SPY - Alta Fox Opportunities Fund Q3 2022 Quarterly Letter

2023-11-03 08:05:00 ET

Summary

- Alta Fox Capital is a long/short hedge fund.

- Alta Fox Opportunities Fund produced a gross return of 6.43% and a net return of 5.88% in Q3 2023.

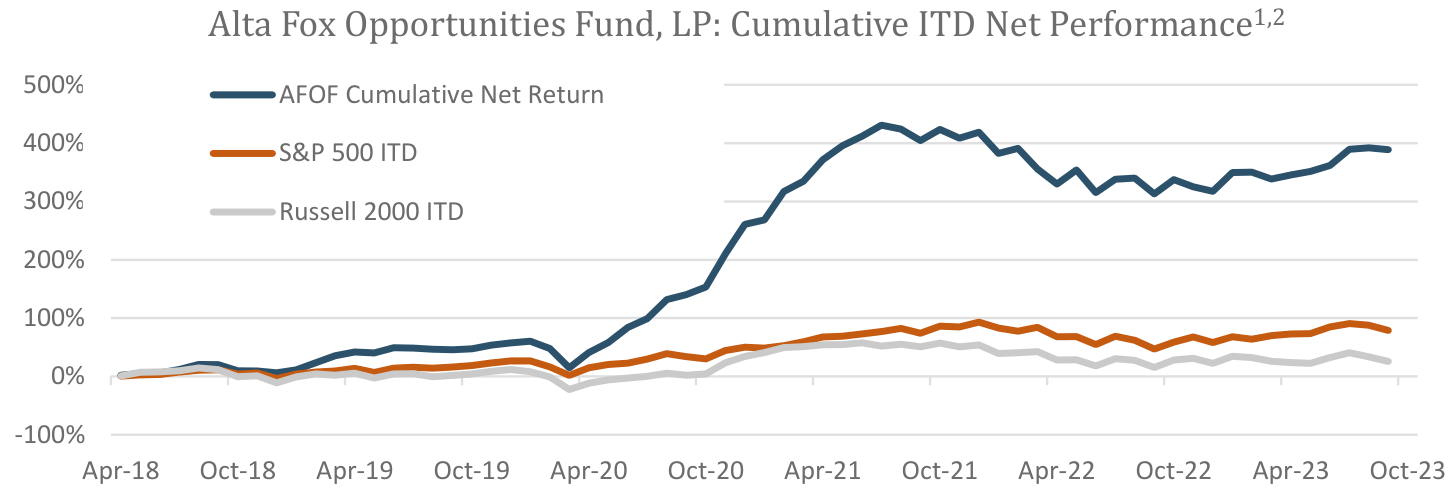

- The Fund has produced a gross return of 627.35% and a net return of 388.73% since inception in April 2018.

- The world is facing mounting geopolitical and fiscal challenges, and the Fund remains focused on its investment approach.

Limited Partners,

In Q3 2023, the Alta Fox Opportunities Fund (“the Fund” or “AFOF”) produced a gross return of 6.43% and a net return of 5.88%. The Fund’s average net exposure during the quarter was 86.43%. Since inception in April 2018, the Fund has produced a gross return of 627.35% and a net return of 388.73% compared to the S&P 500’s ( SP500 , SPX ) return of 78.75% and the Russell 2000’s ( RTY ) return of 25.63%.

| Alta Fox Opportunities Fund, LP 1 |

| Relevant Index Returns 2 |

| Gross Return |

| Net Return |

| S&P 500 ( SPY ) |

| Russell 2000 ( IWM ) |

| Q3 2023 |

| 6.43% |

| 5.88% |

| -3.27% |

| -5.13% |

| YTD |

| 18.87% |

| 17.06% |

| 13.07% |

| 2.54% |

| Since Inception |

| 627.35% |

| 388.73% |

| 78.75% |

| 25.63% |

| Annualized |

| 43.44% |

| 33.44% |

| 11.14% |

| 4.24% |

Alta Fox Opportunities Fund, LP: Cumulative ITD Net Performance 1,2

{kind=link}

| 1 Past performance is not indicative of future results. The Alta Fox Net Return figures reflect the hypothetical USD performance of an LP in the Alta Fox Opportunities Fund that has participated in all Special and Private investments, and are net of all Fund related expenses, a 2% management fee, and 20% performance fee. Net returns will vary by share class. 2023 returns are unaudited but have been verified by the Fund’s administrator. Please see the endnotes on the final page for important information with respect to the calculation of returns and indices referenced. All figures in the table above are presented as of September 30, 2023. 2 Source: Bloomberg - S&P TR (SPXT Index) and Russell 2000 (RU20INTR Index). Reference to an index does not imply that the funds will achieve returns, volatility, or other results similar to the index. Please see the endnotes on the final page for important information with respect to the calculation of returns and indices referenced. |

As always, Alta Fox strives to ignore short-term price fluctuations and instead focus on the intrinsic value growth in our portfolio holdings, which should converge with portfolio performance over time. We encourage limited partners to do the same both in times of outperformance and underperformance. We firmly believe that in the long run, our strategy of buying high-quality and underfollowed businesses at cheap prices will deliver attractive absolute and relative returns. Most importantly, our process remains disciplined with strict risk controls, minimal gross leverage, and, in our view, a sound research process.

Global Commentary

The world is facing mounting geopolitical and fiscal challenges, and we find ourselves increasingly concerned by the ineffective governments that fail to address them. The government, regardless of political affiliation, has expended taxpayer funds at a record pace, with a substantial portion being lost to fraud and waste, and missed the opportunity to refinance a ballooning debt balance at historically low rates. While there have been many 'deficit doomsdayers' throughout history who held bearish equity market views that proved incorrect, the current situation warrants heightened concern. Deficits are increasingly expensive, even if politicians would like to ignore this reality.

Witnessing the glaring government waste, corporate malfeasance, and outright fraud financed by taxpayers in response to poorly executed COVID-19 policies and programs has been deeply disheartening. According to a recent Associated Press analysis , over $280 billion of COVID-19 relief funding was misappropriated, and an additional $123 billion was squandered or misused. These staggering figures do not even account for the various instances of program abuses that, while technically complying with the law, flagrantly violated its intended spirit.

While the magnitude of COVID-19 fraud and corruption would distress any taxpayer, an even costlier government error was its inaction in refinancing U.S. debt during historically low-interest rate periods. Noted investor Stanley Druckenmiller succinctly summarized this costly oversight in a recent interview:

When interest rates were nearly zero, numerous entities refinanced their mortgages, and corporations extended their debt... except for one entity, the U.S. Treasury. Janet Yellen, possibly due to political myopia, issued two-year bonds at fifteen basis points when she could have issued ten-year bonds at seventy basis points or thirty-year bonds at one hundred and eighty basis points. I believe this was the most significant blunder in the Treasury's history, and I am baffled as to why she hasn't been held accountable for it.

As Druckenmiller highlights, the impending pain point from an interest expense standpoint is evident. Predicting the precise timing is challenging, but it is clear that the current fiscal trajectory is unsustainable. Significant reforms in entitlement spending and a reassessment of runaway deficits should not be deferred any longer, particularly in a higher interest rate environment.

Finally, the tragic events in Israel a few weeks ago have weighed heavily on our hearts. The stories of the atrocities committed are painful to read, and our deepest condolences go out to all those affected. The surge in antisemitic hate, especially within the United States, is also deeply disturbing. We firmly stand against all forms of discrimination and hate and hope for a peaceful resolution.

In the face of this challenging global backdrop, sustaining optimism becomes an arduous, but important task. We remain focused on our process and believe that current market conditions are a fertile ground for patient and diligent stock pickers.

Market Commentary

Turning to the financial markets, we continue to observe a tale of two stories. On the one hand, the large technology companies have propelled the S&P 500 to solid gains for the year. On the other hand, small-cap stocks have significantly lagged, with the Russell 2000 experiencing a notable decline year-to-date [1] . At Alta Fox, we remain steadfast in our belief that our investment approach, which involves identifying underfollowed companies early in their growth cycle at attractive valuations, will yield substantial returns over time. These companies often possess the resilience to overcome market headwinds.

In addition to our core strategy, we have expressed two key themes in our portfolio today. The first theme centers around counter-cyclical businesses that we perceive as undervalued based on their current earnings power, and we anticipate an acceleration in their fundamentals during an economic downturn. The second theme revolves around low-risk securities that offer equity-like returns while carrying significantly less risk. We provide two current examples from our portfolio below.

New Position: First Cash Holdings ( FCFS )

First Cash Holdings is a new position in the Alta Fox portfolio and is a good example of a business in our counter-cyclical theme. It is a high-quality business with an excellent track record of compounding value for shareholders at a discounted multiple to historical levels despite likely accelerating near-term fundamentals.

FCFS is the largest pawn shop operator in the fragmented US & Mexican markets and well over 2x the size of its closest competitor. At scale, pawn shops tend to be excellent businesses due to limited competition (high regulatory barriers to entry at the local level) and their unique ability to provide fully collateralized short-term financing. Current management has run this business for decades, boasting an impressive total shareholder return since IPO in 1994 of 17.5% per year vs the S&P 500 at 10.0%. [2]

We believe this is a particularly compelling time to invest in FCFS. The pawn shop industry has faced decade-long cyclical headwinds driven by low interest rates and full employment. Macro is now turning into a tailwind as dwindling consumer savings balances coupled with increasingly restrictive access to credit has significantly improved pawn shop demand. After a decade of approximately flat pawn loans outstanding per store, FCFS’s Q3 23 showed accelerating double-digit y/y growth in this metric, which hit all-time highs in the quarter. We believe this critical KPI is poised to grow significantly over the coming years and will result in earnings significantly ahead of current sell side estimates. At a historically cheap multiple of <16x NTM PE on consensus numbers that appear too conservative, we believe FCFS is well positioned to deliver attractive shareholder returns for the foreseeable future. Equally as important, the business is very defensive and can outperform in a variety of market environments.

Relative Merit of Credit Opportunities Versus Large-Cap “Generals”

Despite being small cap focused, there has always been an allocation in the Alta Fox portfolio reserved for “generals,” which are larger market caps and “best in breed” businesses. Even though the expected IRR of the generals category tends to be lower than our “gems,” they are worthy portfolio candidates due to the diversification benefit and lower risk profile. However, given the recent strength in some of these generals alongside much higher interest rates, Alta Fox is finding opportunities to produce a similar return profile with less risk via the credit market. Grupo Aeroméxico SAB is a good example of our selective approach to credit given its off the run nature, attractive yield in a high-quality business, short duration credit, and significant downside protection.

Grupo Aeroméxico SAB 8.50% 3/17/27 Secured Bonds

Alta Fox purchased secured bonds in Grupo Aeroméxico SAB, Aeroméxico, at an average cost of 90 in July 2023 (the latest price is 93/94). We believe from this basis that we could earn a 13.5% yield if bonds are refinanced one year early and 12.3% YTM [3] (11.8% and 11.0%, respectively from latest mid-point price). In our view, that risk/reward profile is attractive as it likely beats equity benchmarks from here and has significantly less risk. This opportunity exists because the bonds are an under the radar, private credit opportunity in a company that recently emerged from bankruptcy with earnings momentum and an upcoming U.S. IPO.

Aeroméxico, the flagship carrier of Mexico, filed bankruptcy on June 30, 2020, in the U.S. and exited on March 17, 2022. It is the leading Mexican airline in terms of fleet size and network. Aeroméxico is a founding member of the SkyTeam Alliance and has a strategic partnership with Delta. The company filed for bankruptcy due to struggles with COVID and used the bankruptcy process to cut costs, rationalize its fleet, extinguish debt (from over 4x pre-filing to under 2x forward EBITDAR), and renegotiate leases. In addition, low-cost peer Interjet ceased operations during COVID and liquidated. The bonds were structured during COVID to ensure over-collateralization in the event of a tepid post COVID recovery. They benefit from a strong collateral package that includes cash, the loyalty points program, real estate, jets and airline slots. It is our belief the collateral fully covers the bonds with ample excess asset coverage. The company’s business is robust, with EBITDAR surpassing chapter 11 projections. Furthermore, Mexico has been upgraded to category 1 air travel with the US allowing further earning expansion. Aeroméxico has been buying back bonds in the open market reducing the $762.5MM principal to $662.5MM ahead of a planned U.S. IPO by year end 2023 / early 2024. Our base case is redemption of the bonds at par when they go current (3/17/2026) for a current 11.8% YTM rather than at maturity (3/17/27). The bonds benefit from strong call protection, 104.25 at 3/14/24 and 102.125 at 3/17/25; providing further upside if they are called prior to 3/17/26.

Firm Updates

Our research team is headed to Cambridge, Massachusetts next week for our annual Alta Fox SmallCap Competition held on Harvard’s campus in conjunction with the Harvard Financial Analysts Club. We had a record number of submissions this year making the finalist choices particularly difficult.

Our trip is also part of a broader recruiting effort. The first open position is for our Junior Analyst Development Program Internship. We are very excited to launch this program as we believe Alta Fox can be the ideal place for passionate college students that want to jump straight to the buyside and hone their investing skills. We are creating an analyst program that I wish existed when I was graduating from school. The Junior Analyst Internship and its associated full-time role places a heavy focus on mentorship, studying the investment greats, and learning a repeatable and rigorous fundamental research process.

We are also recruiting for multiple spots in our Quantitative Internship program. We had significant success with this role last year and have multiple spots available for this upcoming summer. This internship will assist our ongoing internal data initiatives, which are progressing well and starting to generate meaningful insights for the investment team.

On a final note, Daniel Koch has embarked on a new chapter in his career and has left the firm to pursue fresh opportunities. We extend our warmest wishes for his success in his future endeavors and express our gratitude for his valuable contributions during his time with us.

Conclusion

We are enthusiastic about allocating capital today with a multi-year time horizon. The convergence of attractively priced small-cap assets, coupled with what we believe to be a diminishing competitive landscape within this specialized market, fuels our excitement.

I have heard from many investment managers that the broader fundraising environment for small cap focused funds, particularly those with a long-term view, is quite dismal. Our view is that this is reducing competition within small caps, and the strongest firms will benefit from the increasing number of attractively priced, idiosyncratic opportunities. Without reaching a critical level of assets, it is difficult to make the necessary investments in technology and team to compete effectively, not to mention the rising regulatory costs. Therefore, I believe that founding Alta Fox today would pose a greater challenge compared to when I established the firm in 2018.

We count ourselves incredibly fortunate to have exceptional Limited Partners (LPs) committed to multi-year partnerships. This has granted us the unique privilege of executing long-term strategic investments that will further fortify the fund for sustained success. Our primary commitment is to leverage this position by making meticulously considered, enduring investments-- both within our portfolio and in talent acquisition.

We are humbled that you have elected to invest a portion of your assets with Alta Fox. We continue to strive to improve all aspects of our research and operational processes in our pursuit of building a world-class investment firm.

Sincerely,

Connor Haley

Appendix: Historical Performance Figures

| Alta Fox Gross Return 1 |

| Alta Fox Net Return 2 |

| Alta Fox Net Exposure (Avg) |

| Q2-2018 |

| 7.82% |

| 5.85% |

| 79.31% |

| Q3-2018 |

| 17.12% |

| 13.46% |

| 85.44% |

| Q4-2018 |

| -13.57% |

| -11.72% |

| 77.23% |

| 2018 |

| 9.14% |

| 6.02% |

| 80.66% |

| Q1-2019 |

| 35.41% |

| 27.87% |

| 83.00% |

| Q2-2019 |

| 12.39% |

| 10.01% |

| 83.45% |

| Q3-2019 |

| -2.20% |

| -2.32% |

| 79.07% |

| Q4-2019 |

| 9.96% |

| 8.07% |

| 77.86% |

| 2019 |

| 63.65% |

| 48.50% |

| 80.84% |

| Q1-2020 |

| -26.77% |

| -27.19% |

| 75.12% |

| Q2-2020 |

| 66.65% |

| 60.31% |

| 75.17% |

| Q3-2020 |

| 37.37% |

| 30.68% |

| 85.35% |

| Q4-2020 |

| 58.32% |

| 50.14% |

| 85.86% |

| 2020 |

| 165.41% |

| 129.03% |

| 80.37% |

| Q1-2021 |

| 26.24% |

| 20.56% |

| 93.70% |

| Q2-2021 |

| 21.75% |

| 17.70% |

| 83.75% |

| Q3-2021 |

| -0.91% |

| -1.43% |

| 75.58% |

| Q4-2021 |

| 3.81% |

| 2.82% |

| 76.48% |

| 2021 |

| 58.11% |

| 43.82% |

| 82.38% |

| Q1-2022 |

| -11.71% |

| -12.13% |

| 79.83% |

| Q2-2022 |

| -8.46% |

| -8.89% |

| 73.18% |

| Q3-2022 |

| 0.11% |

| -0.55% |

| 54.23% |

| Q4-2022 |

| 0.92% |

| 1.10% |

| 58.97% |

| 2022 |

| -18.35% |

| -19.50% |

| 66.55% |

| Q1-2023 |

| 5.56% |

| 5.04% |

| 56.55% |

| Q2-2023 |

| 5.80% |

| 5.26% |

| 71.36% |

| Q3-2023 |

| 6.43% |

| 5.88% |

| 86.43% |

| YTD 2023 |

| 18.87% |

| 17.06% |

| 71.45% |

| 1 The Alta Fox Opportunities Fund’s Gross Return (“Alta Fox Gross Return”) reflects the USD investment performance of a share class subject to all Fund related expenses but are gross of any management fee and performance fee. 2023 returns are unaudited but have been verified by the Fund’s administrator. Past performance is not indicative of future results. Actual returns may differ from the returns presented. References to net exposure and attribution data are internally calculated estimates and could be subject to errors. 2 The Alta Fox Opportunities Fund’s Net Return figures (“Alta Fox Net Return”) reflect the hypothetical USD investment performance of an LP in the Alta Fox Opportunities Fund that has participated in all Special and Private investments, and are net of all Fund related expenses, a 2% management fee, and 20% performance fee. Net returns will vary by share class. 2023 returns are unaudited but have been verified by the Fund’s administrator. Each partner will receive individual statements showing returns from the Partnerships’ administrator. |

Footnotes[1] The decline year to date is at the time of writing (10/31/2023), not as of the end of Q3 2023 [2] Source: Bloomberg. Total shareholder return data from 12/30/1994-10/31/2023 [3] This does not represent an actual IRR; this is a hypothetical return figure that would be less on a net basis for a hypothetical investor of Alta Fox Opportunities Fund, LP. The annualized net IRR would be approximately 10.5% and 9.7% respectively assuming a pro rata 2% management fee, 20% performance fee and a pro rata 0.50% for fund-related expenses. Actual net returns will vary by share class and individual investor’s subscription timing. DisclaimerAlta Fox Capital Management, LLC (“Alta Fox”) is an investment adviser to funds that are in the business of buying and selling securities and other financial instruments. This information is provided for informational purposes only and does not constitute investment advice or an offer or solicitation to buy or sell an interest in a private fund or any other security. An offer or solicitation of an investment in a private fund will only be made to accredited investors pursuant to a private placement memorandum and associated documents. Alta Fox may change its views about or its investment positions in any of the securities mentioned in this document at any time, for any reason or no reason. Alta Fox may buy, sell, or otherwise change the form or substance of any of its investments. Alta Fox disclaims any obligation to notify the market of any such changes. The Alta Fox Opportunities Fund’s Net Return figures (“Alta Fox Net Return”) reflect the hypothetical USD investment performance of an LP in the Alta Fox Opportunities Fund that has participated in all Special and Private investments, and are net of all Fund related expenses, a 2% management fee, and 20% performance fee. Net returns will vary by share class. 2023 returns are unaudited but have been verified by the Fund’s administrator. Each partner will receive individual statements showing returns from the Partnerships’ administrator. The Alta Fox Opportunities Fund’s Gross Return figures (“Alta Fox Gross Return”) reflect the USD investment performance of a share class subject to all Fund related expenses but are gross of any management fee and performance fee. 2023 performance returns are estimated pending the year-end audit. Past performance is not indicative of future results. Actual returns may differ from the returns presented. References to net exposure and attribution data are internally calculated estimates and could be subject to errors. The S&P 500 and Russell 2000 are U.S. equity indices. The S&P 500 Index is one of the most commonly used benchmarks for the overall U.S. stock market, and it tracks the average performance of 500 widely held stocks including industrial, transportation, financial, and utility stocks. The composition of the S&P 500 is flexible and the number of issues in each sector varies over time. Since the Fund invests across a wide universe of companies and stocks, we provide the S&P 500’s returns as a measure for investors to compare the Fund’s returns to broader market performance. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 is a subset of the Russell 3000 Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000 is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true smallcap opportunity set. Since Alta Fox’s research process typically leads us to opportunities in the smallcap space, we provide the Russell 2000’s returns as a measure for investors to compare the Fund’s returns to broader small-cap performance. These indices’ returns are included for informational and comparative purposes only and may not be representative of the type of investments made by the Fund. Reference to an index does not imply that the Fund will achieve returns, volatility, or other results similar to the index. The Fund’s portfolios are less diversified than these indices. These indices’ returns are total returns which include dividends and do not reflect the deduction of any fees or expenses which would reduce returns. An investment in the Fund/partnership is speculative and involves a high degree of risk. Opportunities for withdrawal/redemption and transferability of interests are restricted, so investors may not have access to capital when it is needed. There is no secondary market for the interests, and none is expected to develop. The portfolio is under the sole trading authority of the general partner. A portion of the trades executed may take place on non-U.S. exchanges. Leverage may be employed in the portfolio, which can make investment performance volatile. An investor should not make an investment unless the investor is prepared to lose all or a substantial portion of its investment. The fees and expenses charged in connection with this investment may be higher than the fees and expenses of other investment alternatives and may offset profits. The enclosed material is confidential and not to be reproduced or redistributed in whole or in part without the prior written consent of Alta Fox. The information in this material is only current as of the date indicated and may be superseded by subsequent market events or for other reasons. Statements concerning financial market trends are based on current market conditions, which are uncertain and outside of Alta Fox’s control. Any statements of opinion constitute only current opinions of Alta Fox which are subject to change and which Alta Fox does not undertake to update. Due to, among other things, the volatile nature of the markets, and an investment in the fund/partnership may only be suitable for certain investors. Parties should independently investigate any investment strategy or manager, and should consult with qualified investment, legal and tax professionals before making any investment. The fund/partnership is not registered under the investment company act of 1940, as amended, in reliance on an exemption thereunder. Interests in the fund/partnership have not been registered under the securities act of 1933, as amended, or the securities laws of any state and are being offered and sold in reliance on exemptions from the registration requirements of said act and laws. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Alta Fox Opportunities Fund Q3 2022 Quarterly Letter