CA - American Hotel Income Properties: 9.4% Yielding Debentures Are Appealing

2023-06-07 11:30:00 ET

Summary

- American Hotel Income Properties is a Canada-listed (but US-taxable) REIT focusing on US-based hotel properties.

- The REIT has about 8,000 rooms, 90% of those are part of a Marriott or Hilton brand.

- The AFFO is strong, but the debt level remains relatively high.

- Most of the debt is fixed rate in nature, but interest expenses will increase by 200 basis points when all existing debt matures.

Introduction

As I own the debentures issued by American Hotel Income Properties REIT LP (AHOTF) ( HOT.UN:CA ), I need to keep an eye on the financial results of the REIT to make sure the vehicle can still comfortably make all interest payments while I also hope the LTV ratio will decrease as that will make refinancing discussions with its lenders easier.

American Hotel Income Properties REIT has a dual listing in Canada: one of the listings is in Canadian Dollar (this is the most liquid listing), the other one in US Dollar. As HOT.UN reports its financial results in US Dollar, I will use the USD as base currency throughout this article unless indicated otherwise.

The AFFO remains strong, but I'm still not a fan of the outsized dividend

While the income statement of a REIT isn't very important, I still tend to have a look at it as it obviously still serves as the starting point of an FFO and AFFO calculation. And it serves another useful purpose in the current economic climate: it provides a look under the hood of how the interest expenses are evolving. This article will mainly focus on the recent evolution; for a better understanding of the REIT's background, I'd like to refer you to my older article .

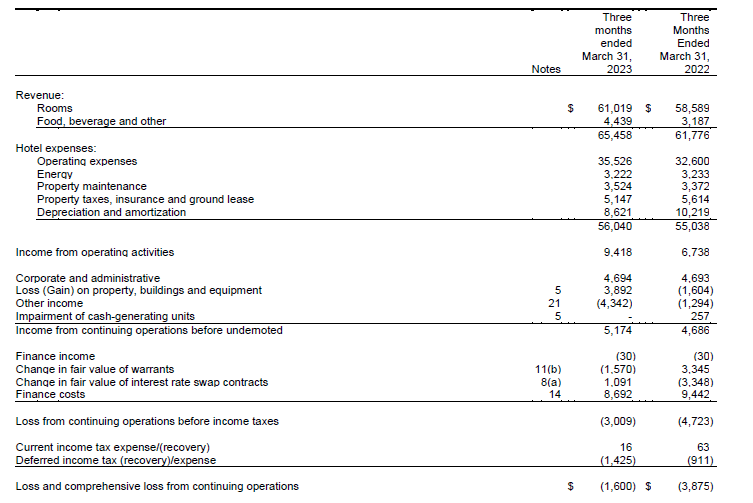

In Q1, American Hotel Income Properties generated a total revenue of US$65.5M , of which about 95% comes from the rooms. This isn't a small operator as its revenue is for instance higher than the revenue generated by Xenia Hotels and Resorts ( XHR ) which I discussed earlier this week .

{kind=link}

The operating income increased from just under $4.7M to just over $5.1M which is very decent considering the first quarter of the year traditionally is the weakest quarter for American Hotel.

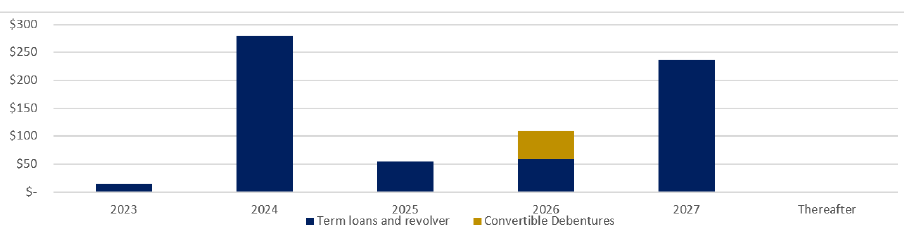

You may be surprised to see the finance expenses actually decreased. Whereas the REIT paid $9.4M in finance expenses in the first quarter of last year, this decreased to just $8.7M in the first quarter of this year. Even if you would include the decreasing value of the swaps to the tune of $1.1M, the net increase of the finance expenses is much lower than what I had anticipated (the average weighted interest rate increased by just 2 basis points to 4.48% in Q1 on a QoQ basis). This is mainly thanks to the smart decision to lock in fixed interest rate on pretty much all of the debt ( 92.2% of the debt either has a fixed interest rate or has been hedged by swaps). The total average interest rate would have been 5.05% excluding the interest rate swaps so even further down the road the interest expenses should remain manageable. Of course, Q4 2024 will be important as that's the first important refinancing date the REIT will have to deal with.

{kind=link}

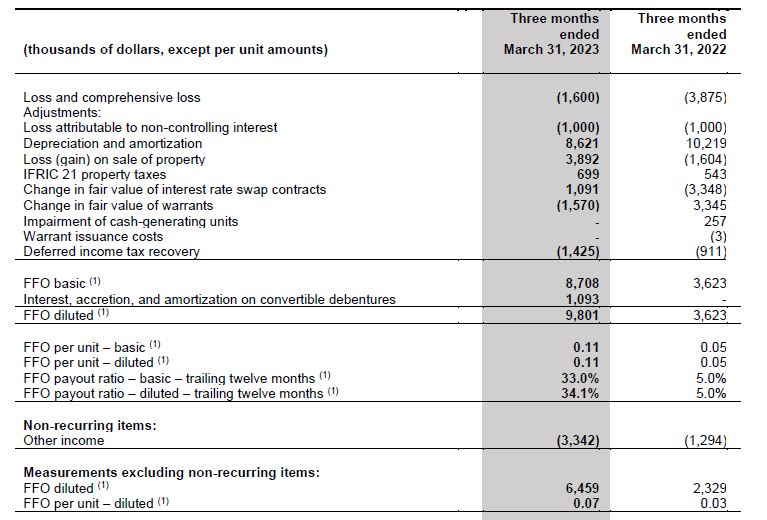

The robust financial performance in the first quarter was a nice surprise (although it obviously was known there was very little near-term interest rate risk), and the FFO and AFFO also came in at pretty decent levels.

The starting point of the FFO calculation is the $1.6M loss and this resulted in an FFO of $8.7M and FFO excluding non-recurring items of $6.5M for a per-share result of respectively $0.11 and $0.07.

{kind=link}

While that sounds great, keep in mind the non-recurring items had a major impact on those results.

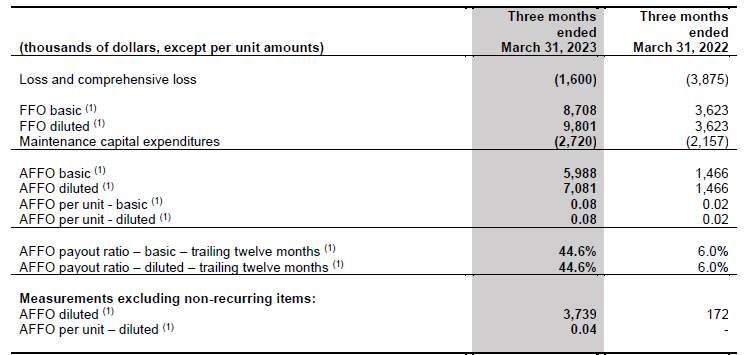

The AFFO calculation is perhaps a better metric to work with, not in the least because American Hotel's AFFO calculation actually includes the maintenance capex - an element that's not included in for instance Xenia's calculation of the AFFO.

{kind=link}

As you can see below, the reported AFFO was $6M but the adjusted AFFO excluding the non-recurring items was just $3.7M. That's just US$0.04 per share on a diluted basis but on an undiluted basis and using the current share count of 78.8M units outstanding, the AFFO in Q1 was US$0.0475, which means the current distribution of US$0.015 per month is still fully covered. Barely covered, but it is covered.

Again, keep in mind the first quarter of the year is the worst for American Hotel Income. Looking at the full-year performance of last year, the full-year AFFO came in at US$0.35 per share despite barely generating any AFFO in the first quarter. The AFFO per share generated in Q2 and Q3 of 2022 was approximately US$0.27 (with some non-recurring events). So the best is absolutely yet to come and the full-year AFFO per share may actually come in at or even exceed $0.30-0.35 per share in which case the distribution would be pretty well covered.

This means the stock is currently dirt cheap at approximately US$1.88-1.90 per share, and the current distribution represents a 10% yield.

I still own the debentures

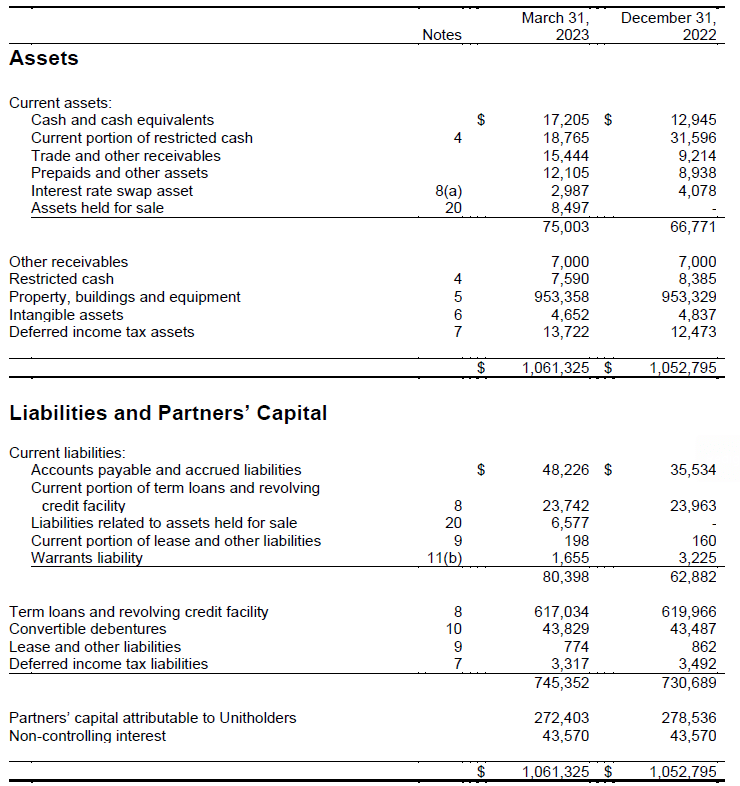

My main issue and reason why I don't have a long position in the common units is the debt levels. The image of the balance sheet below shows there's about $30M in current financial debt (including the debt associated with a property held for sale) and about $660M in long-term debt for a total gross financial debt level of approximately $690M.

{kind=link}

Fortunately, the balance sheet also contains $17M in unrestricted cash, $19M in restricted cash (on a current basis, excluding the $7.6M in non-current restricted cash) and the asset held for sale. Interestingly, the book value of the asset is just $8.5M while American Hotel mentioned a $11.7M sales price. When the transaction closes this quarter , the cash position would increase by $11M to $47M (still excluding the non-current restricted cash but including the current restricted cash) which means the net debt level will drop to approximately $613M.

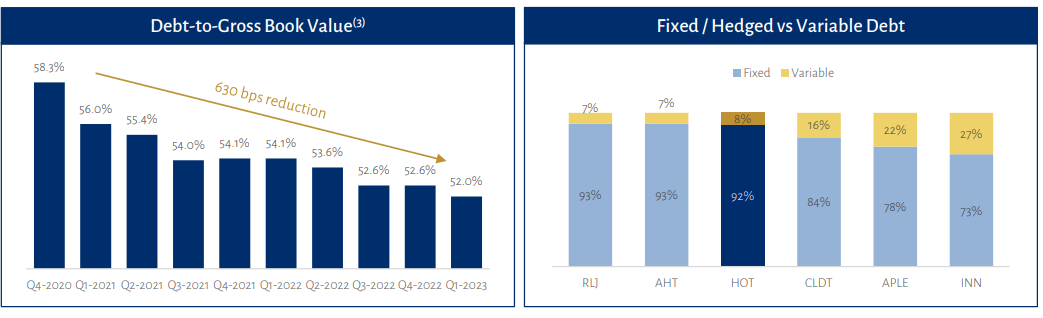

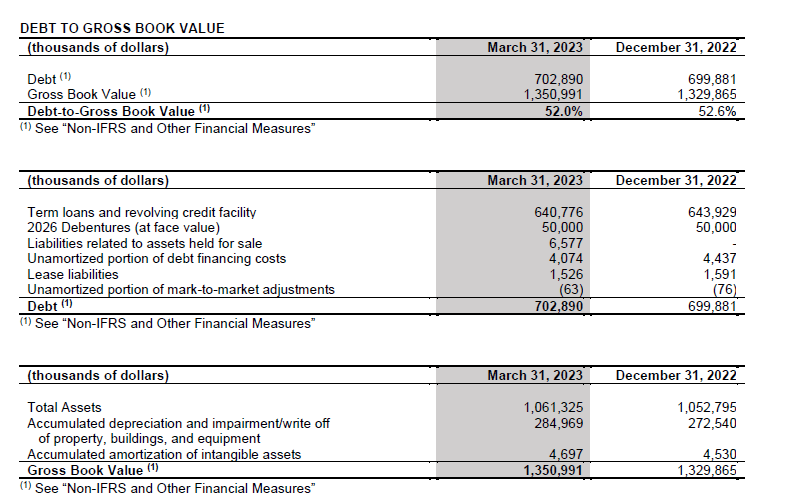

That's still pretty high considering the total book value of the assets is just $953M. It indicates a LTV ratio of close to 65% although the REIT uses the 'gross book value' of its real estate assets The gross book value is approximately $1.35B (excluding the accumulated depreciation) and using that metric, the (gross) debt to gross book value is approximately 52%. And as you can see below, the REIT has clearly made good progress in reducing the net debt and debt ratio .

{kind=link}

The net debt to the adjusted book value is approximately 50% and that's more reasonable.

{kind=link}

I'm generally reluctant to use what essentially is the acquisition cost of the portfolio as base case scenario but the recent sale of the hotel at a premium of more than 30% versus the book value reduces my concerns.

As a reminder, the con vertible debentures mature on December 31, 2026 and pay an interest rate of 6% per year. At 90 cents on the dollar (the current asking price) the yield to maturity is close to 9.5% and I think that's a very fair compensation for being a creditor. The total size of the debenture offering is just US$50M, and the debentures can be converted into common units at a price of US$4.95.

{kind=link}

Investment thesis

I own the debentures but I am not a common shareholder at this moment. I would perhaps consider going long the common units as well if I would see the REIT taking debt reduction slightly more serious. I'm happy with the FFO and AFFO performance and I don't expect the hotel REITs to run into the same issues as they experienced during COVID, but I am personally a little bit uncomfortable with the current debt ratio. I am rating the stock a 'buy' though, but with the caveat it is a speculative buy, and if you're a more conservative investor, you may want to look at the debentures as I prefer to be a creditor than a shareholder at this time.

For further details see:

American Hotel Income Properties: 9.4% Yielding Debentures Are Appealing