CA - Alamos Gold: Island Gold Continues To Grow

Summary

- Alamos Gold was one of the best-performing gold stocks in 2022, up 31% vs. a 10% decline in the Gold Miners Index.

- The outperformance can be attributed to continued exploration success across its portfolio, continued capital discipline, and that it was one of only a few miners not to raise cost guidance.

- Meanwhile, investors received more good news earlier this year, with the company's three-year outlook pointing to below-industry-average costs and declining costs year-over-year (2023 vs. 2022).

- Given Alamos' combination of capital discipline, continued exploration success combined with an industry-leading organic growth pipeline, I would view sharp pullbacks in the stock as buying opportunities.

2022 was a rollercoaster year for investors in the Gold Miners Index ( GDX ). Most gold producers finished the year in negative territory, with some of the largest producers suffering 30% drawdowns after the index made a lower high in April 2022. Fortunately, investors that sought sanctuary in Alamos Gold ( AGI ) were rewarded nicely, with the stock putting up a 31% return, trouncing more than 90% of US-listed stocks from a share-price performance standpoint and all of its peers. The outperformance can be attributed to continued exploration success across its portfolio, continued capital discipline, and that it was one of only a few miners not to raise cost guidance.

However, although 2022 was an exciting year with multiple impressive intercepts drilled at PDA and Island Gold, this story is still in its early innings. This is because Alamos may be a 500,000-ounce producer today, but it can grow to ~800,000 ounces long-term with the current Phase III Island Gold Expansion underway and the potential for 170,000 ounces per annum post-2026 from Lynn Lake in Manitoba. Even more importantly, Island Gold is set to become Canada's lowest-cost gold mine post-2025, giving Alamos a rare combination of growth and margin expansion. Given these unique attributes combined with the company's capital discipline, I expect sharp pullbacks to provide buying opportunities.

{kind=link}

Island Gold Shaft Construction (Company Presentation)

Recent Developments

Alamos Gold had a busy year in 2022 with multiple highlights that included the following:

- The sale of its non-core Esperanza Project for total consideration of up to $60 million

- Ground-breaking for its Phase III Expansion at its Island Gold Mine

- The start of initial production at its high-grade La Yaqui Grande Mine

- The confirmation of robust economics for Island Gold Phase III (25% IRR at $1,850/oz gold with ~287,000 ounces produced per annum

- Continued exploration success with high-grade intercepts at PDA that suggest further resource/reserve growth ahead

- Multiple high-grade step-out intercepts at Island Gold that point to continued resource/reserve growth at this phenomenal asset

- Beating the mid-point of its production guidance for FY2022 while maintaining cost guidance in a sea of misses sector-wide

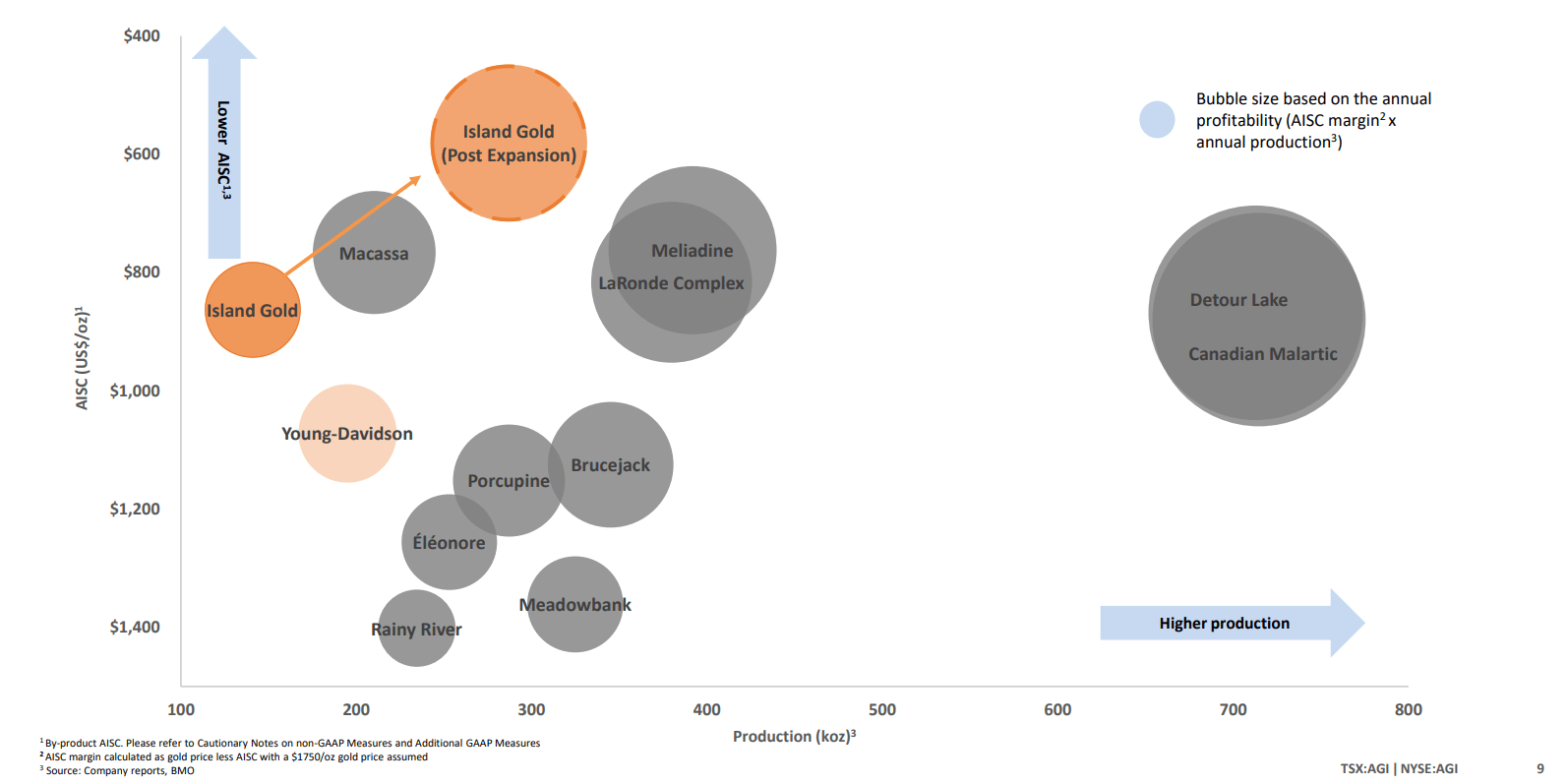

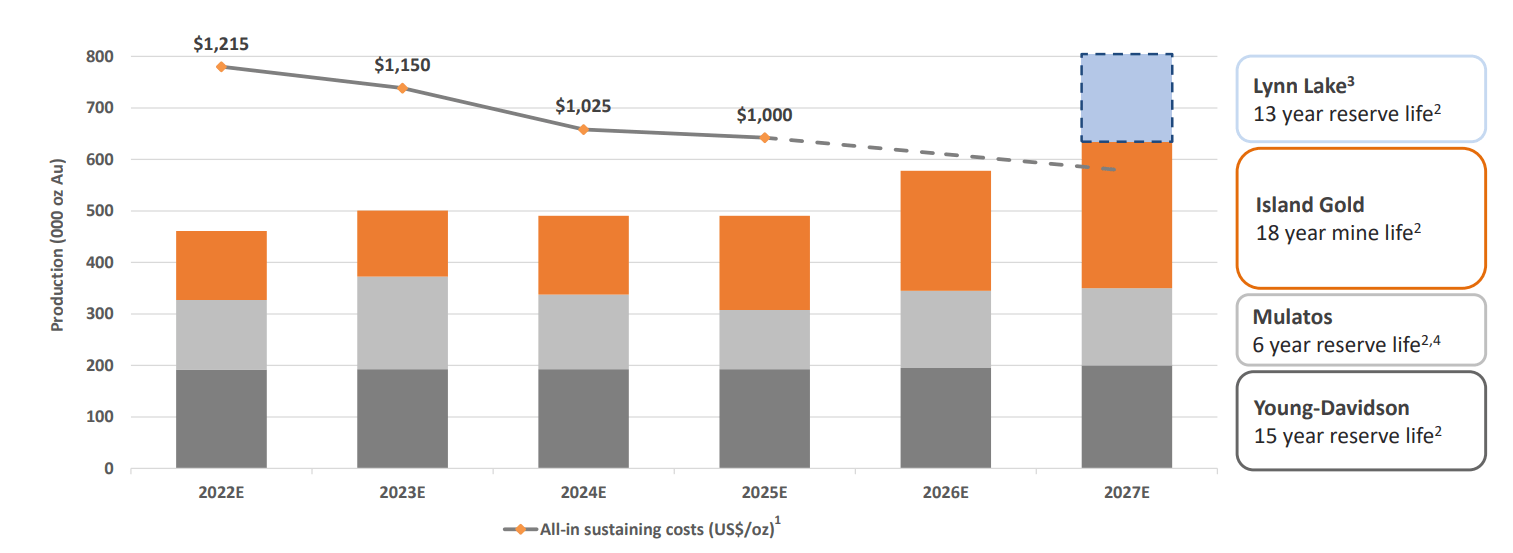

However, arguably the most exciting news was the continued exploration success at Island Gold which could augment an already impressive production profile post-2026 once the shaft with a hoisting capacity of 4,500 tonnes per day is complete. For those that missed the study, the Phase III Expansion is expected to turn Island Gold from a ~140,000-ounce per annum operation with $950/oz costs to a ~287,000-ounce per annum operation at $580/oz all-in sustaining costs [AISC]. This would make Island Gold the lowest-cost operation in Canada by a wide margin and potentially the lowest-cost gold mine in North America now that Long Canyon is offline. However, with continued exploration success at Island Gold, it's looking like this production profile could be improved upon, and the already industry-leading 18-year mine life could be extended.

{kind=link}

Island Gold Current vs. Post-Expansion vs. Other Canadian Gold Mines (Company Presentation)

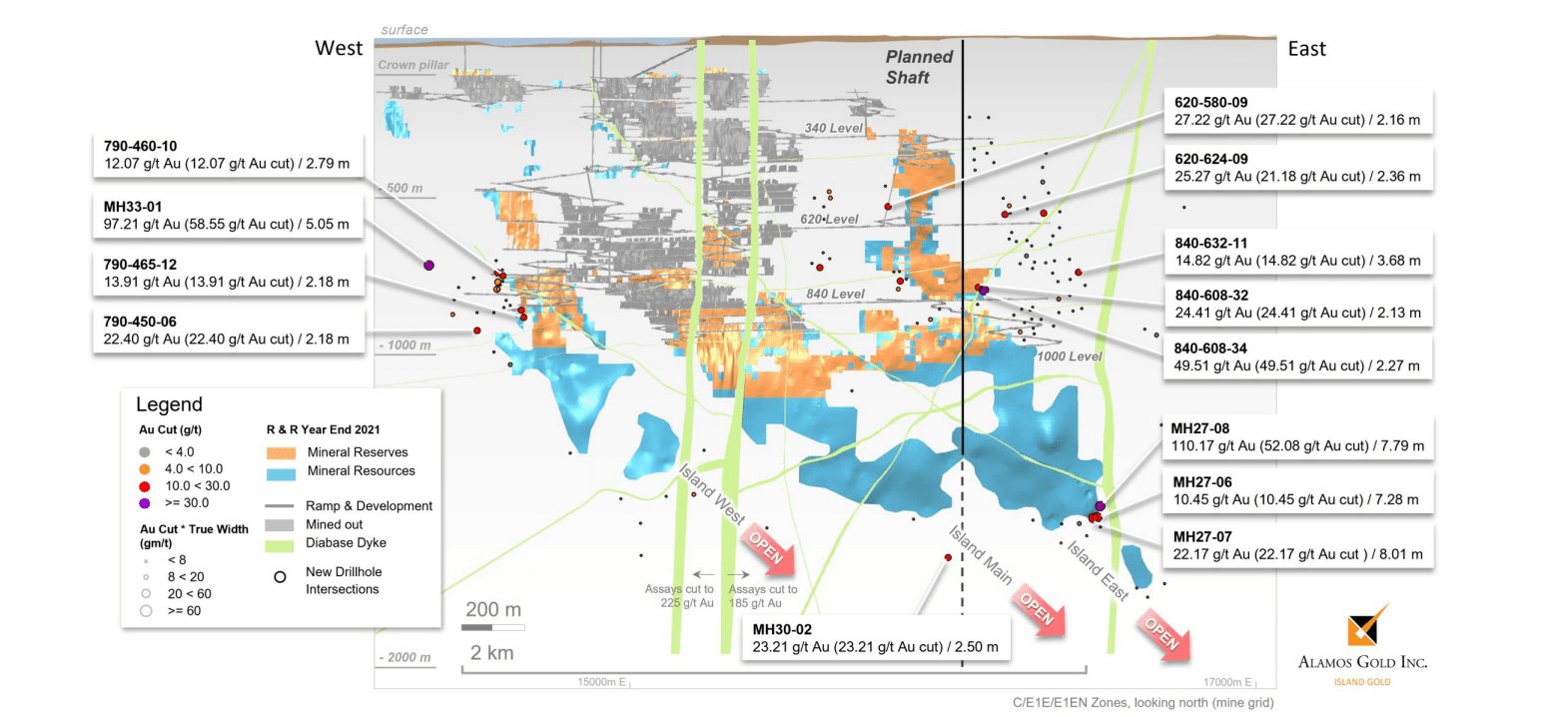

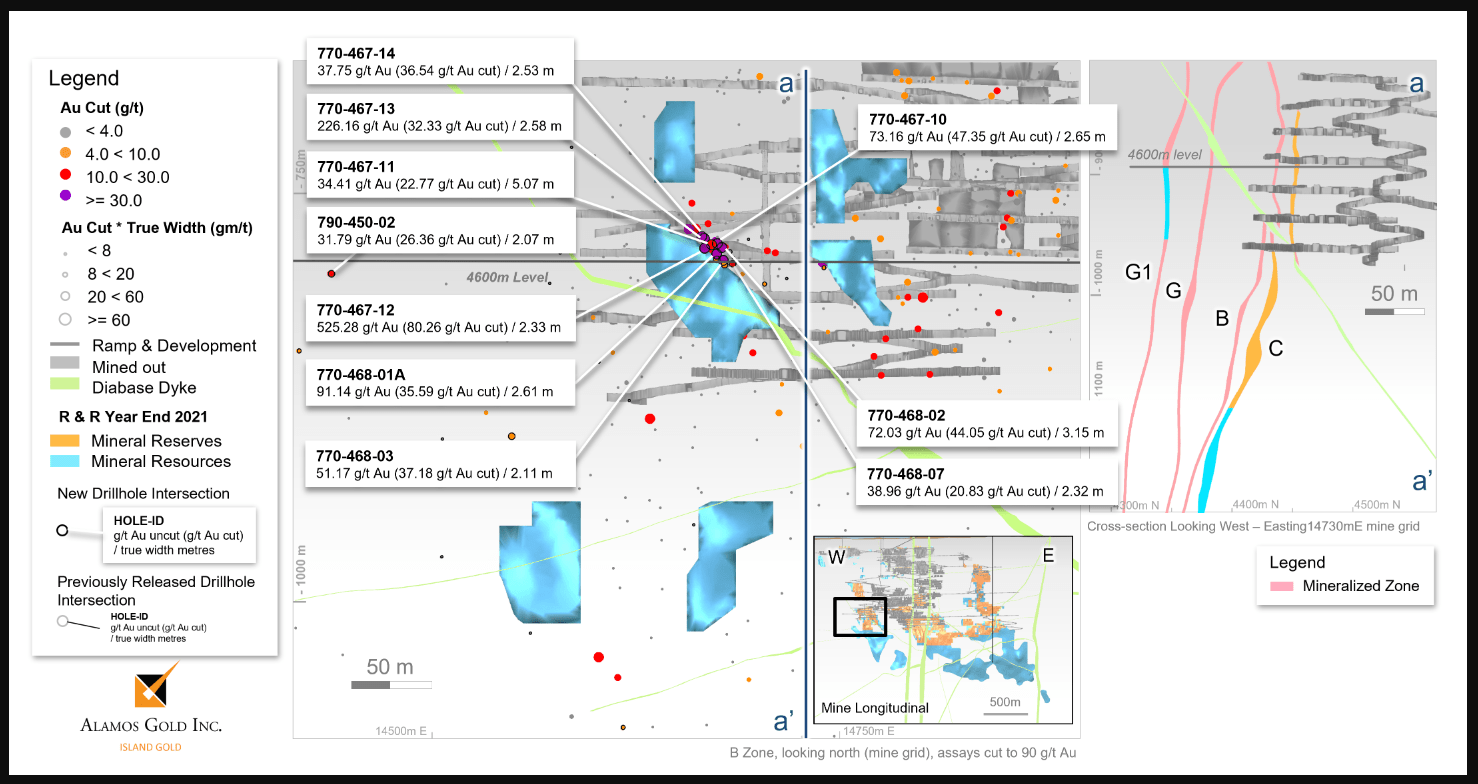

As reported in November, Alamos Gold announced multiple high-grade in multiple zones at its Island Gold Mine in Ontario, Canada, with the highlight intercepts from a grade and thickness standpoint being as follows:

- 5.05 meters at 97.21 grams per tonne of gold

- 2.33 meters at 525.28 grams per tonne of gold

- 3.15 meters at 72.03 grams per tonne of gold

- 2.58 meters at 226.16 grams per tonne of gold

- 7.79 meters at 110.17 grams per tonne of gold

- 8.01 meters at 22.17 grams per tonne of gold

These results are encouraging because they come in well above the Island's average reserve grade of 10.12 grams per tonne of gold, and they've extended high-grade gold mineralization in multiple areas of this already well-endowed asset. In fact, if there were any critics of Alamos' 2017 acquisition of Richmont due to the price paid per ounce, those critics have been silenced, with Alamos growing its total resource base to ~5.1 million ounces of gold, double that of its resource when the project was acquired even after accounting for annual mining depletion (below chart). Just as noteworthy and rare in this sector, the inferred resource base backing up its reserves is nearly 40% higher grade.

{kind=link}

Island Gold - Reserve & Resource Growth (Company Filings, Author's Chart)

Digging into the recently reported drill results in more detail, we can see that Alamos hit multiple high-grade intercepts down-plunge of the ultra high-grade inferred resource block of ~1.97 million ounces at 15.49 grams per tonne gold. These intercepts included 8.01 meters of 22.17 grams per tonne of gold, 7.28 meters of 10.45 grams per tonne of gold, and 7.79 meters at an incredible 110.17 grams per tonne of gold. These intercepts are just east of the planned shaft and right next to this high-grade resource block, suggesting that Island Gold could look at pulling a significant portion of these ounces forward in the mine plan if converted to reserves, which could spike production in the earlier years of the mine life and boost Island's NPV (5%).

{kind=link}

Island Gold - Highlight Drill Intercepts & Existing Infrastructure/Planned Shaft (Company Presentation)

{kind=link}

Island Gold - Highlight Intercepts (Island East & Main) & Planned Shaft (Company Website)

Meanwhile, at Island East and Main, but closer to the surface (840 level) and just east of the planned shaft, Alamos hit 2.13 meters at 24.41 grams per tonne of gold and 2.27 meters at 49.51 grams per tonne of gold to expand on existing reserves in the area. In addition, Alamos stepped out from reserves and hit multiple high-grade intercepts that included 2.36 meters at 25.27 grams per tonne of gold and 2.16 meters at 27.22 grams per tonne of gold (620 level), with the former intercept (620-580-09) being a significant step-out more than 100 meters from the closest reserve/resource block. Finally, hole 840-632-11 hit above-average grades (14.82 grams per tonne of gold) 120 meters east of the nearest mineral resource, drilled from the eastern extent of the 840-level exploration drift.

{kind=link}

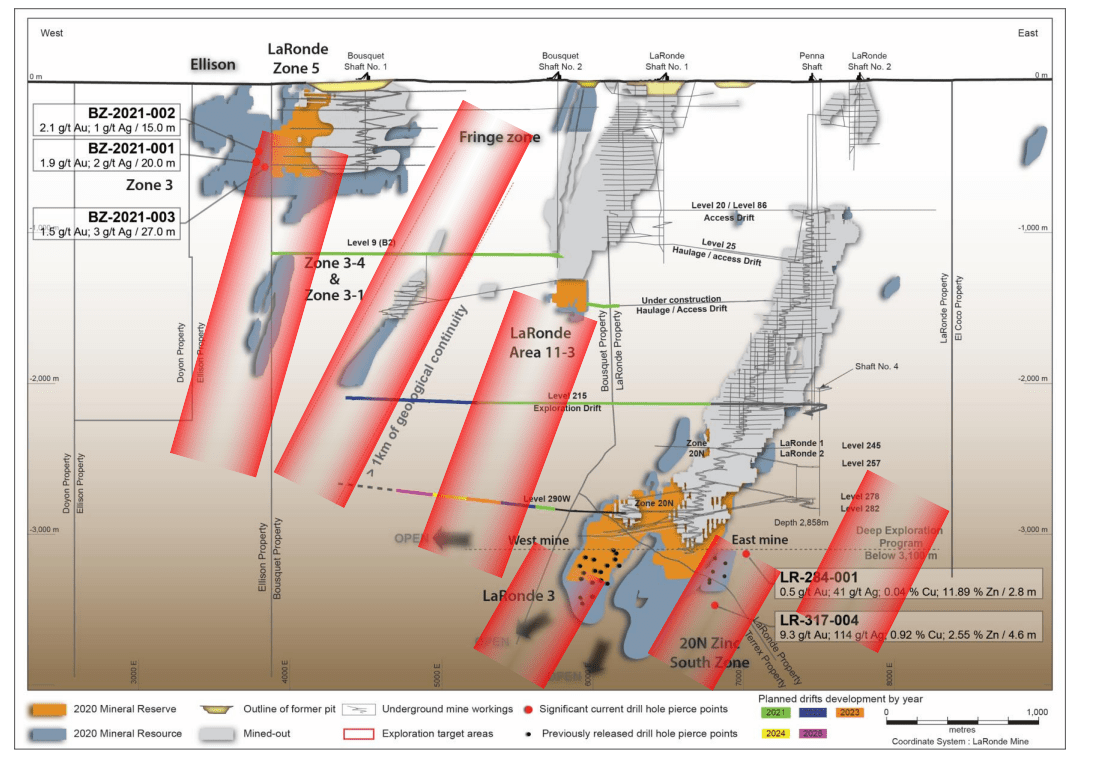

Agnico - LaRonde Complex Highlighting Reserves Below 3,000 Meter Vertical Depth (Agnico Presentation)

Finally, I'd be remiss not to point out that drill hole MH30-02 intersected 2.50 meters at 23.21 grams per tonne of gold and is one of the deepest intersections drilled to date at the mine at a vertical depth of more than 1.50 meters. The grades on this hole are exceptional and suggest that there's likely further growth ahead for this mine, not just laterally but also at depth, supported by the fact that underground gold deposits in the Canadian Shield have been shown to extend to depths well below 3.0 kilometers in the case of Red Lake - Campbell in Red Lake, Ontario, and LaRonde, a mine that's been operating for over 30 years in northwestern Quebec.

Moving over more than one kilometer to the west to Island West, Alamos saw just as much success in this area of its mine, reporting an ultra high-grade intercept of 5.05 meters at 97.21 grams per tonne of gold more than 200 meters west of existing reserves. The company also intersected 2.18 meters at 22.40 grams per tonne of gold just west of an inferred resource block near the 1,000-meter level. Elsewhere at Island West, Alamos reported multiple high-grade intercepts within newly defined sub-parallel zones in the hanging wall (B, G, and G1 zones, which lie 20 meters, 75 meters, and 110 meters south of the main C-Zone, respectively). This points to continued resource and reserve growth in the western portion of the mine right next to existing infrastructure and at impressive grades (highlight intercept of 2.33 meters at 525.28 grams per tonne of gold), pointing to a very high return on these ounces (limited development work needed).

{kind=link}

Island West Drill Highlights (Company Website)

Overall, these drill results are highly encouraging in terms of the future of this asset, and they certainly reinforce Alamos' decision to increase mine and mill production at this asset to access these ounces much quicker. Ultimately, given the exploration success to date just from near-mine drilling and without accounting for regional upside from its Trillium Mining acquisition, it looks like Alamos could ultimately delineate 8.0+ million ounces of mineral inventory (resources and reserves combined) by the end of the decade, which would make Island stand out as not only one of the lowest-cost gold mines globally but also one of the longest-life assets globally (especially among underground mines), which should help Alamos to command a premium when combined with Young-Davidson's long mine life as well.

So, what does this mean for Island Gold and Alamos?

While Island Gold was already expected to be a transformative asset with the production of more than 285,000 ounces of gold per annum post-shaft completion at sub $600/oz AISC, it's looking like we could see further improvements to this production profile if higher-grade ounces near existing infrastructure can be pulled forward. This could result in average annual production closer to 320,00 ounces per annum from 2027-2033 vs. a current outlook of ~306,000 ounces based on the current mine plan. That would result in even higher margins, and it's already looking like Alamos will be a cash-flow machine post-2025 with nearly $300 million in average free cash flow per annum (2026-2031) at spot gold prices.

{kind=link}

Production Profile & Cost Profile with Industry-Leading Mine Lives (Alamos Gold Presentation)

Combining this production and free cash flow profile with the company's existing two mines suggests that Alamos can easily fund Lynn Lake internally, grow its dividends and opportunistically buy back shares while maintaining one of the strongest balance sheets sector-wide ($130 million in net cash currently with no debt). Most importantly, though, Alamos should command a higher multiple in the future, given that it will go from being a low-cost producer ($1,125/oz AISC vs. $1,270/oz industry average) to one of the lowest-cost producers sector-wide that also benefits from ~80% of production coming from Tier-1 ranked jurisdictions.

Hence, for those skating to where the puck will be post-2025, I would argue that Alamos could easily become a top-3 producer from an attractiveness standpoint, just behind Agnico Eagle ( AEM ), which has earned itself the #1 spot due to its disciplined growth and capital discipline, diversification, portfolio of world-class assets in safe jurisdictions, and its industry-leading track record of dividend growth. Let's take a look at Alamos' technical picture to see if it confirms the attractive fundamental story.

Technical Picture

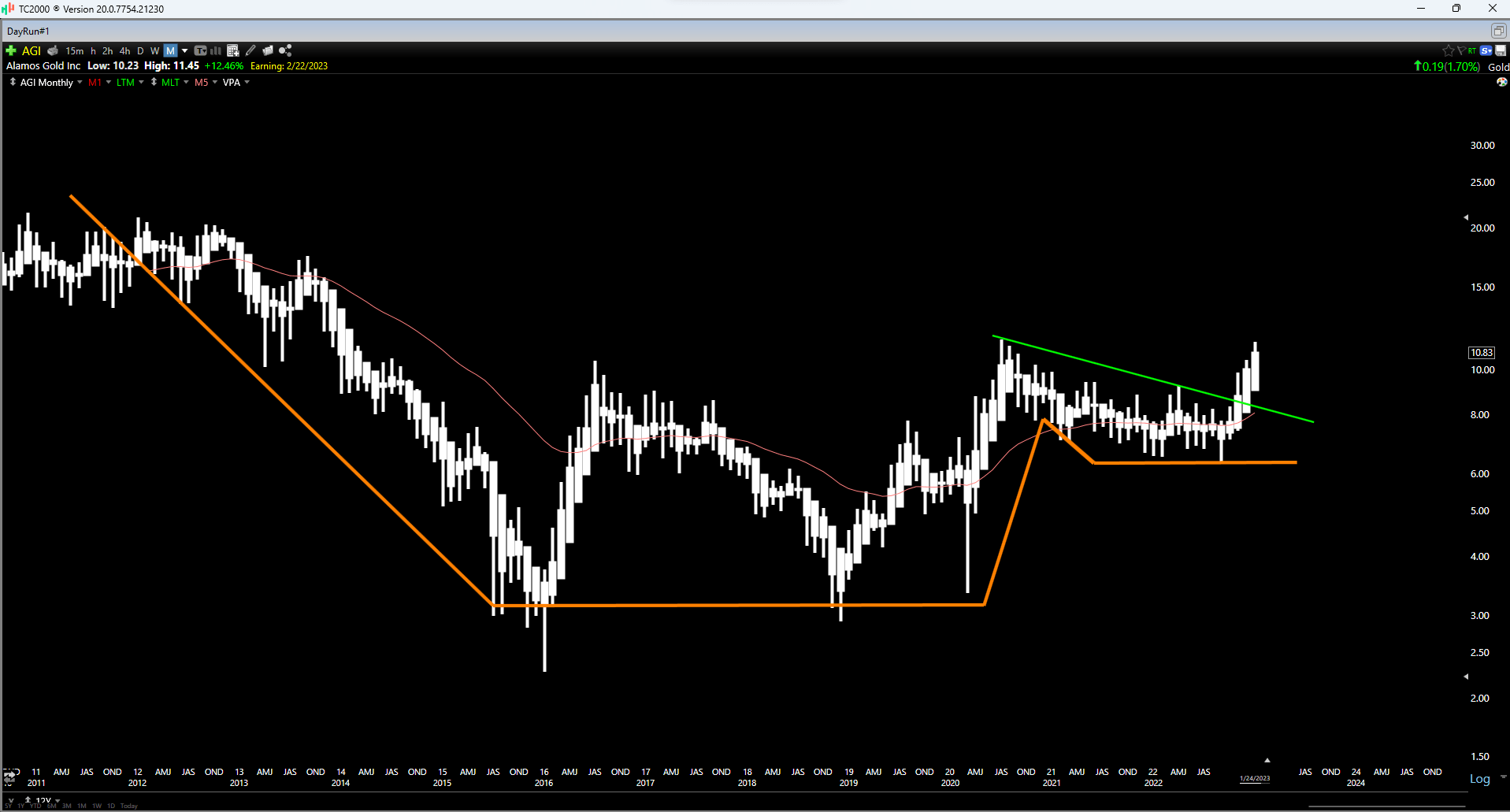

While Alamos' fundamentals are clearly strong, its technical picture is also positive, with the stock standing out among its peers in this category. This is because the stock emerged from a multi-year base after it confirmed a breakout above the $9.50 level in November. Since then, we've seen strong follow-through to this breakout, and the next major resistance level doesn't come in until $14.20, roughly 25% above current levels. This doesn't mean that the stock must head there in a straight line, but with AGI's key moving averages turning higher, I expect we'll see strong buying support on any sharp pullbacks in the future.

{kind=link}

AGI Monthly Chart (TC2000.com)

Summary

As I've often stated when praising Agnico Eagle Mines ( AEM ), the one reason to own the stock and be overweight is management's discipline and consistency, making it a sleep-well-at-night company in a sector that can be intimidating with regular negative surprises among weaker operators. This is evidenced by the company sticking to its core business plan (aiming to be a regional miner with high-quality assets and only acquiring at the right price in jurisdictions where it can see itself operating for decades). However, as great as Agnico Eagle is, some diversification is imperative even if one wants to run a relatively concentrated portfolio, and it would be aggressive to place more than 10% of one's portfolio in a single gold producer even if it does have a flawless track record.

{kind=link}

AGI - Cash Flow Per Share & Dividend Per Share Growth (FASTGraphs.com)

However, with Kirkland Lake out of the picture after the Agnico/Kirkland merger, I would argue that the runner-up for sleep-well-at-night sector leaders is Alamos Gold, which continues to operate nearly flawlessly under its co-founder and current CEO, John McCluskey. This is because the company consistently delivers on its promises, strives to maintain a strong balance sheet while regularly increasing dividends, and grows at a steady pace, not pursuing growth in an aggressive manner or at any cost, which has cost Equinox Gold ( EQX ) shareholders and could ultimately lead to an asset sale or share dilution to clean up the balance sheet.

Most importantly, though, the company doesn't make stupid decisions like making acquisitions near cyclical peaks, which is more than can be said for 80% of miners in this sector. Looking at Alamos' transaction track record, we can see that it has consistently transacted in a counter-cyclical manner, merging with National Gold in 2002, which gave it its first asset, Mulatos. It then merged with Aurico in the depths of the secular bear market in gold in April 2015 to add Young-Davidson, a consistent cash flow generator with a long mine life ahead of it. Shortly after, it acquired Lynn Lake for a song (~$22 million). Finally, it acquired Richmont to add the ultra-high-grade Island Gold Mine in September 2017, just before the bull market for gold took off, and it had the foresight to scoop up a 3.0% NSR on Island Gold in March 2020 ahead of its inevitable expansion.

{kind=link}

Alamos M&A History (StockCharts.com, Author's Notes)

To summarize, while Alamos can be trusted to operate and grow in a disciplined manner, investors also have the comfort of knowing that it's not going to acquire near a cyclical peak and take on elevated risk unless it's a rare case of an asset being special, offering unique synergies, and being significantly mispriced by the market. This combination of capital discipline, consistent operational excellence combined with three solid operating mines, and a robust development project make Alamos unique and justifies holding a core position in the stock. So, while I am not adding to my position here, given that the stock has had a nice run, I will be watching for any sharp pullbacks to top up my current position with a current average cost of US$7.20.

For further details see:

Alamos Gold: Island Gold Continues To Grow