CA - American Homes 4 Rent: A Sunbelt SFR REIT Doing Its Part To Alleviate The Housing Shortage

Summary

- The United States has a severe housing shortage.

- Even after the strong rally in home prices over the last few years, homebuilders aren't significantly ramping up construction.

- And yet, there is a huge cohort of Millennials entering their prime single-family home years over the next decade.

- AMH is perfectly positioned to benefit from the housing shortage as well as the domestic migration into Sunbelt states.

The United States has a housing shortage.

Mark Zandi, Chief Economist at Moody's Analytics, says the US is short 1.6 million homes. The US government-sponsored enterprise Freddie Mac puts the supply shortage much higher at 3.8 million housing units, mainly in smaller and more affordable homes. Some estimates, such as the National Association of Realtors in 2021, say underbuilding is as high as 7 million units.

One satisfying way to invest is to identify problems and then find companies that are actively working to solve them. Though capitalism is not a perfect system, it's good at solving problems, for the most part.

That's where American Homes 4 Rent ( AMH ) comes in.

When it comes to the housing shortage, investors typically think to invest in either owners of rental housing or homebuilders. The beauty of AMH is that it is both. The real estate investment trust ("REIT") owns and develops single-family rental ("SFR") homes.

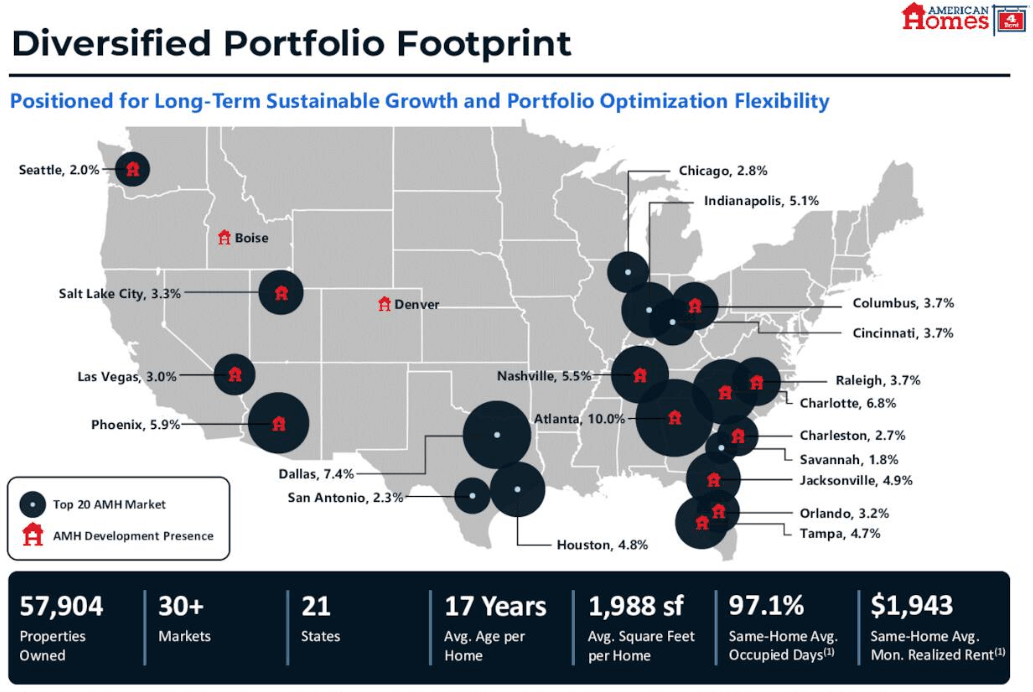

AMH owns around 58,000 SFRs across the United States with a particularly heavy concentration in fast-growing Sunbelt states like Texas, Florida, Georgia, North Carolina, and Arizona. These states were beneficiaries of domestic net migration before the pandemic, and COVID-19 only accelerated that trend.

With a strong balance sheet, ample growth opportunities, a supply shortage likely to support rent growth for the foreseeable future, lower input costs for its home development arm, and a relatively modest valuation of 20x core FFO, AMH looks like a fantastic buy today.

Could it endure further downside in the case of a 2023 recession? Yes, it certainly could. But the strength of the long-term outlook for AMH is such that buying today at a price of around $31 provides a great risk-adjusted return and likely total returns in the mid-teens, not to mention the probability of double-digit dividend growth.

Solving The Housing Shortage

Back to the housing shortage problem.

We all know at this point that home prices soared higher in the last few years by around 20-40%, depending on the market. But did incomes rise by that much? Nope. Not even close.

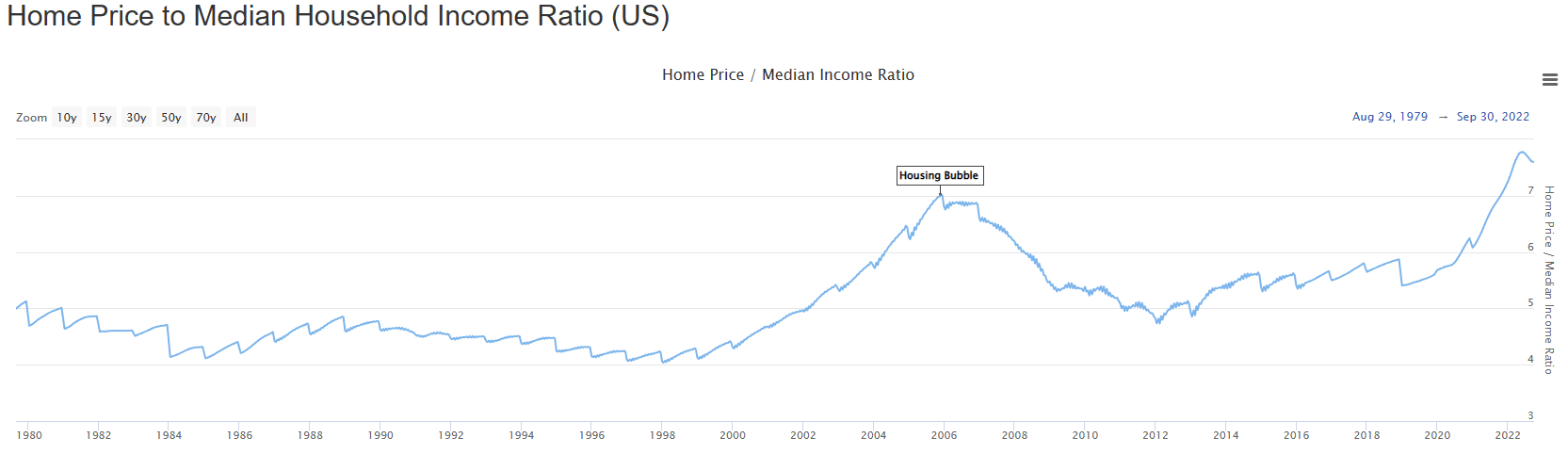

As such, homeownership affordability as measured by home price to median household income spiked to its highest level on record - higher even than at the peak of the housing bubble in the mid-2000s.

{kind=link}

The chart above goes through the end of Q3 2022 (end of September). It appears that the home price to median income ratio peaked in May 2022 at 7.78x and has been on the decline ever since. That probably continued into the end of 2022 as incomes rose and home prices mostly slid.

But even after this slight dip in the latter half of 2022, home affordability as measured by home price to median income is probably still well above the peak of 7x reached during the mid-2000s housing bubble . The housing shortage remains acute.

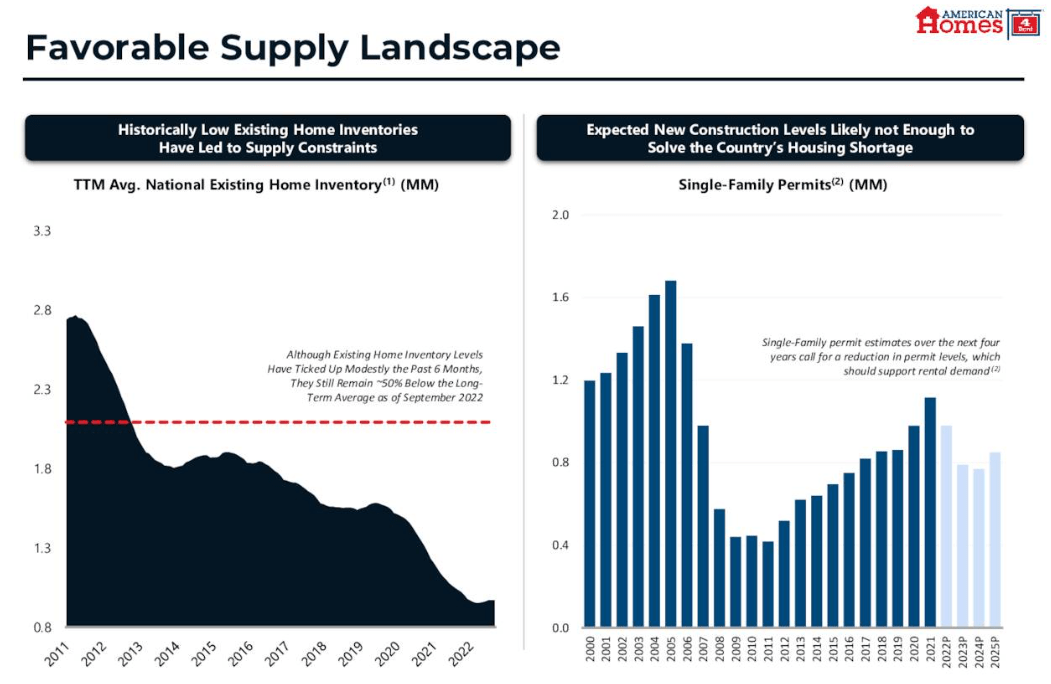

We can see evidence of this in the fact that the inventory of existing homes on the market for sale in 2022 was at one of its lowest levels ever (left image below). And fear of repeating another extreme home glut is so thoroughly ensconced in the minds of homebuilders (not to mention slowing population growth) that construction of new homes does not come close to solving the problem (right image below).

{kind=link}

As I see it, homebuilders are acting a lot like oil producers today. Neither want to produce so much of their respective products as to make the price drop.

For homebuilders, they definitely don't want to see home prices substantially drop, because their input costs have spiked so dramatically that their margins haven't really expanded along with the rise in home prices. There has been some relief on construction costs recently (more on that below) but still not enough to start throwing up homes left and right.

This means that the housing shortage isn't on the verge of going away anytime soon.

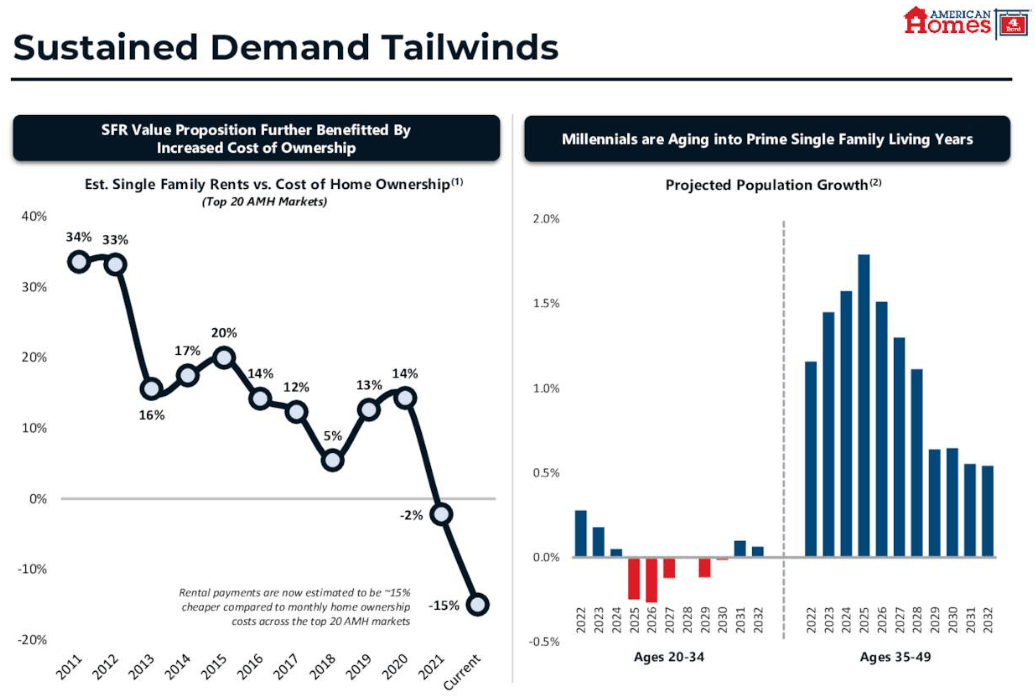

What's more, given the dramatic increase in home prices in the last few years (even with the slight drop in recent months) along with the huge increase in mortgage rates, the cost of homeownership remains far above rent rates.

As AMH CEO David Singelyn explained on the Q3 2022 conference call :

[R]enting today is significantly more affordable than homeownership. Using recent John Burns data, it is about 15% cheaper to rent versus own across our top 20 markets.

On the "cheaper to rent than buy" point, see the chart below on the left:

{kind=link}

Moreover, as you can see on the chart above on the right, from a demographic standpoint, AMH is in a strong position for the next decade. The large millennial cohort has mostly aged out of their 20s and is entering their prime single-family home years of 35-49.

Many would like to buy, of course, but if homeownership is unaffordable, then many will choose to rent single-family homes instead.

Why AMH Is A (Profitable) Solution

We've already gotten into the subject of why AMH is a great way to profit from the housing shortage, so let's camp it right there on that point.

As previously mentioned, AMH's SFR portfolio is overwhelmingly weighted to the Sunbelt, especially Texas, Florida, Georgia, and the Carolinas.

{kind=link}

Also, notice the lack of exposure to either California or the coastal Northeast. I very much like that fact, as these are the areas that have seen the most net outmigration over the last several years.

Other than location, AMH has a few things going for it.

{kind=link}

First, have I mentioned the housing shortage yet? I have? Well, it's hard to overstate.

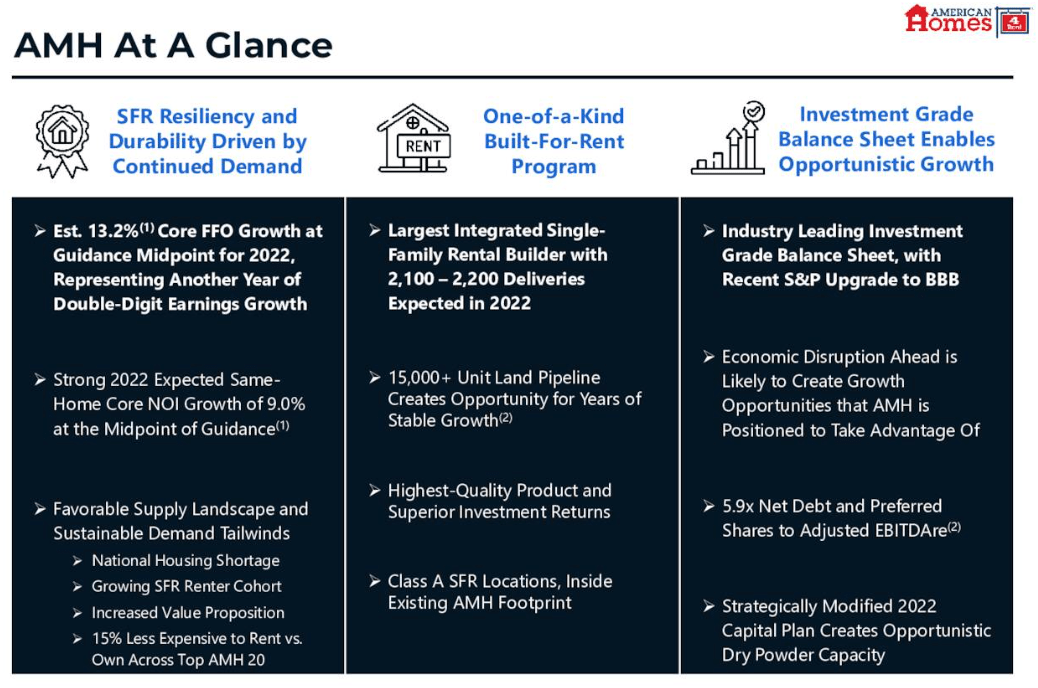

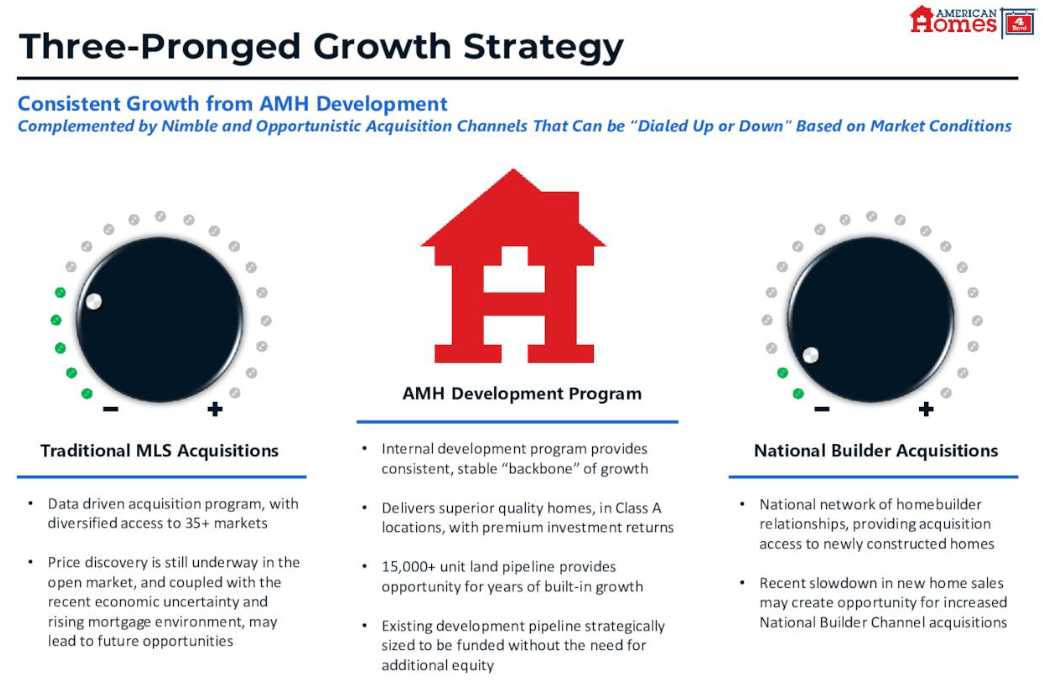

Second - and this is so important - AMH has an internal SFR development program. In other words, the REIT can build SFRs from the ground up itself. This is not an asset that any of its SFR REIT peers share.

AMH sometimes develops houses within third-party neighborhoods, especially in its joint ventures. But for the most part, AMH's internally developed SFRs are located in wholly-owned, master-planned, highly amenitized neighborhoods. This basically takes the synergies of apartment complexes, including community pools, clubhouses, and fitness centers, and puts them in a neighborhood of SFRs.

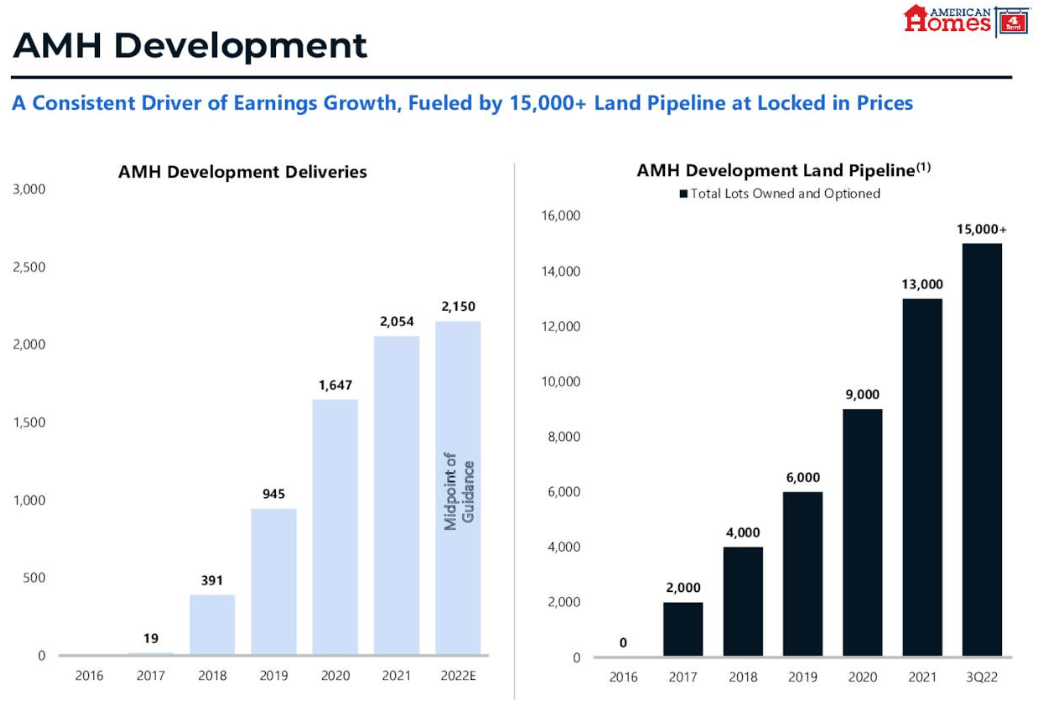

With a land bank of over 15,000 sites and a current development rate of about 2,000 new homes per year, AMH has a growth runway from developments spanning over seven years. And that pipeline continues to grow.

{kind=link}

In Q3 2022, AMH delivered 501 new homes from its development arm, slightly less than half of which were for joint venture partnerships and slightly more than half of which went into the wholly-owned portfolio.

Typically, AMH is able to develop homes at stabilized yields about 100 basis points above the cap rates on existing SFRs on the market. That is a huge benefit at a time when all REITs' cost of capital has gone up significantly.

Moreover, on the Q3 conference call, AMH's management said they are seeing early signs of input costs coming down, especially in the pre-drywall stage of construction. The price of lumber, for instance, is now below its level immediately preceding the onset of COVID-19.

If input costs fall and SFR rent rates do not, then the effective yield on AMH's newly developed homes will rise.

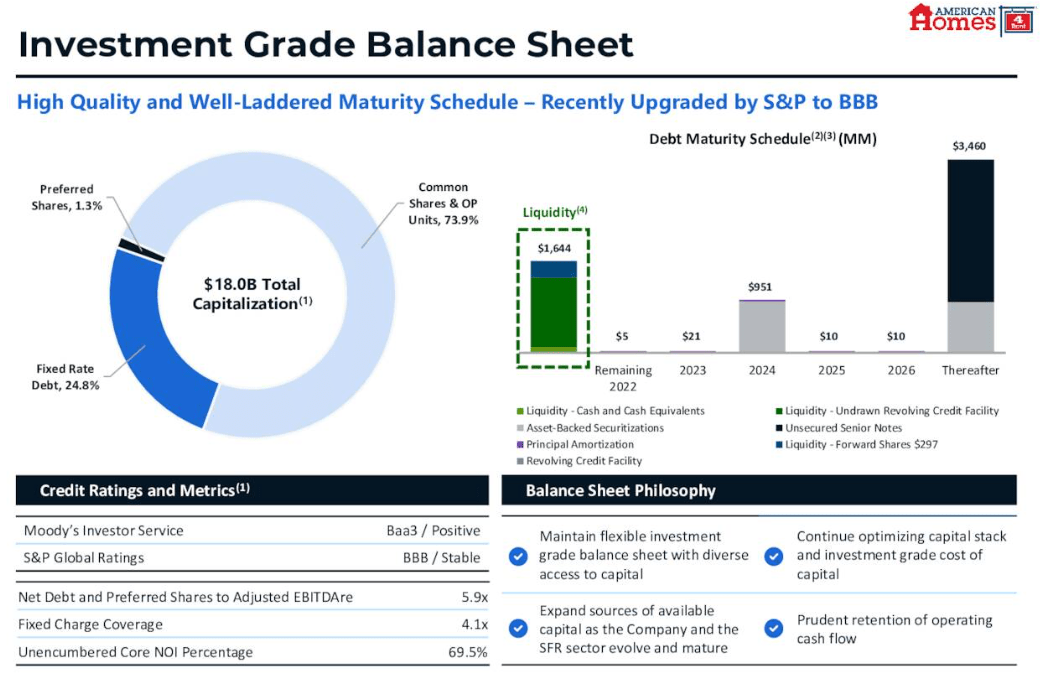

Third, AMH has a very strong balance sheet, with common equity accounting for ~74% of total capitalization. Compare that to your average mom-and-pop SFR landlord using only 20-40% equity for their properties.

{kind=link}

What's more, AMH has an investment grade credit rating of BBB, and just shy of 70% of its assets (as measured by NOI) are unencumbered by secured financing in the form of mortgages.

The REIT has almost no debt maturing this year and plenty of liquidity with which to refinance or pay off its debt maturing in 2024.

AMH's net debt plus preferreds to EBITDA ratio sat at 5.9x at the end of Q3 2022. That is just a smidge above peer Invitation Homes' ( INVH ) 5.7x net debt to EBITDA and well below Tricon Residential's ( TCN ) 8.3x net debt to EBITDA.

Speaking of a peer comparison, AMH's particularly strong performance in the COVID era has shined through in its total return performance.

This is mostly from superior price performance, because AMH's dividend yield of 2.3% is lower than both INVH's 3.0% and TCN's 2.9%.

But I believe AMH is superior to its SFR REIT brethren in a few key ways.

First, notice in the chart below that in the last three years (what we might think of as the "COVID years"), AMH's core FFO growth has exceeded that of any SFR or multifamily REIT peer, including my favorite Sunbelt multifamily REIT Mid-America Apartment Communities ( MAA ):

AMH December Presentation

Second, notice above that AMH's particular mix of markets is expected to enjoy slightly faster household growth this year than INVH. Only MAA's market mix is expected to have faster household growth than AMH.

Third, unlike INVH or TCN, AMH enjoys the crucial benefit of having an in-house development platform as a growth channel.

{kind=link}

INVH and TCN only have the other two basic growth channels: buying homes listed on the MLS and acquiring directly from homebuilders.

As stated before, when you can build your own SFR from the ground up at an all-in yield about 100 basis points higher than market cap rates, you have a huge advantage over your peers.

A Primary Risk: Property Taxes

Recessions are of course a risk for AMH, as they could result in higher unemployment and an uptick in tenant defaults / premature move-outs. This is especially true if 2023 sees a downturn mostly for white-collar workers (a " richcession ," as the Wall Street Journal called it). AMH's higher rent properties are mostly inhabited by relatively high-income workers and/or dual income households.

However, this is not a big concern for me, because most SFR residents will do what it takes to stay in their home, even if it takes selling the Model 3 charging up in their garage. For families, especially, moving into some sort of multifamily housing is probably off the table, if they can do anything about it.

Once you go single-family, you don't tend to backslide into the apartment life.

The far bigger risk I see is that state governments may target SFR owners, especially the big institutional players like AMH, for higher property taxes. Unlike the Federal government, states do not have the printing press, nor the effectively infinite capacity to borrow money. They have to pay their bills somehow. Big SFR owners certainly seem like the most politically feasible targets from which to extract revenue.

We may already be seeing this begin in some states like Texas.

Initial property tax assessments in the state of Texas targeted SFRs with particularly high jumps in home valuations. AMH reported that its initial (pre-contest) taxes in the Lone Star State leaped by over 20% year-over-year.

If Texas succeeds in supercharging its tax revenue from mustache-twirling Monopoly Man SFR owners like AMH, other states may follow suit.

On the hopeful side, AMH is of course contesting these tax assessments and doing its best to encourage lawmakers not to come down too hard with the property tax hammer. It's not like higher taxes are going to encourage anybody to build more housing.

In the words of Ronald Reagan, "If you want less of something, tax it." You'd think the conservatives in the Texas state legislature (probably all with pictures of Ronald Reagan hanging on their office walls) would understand that.

Moreover, lower home prices in 2023 could ease the growth in property taxes, at least for now.

Bottom Line

The bottom line is simple: the US has a housing shortage. AMH profits from that housing shortage while simultaneously doing its part to alleviate it.

The balance sheet is strong, the portfolio well-located, and both core FFO and the dividend are likely to grow by double-digits going forward.

For further details see:

American Homes 4 Rent: A Sunbelt SFR REIT Doing Its Part To Alleviate The Housing Shortage