ET - Alerian MLP ETF: Upgrading To 'Buy' With Midstream Sector Undervalued

2023-12-21 11:26:13 ET

Summary

- Alerian MLP ETF is "Buy" as the midstream space remains undervalued.

- Energy Transfer is the top holding in AMLP and is one of the most attractive stocks in the midstream space.

- All of AMLP's top holdings are trading below pre-pandemic historical norms for the midstream sector despite generally solid results over the past few years.

With the Magellan ONEOK (OKE) deal out of the way, it's time to take the Alerian MLP ETF (AMLP) back to a "Buy" rating. The ETF has generated an over 22% return since my original March article , where I argued that MLPs were trading at a historic discount despite being better companies than they were in the past. In June, meanwhile, I wanted new money buyers to just wait until after the Magellan acquisition was complete, as the ETF would have to dump its OKE shares.

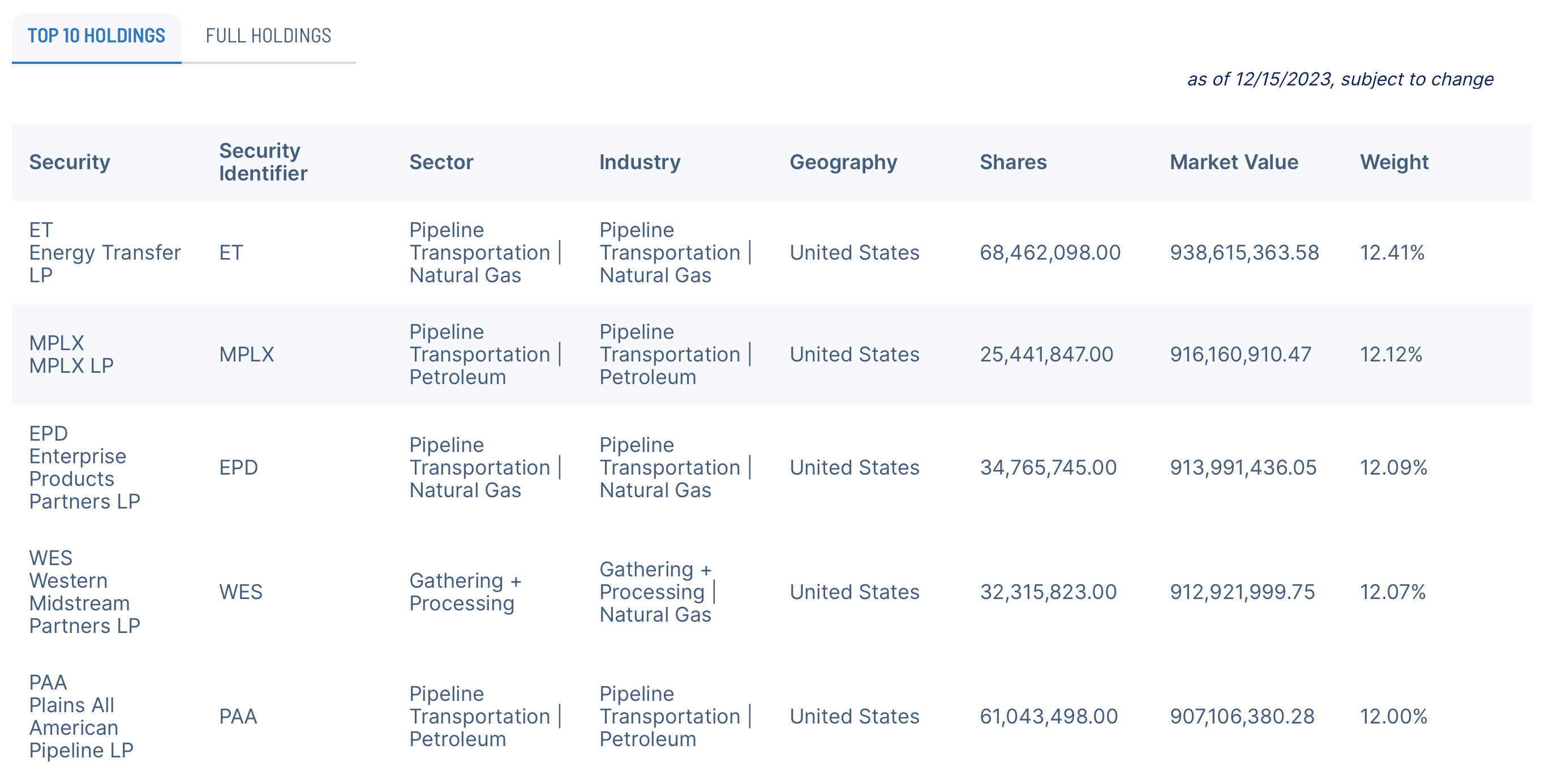

Once again, let's take a look at the ETF's top-5 holdings.

{kind=link}

Energy Transfer ( ET ) - 12.41%

ET jumps up to become the top holding in the AMLP following its acquisition of Crestwood. Notably, though, the stock holds a much larger position in the Alerian MLP Index itself at 16.0%.

I view ET as the most attractive midstream company in the space, given the quality of its assets and current valuation. It has the most diversified midstream footprints in North America, and as a result, it acts as the largest energy arbitrageur in the U.S.

Currently, ET is operating on all cylinders, seeing strong adjusted EBITDA and cash flow growth, while setting a number of new volume records in the quarter. It's been steadily growing its distribution the past two years and has an over 9% yield. At a 7.1x multiple, ET trades well below its peers despite its strong assets. The stock has a lot of upside from here.

MPLX ( MPLX ) - 12.12%

Diversified midstream operator MPLX returns to being the #2 holding in the AMLP ETF, down from the top spot last time I wrote about the ETF. MPLX has proven to be a steady performer throughout the years, and 2023 has been no exception, with strong over 10% adjusted EBITDA growth in its larger Logistics & Storage segment and modest growth from its smaller Gathering & Processing segment.

The company remains in great shape, with end of Q3 leverage of 3.4x and a distribution coverage ratio of 1.6x. With a strong backlog of growth projects and attractive contracts anchored by its parent Marathon Petroleum ( MPC ), MPLX offers a nice combination of yield, defense, and growth potential.

It remains another solid top holding in the AMLP ETF. It trades at 8.5x 2024 EBITDA.

Enterprise Products Partners ( EPD ) - 12.09%

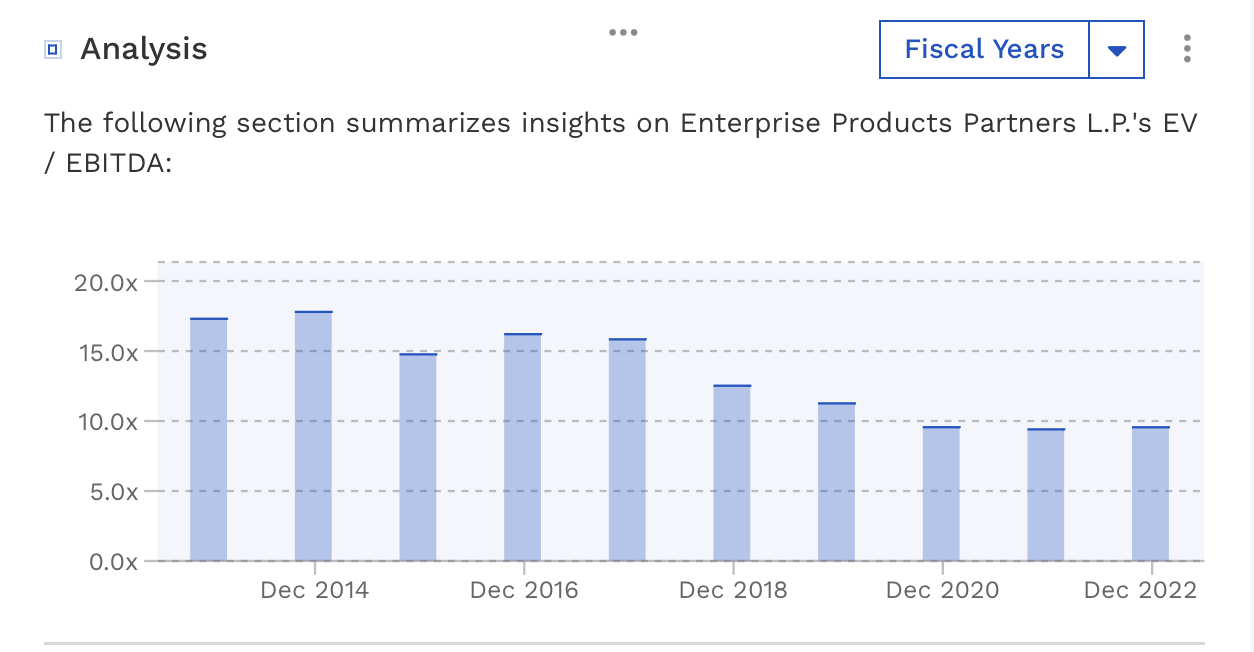

EPD is quite simply the company you want to see helping anchor any MLP or midstream fund. It has the best long-term record of any midstream company and has proven to be one of the most shareholder friendly in the process. 2023 will mark the 25th consecutive year EPD has raised its distribution, which is a remarkable feet spanning energy crashes and various other market meltdowns.

Growth was a bit modest in Q3, with just 3% adjusted EBITDA growth and flat DCF growth, and adjusted EBITDA is down nearly -2% year to date. This is more due to some spread opportunities last year that did not repeat this year.

While 2023 was a bit of an off year, with low leverage around 3.0x, a nice backlog of growth projects, and a history of solid execution, I would not bet against EPD in 2024. This remains a core holding for any midstream investor. It currently trades at 8.8x 2024 EBITDA.

Western Midstream ( WES ) - 12.07% Weighting

As a reminder, WES is a gatherer and processor (G&P) mostly for its parent Occidental Petroleum ( OXY ) in the Delaware Permian and DJ Basin in Colorado. Over 90% of its contracts are fee-based, while over 80% of its cash flows are supported by minimum volume commitments (MVCs) or cost-of-service contracts.

The company has put up solid results, growing EBITDA nearly 5% in Q3, while increasing its distribution the past two quarters. Trading at 7.3x 2024 EBITDA, the stock, meanwhile, is inexpensive.

That said, there is some uncertainty surrounding WES with OXY's acquisition of CrownRock and its subsequent planned $4.5-$6.0 billion divestiture program. This could include OXY divesting assets WES serves in the DJ, as well as potentially WES itself. OXY has been slowly unwinding its shares in WES, and the midstream operator bought back $127.5 million in units in Q3 from its parent.

Plains All American ( PAA ) - 12.00%

PAA returns to the top-5 holdings for the AMLP ETF after Magellan Midstream was acquired by OKE, which is a C Corp and thus not in the index or ETF.

PAA has a bit more hair on it than some of the other top holding in the AMLP, as it has had some issues in the past, including watching its former large Supply & Logistics segment become inconsequential and more recently overbuilding in the Permian, leaving its pipelines underutilized in the region. However, it is the latter issue that could now become an opportunity for the company.

PAA has posted some solid results this year, helped by tariff increases. However, it wasn't an easy year for the company, as industrywide Permian volume growth did not materialize as much as it was projected to at the beginning of the year. Nonetheless, PAA should benefit from future volume growth in the basin given its underutilized pipelines in the area.

I recently raised my price target on PAA, while keeping my "Buy" rating on it. It trades at 7.9x 2024 EBITDA.

Other Top Holdings

I also have recent articles on #6 holding Sunoco LP ( SUN ) from November and #8 holding Hess Midstream ( HESM ) from earlier this month.

Conclusion

With the MMP-OKE merger now out of the way, I'm going to raise my rating on AMLP back up to "Buy." I really like how its top-5 holdings are situated.

Meanwhile, I continue to believe that the midstream space remains undervalued. The AMLP ETF is a good example of this with its top-5 holding all trading between 7-9x 2024 EBITDA. Prior to the pandemic, midstream stocks were commanding a 10x multiple, while private market midstream values were about 12x. One look at EPD, meanwhile, can show the multiple compression in the space over the years.

{kind=link}

{kind=link}

This multiple compression comes despite the companies having changed for the better over the past decade by greatly reducing leverage, eliminating IDRs, and putting in place more stringent growth project criteria. At the same time, their E&P customers have also turned their focus on cash flow versus production growth, making the industry much healthier.

Overall, I think the AMLP ETF is a nice way to play the undervalued midstream space without the inconvenience of getting a K-1.

For further details see:

Alerian MLP ETF: Upgrading To 'Buy' With Midstream Sector Undervalued