CA - Amerigo Resources: The Upside Seems Limited (Rating Downgrade)

2023-04-11 00:24:25 ET

Summary

- The quarterly dividend of CAD$0.03/share seems sustainable in the current environment.

- Management expects cash cost inflation of 10.3% YoY to US$2.14/lbs.

- Despite the high-cost profile, Amerigo doesn’t offer much torque to rising copper prices due to its royalties structure.

In the beginning of the year I wrote an article about Amerigo Resources (ARREF) (ARG:CA) – a company that extracts copper out of mine waste in Chile. Since then, the share price has appreciated more than 26%, which is a decent return, given the overall market sentiment. Taking a look at the company in the current environment, management’s 2023 guidance indicates that Amerigo isn’t spared by cost inflation. At the same time, the high cost profile doesn’t translate into significant torque to rising copper prices, due to the sliding scale royalty payments. On the bright side, copper prices around US$4.00/lbs should be sufficient to support the quarterly dividend, but considerable share repurchases and special dividend appear unlikely. Overall, the upside looks limited.

2022 highlights

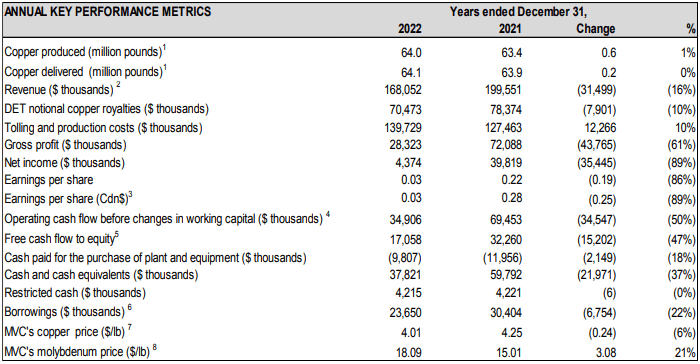

Looking at Amerigo’s 2022 results, it’s quite clear that the combination of lower average realized copper price (US$4.01/lbs; -5.6% YoY) and higher costs (normalized cash cost of US$1.94/lbs; +10.9% YoY) has led to deteriorating performance. Total costs amounted to US$3.45/lbs (+3.9% YoY) as part of the cash costs increase was offset by lower royalties, due to lower copper prices. Free cash flow was more than halved to US$25.1M (-56.3% YoY), while after deducting debt and lease repayments, FCFE amounted to US$17.1M (-47.1% YoY).

{kind=link}

Amerigo's 2022 KPIs (Amerigo Resources)

Still, management felt that the market environment justifies focusing on shareholder returns and distributed US$15.7M of dividends and spent US$12.3M to repurchase 9.4M shares. However, the combined US$28M of shareholder returns were significantly higher than the FCFE that Amerigo generated in 2022, so the cash reserve had to be tapped into. As a result, cash and equivalents fell to US$37.8M as of 2022 year-end, compared to US$59.8M in the beginning of the year.

2023 guidance

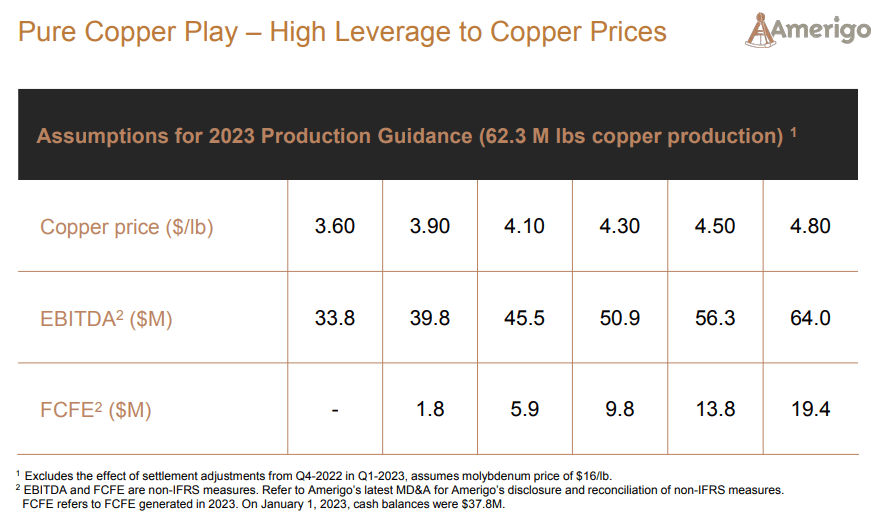

On 17 January, Amerigo release its 2023 guidance . The projections indicate further cost inflation hit as cash costs are anticipated at US$2.14/lbs, indicating 10.3% YoY increase, mostly on higher power costs and refinery charges. The guidance was prepared under US$3.60/lbs copper price and US$16/lbs molybdenum price scenario. Management also provided projected CAPEX of US13.3M for the year, the majority of it being related to sustaining activities. The company also included projections about EBITDA and FCFE under various copper price scenarios in its corporate presentation .

{kind=link}

Amerigo's results sensitivity to copper prices (Amerigo Resources)

Looking at the table, I find the discrepancy between EBITDA and FCFE quite substantial and contradictory to the CEO claims in the earnings call of maintaining the share buyback and even paying performance dividends:

In addition to quarterly dividends of CAD 0.03 per share and the repurchase of common shares for cancellation under the normal course issuer bid, we are confident in stronger spot copper prices and a robust copper price outlook will translate into deployment of performance dividends in 2023.

In order to maintain just the quarterly dividend alone, Amerigo will need about US$15M for the whole year. However, according to the sensitivity table in the corporate presentation, this will require copper prices north of US$4.50/lbs. The huge difference between EBITDA and FCFE doesn’t make sense to me, given the 13.3M of anticipated CAPEX, around US$20M of depreciation and even US$7M of debt repayment. So I decided to take the 2022 and the 2023 guidance as reference points and do a simulation of my own. However, I didn’t assume any borrowings reduction as the debt level of the company is rather low and it may decide to maintain it and return capital to shareholders.

FCFE/share sensitivity to costs and copper prices (Author's own assumptions)

*Tolling and production costs exclude depreciation and administration expenses

In order to continue paying US$15M of annual dividends, given the 165.5M shares outstanding will require FCFE of at lead US$0.09/share. Under my base scenario of direct tolling and production costs of US$1.90lbs (US$1.73/lbs in 2022) and copper price of SU$4.00/lbs, this seems achievable. However, almost nothing would be left for the buyback, let alone any performance dividends.

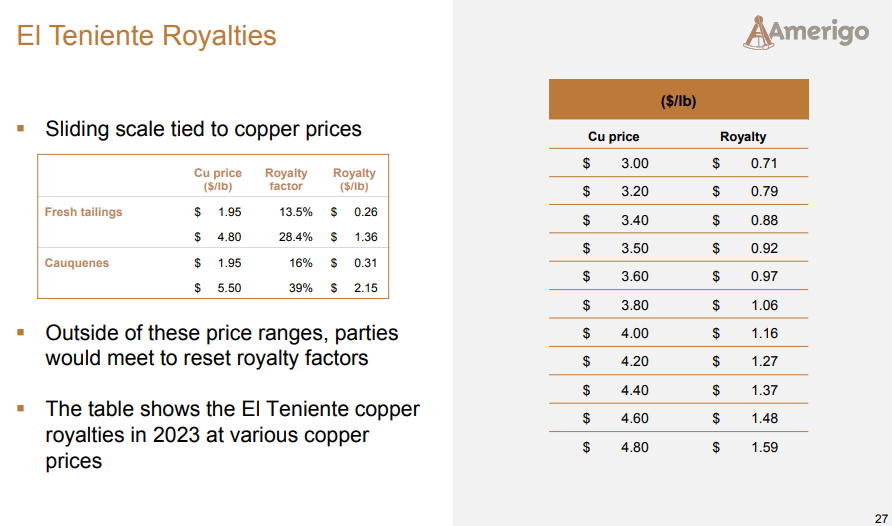

Inferior torque to copper prices

{kind=link}

Royalty structure (Amerigo Resources)

The overall impression that one may get from the corporate presentation is that Amerigo offers high leverage to copper prices. Typically, this is true for most miners – a high AISC profile, close to the price of the commodity, induces geometrical margin expansion if commodity prices go up. However, the structure of Amerigo’s royalty payments eats away literally 50% of the upside before even considering the effect of taxes. As a result and as evident from the two sensitivity tables above, the torque of rising copper prices on Amerigo’s FCFE is rather small.

Valuation discussion

Since the beginning of the year, Amerigo’s share price has appreciated more than 30%, outperforming both the commodity price itself, represented by the iPath® Series B Bloomberg Copper Subindex Total Return ETN ( JJC ) as a proxy and the miners represented by the Global X Copper Miners ETF ( COPX ). Also, Amerigo has outperformed a typical high cost miner like Taseko Mines ( TGB ), which has substantial torque on rising copper prices.

At the same time, the prospects before Amerigo don't look impressive as the sliding scale royalties are a considerable drag. On the other hand, they provide some support in a falling commodity price environment. Using the CAD0.03/share quarterly dividend as a guideline, this implies 7.1% gross dividend yield on the current share price of the company. This is on the high side in the commodity space, so some income oriented investors may still find the stock attractive. But for me, the upside looks limited.

Risks

Due to its business model, Amerigo doesn’t assume any risks related to actually developing and operating a mine. For that reason, the biggest threats are cost inflation and copper prices. Regarding the latter, the sliding scale nature of royalty payments provides both some protection to the downside, but also a burden to the upside. As far as cost inflation pressures, the easing of energy prices could offer some relief into the year, but I doubt that will be for long, given the recent OPEC oil production cuts.

Takeaway

Following the recent jump in the share prices of Amerigo Resources stock, the upside potential looks limited. Contrary to management’s claims, the company doesn’t appear to have substantial leverage on the copper price as royalty payments are eating away 50% of the price increase on the spot. The quarterly dividend could be maintained in the current price environment, but I doubt significant share repurchases, let alone a performance dividend in 2023, unless copper prices approach the US$5.00/lbs levels.

For further details see:

Amerigo Resources: The Upside Seems Limited (Rating Downgrade)