CA - Amerigo Resources: Molybdenum Will Be Key In 2023

Summary

- Amerigo Resources ("Amerigo") just released its 2022 production report and its guidance for 2023.

- The guidance shows significant cost inflation, which will eat into margins.

- The dividend safety has deteriorated, but the company is sitting on a comfortable cash pile, and looks committed to the current level of distributions.

- Molybdenum, a by-product of Amerigo's copper production, has been on a tear. This could support the 2023 earnings.

- I remain invested in Amerigo above all for the income - which makes up for the high volatility of the share price.

Amerigo Resources ( ARG:CA , ARREF ), the Canadian company which processes copper tailings in Chile, just released its Q4 2022 production report along with its guidance for 2023. The latter shows a significant increase in projected costs, meaning that higher copper prices will be required to sustain margins.

In case of copper weakness, Amerigo could have trouble covering its current dividend based on 2023 earnings alone. However, the company looks committed to shareholder returns and could still cover the dividend thanks to its net cash position.

There could be room for upside in case molybdenum, a lesser-known metal which is a by-product of Amerigo's copper production, can maintain its current high prices.

In terms of share price, Amerigo's stock has largely recovered after a sell-off in H2 2022 amid lower copper prices and negative macro headlines. It is a volatile stock, which I now consider above all as an income play.

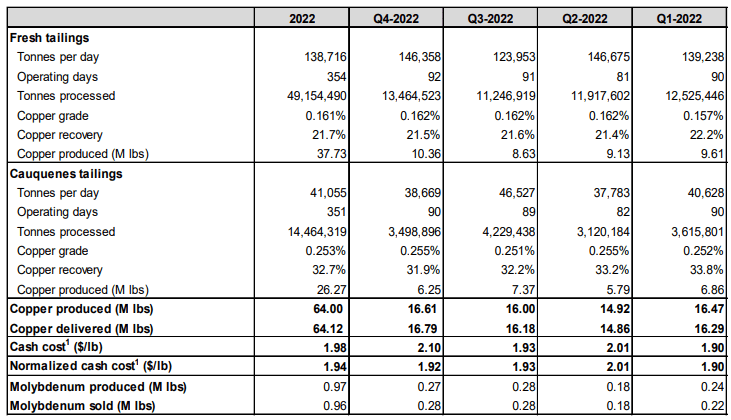

Amerigo's 2022 Production Report

The final production report showed decent quarterly volumes in Q4 - in fact, they were the highest of 2022 at 16.61M pounds. The yearly total of 64M lbs compares favorably with the initial 2022 target of 62M lbs.

{kind=link}

These volumes should ensure decent Q4 financial results - to be released in February - though an adjustment related to a collective labor agreement will constrain margins (including this effect, the cash cost was an elevated US$2.10/lb in Q4).

Another takeaway from the production report is that the Cauquenes historical tailings constantly exceed the fresh tailings received from Codelco in terms of copper grade and copper recovery. Amerigo's capacity to sustain its current level of production, therefore, depends on the remaining quantities of historical tailings. The good news is that there is still about 200M tonnes of material to be processed (14.5M tonnes were processed in 2022).

Amerigo Resources' Technical Report - March 30, 2022

Amerigo's 2023 Guidance

While the Q4 report showed good operational performance, I was not impressed with the 2023 guidance. Volumes are expected to decrease to 62.3M lbs of copper produced - admittedly, the company tends to be conservative in its forecasts. More concerning is the projected 10% increase in cash costs.

The cost increases are found across the board, including power costs and pretty much all services:

Amerigo's 2023 cash cost1 is expected to be $2.14/lb, compared to 2022's normalized cash cost of $1.94/lb. The increase in projected cash cost is mostly attributable to higher power costs of $0.06/lb. [...] MVC will also face a $0.05/lb increase in treatment and refinery charges . These are industry benchmark charges and this year are at the highest level since 2018. Other increases include lime costs ($0.02/lb), Cauquenes processing costs ($0.02/lb), industrial water costs ($0.01/lb) and all other costs combined ($0.04/lb).

I really like Amerigo's transparency under its current management, and the detailed nature of the reports. I also acknowledge that these cost increases are beyond the company's control, and by no means unique in a world of higher inflation.

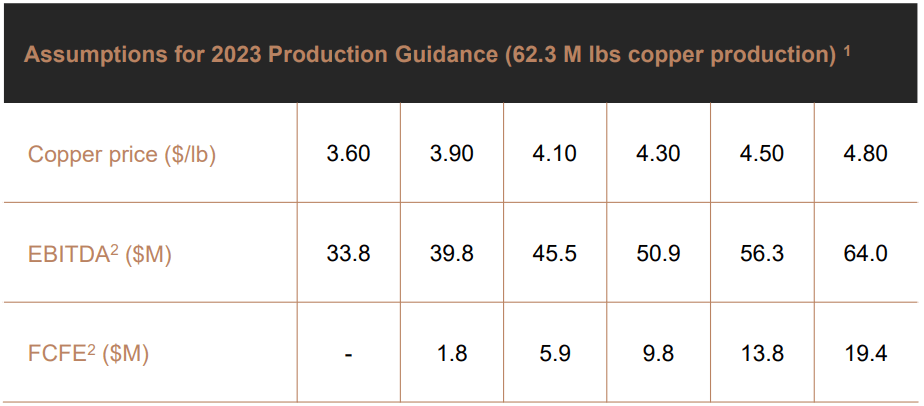

However, this higher cost base does reduce margins, raising the copper price necessary to achieve significant free cash flow - and ultimately, the potential distributions to shareholders. The table below in USD shows the amount of FCFE (FCF to Equity, meaning the cash available for shareholder returns once debt repayments have been made), as a function of the copper price:

{kind=link}

The cash required to cover the regular quarterly dividend of CAD$0.03 per share is approx. US$15M per year. Based on this table, a copper price of at least US$4.5/lb is needed - higher than the current market price of $4.25/lb.

For comparison purposes, I'm showing below the same table as it stood only 6 months ago. At the time, a copper price of $4/lb was enough to secure the current level of distributions.

Amerigo Resources' Aug2022 corporate presentation

How Safe Is Amerigo Resource's Dividend?

Based on the cost increases above, it is clear that the dividend coverage of Amerigo has deteriorated. By contrast, the press release strikes a positive tone:

Under the 2023 guidance assumptions presented in this news release, the Company remains confident in the security of the quarterly Cdn$0.03 per share dividend, and in Amerigo's ability to opportunistically reduce its common shares outstanding. In addition [...], the Company is confident that stronger copper prices will permit the deployment of performance dividends in 2023.

Amerigo seems committed not only to the regular dividend at its current rate, but also to further buybacks, and, potentially, to a special dividend at year-end. How come the company's management is so confident? First, copper prices seem to be in an uptrend, helped by China's reopening and production issues in the likes of Peru. Prices, though, could remain volatile.

In my opinion, the main reason management is committed to shareholder returns is that Amerigo is sitting on a decent cash pile. In fact, its net cash position was approx. $13M at the end of 2022 ($37.8 million cash, $24.5 million outstanding bank debt).

However, this is not what I call a safe dividend. The sooner Amerigo covers the dividend and other shareholder returns through its current year's earnings, the better. In 2023, I will for sure be monitoring the copper price, and, also, that of molybdenum.

Molybdenum To The Rescue?

Molybdenum is a metal used primarily in steel production, bringing strength, hardness, electrical conductivity and resistance to corrosion and wear. It also has a variety of smaller uses, including in renewable energy generation and storage (wind, geothermal, solar, nuclear, and hydro).

Molybdenum is for the most part produced as a by-product of porphyry copper mines, which is the case of Codelco in Chile, whose tailings are processed by Amerigo. There are also a few primary producers, notably in China and the U.S.

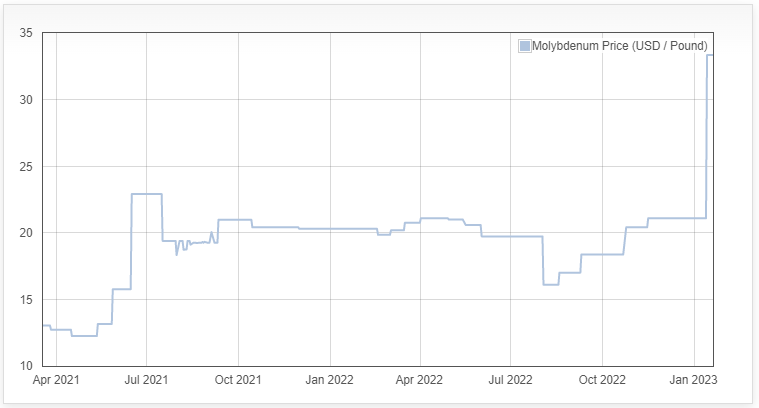

Several producers, both primary and secondary, have been facing production headwinds of late. These supply issues have resulted in a 50% surge in the molybdenum price in January, to around $33 per pound:

{kind=link}

The question, of course, is what happens to prices when factors such as the riots in Peru subside. They will probably normalize, to a certain extent, but there could also be supported by a lasting supply-demand imbalance according to some analysts, due to lower grades being mined:

Global molybdenum consumption is expected to continue increasing over the next decade as demand for molybdenum-containing steels grows. But production has been squeezed by lower molybdenum content in mined ores seams and a lack of new molybdenum projects to meet demand.

Source: Argus, quoted by Mining.com

How does this relate to Amerigo? Molybdenum is a by-product which the company sells, and books as a deduction of costs (credit). The higher the molybdenum price, the bigger the credits, and the lower the cash cost as a result. Contrary to copper, Amerigo doesn't have to pay royalties to Codelco for molybdenum (as far as I know) so the impact of high prices can be quite significant:

Amerigo Resources' corporate presentation

The current molybdenum market price results in a credit of almost $0.45 per pound of copper produced. This compares to $0.21 in the guidance, which is based on an assumption of $16/lb for moly. The $0.24/lb extra credit would bring cash cost down from $2.14/lb to $1.90/lb. Based on the planned yearly production of 62M pounds of copper, this represents almost $15 million in savings.

To be honest, I don't expect molybdenum prices to remain this elevated. But I wouldn't be surprised if they remained significantly higher than the $16/lb base case, if the scenario of supply scarcity is correct. This would greatly improve Amerigo's earnings and dividend coverage.

Takeaway

Amerigo Resources' guidance shows that the company is not immune to inflationary pressures. The higher cash cost will make the company even more dependent on high copper prices. There are, no doubt, reasons to be bullish on copper, and on molybdenum too, which could provide valuable credits and help mitigate cost inflation.

I would not rush to buy the stock at this price, but I'm happy to keep the shares in my income portfolio. Management has proven to be shareholder-friendly, and they look committed to the 2023 distributions. The cash pile can be put to use while we wait for higher copper prices.

For further details see:

Amerigo Resources: Molybdenum Will Be Key In 2023