CA - Algoma: Mr. Market Continues To Offer This Stock At A Steep Discount

2023-10-25 10:52:30 ET

Summary

- Algoma Steel Group Inc. is a Canadian steel provider that meets the criteria of being oversold with compelling valuations and a robust balance sheet.

- The company's shares have been on a downward trend, but there is potential for support at the recent December lows, making it attractive to value investors.

- Algoma's valuation is significantly lower than the sector average, with cash flow, earnings, and sales all below industry standards.

Intro

Algoma Steel Group Inc. (ASTL) is a Canadian steel provider that has been in operation for well over a century. This company came across our desk from a screen we ran where the objective was to find oversold stocks with compelling valuations and robust balance sheets to boot. Furthermore, the screen's crucial component was that the companies in question had to have maintained profitability (positive net earnings) despite their most likely recent bearish trends. ASTL fulfilled these conditions which made us investigate the company further.

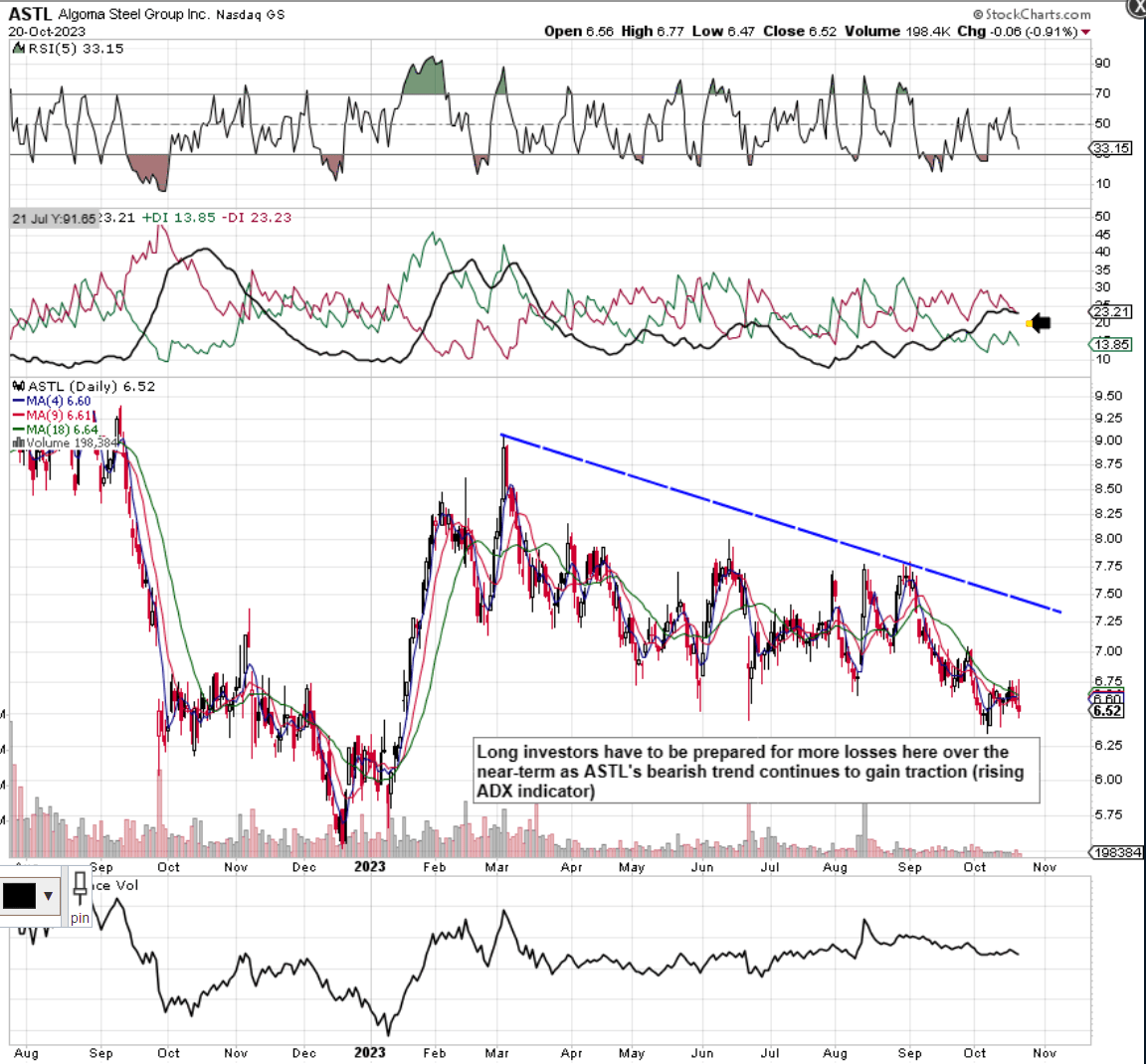

If we look at ASTL's technical chart, we see that although shares started off calendar 2023 on a sound footing with shares rallying above $9 a share by early March of this year, lower highs then began to become the norm over the past 8 months or so. Suffice it to say, that if Algoma's present bearish trend persists over the near term, we could easily see at least a retest of the recent December'2022 lows below $5.70 a share (14%+ below the prevailing share price). However, we believe that underside support would hold there given how the stock's ultra-low valuation would be even more attractive to value investors at that juncture.

Algoma Steel Technical Chart (Stockcharts.com)

{kind=link}

Valuation & Balance Sheet Strength

Algoma's valuation (when put into context with the sector at large) is definitely where this company stands out. As we see below, Algoma's assets, earnings & sales all come in significantly below what the sector is trading at over a trailing 12-month basis. As mentioned Algoma remains profitable with the company's operating profit coming in at $86.5 million over the past four quarters which is key to our thesis.

| Multiple |

| Algoma (FWD) |

| Sector Median |

| Price To Book |

| 0.58 |

| 1.54 |

| Price To Earnings (GAAP) |

| 8.84 |

| 14.39 |

| Price To Sales |

| 0.33 |

| 0.99 |

Furthermore, when we delve deeper into how cheap this company's earnings are at present, it quickly becomes apparent how attractive this company is compared to the sector in general. In fact, by using Algoma's trailing earnings yield instead of its trailing GAAP earnings multiple, we see a further discount due to the following reasons.

The earnings yield is calculated by dividing a company's operating profit by its enterprise value. Now, given, that Algoma's enterprise value brings the company's balance sheet into play (as opposed to market-cap which does not take into account the respective debt & cash balances), it is a useful metric when attempting to discern the value of a company.

Therefore, when we divide Algoma's trailing EBIT of $86.5 million by its enterprise value of $546.43 million, we get a trailing earnings yield of 15.8%. What is the moral of the story here? It is that Algoma's earnings (compared to the sector) are more attractive to us given how the company's enterprise value ($546 million) comes in lower than the present market cap ($675 million).

Improving Profitability

Although the company's EAF (Electric Arc Furnace) project discussed here is expected to boost production and cut maintenance expenses significantly over the long term, Algoma's core profitability is not as depressed as it may look at the present. In fact, if we return to the balance sheet and only focus on the capital that is actually required to run the business in earnest, we see a much sounder profitability picture.

Suffice it to say, through the following formula where we take Algoma's generous cash & ST investment balance ($226 million) out of the equation, we get a more accurate picture of the company's return on capital post Q1 of fiscal 2024. From this, we can say that Algoma's adjusted ROC (where we use EBIT as opposed to GAAP earnings to take tax & debt payments out of the equation) results in the following.

Adjusted Return On Capital Formula (oldschoolvalue.com)

{kind=link}

Adjusted ROC = 86.5 / (570.5 + 859.9) = 6.05% which is 33%+ higher than Algoma's stated ROC of 4.53%.

Forward-Looking Investing Gameplan

Most likely the biggest mistake value investors make when putting capital to work is one of timing. Especially now, (due to elevated inflation), the opportunity cost in an investment over the short term can be very real & costly for that matter. Suffice it to say, we would need to see the stock's current 10-week moving average ($6.88) rise above its 40-week counterpart ($7.31) before entertaining any thoughts of putting capital to work on the long side in ASTL.

The issue the market has at the moment with the stock is one of growth over the near term. In fact, the company's GAAP earnings have literally collapsed over the past 3 years (whilst remaining profitable) with negative bottom-line growth also expected in fiscal 2024. However, expected EPS growth from fiscal 2025 (34%+) onward has certainly not been priced in yet by the market. Therefore, as investors, looking to buy into this growth story, we should be watching earnings reports closely to see if indeed Algoma is on track to meet these projections. The company's first test is the upcoming Q2 earnings numbers which are projected to be announced on the 2nd of November next. Remember, current events form future trends so a pattern of repeated earnings beats as well as positive guidance from management in the upcoming Q2 report would most certainly keep the market interested which should keep the stock from testing those 2022 lows. ASTL's GAAP estimate is $0.21 per share. Recent EPS revisions have been encouraging so a strong beat could easily hurl shares above $7 a share.

{kind=link}

Conclusion

To sum up, although this company will undoubtedly be radically changed for the better as a result of the EAF project, we also believe the relationship between ASTL's current valuation and profitability profile is better than other peers in the steel industry as seen here . Algoma's strong balance sheet where we see shares trading at a mere 3 times their cash position means balance-sheet cash plus internal working capital will fund the grand majority of the EAF project. Therefore, we believe it is only a matter of time before value investors begin to step in here. We look forward to continued coverage.

For further details see:

Algoma: Mr. Market Continues To Offer This Stock At A Steep Discount