CA - Algoma Steel Group: Strong Prospect About To Get Cheaper

2023-08-17 01:53:11 ET

Summary

- This analysis issues a Hold recommendation rating for Algoma Steel Group Inc., a Canadian manufacturer and seller of steel products primarily for the US automotive, transportation, and infrastructure sectors.

- Algoma Steel Group Inc. is well positioned. As a result of its transformative growth plan, it aims to expand steel production and reduce carbon emissions.

- Shares are not expensive at all compared to growth prospects, but could become even cheaper soon.

A Hold Recommendation Rating for Algoma Steel Group Inc.

This analysis has issued a Hold recommendation rating for shares of Algoma Steel Group Inc. ( ASTL ) ( ASTL:CA ), a Canadian manufacturer and seller of steel products primarily for the automotive, transportation, railroad, public and private infrastructure, and for military applications. The company primarily serves the US steel markets.

The Outlook for the Steel Products

The outlook for steel products is robust as demand for these goods is boosted by the production of electric vehicles, the shift from technologies that emit CO2 and other greenhouse gases to those that do not affect the environment, as well as infrastructure expansion and increasing defense spending.

The steelmaking industry is often alleged of being one of the most polluting industries, as emissions from thermal processes, dust generation during raw material handling, and thermoelectric plants contribute to overheating, the main cause of extreme meteorological events related to climate change worldwide. However, steel is also a cornerstone of the society of the future and since we cannot do without this product, the adoption of electric furnaces will allow the steel-making industry to continue to operate with significantly less environmental impact. The introduction of environmentally friendly technologies will increase steel production as a higher quality product will be able to meet the requirements of manufacturers and the needs of the market.

Despite unstable geopolitical and macroeconomic factors, some analysts have nonetheless entered the treacherous terrain of forecasts, estimating the growth rate at 3% ( see Straits Research report 2022) or close to 5% per annum ( see Precedence Research report July 2023), indicating significant expansion for the steel market in the coming years. The most commonly cited drivers are global population growth, strong demand from China and India, and positive momentum in certain industrial sectors such as construction and automotive.

In such a global growth context and with environmental concerns in mind, Canadian steelmaker Algoma Steel Group Inc. is well positioned.

Algoma Steel Group Inc.: The Foundation for Transformative Growth Is Being Laid Despite Short-Term Headwinds

This company has an ongoing plan for a transformative Electric Arc Furnace ((EAF)) project that aims to significantly expand annual steel production capacity while dramatically reducing carbon emissions.

Additionally, the company can count on solid financials that enabled it to install a quarterly dividend in 2022 and maintain it despite a low steel price environment with near-term downside risk.

The last aspect is influenced by the looming economic recession, which is expected to hit between the end of 2023 and the first quarter of 2024 due to the very restrictive monetary policies of the central banks in the US, the Eurozone, and the UK, as part of efforts to counter runaway inflation. US real estate giant Fannie Mae and Fitch's long-term US rating Fitch downgrades US debt on debt ceiling drama and governance worries | CNN Business from AAA to AA+ recently pointed to a sharp downturn in the business cycle. These kinds of expectations can also be applied to the European space, as the US economy – the leading economy in the world – is a reliable benchmark for most developed countries, including the Eurozone and the UK, whose central banks mimic the US Federal Reserve in raising interest rates, albeit with a lag.

Signs of a deteriorating cycle stem from the continued contraction in manufacturing activity. Plus, as the economy deteriorates, overall credit quality is at stake and, given the looming economic recession, US agency Fitch indeed appears poised to downgrade the credit ratings of some major US lenders.

However, with the markets currently in the opposite mood, the recession would surprise the market as many operators are now confident that there will be a soft landing in the economy i.e., growth while controlling inflation despite the high cost of borrowings.

The recession could result in significant declines for US-listed stocks, the market value of which has likely risen disproportionately on the hype surrounding the benefits of the widespread use of artificial intelligence. This overvaluation occurred even though the regional banking crisis in the US made access to credit more difficult, hampering the chances of an economic expansion. As a result, the gap between the valuation of listed US equities and the US economy is currently a large one.

The onset of an economic recession could create a very strong headwind for the market value of US-listed shares, adversely affecting Algoma Steel Group Inc.’s stock as well, which has been tracking the unfavorable development of steel prices for about a year. As a benchmark for steel product prices, rebar futures have lost -9.58% over the past year, Trading Economics reports at the time of writing. ASTL is down 19.6% over the past year, while the S&P 500 is up nearly 4% year over year.

How an Unfavorable Steel Price Affects Algoma Steel Group Inc's Profitability, and What to Expect in the Near Future

On an operational level, Algoma Steel Group Inc. suffered significantly from the low prices of steel products in domestic markets. Despite an increase in shipment volume, which rose to 569,433 tons in the first quarter of fiscal 2024 (ended June 30, 2023) from 537,524 tons in the first quarter of fiscal 2023 (ended June 30, 2022), the Canadian steel company reported a decline in income and profit margins.

In the first quarter of fiscal year 2024 , Algoma Steel Group Inc. saw revenue of CAD 827.2 million [Canadian dollar] (or ?$624.4 million), leading to an 11.4% year-over-year decline in terms of CAD currency.

In CAD terms, Adjusted EBITDA was CAD 191.2 million (or ? $144.32 million) - a 46.5% year-over-year decrease, leading to an Adjusted EBITDA margin of 23.1% of total revenue, which in turn, decreased by 1,520 basis points year-on-year.

Steel rebar futures are currently trading at 3,575 CNY (Chinese yuan renminbi) per metric ton [MT] and analysts at Trading Economics expect the benchmark steel price to fall to 3,540.64 CNY/MT by the end of Q3-2023 and then further down to 3,402 CNY/MT in 12 months’ time. Due to a positive correlation with the price of the product it deals with, the share price of Algoma Steel Group Inc. may follow the same bearish trend expected for the steel market in the short term.

The unfavorable steel price environment is also due to deteriorating sentiment in China's steel-intensive construction sector, which has led to significant production cutbacks in key manufacturing hubs, Trading Economics reports .

The negative momentum in China's construction sector is affecting the U.S. domestic steel markets as well, which Algoma Steel Group Inc. primarily focuses on. This is due to a phenomenon observed by other international steel companies : increased penetration of imported products is putting downward pressure on the prices of steel products in domestic markets.

Given the solid growth prospects for the future, since the company targets an annual crude steel production capacity of 3.7 million tons sharply up from the current 2.28 million tons, as well as a 70% reduction in carbon emissions, but also a concrete risk of a lower share price in the short term, this analysis assumes that the stock in Algoma Steel Group Inc. earns a Hold rating instead of a buy rating at the present.

While a share price drop may well be used to strengthen the position in this Canadian steelmaker sometime in the coming weeks, investors can benefit from the dividend in the meantime.

This stock offers a forward dividend yield of 2.57%, which isn't bad when you consider that the overall US stock market - as measured by the S&P 500 index - is yielding 1.55% at the time of writing.

On September 29, 2023, Algoma Steel Group Inc. will pay a quarterly dividend of $0.05 per common share, marking the seventh consecutive dividend payment.

The Financial Condition: The Growth Project Seems to Be Well Financed

As a result of marked negative pricing factors, Algoma Steel Group reported lower cash flow from operations in the first quarter of fiscal 2024 compared to the corresponding quarter of the previous fiscal year: CAD 163.9 million (?$123.7 million) versus CAD 276.6 million (?$214. 9 million).

Thanks to a solid financial position that allows it to compensate well for this lower cash flow, the steel company manages to find the means to finance the payment of the recently introduced dividend (?$20.714 million is required for one year's dividend) and to continue the transformative EAF project, which will increase crude steel production even more than 60%. The total investment in the EAF project represents a total cost of CAD 852.5 million, of which 40% was allocated as of Q1 FY2024.

The project is expected to be commissioned before the end of 2024 when recession headwinds are likely to have passed. Meanwhile, the remaining 60% (?C$495.3 million) of the total investment will be funded by available cash (?C$301 million as of June 30, 2023) plus ?C$353 million in an undrawn revolving credit facility based on senior secured assets.

In addition, the company can rely on a) a repayable CAD 200 million contribution under the Strategic Innovation Fund [SIF] federal loan; b) the utilization of excess working capital; and c) cash inflows from operations.

Estimating how much the operations could generate over the next few weeks is extremely difficult, and probably not even useful, as they grapple with an expected lower steel price and a future that promises to be highly volatile.

According to Seeking Alpha’s analysts’ estimate of Price/fwd. Cash Flow of 2.37x, and a $787.38 million market cap for the stock, the next 12-month cash flow is therefore projected to be $332.23 million or CAD 447.72 million, which would make an important contribution to support the business and boost growth initiative.

However, should the cash inflow from operations turn out to be lower than forecast, it must be said that the following two financial ratios continue to give shareholders confidence in the soundness of the company's financial position.

- Amid the decline in the price of steel products, the company continues to generate returns that exceed the cost of financing a project, as evidenced by Algoma Steel Group's return on investment [ROIC] of 13.90% compared to Algoma Steel Group's weighted average cost of capital [WACC] of 10.65%, analysts at GuruFocus have calculated .

- Additionally, the cost of the loan is currently easily borne by Algoma Steel Group, as evidenced by an interest coverage ratio of 7.2x. The ratio is calculated as a 12-month operating income of CAD 114.6 million divided by a 12-month interest expense of CAD 16 million.

The Stock Valuation

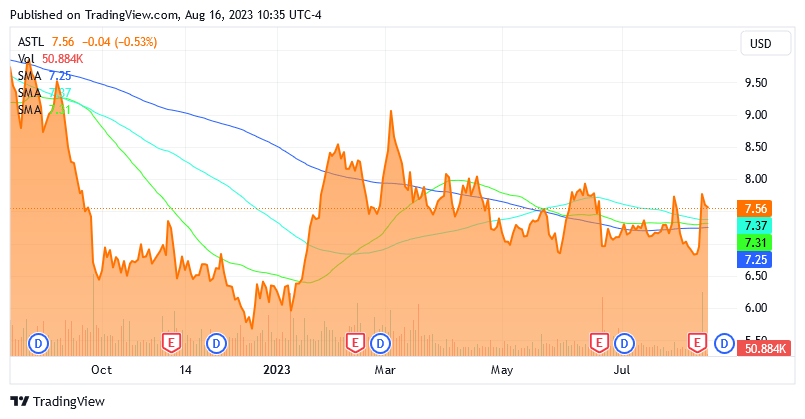

Shares of Algoma Steel Group Inc. traded at $7.56 for a market cap of $787.38 million as of this writing. The share price has fluctuated between a low of $5.64 and a high of $9.94 in the past 52 weeks. Shares are currently slightly below the middle point of $7.79 of the 52-week range.

{kind=link}

Source: Seeking Alpha

Shares are also slightly above the 200-, 100-, and 50-day simple moving average lines of $7.25, $7.37, and $7.31, respectively.

In terms of Ebitda margin compared to the steel industry, Algoma Steel Group Inc. stock is not expensive at all as its 12-month EV/EBITDA ratio is 4.15x compared to the industry median of 8.82x, and its forward EV/EBITDA is 2.12x compared to the industry median of 8.05x.

Indices constructed with EBITDA as the denominator are highly indicative and reliable as the EBITDA metric is preferred by investors to assess stocks operating in capital-intensive industries such as the steel industry.

However, there is a good chance that ahead of the steel price recovery, which after the economic recession would coincide with transformative annual crude steel production capacity, the share price of Algoma Steel Group Inc. stock could be even cheaper than the current one.

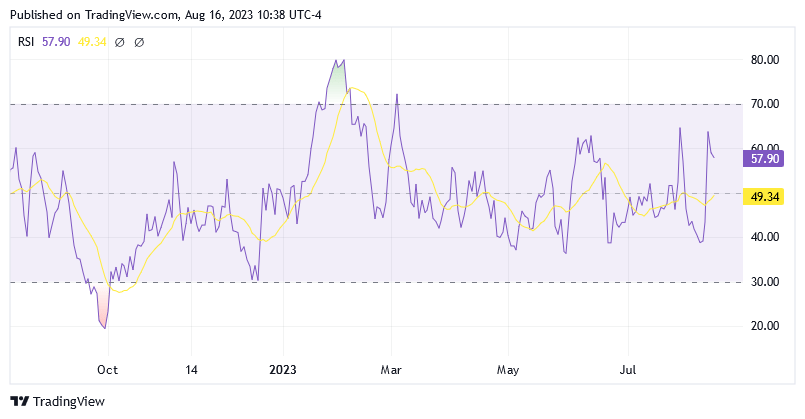

From a technical standpoint, there is scope for significantly lower levels for the share price as illustrated in the chart below, which depicts the patterns of the 14-day relative strength indicator at 57.90x as of this writing. With oversold levels still a long way off, shares can still trade significantly lower.

{kind=link}

Source: Seeking Alpha

Along with headwinds from a recession in Western countries and weak economic growth in China, the need for further rate hikes, expected by Federal Reserve Governor Michelle Bowman on August 7, to bring inflation on target by the FOMC will create strong headwinds for Algoma Steel Group Inc.’s shares. A US stock market heavily dependent on growth tech stocks, especially FAANG stocks, cannot see rising borrowing costs in good order as it affects the present value of growth stocks (higher interest rates = higher discount rate) which are very numerous among techs.

A decline in the market value of US-listed stocks is proportionately reflected in the share price of Algoma Steel Group Inc. as this stock has a 24-month beta of 1.02x (scroll this page down to the "Risk" section).

Shares also trade on the Toronto Stock Exchange under the symbol ( ASTL:CA ). Shares were trading at CA$10.24 per unit on the TSE as of this writing for a market cap of CA$1.06 billion. Shares are trading slightly above the 200-day simple moving average of CA$ 9.76, slightly above the 100-day simple moving average of CA$ 9.87, and slightly above the 50-day simple moving average of CA$ 9.72.

Shares are also slightly below the middle point of CA$ 10.265 in the 52 Week Range of CA$ 7.70 to CA$ 12.83. Also, the 14-day Relative Strength Indicator of 60.68x suggests that shares are far from oversold levels.

Conclusion

We cannot do without steel, but we can produce it with clean technologies. It is estimated that there will be a great need for this product in the coming years and that the growth of the world population, the recovery of the Chinese economy and industrial sectors such as construction and automotive will be strong key factors. Algoma Steel Group Inc. is very well positioned in this growth context as the company will complete a project to increase annual steel production by 60% before the end of 2024 while reducing emissions by 70% thanks to the use of electric furnaces. Shares are not expensive at all compared to growth prospects but could become even cheaper soon. Thus, this analysis suggests a Hold rating in the sense of waiting for the materialization of an even cheaper share price than the current one.

For further details see:

Algoma Steel Group: Strong Prospect About To Get Cheaper