CA - Alimentation Couche-Tard: Resilient But At An Unattractive Price

2023-09-12 12:31:03 ET

Summary

- Alimentation Couche-Tard has a strong track record of growth through acquisitions and reported strong earnings growth in Q1.

- It has a strong and flexible balance sheet and share repurchases are likely to lead to EPS accretion.

- However, the current valuation which is higher than historical means and in line with its peers offers limited upside. Initiate at Neutral.

Investment Thesis

Alimentation Couche-Tard (ATD:CA) (ANCTF) had a strong track record of growth, primarily through acquisitions, over the years. It has reported strong earnings growth in Q1 driven by robust fuel gross margins in the US which has been 50c/gallon, at an all-time high. However, we believe current valuation which is in line with peers and higher than historic means, factors in all the positives and leaves a balanced risk-reward for investors. Initiate at Neutral with a target price of $56.

Company Overview

Alimentation Couche-Tard is a leading global convenience store operator with over 14,000 stores spread across 25 countries. It has about 50% of its stores in US but only has 5% market share in the fragmented US market. Its major contributor is fuel sales (~74% of total revenue) while merchandise and service sales form the rest of the revenue.

Historical Track Record

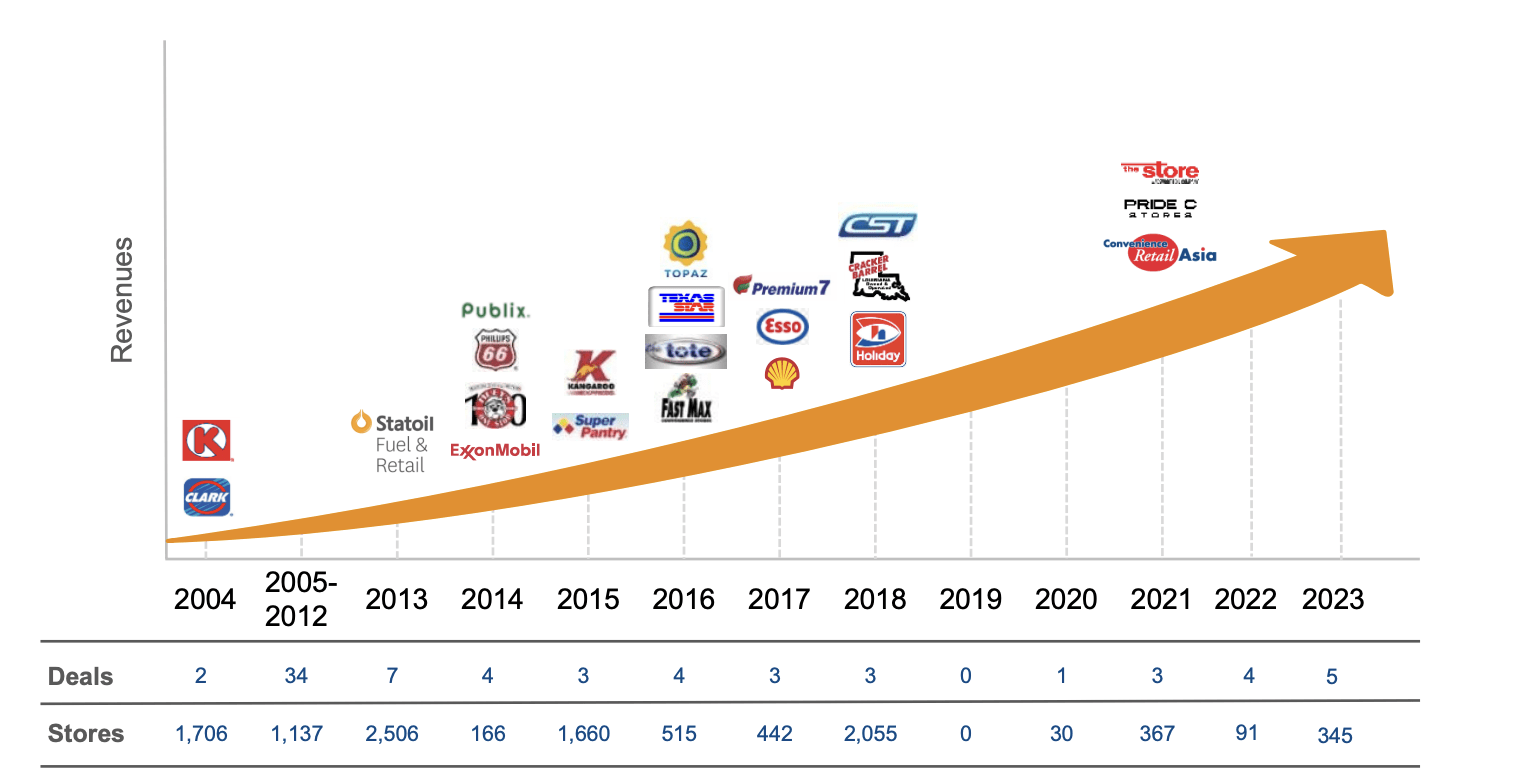

The company's growth trajectory has been significantly via inorganic approach as it has added over 11,000 stores since past two decades through over 70 acquisitions of different scale and size globally.

{kind=link}

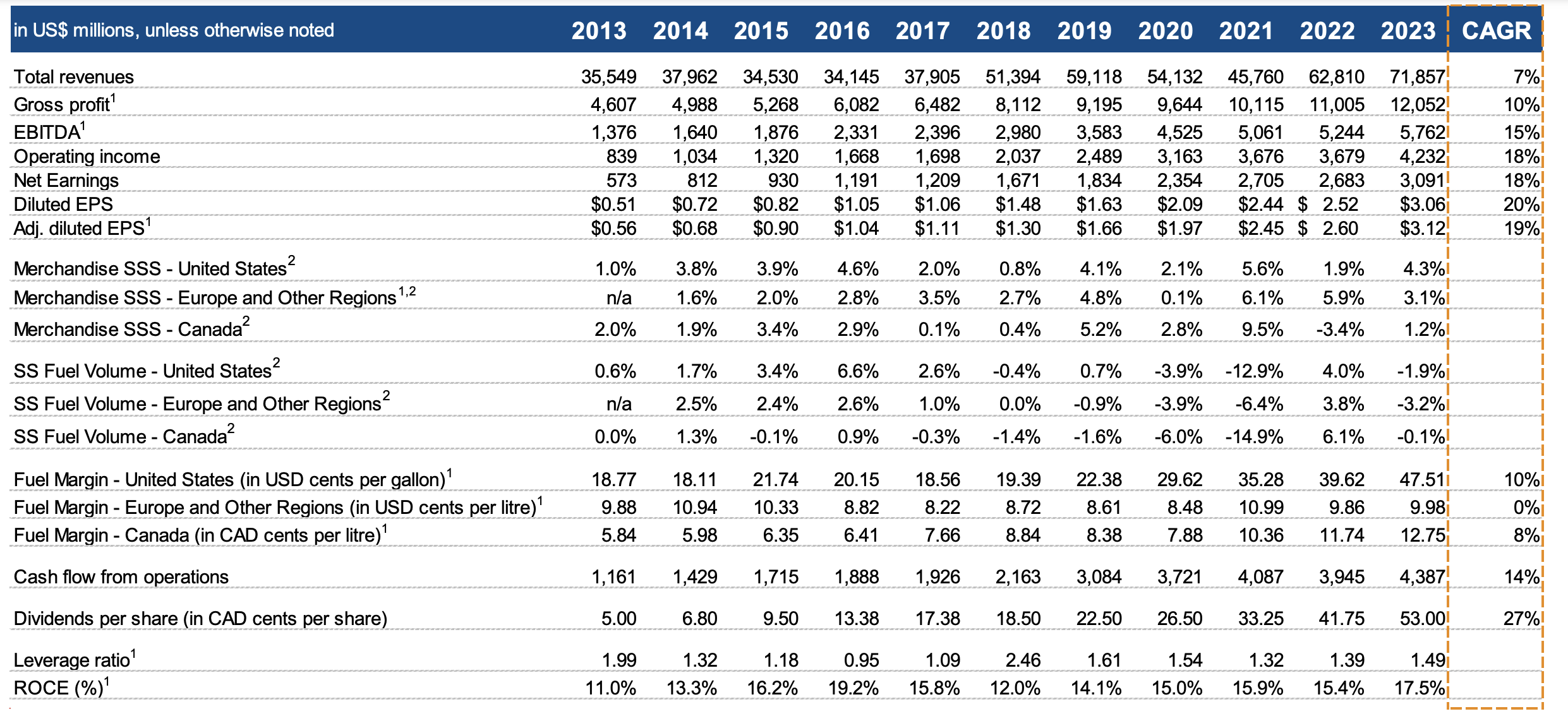

It has a strong track record of integration and has been able to report positive SSS across its stores during the last 10 years (except for COVID-19 disruption) with sustainable positive Merchandise SSS across all regions. Despite the COVID disruption, total revenues have increased 7% CAGR in the last 10 years with Adj. EPS jumping 20% CAGR, demonstrating the robust performance across cycles.

{kind=link}

Note: 1. Calculated using Non-GAAP accounting.

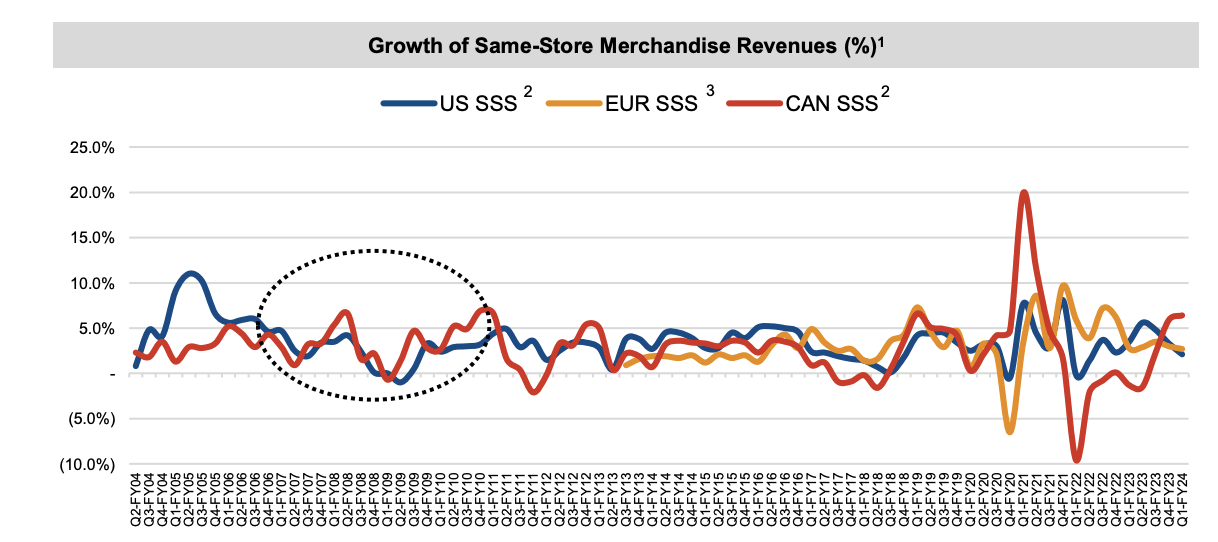

Apart from that, it has demonstrated resilient performance even during previous recessions, with stable merchandise SSS across US and Canada underlining its ability to perform even during the recessionary periods.

{kind=link}

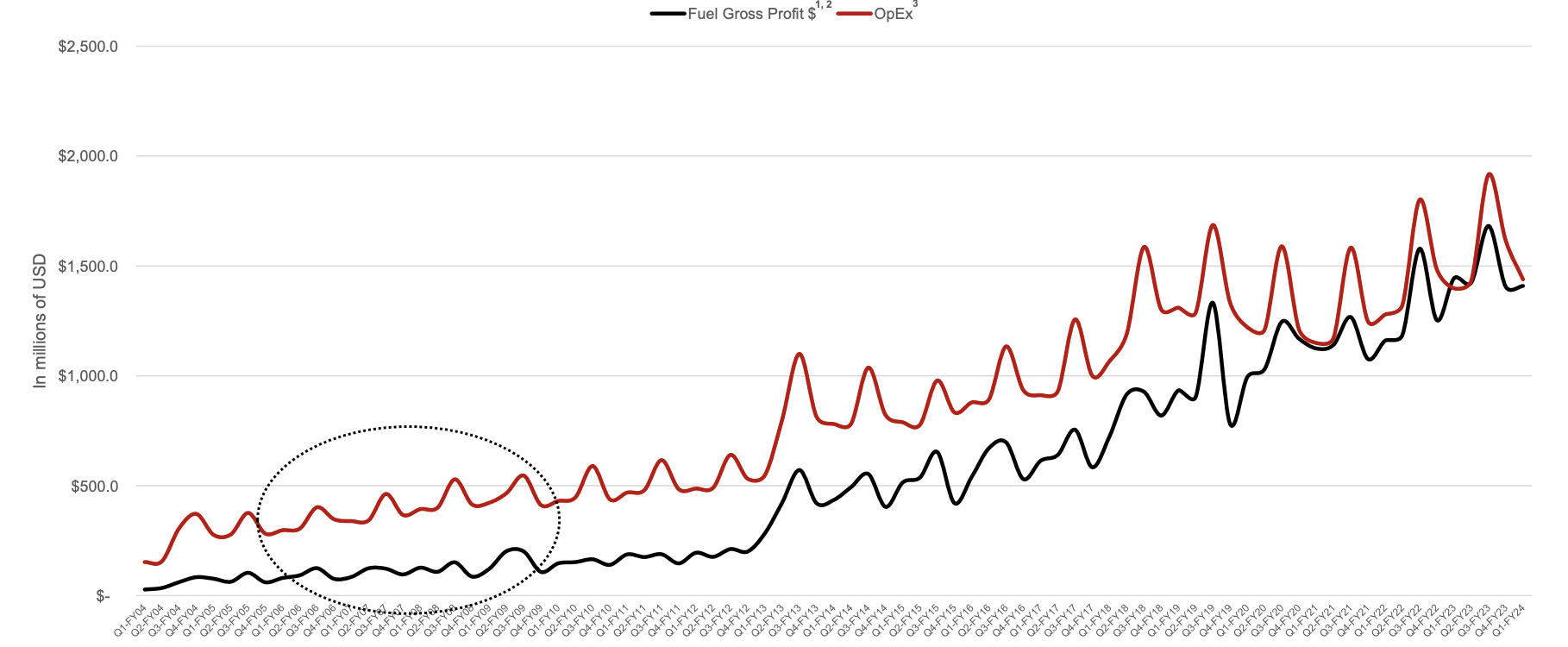

While the RTF sales volume declined during the recessionary period, it has been able to maintain or improve fuel margins, enabling them to generate sustained sales and gross profit dollars and further providing them room to sustain any opex requirements.

{kind=link}

Strong Earnings

ATD posted a strong entry into FY24 with Q1 revenues of $15.6 bn, declining 16% YoY primarily as a result of lower fuel revenues. Fuel revenues declined 21.5% YoY as a result of lower average selling price across regions. This was partially offset by same store volume sales that grew by 0.7% in the US and a robust 7.2% in Canada (due to promotional activities) while Europe volumes declined 1.5% as a result of touch macro backdrop and inflationary headwinds. Merchandise revenue increased 5.0% YoY primarily driven by a 5.6% contribution from organic growth with SSS revenues growing 2.1% in the US, 2.7% in Europe and 6.4% in Canada as a result of strong performance of its beverage, fresh foods and private brands.

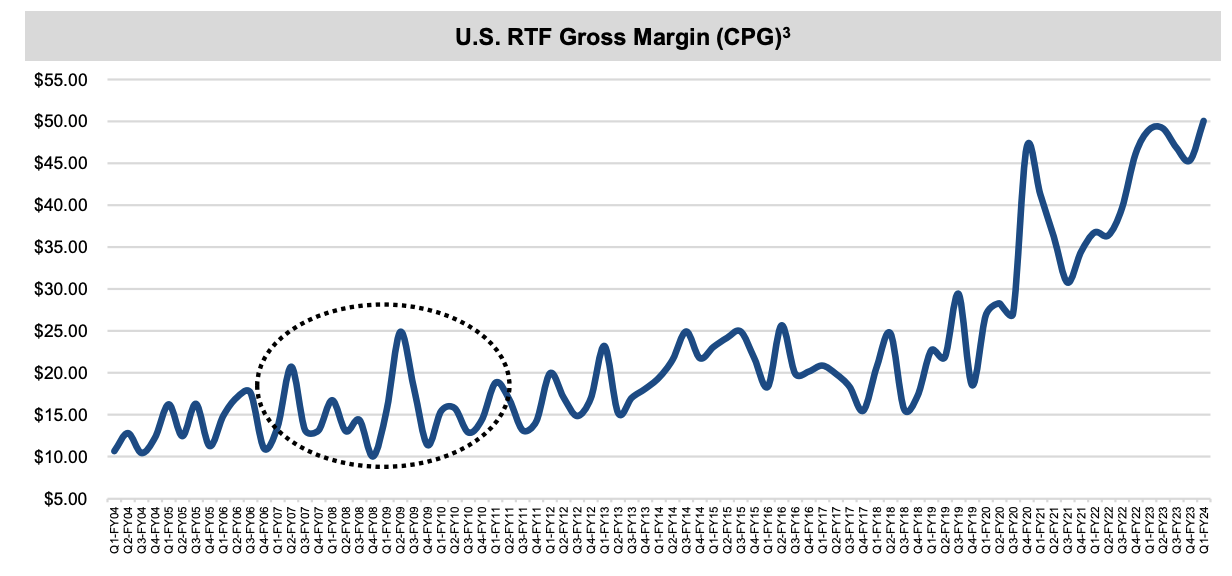

Fuel gross margins came ahead of estimates as it reported 50c/gal in the US, 8.2c/litre in Europe and CA$13.25c/litre in Canada with Europe being hit the most as a result of volatility in global fuel market and lesser hedging in the region due to its relatively more integrated supply chain. Fuel gross margins in the US remain above 40c mark for 6 straight quarters, as a result of pressure on independent stores and its improving benefits mix, which has also been resilient during the previous recession.

{kind=link}

We continue to see pressure on the industry in several fronts. Inflation is not gone. Certainly, there's some wage pressures there yet...the smaller players, rely very heavily on the tobacco category, which after a couple of years of pause during COVID, we've seen an acceleration in volume decline in that category... The bottom half of the industry (is) losing gallons to larger and more modern facilities, the pressure builds...the breakeven needs of that independent just continue to rise.

-Brian Hannasch, President and CEO, Alimentation Couche-Tard

Merchandise gross margin came in at 35%, up 60 bps YoY, as a result of margin expansion across regions driven by improving product mix, in particular within its Fresh Foods, Fast segments. Adj. EBITDA came in at $1.5 bn ahead of street estimates pegged at ~$1.38bn driven by robust gross margins. Adj. EPS came in at $0.86 beating consensus estimates of $0.78 driven by robust operating performance.

Balance sheet strength remained robust with cash balance of ~$2.0bn and comfortable leverage ratio (Net debt/ EBITDA) of just 1.4x allowing further room for acquisitions and share repurchases. It has strong cash generation ability and driven by flexible balance sheet has repurchased 4.7 mn shares in Q1 and an additional 10.8 mn shares in July out of the 49 mn shares in authorization for repurchase for the year.

Valuation

ATD trades in line with its peers, Casey's General Stores ( CASY ) and Murphy USA ( MUSA ) with valuations near historic medians. We believe the industry giants will continue to leverage on their wider network and offerings at the cost of independent retailers, and ATD is likely to benefit from further acquisitions as well as EPS accretion from repurchases. However, at current levels, we believe the risk-reward is balanced as it largely factors in the positives. This was also demonstrated by a muted share response hovering around $52 mark following the earnings announcement. We assign a target price of $56 (17x 1Y Fwd P/E). Initiate at Neutral.

Risks to Rating

1) Any significant crude oil volatility can have an outsized impact on fuel gross margins.

2) Recessionary pressure and inflationary headwinds can lead to a decline in fuel sales volume and merchandise sales as witnessed during 2023 where the company reported a decline in SSS fuel sales volume across regions.

3) Transition to EV could have an adverse impact on fuel sales volume and the company's lack of presence in the North America and negligible presence in Europe could damp growth.

3) Upside risks include share repurchases which can lead to EPS accretion and can further lead to rerating and support stock price.

Conclusion

ATD has reported strong earnings momentum and has been a beneficiary of improving fuel gross margins recently due to favorable crude prices as well as adverse impact on independents along with improving product mix. We believe its flexible balance sheet and robust cash generation ability provide them room to grow through inorganic as well as organic strategy. However, we believe the current valuation prices in most of the positives and we assign a neutral rating.

For further details see:

Alimentation Couche-Tard: Resilient But At An Unattractive Price