CA - Alimentation Couche-Tard: Slim Margin Of Safety In Its Valuation

2023-09-29 04:51:16 ET

Summary

- ATD:CA reports strong Q1 2024 results with net earnings of $834.1 million and a 1.2% increase in EPS.

- The company attributes its growth to exceptional fuel margins in the U.S. and consistent performance in Canada.

- The main issue I have with the stock is valuation as it lacks margin of safety.

Investment action

Alimentation Couche-Tard ( ATD:CA ) first quarter 2024 results reflected a strong performance. This growth is largely attributed to exceptional fuel margins in the U.S. and consistent, strong results in Canada. U.S. fuel margins reached a record due to advantageous market conditions and strategic supply chain enhancements. This was underscored by data highlighting rising gas demand and diminishing U.S. gasoline stocks, further influenced by Russia's temporary suspension of diesel and gasoline exports. Although ATD:CA’s in-store U.S. sales exhibited modest year-over-year growth, the company continues to employ strategies to ensure robust growth is retained. Although it has an impressive financial performance and the potential to excel in fuel margins that will drive growth, there's a slim margin of safety in its current valuation even with its positive outlook. I recommend a hold rating on ATD:CA's stock.

Basic Information

ATD:CA is an international convenience store conglomerate based in Canada. Recognized as one of the leading convenience store chains globally, ATD:CA provides an extensive range of products, including food, drinks, snacks, and automotive fuel. Among its various brand presences, Circle K stands out as its most prominent. Beyond its comprehensive convenience store operations, ATD:CA has a significant footprint in the fuel retail industry, supplying road transportation fuel at numerous outlets. Its operations are widespread, encompassing North America, Europe, and several other regions.

For the first quarter of 2024, net earnings stood at $834.1 million, or $0.85 per diluted share. This is in comparison to the first quarter of fiscal 2023, which saw earnings of $872.4 million, also at $0.85 per diluted share. When adjusted, the net earnings for the quarter reached around $838.0 million, slightly down from the $875.0 million of the previous fiscal year's first quarter. However, the adjusted diluted net earnings per share showcased a growth of 1.2%, moving from $0.85 in the previous year to $0.86 in the current one.

Review

ATD:CA reported a strong first quarter FY24 result. This upswing has its roots in two primary factors: the outstanding fuel margins from the U.S. market and a consistently strong performance in Canada.

A milestone for ATD:CA, the U.S. fuel margins peaked at 50.05 cents per gallon [CPG]. This record performance can be traced back to favorable market conditions and strategic improvements ATD:CA made in its supply chain. Recent data from the EIA underscores this, indicating a rise in gas demand to 8.410 million b/d in the week ending September 15th. Concurrently, US gasoline stocks decreased by 831,000 barrels. International events, such as Russia's temporary halt on diesel and gasoline exports, further exerted pressure on global fuel markets. Given these dynamics, I'm inclined to believe that ATD:CA's fuel margins will sustain higher profitability levels in the foreseeable future.

Compared to its counterparts, ATD:CA is primed to lead in terms of fuel margins. This edge is due in part to shifts in the industry landscape, especially the mounting operational costs for smaller operators. Such changes have positively affected ATD:CA's break-even margin compared to the industry's underperformers. While U.S. fuel volumes didn't quite meet predictions, ATD:CA's strategic initiatives, including Global Fuel Day and the Circle K rebranding, are contributing to a rise in volumes and diminishing cost strains.

So I think you put those things together along with some of the bottom half of the industry losing gallons to larger and more modern facilities, I think the pressure builds. So I think the breakeven needs of that independent just continue to rise. 1Q24 call

In-store sales in the U.S. witnessed modest growth of 2.1% year-over-year. However, ATD:CA remains proactive, employing strategies to retain its share in the declining cigarette market. The company's growth trajectory is also marked by its emphasis on initiatives like Fresh Food Fast, private-label offerings, and innovative beverage sales. Nonetheless, factors such as waning stimulus support and escalating fuel costs are applying pressure on consumer expenditure.

On the international front, while Canada basks in substantial growth, Europe grapples with some hurdles. Canadian in-store sales surged by 6.4%, bolstered by beverage sales and competitive fuel pricing. Europe, however, faced a 1.5% drop in fuel volumes year-over-year and an 8.21 CPL in fuel margins, challenges exacerbated by ATD:CA's intricate supply chain in the region. Additionally, sales in Europe and other regions were impacted by tax alterations in Hong Kong and comparisons with previous lockdown periods.

Valuation

I believe ATD:CA can grow at 13%. This anticipation stems from its impressive first-quarter 2024 performance, particularly its robust fuel gross margin. This margin enhancement results from both favorable market conditions and strategic supply chain enhancement made by the company, coupled with escalating fuel demand. Events like Russia's decision to momentarily suspend diesel and gasoline exports have further tightened the global fuel market, pushing prices higher. Globally, Canada's significant growth somewhat balances out the weaker sales observed in Europe. Canada’s growth was driven by beverage sales and attractive fuel prices.

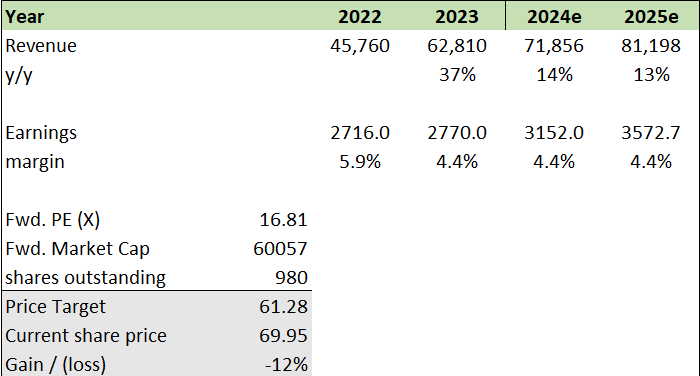

Currently, ATD:CA forward P/E is trading at 16.81x, aligning closely with its industry counterparts. In terms of EBITDA margins, ATD:CA excels beyond its peers, showcasing a margin of 8.02%, which surpasses the industry median of 6.37%. However, it's worth noting that ATD:CA's next twelve months [NTM] revenue growth rate of 6% lags slightly behind the industry median of 8%. Thus, I view its forward P/E as reasonable.

By applying ATD:CA existing forward P/E, I've calculated a target price of $61.28 for ATD:CA, which is currently below its traded price. Given the slim margin of safety, despite ATD:CA's commendable financial performance, strong in-store sales, and anticipated sustained strong fuel margins, I'd recommend a hold rating on the stock.

{kind=link}

{kind=link}

Risk and final thoughts

There are potential upside opportunities connected to ATD:CA. One positive factor stems from the stability of the global market. While ATD:CA faces challenges in specific regions, it also has the potential to benefit from stable markets in other areas. As uncertainties in Europe and other regions get addressed, and if there are increases in fuel volumes along with favorable changes in regional taxation, these developments could enhance ATD:CA's overall financial performance, resulting in share price improvements.

Another potential avenue for growth centers on further enhancements in fuel margins. If external factors like prolonged or worsening geopolitical events further disrupt the supply-demand balance, this could result in increased fuel demand, presenting an opportunity for ATD:CA to further expand their fuel margins.

In summary, ATD:CA's impressive first quarter FY24 results are driven by exceptional fuel margins in the U.S. market, consistent in-store sales in the U.S., and strong international in-store sales. ATD:CA stands out as a front-runner in fuel margins when compared to its industry peers, partly due to the evolving industry landscape and the mounting operational costs affecting smaller operators.

While U.S. in-store sales showed moderate year-over-year growth, Canada experienced thriving sales despite encountering its own set of challenges. However, it's crucial to acknowledge the impact of reduced stimulus support and the rising costs of fuel, which are squeezing consumer spending.

Looking ahead, the company appears poised for ongoing profitability, bolstered by increasing fuel demand and strategic supply chain improvements.

Considering these factors and the relatively slim margin of safety, despite ATD:CA's robust financial performance, strong in-store sales, and the anticipation of sustained strong fuel margins, I recommend a hold rating for the stock.

For further details see:

Alimentation Couche-Tard: Slim Margin Of Safety In Its Valuation