CA - Altria: Poor Q4 2022 Results Show Why Glory Days Are Not Coming Back

Summary

- Altria Group, Inc. reported Q4 2022 results that beat earnings estimates, though revenues fell a bit short.

- The stock appears cheap with a low P/E and big yield, and Altria Group, Inc. has a distinguished history.

- The Altria Group, Inc. results, though, look extremely poor from one angle, and we would only be interested in purchasing the stock lower.

When we last covered Altria Group, Inc. ( MO ), we had the opinion that it could be safely purchased only at a lower price and pointed out the key risk factor.

A moment will come where price hikes will accelerate declines and that will only be apparent with hindsight. In fact, looking at the last 12-18 months suggests that we might actually be at that point or even past that point. We maintain a cautious outlook and bulls might suddenly be greeted to a few quarters where price hikes fail to actually offset volume declines. In that case the numbers below may look too optimistic.

Source: Altria Earnings Estimates Look Optimistic .

Since then, Altria has trailed both the S&P 500 (SP500) and the Consumer Staples Sector ( XLP ), by a small margin and validated our decision to stay out.

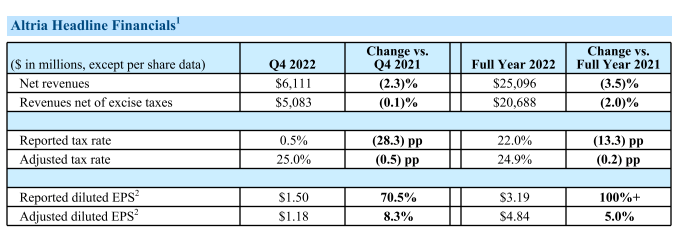

Altria Group, Inc. just reported Q4-2022 results beat earnings estimates slightly but came up short on revenues by a bit. We examined the numbers to see if our thesis was playing out as we envisioned.

Q4-2022

If you wanted growth in earnings per share, you got it. Q4-2022 adjusted earnings were up 8.3% and full year numbers were up 5%.

{kind=link}

Altria did report a rather rare quarter and year where revenues declined. In favor of the bulls was the fact that net of excise taxes, revenues were down just 0.1%. Still, it underscores the fact that Altria is struggling to grow its revenues. This is happening in a high-inflation era, which normally is supportive of nominal revenue increases.

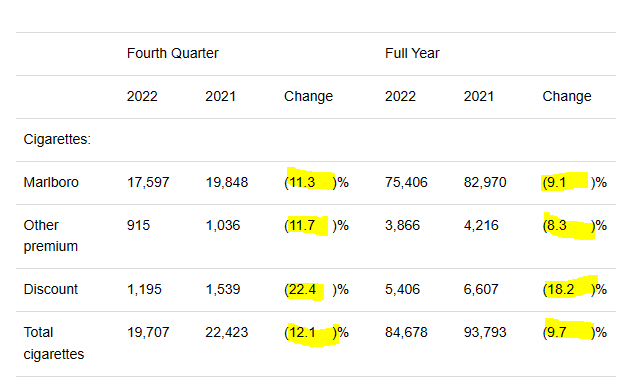

The key reason for this was that stick volumes continue to fall off the proverbial cliff. Altria presents this via three different numbers.

Smokeable products segment reported domestic cigarette shipment volume decreased 12.1% , primarily driven by the industry’s decline rate and retail share losses (both of which were impacted by macroeconomic pressures on ATC disposable income) and calendar differences.

When adjusted for calendar differences, smokeable products segment domestic cigarette shipment volume decreased by an estimated 11% .

When adjusted for trade inventory movements, calendar differences and other factors, total estimated domestic cigarette industry volume decreased by an estimated 9% .

Source: Altria Q4-2022 Press Release (emphasis added).

In our opinion, the middle one showing the decline of 11% is the most relevant. Our rationale is that calendar differences should be adjusted for, but trade inventory movements should be ignored. If you accept the idea Altria's cigarette volumes have a date with zero at some point, and there is nothing in the last 5 years that provides evidence otherwise, then you have to accept that all retailers will carry far lower inventories over time. So trade inventory movements will generally make the declines look worse, but that should not be adjusted for. It is not like Altria can suddenly reverse this secular decline or force everyone to carry more inventory. Altria's chronic price increases have pretty much maximized incentives for everyone to hoard as much as they can. If after that, inventories stocked keep declining, there is nothing that can be done about it.

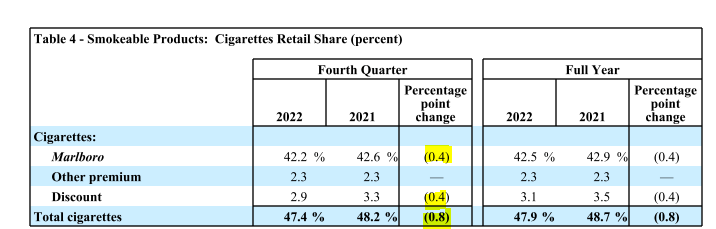

Getting back, these declines do need to be seen in detail to truly understand the speed at which things are falling apart. Even within the year itself, fourth quarter was the worst. The discount segment was down almost by one quarter in Q4-2022.

{kind=link}

Total cigarettes run rate (Q4 annualized) was 78,828 million in Q4-2022. That means that the fourth quarter annualized itself was 7% below the whole year's 84,678 million number. That is a breathtaking (pardon the pun) decline. Compare that 78,828 Q4-2022 run rate with the numbers from 2015 (Source 10-K from 2017 ). That is a 37.5% drop. The discount segment is already 57% below 2015 levels (Q4-2022, 1,195 million annualized).

2017 10-K

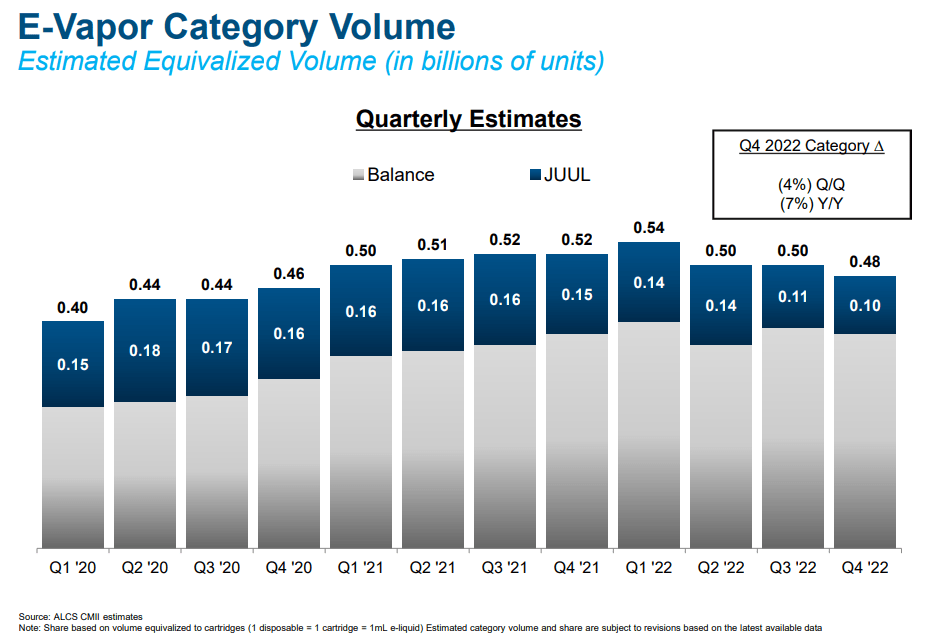

Moving on from cigarettes, we saw that the much hyped JUUL ( JUUL ) investment continued to be a disappointment. The E-vapor fad appeared to be fading, and even that showed a solid decline in volumes.

{kind=link}

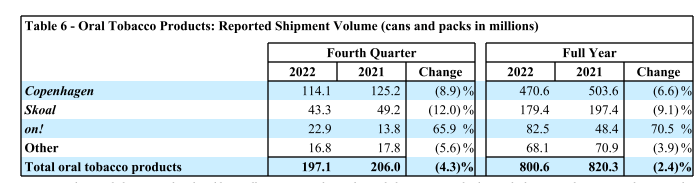

Finally, in the oral tobacco segment, volumes and revenues declined by similar amounts, as Altria did not try and offset volume declines with huge price hikes.

{kind=link}

Valuation & Verdict

On one hand, there is that lofty dividend that dwarfs most others that you can find today. On the other, there is the certainty that some day the math will come to bite and the last smoker standing (figuratively) won't pay for all those dividends. For a moment, just forget about percentages. Assume that the volume decline from Q4-2021 to Q4-2022 stays constant every year.

Altria Q4-2022 Press Release

In that scenario, volumes go to zero in under 8 years. Some might argue that this is never going to happen but every indicator suggests that these trends have so far accelerated. Whatever price hikes were done to offset these declines will have to be higher and higher if these trends persist. That's the math. Even without big price hikes having a negative feedback loop, we see this as a problematic investment. When feedback loops kick in, you will have big problems.

The final issue is what happens when cigarette companies start competing on price. So far, that has not been the case. Altria was happy to lose market share to preserve its revenues.

{kind=link}

If competitors start aggressively undercutting Altria, it may start to lose market share more rapidly in a declining industry. With these things in mind, you generally want to max out at paying 7-8X earnings for a company like this. With $5.00 in earnings expected, the maximum we would be interested in paying would be the $35.00-$40.00 range. Investors might have wondered why we have not given it credit for the equity investments that Altria has, including those in Anheuser-Busch InBev SA/NV ( BUD ) and Cronos Group Inc. ( CRON ). The rationale is very simple. These investments are dwarfed by the total debt and other liabilities outstanding.

Altria Q4-2022 Press Release

The fact that Altria Group, Inc. has a net debt amount outstanding (defined here as total liabilities less current assets and equity investments) is a negative for such a rapidly declining user base. We would use extreme caution in chasing this yield. The past is not the future. While the market may celebrate the Altria Group, Inc. "beat," we would focus on the long-term trend, and it is not your friend.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Altria: Poor Q4 2022 Results Show Why Glory Days Are Not Coming Back