ETR - Ameren: This Utility Is A Good Stock To Accumulate Today

2023-06-21 18:26:49 ET

Summary

- Ameren Corporation is a regulated electric and natural gas utility that serves much of the states of Illinois and Missouri.

- The electric utility business is much larger than the natural gas one, which removes some of the seasonality from the company's cash flows.

- The company has an ambitious growth capital investment program that should allow it to deliver a 9% to 11% total return annually.

- The company has a reasonably strong balance sheet with less debt than its peers.

- Ameren Corporation has a reasonable valuation today and could be worth accumulating.

Ameren Corporation ( AEE ) is an American regulated electric and natural gas utility that provides services to much of Illinois and Missouri. The company does not provide service to Chicago, however. The utility sector has long been one of the favorite sectors for conservative risk-averse investors, especially retirees. There are a few good reasons for this, including the fact that most electric utilities enjoy remarkably stable cash flows that are largely independent of fluctuations in the economic environment. This is a quality that could be very desirable right now, as the near-term future of the economy is rather uncertain.

Ameren has historically also boasted a fairly high dividend yield, which today sits at 3.04%. That is much higher than the yield of the S&P 500 Index (SP500) and the company's penchant for increasing it regularly means that the effective yield on cash that an investor receives will be considerably higher after holding the stock for a few years. Ameren also has an attractive valuation at the current price, which is always nice to see.

Admittedly, this thesis is pretty similar to the one that I presented the last time that I discussed this company, but that was a few months ago so a few things have changed. Therefore, let us revisit our thesis and see if it makes sense to continue accumulating shares today.

About Ameren Corporation

As stated in the introduction, Ameren Corporation is a regulated electric and natural gas utility that serves most of the state of Illinois, other than Chicago. The company also serves the city of St. Louis, Missouri, and the surrounding area:

Ameren Corporation

In addition to its electric utility services, the company provides natural gas service to homes and businesses within parts of its service territory. Its natural gas business is somewhat smaller, however. This is evidenced by the fact that the company only has 900,000 natural gas customers compared to approximately 2.4 million electric customers. This is something that may be attractive to some investors.

Over the past few years, politicians and others in the media have been making claims about how natural gas will soon become obsolete as people convert to electricity for all of their energy needs. This claim is completely nonsensical because natural gas is much more economically sensible as a source of heat. I explained this in several previous articles (see here and here ). In short, natural gas is more efficient at creating heat than electricity so it is cheaper to use for such purposes. That is almost certainly going to be a very important consideration for people of limited means, who are very unlikely to spend a considerable amount of money to convert a space heating system to electricity from natural gas only to have their heating bills go up.

With that said, electric utilities do tend to be more stable financially from quarter to quarter. This is because electric consumption does not exhibit the seasonal variation that natural gas does. While we do see higher electric usage and bills during the summer months due to air conditioner use, not all homes have air conditioners and households continue to use electricity during the cooler winter months. As such, while bills do vary somewhat, electric utilities tend to have very stable quarterly revenue and cash flows. This extends somewhat to Ameren Corporation, as its electric utility accounts for more than double the customer base of its natural gas utility. Here are the company's quarterly operating cash flows for each of the past eleven quarters:

{kind=link}

We do still see some fluctuations, but for the most part, the company's cash flows are usually between $400 and $750 million during each and every quarter. This is much less variation than we see with a pureplay natural gas utility like ONE Gas, Inc. ( OGS ), which I discussed yesterday. We also see that the COVID-19 pandemic, the raging inflation of 2021, and the weakening economy from the rising interest rates that started in 2022 had no real impact on Ameren Corporation's cash flows. This provides evidence for the point that I have been making about the company's cash flow stability and resistance to economic events.

The reason for this overall stability should be pretty obvious. Ameren provides a product that is typically considered to be a necessity for this day and age. After all, how many homes do not have electric service and heat for cold days? Due to this necessity status, most people will prioritize paying their utility bills ahead of discretionary spending during times when money gets tight. As I pointed out in a recent blog post , the high inflation that has been plaguing the economy has made money very tight for the average American household as evidenced by the fact that revolving credit card debt is near record levels and the savings that were built up during the pandemic have largely been drained. If economists are right and a recession does hit during the second half of the year, household finances will probably get even tighter if the recession results in layoffs.

In fact, we are already seeing this, as FedEx ( FDX ) is in the process of laying people off and closing down stores, and the technology sector has laid off more than 210,000 people since January 1. In such an economy, it can help anyone sleep well at night if at least part of their portfolio is invested in companies that are unlikely to be affected by a weakening economy. Ameren appears to be an excellent candidate for such a role.

Growth Prospects

Naturally, as investors, we are unlikely to be satisfied with mere stability. After all, we like to see a company that we are invested in grow and prosper with the passage of time. Fortunately, Ameren Corporation is well-positioned to deliver on that goal.

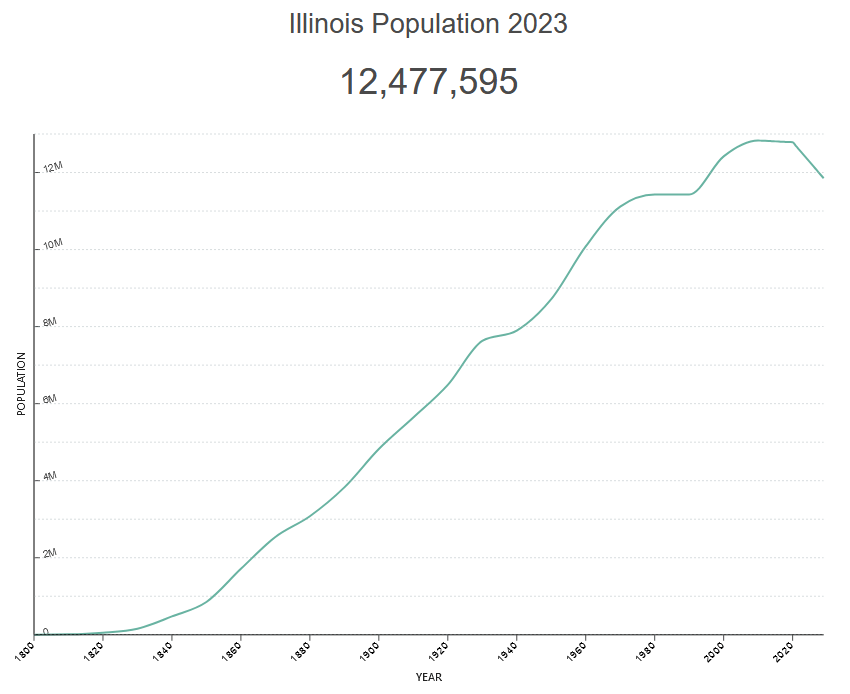

Unfortunately, it will not be able to deliver much growth based on population growth. Illinois is one of the fastest-declining states in the nation in terms of population:

{kind=link}

As we can clearly see, the state's population has been declining fairly rapidly since the pandemic occurred. Fortunately for Ameren, much of this population decline has been localized in Chicago, which Ameren does not serve. However, many of the same factors that are causing an exodus from Chicago are also present in the rest of the state.

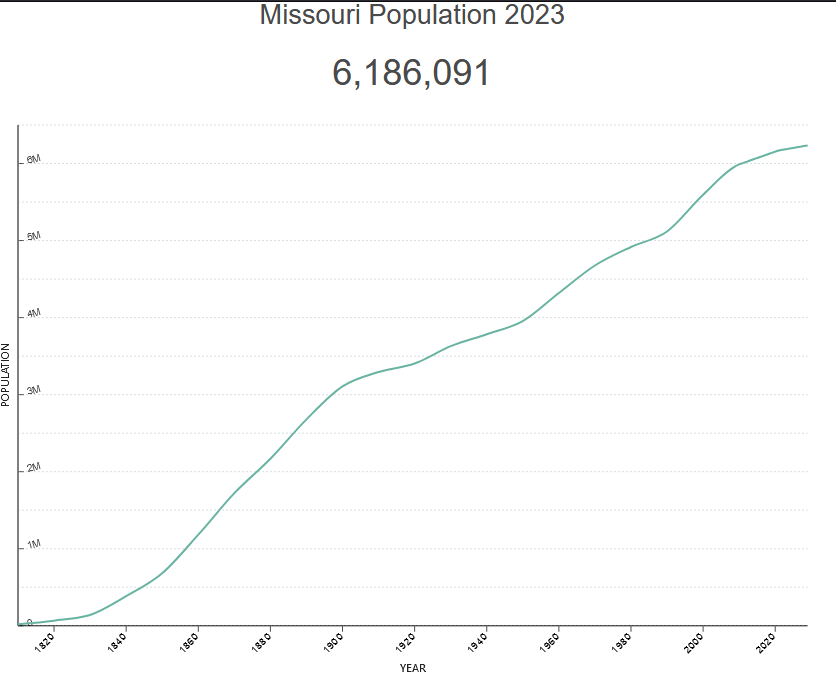

Things are a bit better in Missouri, which is seeing population growth:

{kind=link}

However, the growth in Missouri is nowhere near rapid enough to offset the population decline in Illinois. The takeaway here is that Ameren cannot depend on population growth in its service territory to drive revenue or earnings growth.

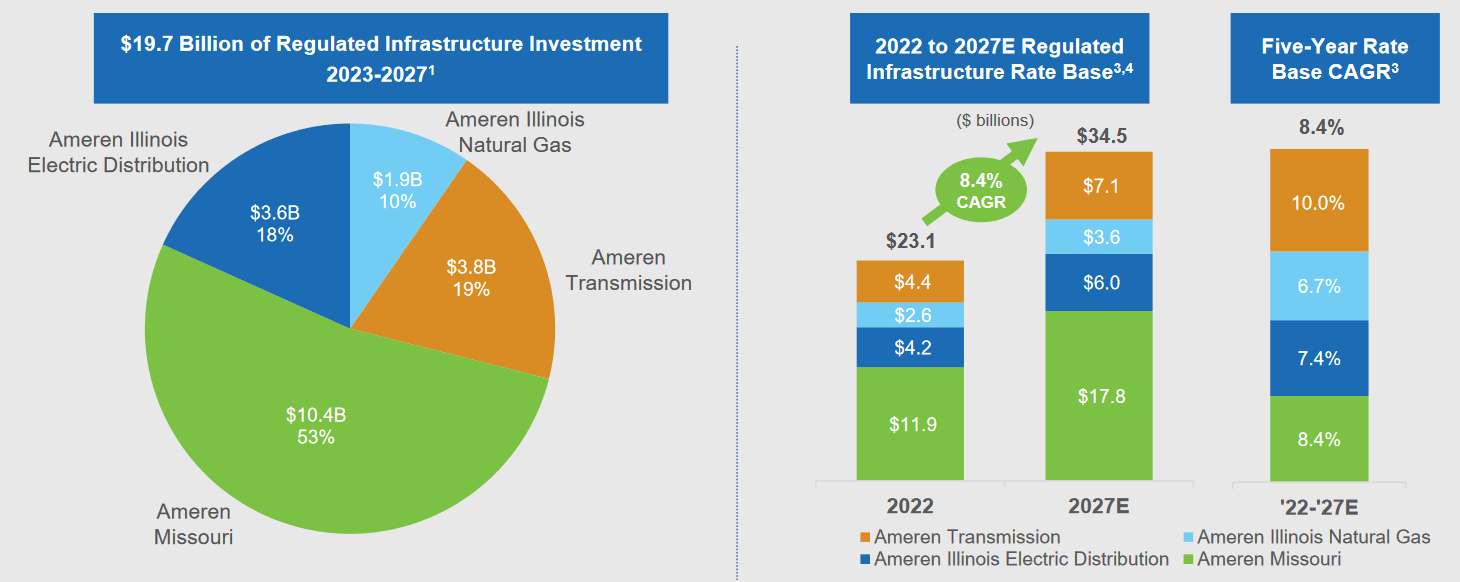

Fortunately, the company does have another method through which it can grow revenue, cash flows, and earnings that is much more reliable. This is by increasing its rate base. The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to positively adjust the prices that it charges its customers in order to earn that specified rate of return. The usual way through which a company increases the size of its rate base is by investing capital into upgrading, modernizing, and possibly even expanding its utility-grade infrastructure. Ameren Corporation is planning to do exactly this, as the company has budgeted $19.7 billion for this purpose over the 2023 to 2027 period:

{kind=link}

It is nice to see that the company has provided us with a five-year plan through 2027. As I have noted in a few recent articles, some of the company's peers are providing much shorter time horizons for the investment programs that they give to investors. As long-term investors, we generally want to have as much information as we can get so that we can come up with our own estimates of where the company will be five years or more down the road. As capital expenditures are the largest expense for a utility, this is the most important piece of information that we can have when making financial projections.

As we can see above, Ameren Corporation is planning to spend $19.7 billion on its infrastructure through 2027 but this will only increase its rate base by approximately $11.4 billion. Thus, the rate base growth is far less than the company's capital spending. This is rather disappointing, but it is understandable when we consider two factors.

The first of these is depreciation, which is constantly reducing the value of assets that the company places into service. Thus, something purchased today will have a lower impact on the rate base in 2027. The company needs to spend enough money to overcome depreciation and still grow the rate base every year or else it will actually see its rate base decline.

The second factor is retirements, as some of the company's planned spending is intended to replace things that will be taken out of service. Once an asset is retired, its value is removed from the rate base, which offsets some of the capital spending.

The plan as presented should be sufficient to grow the company's rate base at an 8.4% compound annual growth rate. This should allow it to grow its earnings per share at a 6% to 8% compound annual growth rate over the same period. The reason why the projected earnings per share growth is lower than the rate base growth is that the company will issue approximately $400 million to $600 million per year in equity to finance its capital expenditures, which will dilute some of the impacts that rate base growth would otherwise have on earnings per share. When we combine the earnings per share growth with the current 3.04% dividend yield, we get an expected total return of 9% to 11% annually, which is very reasonable for a conservative utility stock.

Financial Considerations

It is always important to investigate the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a business than equity because debt must be repaid at maturity. That is typically accomplished by issuing new debt and then using the proceeds to repay the existing debt, as very few companies can afford to repay their debt with cash as it matures. This exposes the company to interest-rate risk, since the new debt may have to be issued with a higher interest rate than the maturing debt in certain market conditions. This is certainly relevant right now because interest rates are at the highest levels that we have seen since 2007. In addition to this risk, a company must make regular payments on its debt if it wishes to remain solvent. As such, an event that causes a company's cash flow to decline could push it into financial distress if it has too much debt. While utilities like Ameren Corporation tend to have remarkably stable cash flow, this is still a risk that we should not ignore as bankruptcies have occurred in the sector.

One metric that we can use to analyze a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well the company's equity can cover its debt obligations in the event of bankruptcy or liquidation, which is arguably more important.

As of March 31, 2023, Ameren Corporation had a net debt of $15.519 billion compared to shareholders' equity of $10.736 million. This gives the company a net debt-to-equity ratio of 1.45 today. This is worse than the 1.40 ratio that the company had at the start of the year, and is back in line with the 1.45 ratio that it had on September 30, 2022. The increase in the ratio is not a particularly good thing to see but it is not out of the historical range for this company.

Here is how Ameren Corporation compares with its peers:

| Company |

| Net Debt-to-Equity |

| Ameren Corporation |

| 1.45 |

| Entergy Corporation ( ETR ) |

| 1.91 |

| DTE Energy ( DTE ) |

| 1.83 |

| Eversource Energy ( ES ) |

| 1.49 |

| CMS Energy ( CMS ) |

| 1.82 |

This is fairly nice to see. As we can clearly see, Ameren Corporation appears to be less reliant on debt to finance itself than many of its peers. Thus, the company's debt load should not present a particularly high risk to investors. We do not need to be overly concerned here.

Dividend Analysis

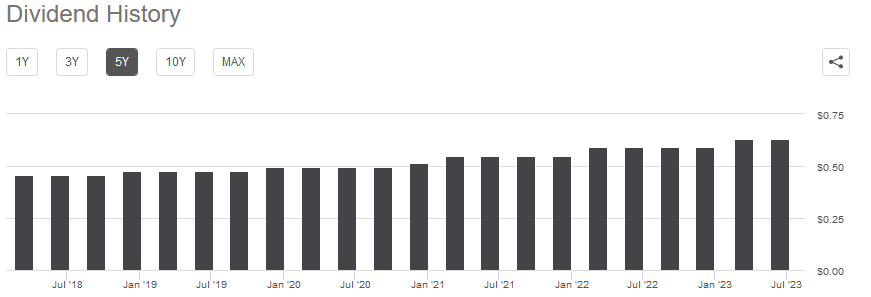

One of the biggest reasons why investors purchase utility stocks is because of the very high yields that they typically possess. This is because these companies have relatively low growth rates, so they pay out a significant portion of their earnings to the investors in order to provide a competitive total return. Ameren Corporation is certainly no exception to this, as the stock currently yields 3.04%, which is substantially above the yield of the S&P 500 Index. In addition to a high current yield, Ameren has a long history of raising its dividend on an annual basis:

{kind=link}

This is very nice to see during inflationary periods, such as the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This can make it feel as though we are getting poorer and poorer with the passage of time, a phenomenon that is especially pronounced among retirees or others that are depending on their portfolios to pay their bills and finance their expenses. The fact that the company increases the amount of money that it pays each year helps to offset this problem and maintains the purchasing power of the dividend.

As is always the case, it is critical that we ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut since that would reduce our incomes and probably cause the stock price to decline.

The usual way that we judge a company's ability to pay its dividends is by looking at its free cash flow. The free cash flow is the amount of money that was generated by the company's ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is therefore the amount that can be used to benefit the shareholders through debt reduction, stock buybacks, and dividends.

During the twelve-month period that ended on March 31, 2023, Ameren Corporation reported a negative levered free cash flow of $1.4225 billion. That is obviously not enough for any dividends, yet the company still paid out $623.0 million to its shareholders over the period. At first glance, this is likely to be concerning as the company had insufficient free cash flow to cover its dividends.

However, it is common for utilities to finance their capital expenditures through the issuance of debt and equity. I mentioned that earlier in this article. The company will then pay its dividends out of operating cash flow. This is done because the high capital expenditures involved in constructing and maintaining a utility-grade infrastructure network over a wide geographic area would otherwise preclude the issuance of any dividends or shareholder returns. During the trailing twelve-month period, Ameren had an operating cash flow of $2.371 billion. That was more than sufficient to cover the $623.0 million that the company paid out in dividends with a great deal of money left over to cover other expenses. Overall, it appears that the company should be able to sustain its dividends over the long term.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a utility like Ameren Corporation, we can value it by looking at the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company's forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa. However, there are very few companies that have such low ratios in today's richly-valued market. As such, the best way to use this ratio is to compare Ameren Corporation to its peers in order to see which company offers the most attractive relative valuation.

According to Zacks Investment Research , Ameren Corporation will grow its earnings per share at a 6.43% rate over the next three to five years. This is in line with the figure that we used earlier to calculate the total return based on the company's rate base growth so it seems pretty solid. This growth rate gives the stock a price-to-earnings growth ratio of 2.96 at the current stock price. Here is how this compares to Ameren's peer group:

| Company |

| PEG Ratio |

| Ameren Corporation |

| 2.96 |

| Entergy Corporation |

| 2.62 |

| DTE Energy |

| 3.04 |

| Eversource Energy |

| 2.56 |

| CMS Energy |

| 2.58 |

As we can see, Ameren Corporation is a bit more expensive than some of its peers, but it is hardly the most expensive company in the group. Its valuation is in fact almost identical to what it had the last time that we discussed this company, which is not really surprising as its three-month stock price has been almost flat:

{kind=link}

Admittedly, this performance may not exactly excite anyone, but as I pointed out in a blog post earlier today, the S&P 500 Index has actually been down year-to-date when excluding the performance of seven technology stocks.

Overall, Ameren continues to look reasonably attractive at the current price in light of all of this. It still makes sense to accumulate at the current level.

Conclusion

In conclusion, Ameren Corporation is a solid utility play that is well-positioned to handle whatever the economy might throw at it over the remainder of this year. The company is also likely to deliver reasonable total returns for a utility as its growth capital spending drives earnings per share growth. It seems likely that the company will continue to raise its dividend as time goes by as well. When all of this is combined with a reasonable valuation, Ameren looks like a good stock to accumulate.

For further details see:

Ameren: This Utility Is A Good Stock To Accumulate Today