CA - Allied Properties: 50% NAV Discount But Is It Enough?

Summary

- We stayed out of Allied as the office property portfolio was unappealing despite the company having some of the best assets.

- The stock has really tumbled and is now lower than 2013 and 2016 lows.

- Valuation is now paying you to be involved, but we still are not taking a bite.

- We explain our rationale in the article.

All values are in CAD unless noted otherwise.

We wrote on the Q1-2021 financial results of Allied Properties Real Estate Investment Trust ( APYRF ) ( AP.UN:CA ) and were neutral on this predominantly office REIT's prospects. They had managed to lock in higher net rents on lease renewals, more so on their Toronto than their Calgary portfolio. On the other hand, they reported a drop in overall occupancy due to building transformations that were underway. We saw a few hurdles in its path, and that along with the high valuation made us stay away despite liking this REIT.

Going forward, Allied will get tested on two fronts. First from the work from home movement, even if it turns out to be a marginal impact. Second, from the ultra-high vacancy rate in Calgary which is now approaching 30% . Edmonton is almost as bad . Of the two, Allied is better equipped to deal with the first as its properties create a very different "feel" than the typical boxed squares. Calgary and Edmonton form under 10% of its portfolio but rents there are now under extreme duress and Allied will be challenged to roll rents over the next few years. This can be best visualized by looking at the in-place vs. market rents. Allied combines three cities here but the bulk of the square footage is from Calgary and Edmonton. There are some big gaps opening up in the next few years.

Source: Allied Properties: A Look At Q1 Results

It has not been pretty.

The third quarter results were released at the end of last month. Today, we will review those numbers and tell you why we think it is still not a bargain.

The REIT

Allied's 15 million square feet of gross leasable area or GLA comprises urban workspaces, urban data centres, retail and parking, in that order. Their Q2 presentation, while slightly dated, provides a good idea of the relative proportion of the property types held.

{kind=link}

Q2-2022 Presentation

The urban workspaces, also known as Class I workspaces, are borne out of adaptation of light industrial structures. These are modern offices that provide a cohesive work environment. They are particularly popular among companies like Google that are propelled by constant employee innovation and creativity. These Class I workspaces go a long way in keeping them engaged and turbo charged beyond the traditional 9 to 5 work hours.

{kind=link}

Allied Presentation

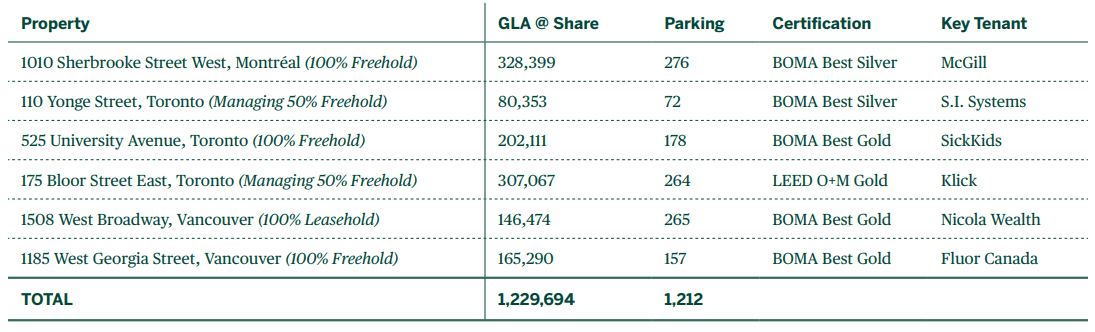

All their properties are centrally located, distinct in appearance and in major cities. While the properties predominantly reside in Toronto and Montreal, Allied does have a presence in Calgary, Edmonton, Vancouver, Kitchener and Ottawa too.

The Choice Transaction

In March of this year Allied purchased six office properties from Choice Properties Real Estate Investment Trust ( OTC:PPRQF ) for $794 million.

{kind=link}

Allied REIT

Around $594 million of the purchase price was settled via the issuance of 11.8 million Class B units at $50.30 per unit, which was the NAV at the time. The issued units are economically equivalent to the trust units. A promissory note maturing on December 31, 2023, was issued for the remaining $200 million, bearing a weighted average interest rate of 1.57%.

Q3 Results

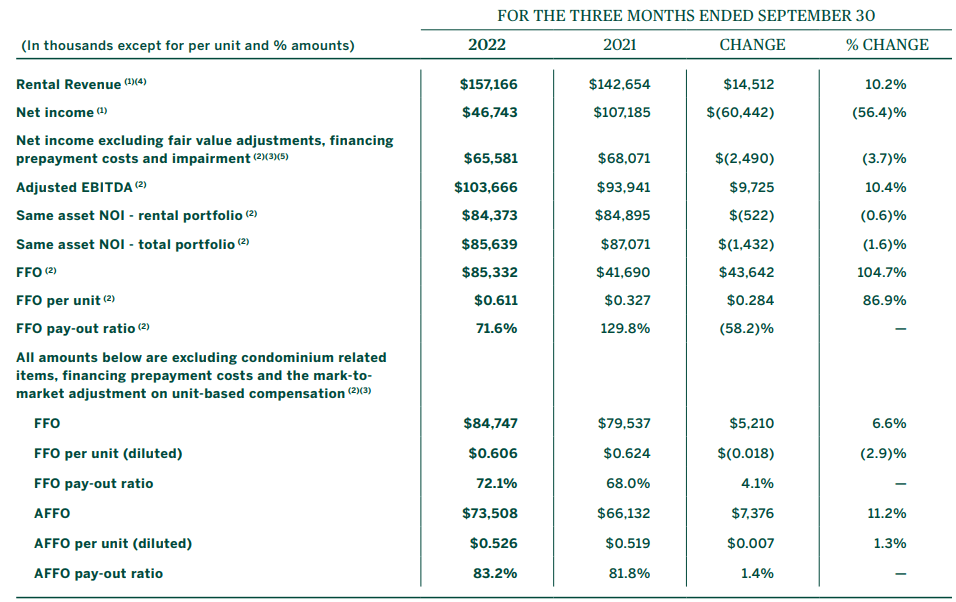

While the year over year overall NOI was up 7.2%, the same property NOI was down by 1.6%.

{kind=link}

Q3-2022 Press Release

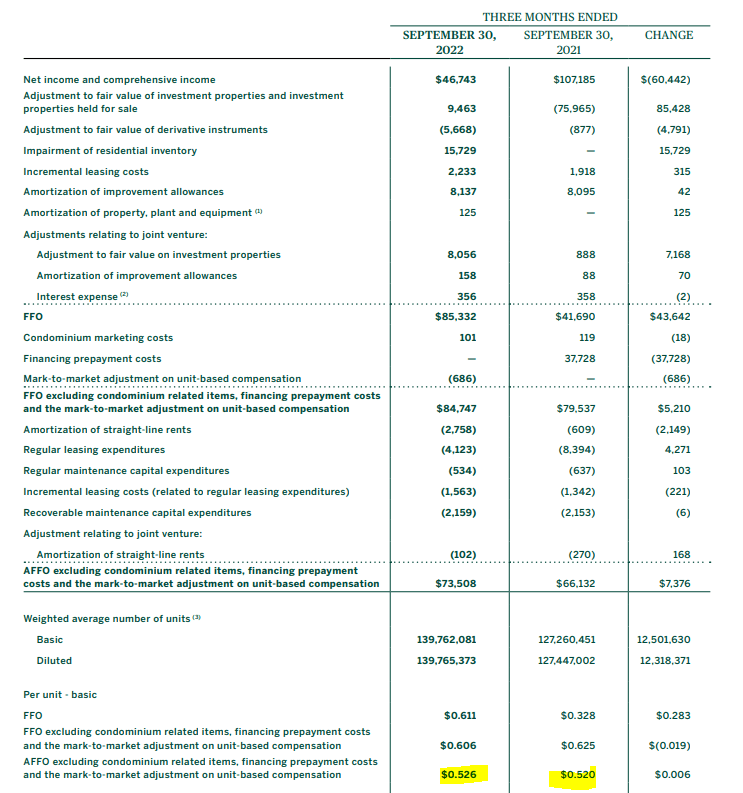

At first glance it appears the FFO went up, a lot. The FFO jump though, can be traced to a big drop in interest expense.

{kind=link}

Q3-2022 Press Release

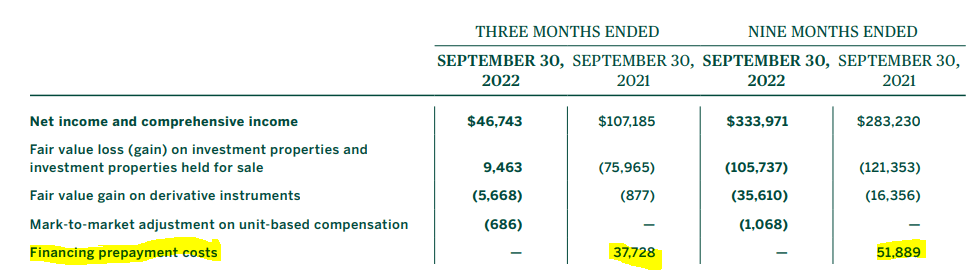

This drop came about as 2021 had a large amount of financing prepayment costs.

{kind=link}

Q3-2022 Press Release

Allied does adjust for this in their adjusted FFO and that showed a small increase year over year.

{kind=link}

Q3-2022 Press Release

The results were fine considering the massive headwinds facing the office market. Allied maintained its occupancy levels and increased rents per square foot.

{kind=link}

Q3-2022 Press Release

Outlook & Verdict

If you are a believer in the future of Canadian office properties, there is likely no better stock than Allied. The Class A unique properties have shown resilience to the downturn and the company is maintaining its FFO per share. The valuation is about as compelling as it has ever gotten for Allied. By its internal estimates, the company trades at about 50% of tangible book value. Some might argue that the number or NAV is bloated and there is certainly that possibility. Historically though, the market has valued this at 10-20% premium over the NAV.

The stock now trades at 2013 and early 2016 levels when the AFFO per share was about 35% lower. Those are good arguments for owning the company.

The arguments for not owning Allied come on a comparative basis. While it has become cheaper, we are finding that everything has become cheaper. This is certainly true when you look within the office space. Dream Office Real Estate Investment Trust ( OTC:DRETF ) ( D.UN:CA ) trades at a similar NAV discount.

It is also true across most Canadian Real Estate asset classes and we have shown Canadian Apartment Properties Real Estate Investment Trust ( CAR.UN:CA ) ( OTC:CDPYF ) as an example. So, while we see Allied as having become cheap, there is no compelling reason to pursue this asset class. Challenges remain here from higher interest rates and lease rollovers. While Calgary and Edmonton exposure is modest, it will still pressure rents going forward. Allied's equity cost has vaulted higher and at this point issuing equity so far below NAV is really not feasible. What it needs to demonstrate here is perhaps the underlying value is sound and sell assets at or above book value. This would help it complete its internal development projects without increasing debt or diluting equity. It will also help investors become more comfortable with the valuation metrics being presented for NAV. Allied remains a good choice for office exposure and we think it is a huge improvement over the yield chasing exercise that is currently being shown on True North Commercial REIT ( TNT.UN:CA ).

We see True North as actually far more vulnerable to a dividend cut, but markets are ignoring the risks there. So Allied is better than some office choices at this price point, but we are not interested in purchasing and continue to rate it as a hold/neutral.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Allied Properties: 50% NAV Discount, But Is It Enough?