NVDA - AMD: The Road To $190 By 2025

2023-11-27 11:52:44 ET

Summary

- Advanced Micro Devices, Inc. showcased significant growth in Q3, outperforming competitors like Nvidia with a 350% increase in year-over-year diluted EPS.

- Strategic acquisitions and partnerships, such as with Microsoft Azure, have bolstered AMD's market leadership in AI and cloud computing.

- Despite declines in gaming and embedded segments, AMD forecasts a 9% YoY revenue increase for Q4 2023, banking on data center and client segment performance.

- AMD's stock exhibits bullish momentum, potentially targeting $190 by 2025, contingent upon sustained financial progress and Supertrend indicator patterns.

Investment Thesis

In Q3 2023 , Advanced Micro Devices, Inc. ( AMD ) showcased significant growth across all segments, outperforming competitors like Nvidia Corporation ( NVDA ) with a 350% increase in year-over-year diluted EPS. From a technical standpoint, AMD's stock has displayed a bullish trend since early 2023, with projections suggesting a potential rise to nearly ~$190 by 2025 , as per the Elliott Wave Theory. This optimistic stock trajectory reflects AMD's robust financial performance and strategic advancements in key technological areas.

Surpassing Nvidia with Stellar Growth in Key Segments

In Q3 2023, AMD has demonstrated top-to-bottom growth both year-over-year and sequentially. Following our previous coverage , profitability, and collective growth in all segments were major hurdles. This collective growth reduced the downside risk on the stock’s market valuation by improving the performance prospect of AMD against Nvidia, leading to year-over-year growth in diluted EPS of 350% against Nvidia’s 1274% .

To begin with, AMD's Data Center segment surged impressively in Q3, reporting revenue marking a significant 21% sequential increase. This considerable growth was primarily propelled by the adoption of 4th generation EPYC processors, resulting in record-breaking quarterly server processor revenue. Therefore, this growth was partially offset by a decline in adaptive system-on-chip (SoC) product sales.

Looking at the bottom line, the segment delivered an operating margin of 19% , +108% sequentially (down from 31% in Q3 2022), but the decline is primarily based on increased investments to boost AI revenue growth and product mix, which is a favorable fundamental in competition with Nvidia and Intel Corporation ( INTC ). Looking at the progress in these segments, nearly 100 new cloud instances were created with major tech giants.

Earnings Presentation

The company's projection of data center GPU revenue exceeding $2 billion by 2024 suggests substantial growth. This accelerated revenue forecast hinges mainly on AI-centric solutions, with the upcoming MI300 GPUs expected to gain traction throughout the year based on their capability to cater to various AI workloads across multiple industries. Notably, the impending launch of Turin server processors based on the Zen 5 core has generated positive feedback, promising significant performance and efficiency enhancements set for a 2024 release.

Further, AMD's Client segment demonstrated remarkable growth with a 42% year-over-year revenue surge and 638% year-over-year growth in operating margin. This surge was predominantly driven by heightened demand and increased sales of Ryzen mobile processors, contributing significantly to the segment's robust 46% sequential revenue increase. The segment may continue to experience tailwinds with the launch of the first Threadripper PRO workstation CPUs, with quick adoption by Dell ( DELL ), HP ( HPQ ), and Lenovo ( LNVGY ).

While the gaming segment faced an 8% year-over-year revenue decline to $1.5 billion due to reduced semi-custom revenue, increased sales of Radeon GPUs partially offset this decline. The 5% sequential decrease aligned with the anticipated stage of the console cycle.

On the other hand, the embedded segment experienced a 5% year-over-year revenue decline, totaling $1.2 billion. This decline was attributed to normalized lead times and customer inventory reduction efforts. However, the company's strategic focus on expanding the Versal SoC portfolio, particularly adaptive SoCs with HBM memory, reflects a targeted approach to address specific market needs and opportunities.

Finally, based on these developments, the company's fourth-quarter revenue outlook anticipates $6.1 billion in revenue, implying a 9% year-over-year increase and a 5% sequential increase. Thus, this growth projection aligns with the expected strong performance in the data center and client segments.

Earnings Presentation

Strategic Acquisitions and Microsoft Azure Partnership Propel Market Leadership

Following the previous coverage, the strategic acquisitions of Mipsology and Nod.ai have bolstered AMD's AI software capabilities significantly. These acquisitions aim to accelerate the deployment of high-performance AI models optimized for diverse AMD processors, enhancing the company's positioning in AI-focused markets. AMD's foray into AI involves various aspects, including hardware development, strategic partnerships, and software integrations.

AMD's collaboration with Microsoft Corporation's Azure suggests a major stride in the AI business. The introduction of the AMD Instinct MI300X accelerator within the Azure ecosystem cements AMD's focus on enhancing AI capabilities in the cloud. The partnership demonstrates their willingness to integrate cutting-edge AI hardware into a leading cloud platform. Thus, the MI300X's inclusion in Microsoft's Azure ND MI300x v5 VM series marks a significant milestone.

This partnership reflects AMD's strategy of aligning with major cloud service providers to ensure their hardware accelerators, such as the Instinct MI300X, are integrated seamlessly into cloud infrastructures. This integration aims to democratize access to AI capabilities for enterprises and developers while ensuring scalability and efficiency in cloud-based AI processing.

In the context of cloud business, the utilization of 4th Gen AMD EPYC processors in Microsoft's new generation of virtual machines (VMs) underlines the substantial performance improvements AMD's server-grade CPUs brought about. Compared to the previous generation, the up to 20% better performance for general-purpose and memory-intensive VMs and up to 2x CPU performance for compute-optimized VMs demonstrates a leap in computational efficiency.

In simple terms, think of these processors as being super-efficient librarians. They can quickly find and deliver information (up to 5.7 terabytes per second). This is way faster than regular memory in a computer, which can handle about 780 gigabytes per second. Because of this unique feature, these computers can work with an average speed of 1.2 terabytes per second, which is fast for many different types of jobs they are asked to do.

azure.microsoft.com

AMD's Ryzen AI Unleashes Cutting-Edge Capabilities for Consumers

To capture the AI market, Ryzen AI for PCs represents AMD's focus on integrating AI capabilities into consumer devices, as their Ryzen AI initiative exemplifies. The Ryzen 7000 Series processors equipped with Ryzen AI demonstrate AMD's focus on embedding AI capabilities directly onto x86 processors. With a significant number of systems already featuring Ryzen 7000 Series processors equipped with Ryzen AI, AMD has effectively made millions of AI-enabled PCs available on the market.

At the ground level, collaborations with software developers, such as the joint effort with Microsoft to enable Windows Studio Effects on Ryzen AI PCs, showcase AMD's proactive approach to expanding AI workloads and generative AI experiences for consumers. Lastly, integrating AI directly into CPUs highlights AMD's strategy to provide consumers with enhanced AI performance without needing additional specialized hardware, thus democratizing AI capabilities in personal computing and leading the AI PC market.

www.canalys.com

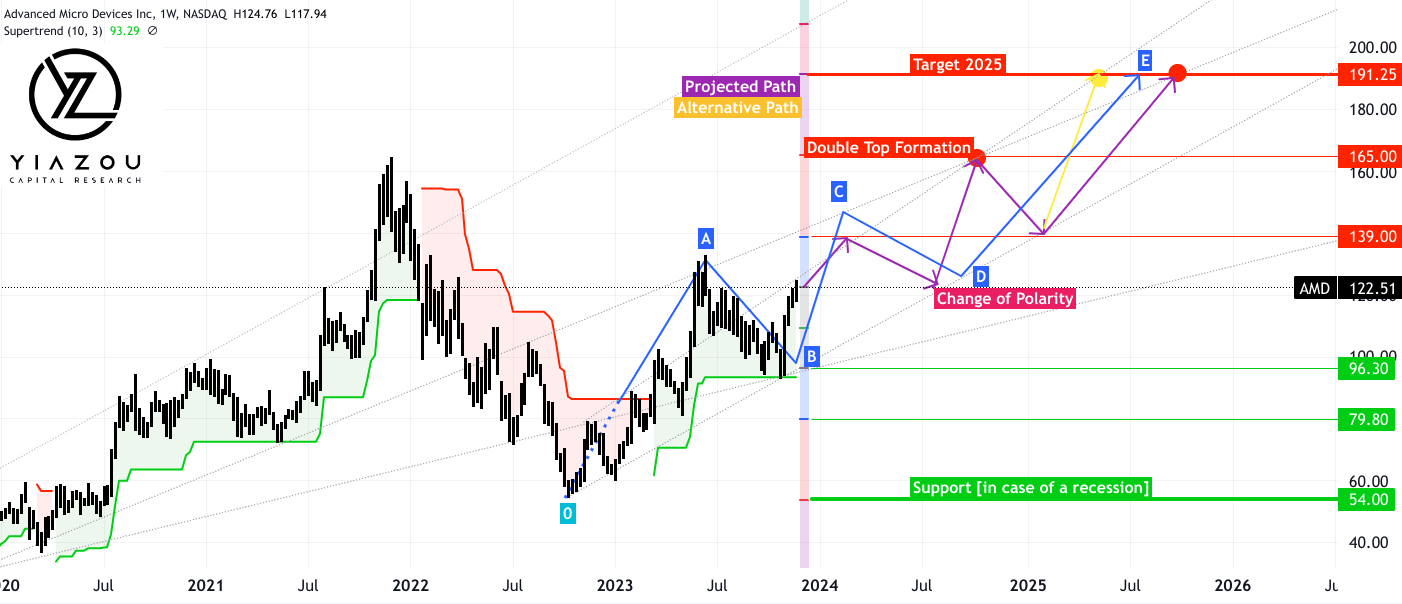

Technical View: The Bullish Momentum Has Just Begun

The stock price of AMD gained long-term support at the beginning of 2023 and has followed a bullish trajectory since March 2023, as confirmed by the Supertrend indicator. Looking at the downside, in the event of any adverse development like a recession, $80 may be a vital support level . In cases of volatility, however, $54 presents a critical accumulation level if the price drops under heightened volatility.

Projecting at the ongoing uptrend, $122.50 is a weak resistance, and the stock price may provide a proper close over this level. However, the price may experience considerable resistance at $139 , pushing it down to $122.50 to retest it as support and establish a change in polarity. Following the trend lines over the mid-term may lead the stock to hit $165, whereas a double top formation may pressurize the price to retest $139 as support.

Ultimately, by 2025, the stock price may reach nearly ~$190 (see projected path) to complete the last impulsive wave (under Elliott Wave Theory, see blue line) if AMD fundamentally keeps its financial performance progressive in the current state. Lastly, the Supertrend indicator may be a navigator to manage the position over the medium term.

{kind=link}

Takeaway

In conclusion, AMD's performance in Q3 2023 marked a significant milestone, showcasing a comprehensive growth trajectory across all its business segments. The company's successful navigation in the competitive landscape, notably against Nvidia, reflects its strong market positioning.

The strategic moves in AI, through acquisitions and partnerships like with Microsoft Azure, have further solidified AMD's standing in the tech industry. The bullish trend in AMD's stock price, backed by solid financials and strategic advancements, points towards a promising future.

With projections of the stock potentially reaching around $190 by 2025, AMD stands out as a compelling investment opportunity, leveraging its advancements in AI, cloud computing, and semiconductor technologies. This combination of technical innovation and financial acumen positions AMD as a leader in the evolving landscape of technology and computing.

For further details see:

AMD: The Road To $190 By 2025