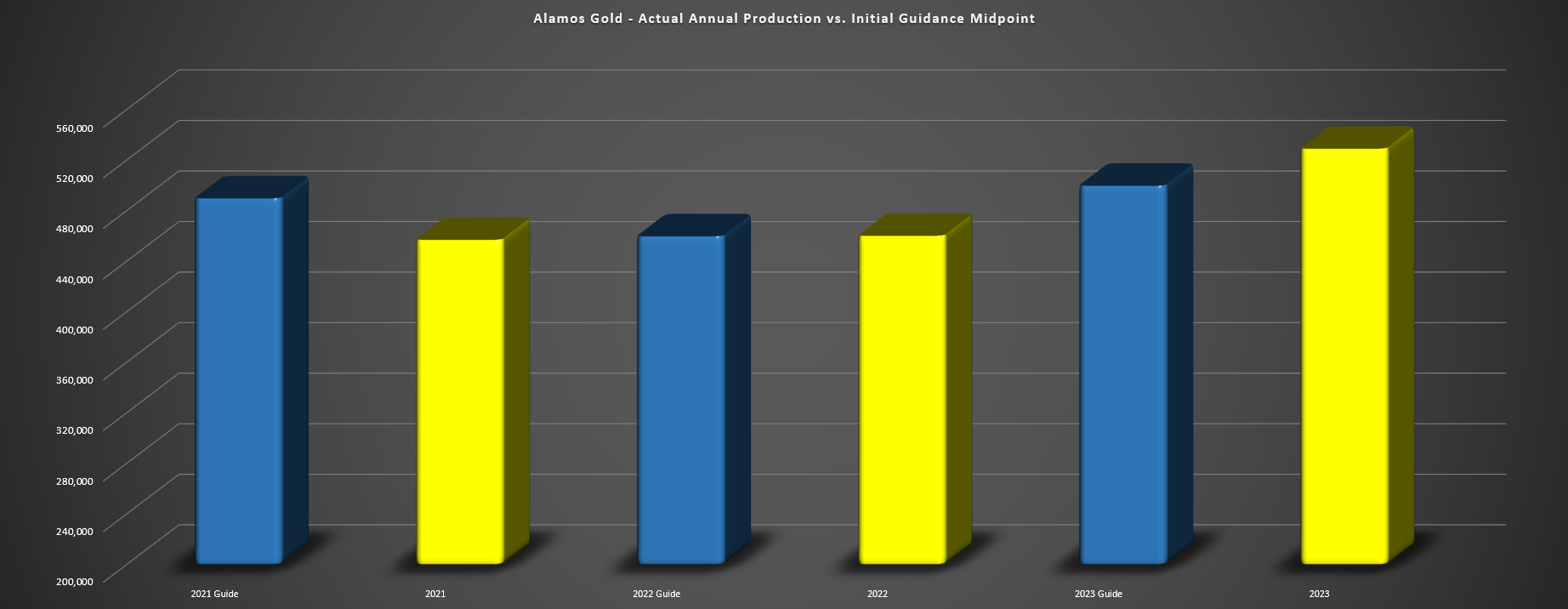

Alamos Gold Actual Annual Production vs. Initial Guidance Midpoint - Company Filings, Author's Chart

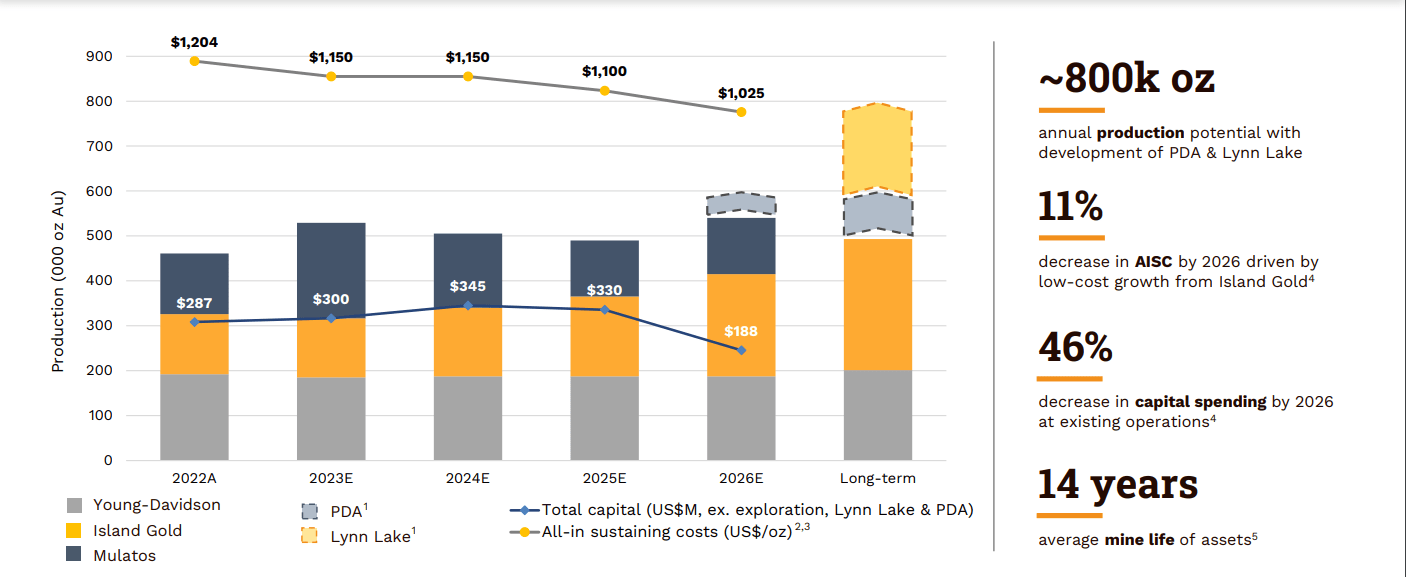

If we look at Alamos' annual production vs. its guidance mid-point we can see that this was the company's second consecutive beat vs. its outlook after a slight beat last year (460,400 ounces vs. 460,000 ounces), but with this year's beat clearly being far more significant (5.9% vs. 0.1%). This has continued Alamos' track record of over-delivering on its promises, and Alamos has been one of the few companies that didn't have to pull its all-in sustaining cost guidance higher even with the impact of a rising Peso. In fact, the company's margin performance is even more impressive given the multi-year breakout in the Peso vs. the US dollar ( UUP ) and with miners calling out rising labor costs in prolific mining jurisdictions (Canada, Australia), and it should see costs drop at least 4% year-over-year when it reports its results vs. $1,204/oz AISC in FY2022.

2024 Outlook

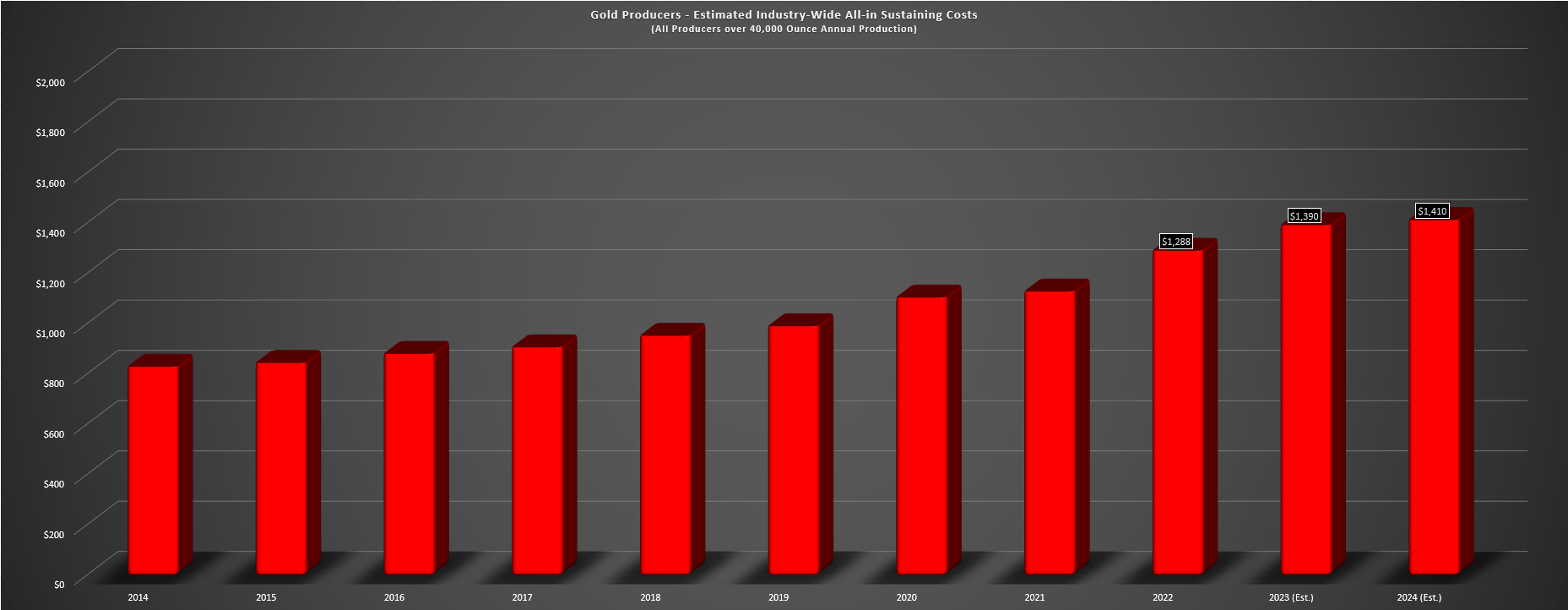

Moving to Alamos' 2024 outlook, the company has increased its full-year production guidance to 505,000 ounces at the mid-point vs. its previous guidance of 490,000 ounces, but costs are expected to be a little higher than previously estimated at $1,150/oz. The increased production vs. the prior outlook can be attributed to residual leaching at Mulatos, but costs have been adjusted to reflect the stronger Peso (17% hedged for 2024), and 4% inflation company-wide with the company noting that the largest driver is labor inflation in Canada. And while this outlook is a minor downgrade from its 2023 results at the midpoint (~505,000 ounces at $1,150/oz vs. ~529,300 ounces at $1,165/oz estimates), it's worth noting that Alamos has historically been conservative with guidance and its costs will still be over 15% below estimated industry average AISC of ~$1,410/oz in FY2024 even if it only meets guidance.

Island Gold, Mulatos, and Young-Davidson are expected to produce ~153,000 ounces, ~188,000 ounces, and ~165,000 ounces in 2024, respectively.

{kind=link}

Gold Producer Universe - Annual AISC & Forward Estimates - Company Filings, Author's Chart & Estimates

Although Alamos has taken a hit with the rest of the sector since releasing its results and updated FY2024 guidance, it's also important to note that its outlook gets much stronger as we look further ahead, with the potential for ~500,000 ounces at ~$1,100/oz AISC in 2025 and ~540,000 ounces at $1,025/oz AISC in 2026. This can be attributed to the ramp-up of Island Gold P3+ in 2026, and does not include potential upside from PDA that could push Mulatos Complex production north of ~140,000 ounces. And looking out to 2029 with the potential for peak production years from Lynn Lake (new study underway) and full production from P3+ combined with PDA (~100,000 ounces per annum), we could see production increase to ~800,000 ounces with peak production, translating to over 50% production growth from current levels.

{kind=link}

Alamos Gold Annual Production & Forward Outlook/Long-Term Potential - Company Website

The 800,000 ounce assumption in 2029 assumes no additional open-pit production and only 100,000 to 110,000 ounces from the Mulatos Complex at PDA based on 2,000 tonnes per day at 5.2 grams per tonne of gold and 85% recoveries.

The most exciting part about this forward outlook for Alamos is that the company expects to benefit from simultaneous margin expansion. This is because all-in sustaining costs [AISC] are expected to decline to ~$950/oz if Lynn Lake is added with Lynn Lake's first five-year set to come in below $800/oz, even adjusting for inflationary pressures. If achieved, this would make Alamos' one of the lowest-cost producers globally, augmenting an already premium multiple given its primarily Tier-1 jurisdictional profile (~80% of production will come from Tier-1 ranked jurisdictions post-2026, increasing to ~85% if Lynn Lake is developed). Hence, while the sector may never see a repeat of Kirkland Lake Gold, which was a solely Tier-1 producer with 700,000 ounces of gold production at sub $600/oz AISC in its prime thanks to an average mined grade of 20-plus grams per tonne of gold (Macassa, Fosterville), Alamos would certainly be a close second if it can deliver on its organic growth potential that's already in its pipeline (P3+, PDA, Lynn Lake).

{kind=link}

Island Gold Mine Operations - Company Website

Recent Developments

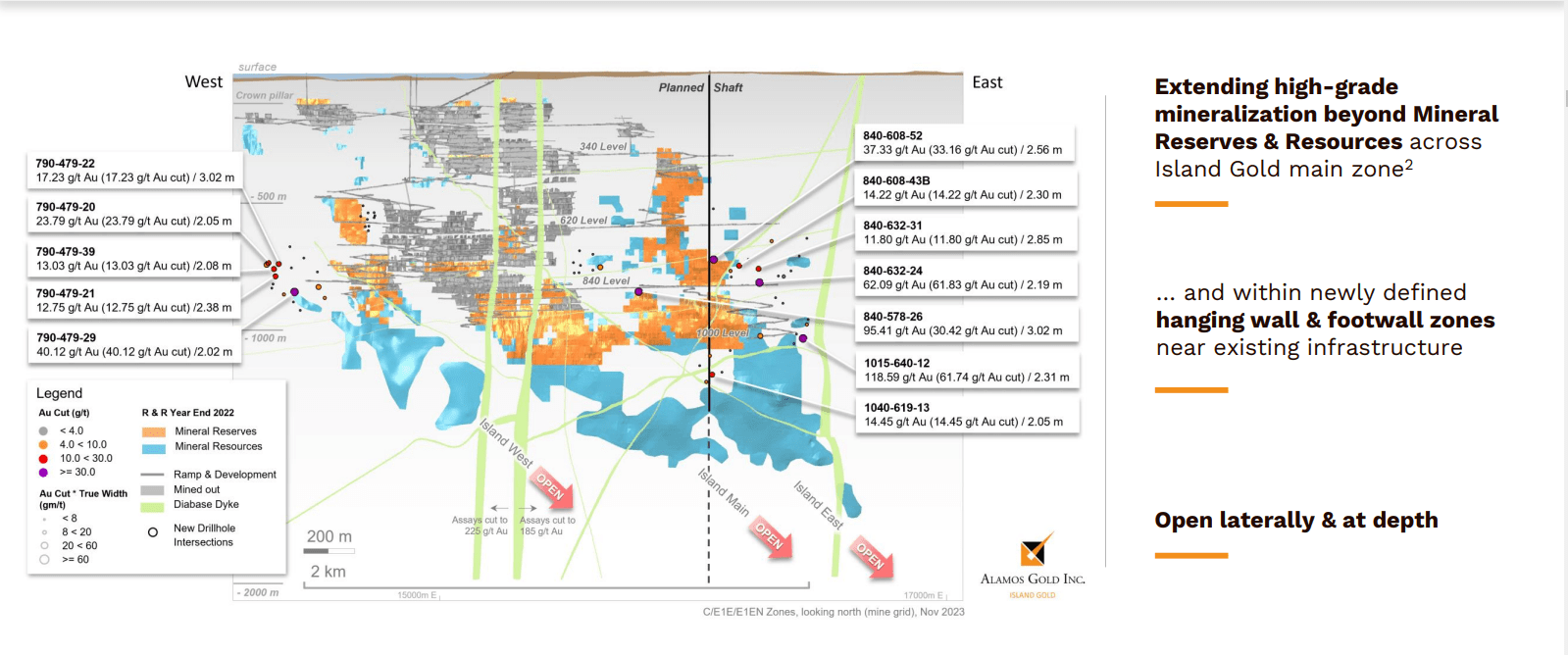

Finally, looking at recent developments, Alamos noted it has a busy year ahead in 2024 with an exploration budget of $62 million (+24% year-over-year), and total capital expenditures of ~$410 million. This includes $34 million in growth capital and capitalized exploration at Lynn Lake (with some of this including expenditures from its planned upfront capex), ~$220 million in growth capital at Island Gold, and ~$22.5 million at Young-Davidson. At Lynn Lake, Alamos plans to complete detailed engineering, upgrade road access, and work on a power line upgrade. As for Island Gold, Alamos expects to spend $19 million on exploration (+ 35% year-over-year), which will include 41,000 meters of underground drilling to add resources/reserves near existing infrastructure and 12,500 meters of surface exploration at what the company believes are high potential areas of Island West, Main, and East, the up-plunge extension of the Island West ore shoot, and the potential for high-grade mineralized hanging wall structures near surface.

{kind=link}

Island Gold Mine Exploration Success - Company Website

As for regional drilling at Island, Alamos will be following up on high-grade hits from Pine-Breccia and the 88-60 Zone, where the company hit an impressive 9.31 meters at 29.77 grams per tonne of gold, 0.67 meters at 3,441 grams per tonne of gold, 4.06 meters at 79.44 grams per tonne of gold, as well as several other high-grade intercepts. This regional program has been expanded to 10,000 meters from 7,500 meters last year, and while it's early days this could represent a mini Island Gold in a best-case scenario, with this prospect less than just 4 kilometers from the Island Gold Mine which would offer further mine life extensions on top of an already long mine life.

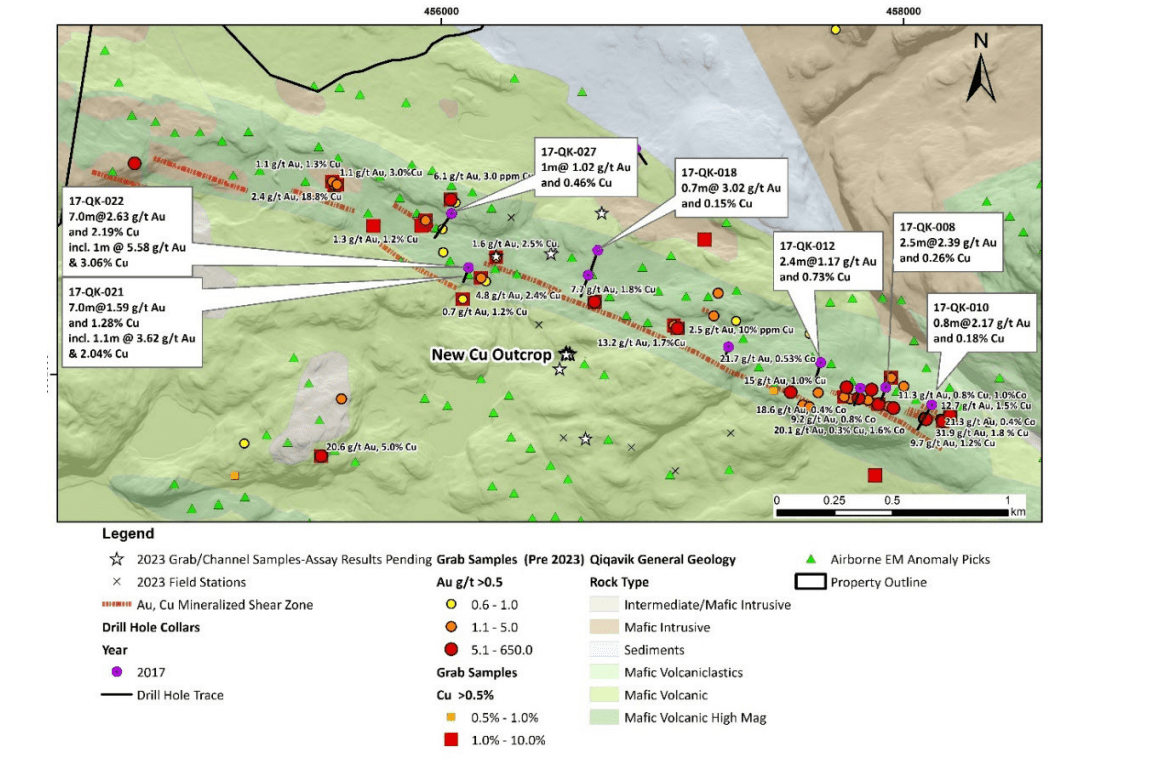

Finally, I imagine that Alamos might do some initial drilling at the Qiqavik Project in Quebec in H2 after its recent ~$16 million acquisition of Orford Mining, with this deal being in line with Alamos' strategy of making low-risk bets counter-cyclically with the potential for massive payouts, similar to its acquisitions of Lynn Lake and Mulatos for less than $35 million combined, with these assets having a combined NPV (5%) of ~$1.2 billion and Mulatos having already generated just shy of $500 million in free cash flow. While drilling has been sparse at Qiqavik, highlight intercepts include 7 meters at 2.63 grams per tonne of gold and 2.19% copper at the Esperance gold-copper showing, and the total land package is 438 square kilometers at Qiqavik, with a total land package of ~1,900 square kilometers in Quebec, including the Joutel gold-copper project just west of the Eagle-Telbel Mine previously operated by Agnico Eagle ( AEM ) that produced over 1.0 million ounces of gold.

{kind=link}

Qiqavik Gold-Copper Project - Orford Mining

Valuation

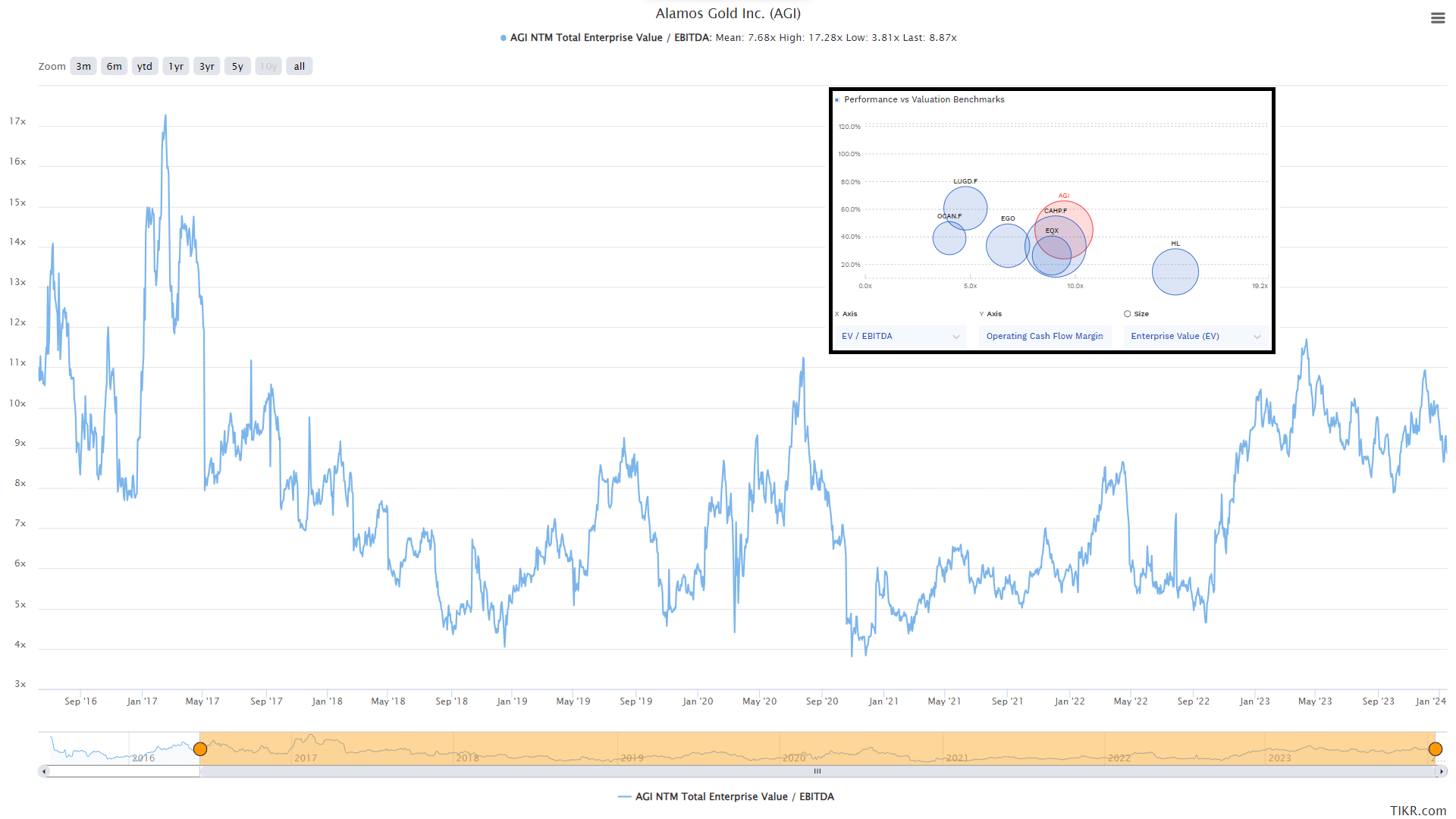

Based on ~404 million fully diluted shares and a share price of US$12.30, Alamos trades at a market cap of ~$4.9 billion and an enterprise value of ~$4.6 billion. This makes Alamos one of the highest capitalization producers in the sub 1.0 million ounce gold-equivalent producer space, ahead of names like Hecla Mining ( HL ), Equinox ( EQX ), Eldorado Gold ( EGO ) and Lundin Gold ( OTCQX:LUGDF ). However, one could argue that Evolution Mining ( OTCPK:CAHPF ) is one of the closer peers to Alamos with a primarily Tier-1 jurisdictional profile, yet it trades at a higher enterprise value with a far less impressive track record, declines in production per share, and much higher costs after backing out its copper by-product credits which don't provide a true measure of profitability. Hence, while Alamos may appear overvalued next to peers at ~9.0x FY2024 cash flow estimates, this is largely a reflection of it being the closest thing to a Kirkland Lake Gold in the sector today with primarily Tier-1 operations, a path to sub $1,000/oz AISC, and an impressive track record of cash flow and reserve per share growth.

{kind=link}

Alamos Gold EV/EBITDA Multiple & Peer Comparisons - FinBox, TIKR

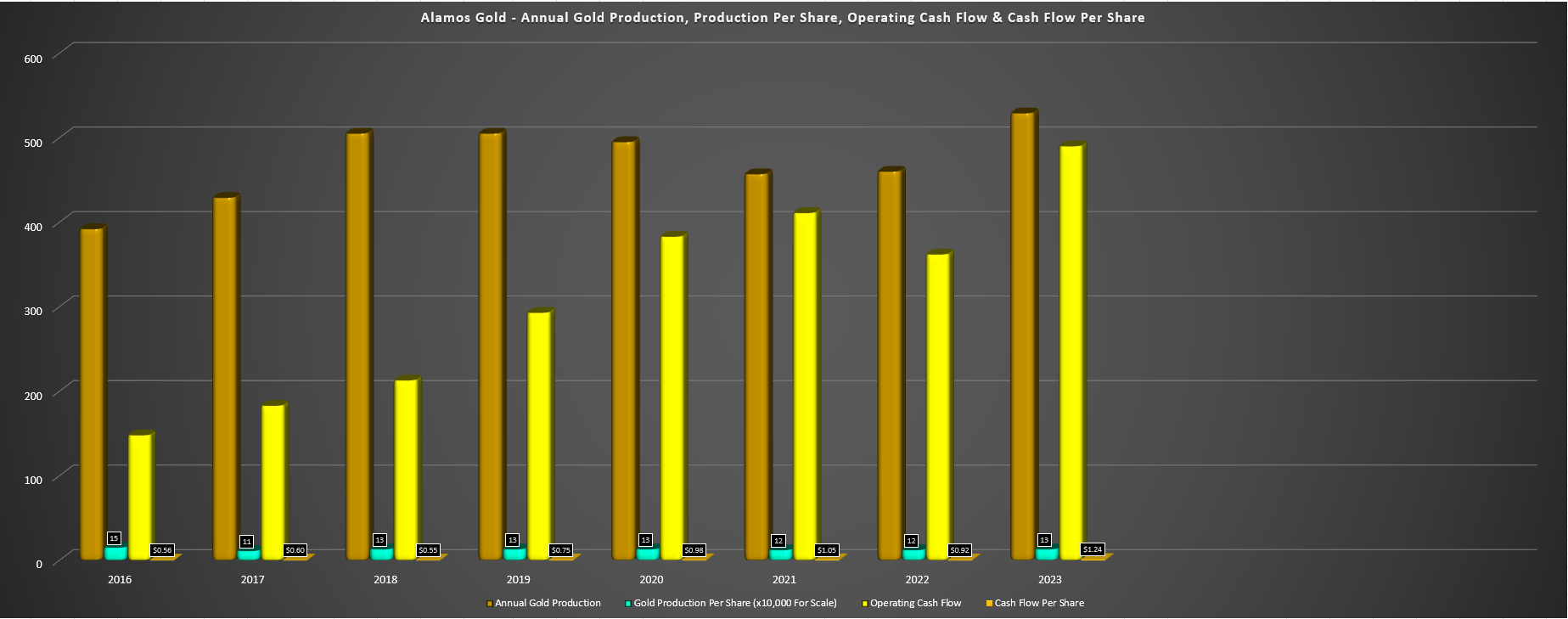

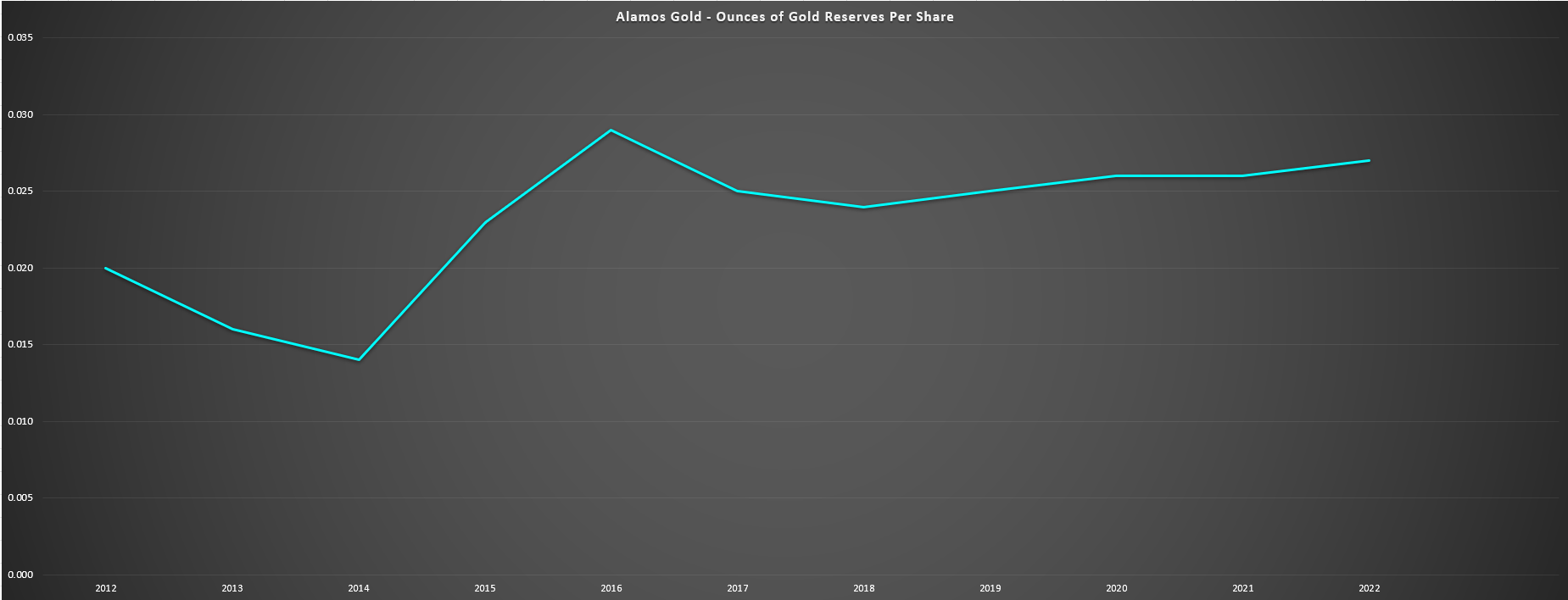

The below chart provides evidence of this track record, with reserves per share trending higher since the last cycle, which places it in rare air vs. peers, and cash flow and cash flow per share also steadily trending higher. And while production growth per share may not have increased since 2016 levels, the timeline is not a fair gauge of true production per share growth given that Island Gold is operating at just half of its average annual production once P3+ is complete (~290,000 ounces), it has another ~180,000 ounces in the pipeline with Lynn Lake, and its production per share plans were disrupted by a hiccup in Turkey, with Kirazli partially constructed and expected to be one of the lowest-cost gold assets globally (~100,000 ounces at sub $600/oz AISC on inflation adjusted basis), but unable to proceed with construction due to the government refusing its Forestry Permit.

So, while gold production per share may not be at new highs, it will hit record levels in 2027 despite this setback, and with higher-quality production, with more ounces coming from Tier-1 jurisdictions and lower-cost ounces overall. Finally, while many producers have seen a significant increase in costs since 2016, Alamos' organic growth profile has placed it on a path to have similar/lower costs a decade later with (~$1,000/oz vs. ~$1,000/oz) due to the addition of a world-class asset in Island Gold and subsequent exploration success that's allowed Alamos to pursue an expansion to 2,400 tonnes per day.

{kind=link}

Alamos Gold - Annual Production, Production Per Share, Operating Cash Flow & Cash Flow Per Share - Company Filings, Author's Chart

{kind=link}

Alamos Gold - Gold Reserves Per Share - Company Filings, Author's Chart

Summary

Alamos Gold continues to be one of the best-run producers sector-wide and has deservedly outperformed the sector over the last 18 months, being one of the few miners sitting well above its 2020 highs at the previous peak for GDX. However, the company hasn't even begun to see the benefits of Island Gold (still in construction phase), it has another high-margin asset in the wings with Lynn Lake, and this transformation from a low-cost producer to an ultra-low cost producer with larger scale should help the stock maintain and grow its premium multiple if it continues to execute successfully. So, with a track record of over-delivering on promises, significant exploration upside still at Island, and the discipline to not over-pay which has led to accretive M&A when it's pursued, I see Alamos as a top-5 producer sector wide, and I would view sharp pullbacks as buying opportunities.

For further details see:

Alamos Gold: Another Beat On Annual Guidance