MU - Amkor Technology: Strong Position In Semiconductor Supply Chain Offers Resilience

Summary

- Growth in Automotive electronics, along with Amkor Technology, Inc.'s capabilities in advanced packaging and its deep relationships with Automotive OEMs, should benefit the company in the future.

- Amkor's recent expansion to Vietnam and its presence in Portugal will help it offer a large-scale, cost-effective advanced packaging and test location to its customers.

- Amkor's technology leadership position in advanced packaging is recognized by its leading customers, differentiating it from its competitors.

Investment Hypothesis

Amkor Technology, Inc.'s ( AMKR ) track record of outperforming the semiconductor markets in 2022 should continue in 2023, as the company is well-positioned to grow at more than the industry rate. Growth from the automotive electronics market due to the proliferation of driver assistance electronics, infotainment and telematics will help the company grow in 2023.

As a part of TSMC's 3D Fabric Alliance , the company will navigate its supply chain challenges by working with other supply chain leaders to accelerate the innovation of next-generation, high-performance solutions for its customers. At the current P/E multiple of 8.8x, Amkor Technology, Inc. stock is trading at a discount, given the company's technology portfolio, scale, global footprint, and track record to outgrow the markets. Thus, investors holding Amkor Technology should continue to hold the stock. It also is a good time to buy the stock for new investors that do not have Amkor Technology, Inc. in their portfolio.

About Amkor Technology

Amkor Technology, Inc. , headquartered in Tempe, Arizona, and incorporated in 1968, is a leading semiconductor packaging and test services provider and a global leader in the Outsourced Semiconductor Assembly and Test ((OSAT)) industry. In addition, the company provides Design Services, Package characterization and Wafer bumping. Further, Amkor is an industry leader in developing and commercializing advanced packaging and test technologies with high demand in the smartphone market, automotive applications and consumer devices.

According to the company, its strategy is to identify opportunities in advanced packaging and testing areas for automotive and industrial end-market customers that can generate a quick return on investment.

We typically look for opportunities in the advanced packaging and test areas where we can generate reasonably quick returns on investments made for customers seeking leading-edge technologies. We also focus on developing a second wave of customers to fill the available capacity when leading-edge customers transition to newer packaging and test equipment and platforms. In addition, we are seeking to add new customers and deepen our engagement with existing customers. This includes an expanded emphasis on the automotive and industrial end market, where semiconductor content continues to grow, and in the analog area for our mainstream wire-bond technologies.

Recently, Amkor launched the Smart Manufacturing Initiative to leverage its Industry 4.0 expertise to deliver near real-time data accuracy with maximum efficiency for its customers.

Amkor Website

The company's capabilities in Industry 4.0 rests on employing autonomous machines that operate with no manual intervention, using Big data analytics to provide insights into machine performance, using Industrial IoT to increase the speed of the manufacturing process, utilizing Cloud computing for real-time data storage, protecting the data through its Digital Rights Management solution and using machine learning to improve defects detection that human beings can find it challenging to identify.

Author Calculations

In the last ten years, Amkor's revenues grew at 9.9% CAGR, whereas in the last five years, the company's revenues grew at 11% CAGR due to the growing demand for semiconductor packaging and testing services.

Author Calculations

The company's operating and net margins have improved in the last five years due to the better cost structure. However, the company reported a reduction in gross margin in 2022 from 20% to 18% due to increased material costs.

According to Megan Faust, Chief Financial Officer of Amkor,

We experienced a product mix shift towards higher material content products, such as advanced SiP, driven by the outperformance in our communications end market.

Author Calculations

Though the company's asset turnover has stabilized in the last three years, its asset efficiency has decreased in 2023 due to the global slowdown resulting in inefficient use of assets.

Author Calculations

The company had a lower asset efficiency in 2022 due to production inefficiencies, excess inventory, and slow collection of accounts receivable. As a result, the DSO has increased from 66 days to 68 days in 2022, while the cash conversion cycle has increased from 41 days to 48 days in 2022.

Seeking Alpha

The company reported its fourth quarter and full-year results for 2022 on February 13th 2023. Its net sales in Q4 2022 were $1.91 billion, up 11% year-on-year and net income of $164 million. For 2022, the company recorded net sales of $7.09 billion, up 16% year-on-year, well above the semiconductor industry growth rate of low single digits. In addition, it reported a gross profit of $1.33 billion and an operating income of $897 million.

According to Megan Faust, Chief Financial Officer of Amkor,

Our strategic focus on advanced packaging, our strong position in key growth markets and our broad geographic footprint yielded another year of records and significant accomplishments.

Author Calculations

The company's CapEx spend for the entire year was $908 million, more than $125 million in 2021 to strengthen its leadership position in the high-growth markets of 5G, automotive, IoT and high-performance computing. Further, the Capex margin has improved from 10.9% in 2020 to 12.8% in 2022.

Author Calculations

In 2022, the company generated $1.1 billion in cash from operations. Despite the increase in CapEx, the company generated $194 million in free cash flow. In the long run, the company wants to return 40-50% of its free cash flows to its shareholders as dividends and share buybacks.

Author Calculations

The company has an excellent financial position with total debt in 2022 of $1.2 billion, a debt-to-EBITDA ratio of 0.8x and total cash reserves of $1.9 billion. In addition, the interest coverage ratio of 15.9x indicates that the company is better able to meet its interest obligations and is at a lower financial risk with a better credit rating giving it a higher borrowing capacity.

According to Giel Rutten , Amkor's president and chief executive officer.

2022 was another excellent year for Amkor. We achieved a record revenue of $7.1 billion and a record EPS of $3.11. In addition, all end markets set new record revenue levels for the year, resulting in significant outperformance compared to the semiconductor market. Amkor's strategic focus on advanced packaging, geographic diversity, and industry megatrends positions us well to continue to outperform the semiconductor industry through this cycle.

Seeking Alpha

The company's sales from the top 10 customers have not changed much, with Amkor getting 65% of revenues from its top 10 customers in 2022.

{kind=link}

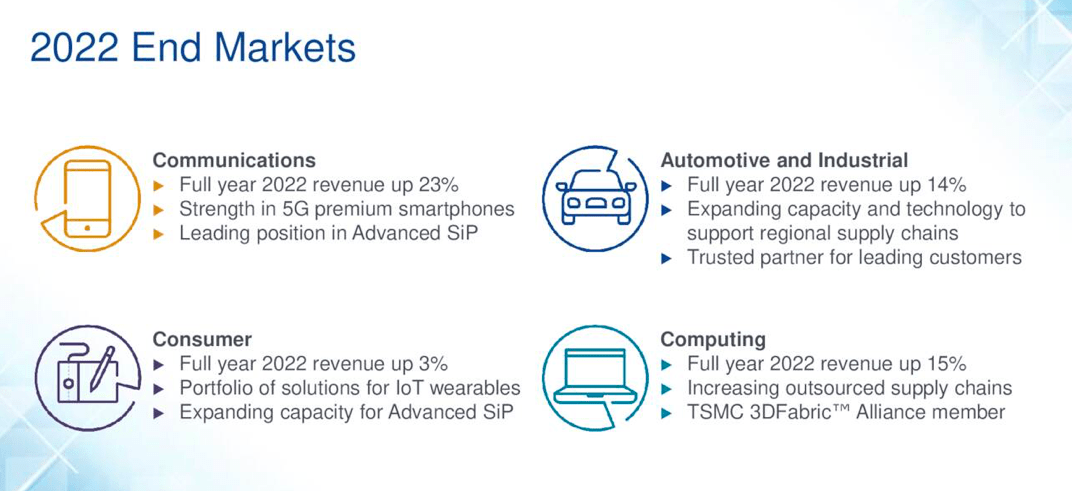

The communications segment continues to be the biggest revenue driver, contributing 44% of its total revenues. It has grown by 23% over the last year and has a strong position at the high end of the market, both in the iOS and Android segments. In addition, the company saw a steep growth in high-power silicon carbide solutions for electric vehicles, requiring unique manufacturing technology. Thus, the company's Automotive and Industrial segments grew by 14% from 2022 to 2021. In the future, the company expects its revenues from automotive electronics to increase due to the higher electrification of vehicles.

According to Giel Rutten , Amkor's president and chief executive officer.

Resilience in the automotive and industrial markets and higher-than-expected premium-tier smartphone demand offset weakening demand in other markets. In the automotive and industrial markets, we set a new quarterly revenue record driven by demand for advanced packaging and infotainment systems.

Finally, Amkor's consumer business increased by 3% in 2022 against 2021 and represented 20% of its revenues, providing a broad portfolio of solutions for IoT wearables and more traditional consumer products.

According to Giel Rutten, Amkor's president and chief executive officer.

Although total smartphone units were down around 10% in 2022, 5G units increased by around 20%. Semiconductor content and premium tier 5G phones continue to increase, and ongoing innovation, improved performance, and added functionality.

Advanced Packaging services contribute 87% of the company's revenues, followed by Testing services, which contribute 13%. The revenues from advanced packaging grew 22% for the year and accounted for 76% of the company's revenue.

According to Giel Rutten, Amkor's president and chief executive officer.

Solutions utilizing our advanced SiP for camera and RF applications and package-on-package flip chip technology for app processes and modems drove most of the growth in 2022. Amkor holds a leadership position in these markets, build on technology expertise and a strong track record as a trusted partner for innovative solutions and operational excellence.

In addition, the company is strategically expanding its capacity and technology base for automotive solutions in Europe, Japan and Korea to support regional supply chains for critical automotive semiconductors.

Author Calculations

The company's ROIC, ROA and ROE have improved in the last two years. However, they showed a slight dip in 2022 due to the higher Cost of raw materials and a slowing economy resulting in weaker growth in the consumer electronics segment.

Author Calculations

Due to the slower growth in 2022, the company's P/E ratio has dipped from 11x to 8.6x, as investors have accounted for slower growth in 2023 due to the global slowdown.

{kind=link}

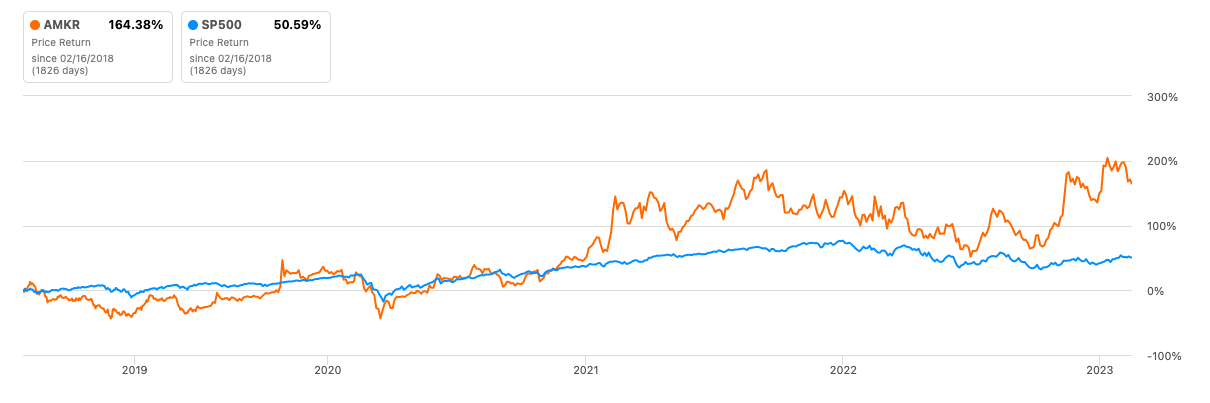

However, the company has given excellent returns to its shareholders in the last five years, generating 164.38% against the S&P 500 (SP500) returns of 50.5%, effectively giving more than 3x returns of the S&P 500 index.

Amkor's Forecast for 2023

Amkor is expanding its footprint to Vietnam and has invested $1.6 billion in 2021 to develop a manufacturing and assembly plant in the northern industrial province of Bac Ninh. The factory will support future customer demand and start high-volume manufacturing in late 2023. Further, the company has strengthened its growing European automotive supply chain through its Portugal factory , where the company is expanding its technology offerings for MEMS, wafer-level fan-out, flip chip and power Solutions.

{kind=link}

In 2023, the company anticipates a challenging macroeconomic environment, and thus expects demand to soften beyond the already weak personal computers and low-end smartphone market.

According to the Giel Rutten, CEO of Amkor:

Current market forecasts indicate that the semiconductor market will decline by mid-single-digit percentages in 2023. We believe the industry is already taking measures to reduce excess inventory in the PC and smartphone market to return to a more balanced supply chain in the second half of 2023.

The silver lining for the company is that the automotive market appears more resilient and expects to grow in 2023. In addition, the company has established automotive manufacturing lines in strategic locations and has received recognition from leading automotive OEMs for its reliability and quality, serving it as a differentiator against its competitors.

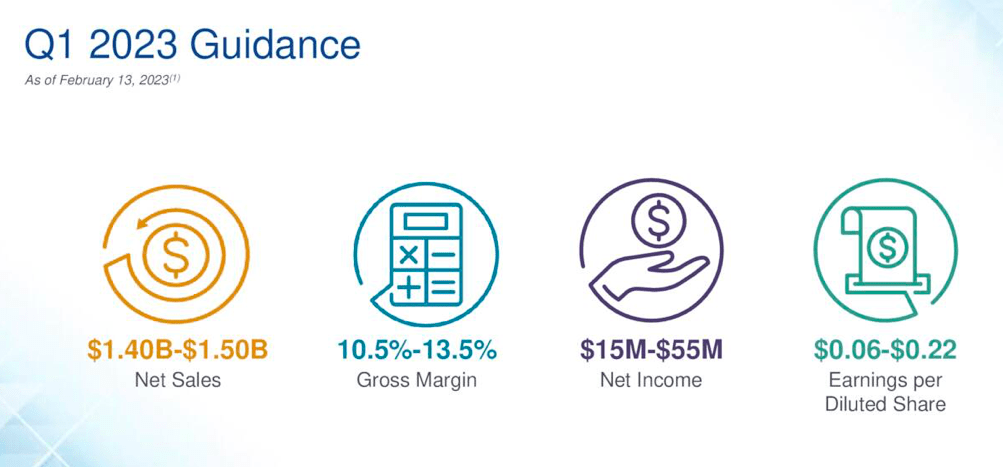

Amkor has given a first-quarter revenue guidance of $1.45 billion, representing a year-on-year decline of 9% due to the challenges in the PC/Smartphone market, consumer wearables and computing markets. In addition, the company intends to reduce its CapEx in 2023 to $800 million, about 45% of that is geared towards our facilities expansion.

Risks

According to the company, the semiconductor industry will decline by mid-single-digit percentages in 2023, but if it extends to 2024, it will affect Amkor's valuation.

Amkor Technology, Inc. relies on a complex global supply chain for its raw materials and manufacturing operations. Therefore, any disruption or delay in the supply chain due to geopolitical situations like the Russia - Ukraine war can result in a higher cost of raw materials that will affect Amkor's gross margins and impact its financial performance.

Further, Amkor Technology's exposure to currency fluctuations can affect its revenue and profitability as the value of the U.S. dollar strengthens relative to other currencies.

Valuation

Before I value Amkor Technology using a Discounted Cash Flow ("DCF") model, I will analyze Amkor's position compared to its competitors by benchmarking the company against its competition.

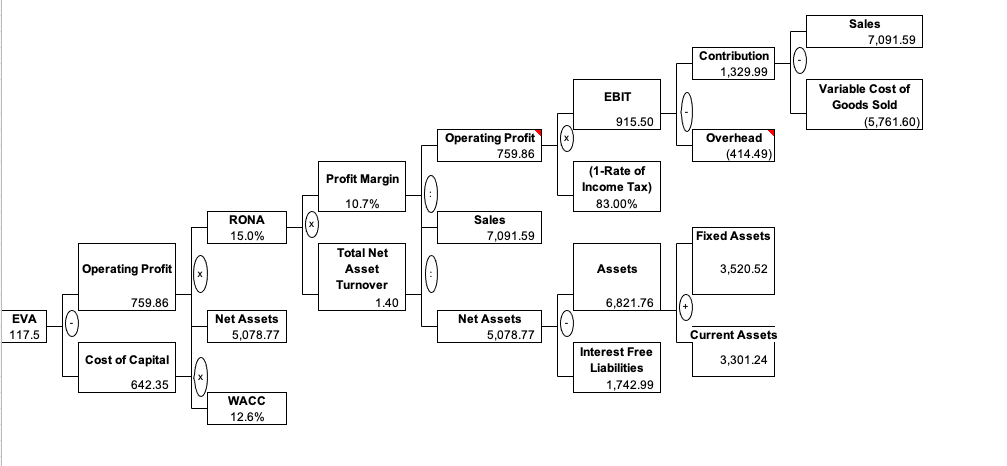

First, I look at the Economic Value Added of Amkor Technology to measure the company's economic profitability by taking into account its cost of capital and the amount of value that a company has created or destroyed by comparing the return on investment to the cost of that capital.

{kind=link}

For 2022, I arrive at $117.5 million as Economic value added for the company, indicating that it has generated more value than the Cost of its capital, which is a good sign for investors.

I identify the following companies for my analysis:

- Micron Technology ( MU )

- ASE Technology Holding ( ASX )

- Kulicke and Soffa Industries ( KLIC )

- MKS Instruments ( MKSI )

- Axcelis Technologies ( ACLS )

- Onto Innovation ( ONTO ).

{kind=link}

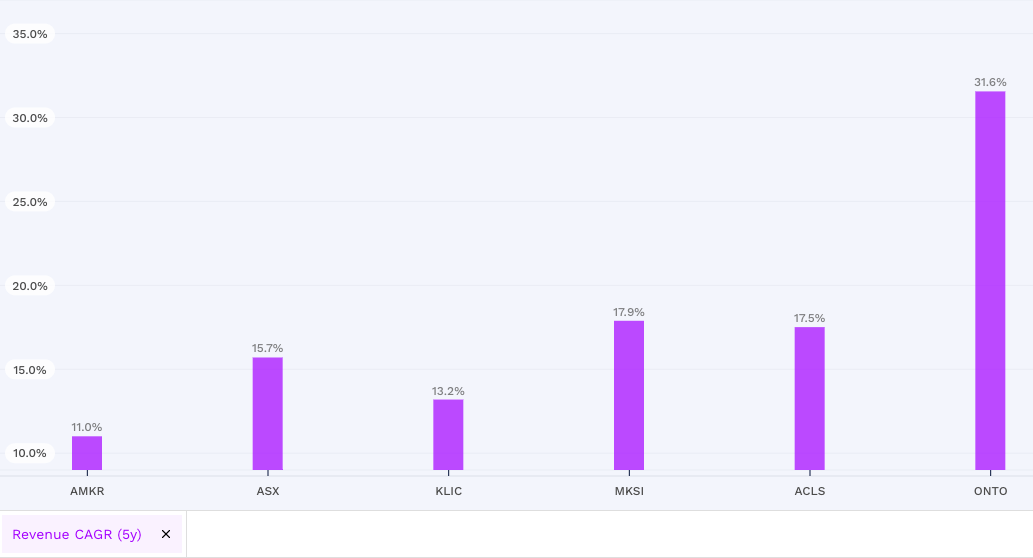

Though Amkor had an impressive revenue growth of 11% CAGR in the last five years, it still ranks below its competitors, implying that there is a potential for the company to grow more than the current rate.

{kind=link}

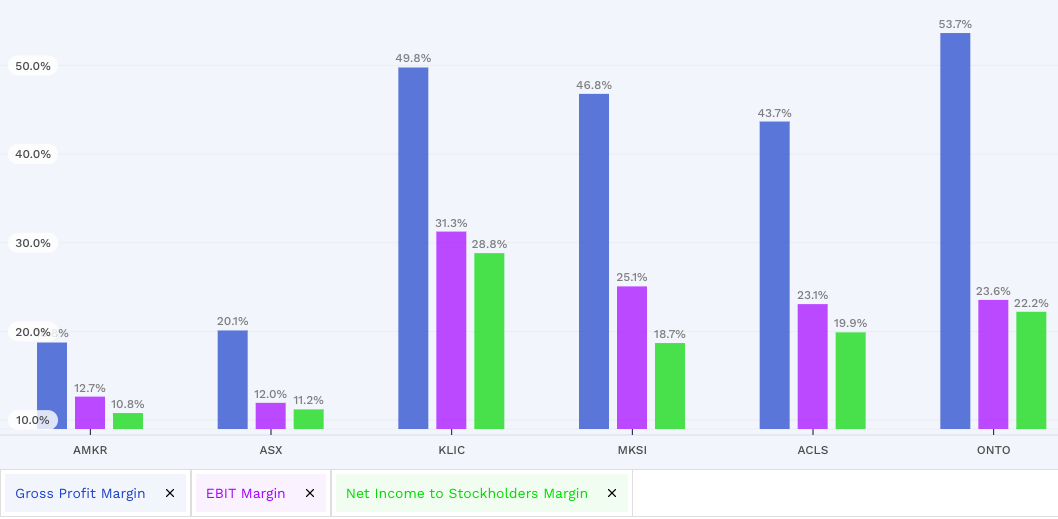

Amkor has the lowest gross margin among its peers. Though the company attributes the lower gross margin due to a slowdown in the economy and higher cost of materials, the company operates in a high-volume segment with low pricing power. Therefore, to maintain its market share, Amkor reduces prices to remain competitive, negatively impacting its gross margin.

{kind=link}

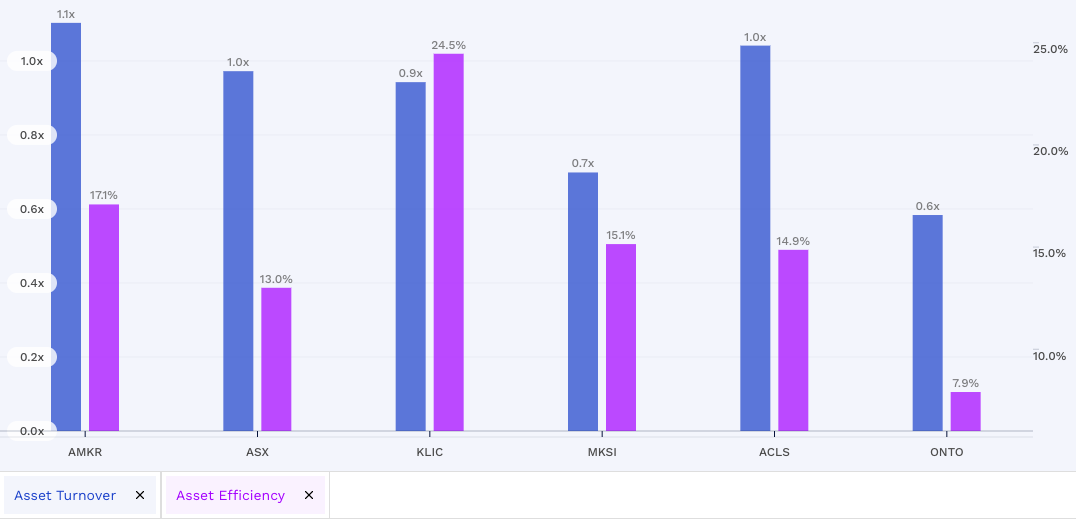

As the company operates in a high volume, and a low premium segment, it has a higher asset turnover ratio. However, the asset efficiency has reduced this year due to the higher raw materials cost and a slowing economy. I assume that this reduction in asset efficiency is an outlier and will rebound once the economy recovers in the second half of 2023.

{kind=link}

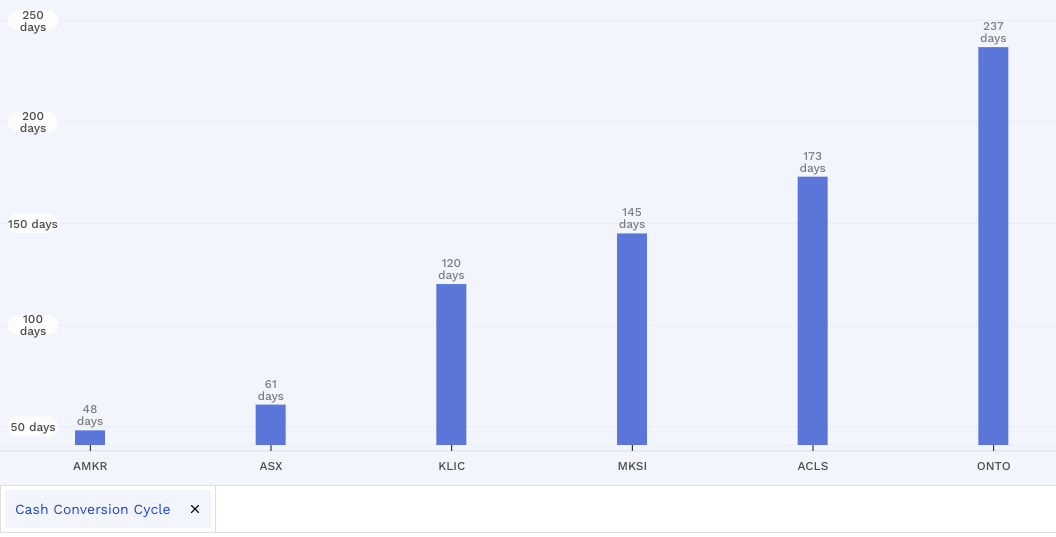

The company has a low cash conversion cycle compared to its peers, implying that it can generate cash quickly, improve liquidity, increase profitability, improve creditworthiness, and show that the company is good in inventory management.

{kind=link}

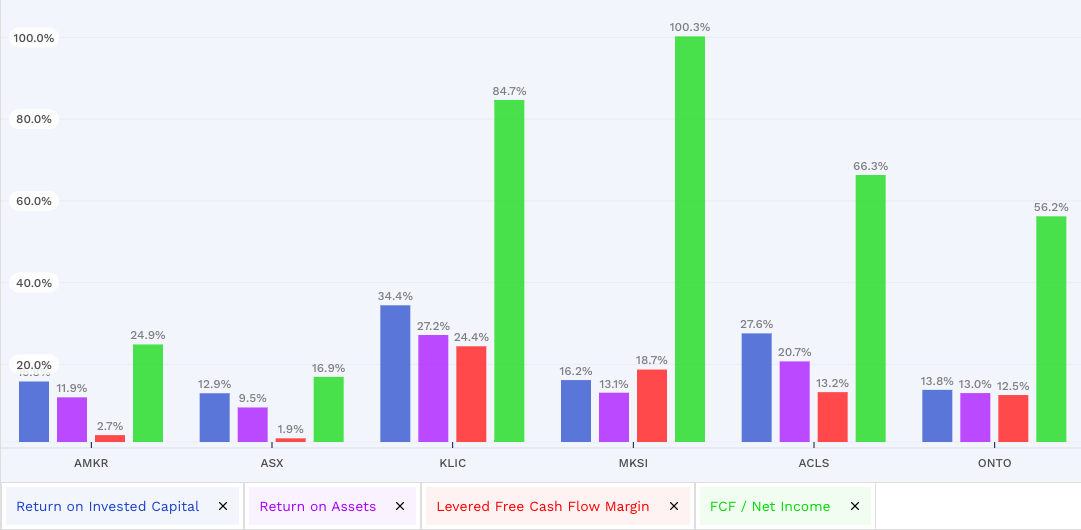

The company has a relatively better ROIC and ROA against its competitors as it generates more profit from the capital and assets it has invested in, resulting in increased earnings and better financial performance. However, there is a scope for the company to improve the free cash flow margin by reducing raw material costs, managing capital expenditures and improving its working capital management.

{kind=link}

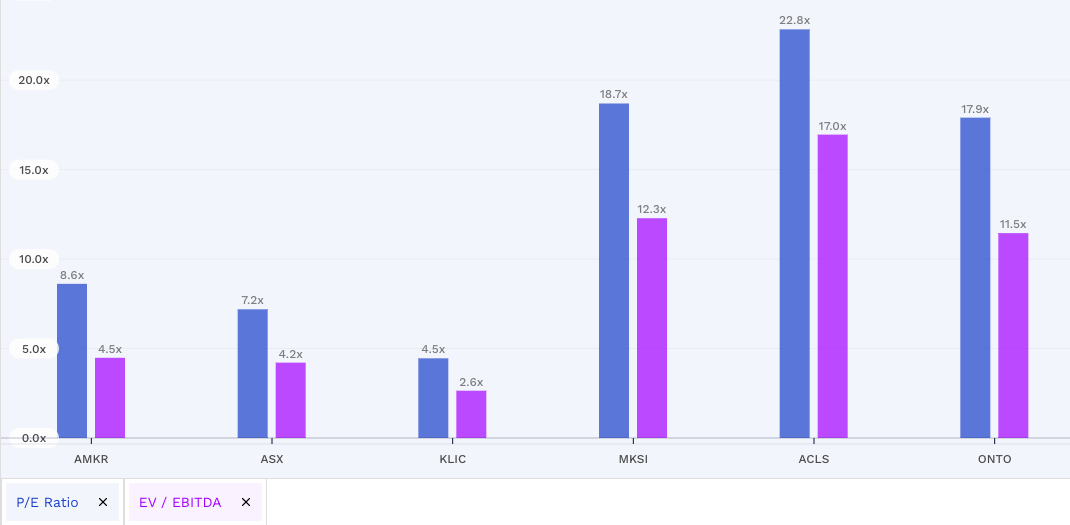

The company trades at a lower P/E and EV/EBITDA multiple against its peers despite excellent performance in the last five years. Thus, there is a higher potential for rerating its multiple in the future.

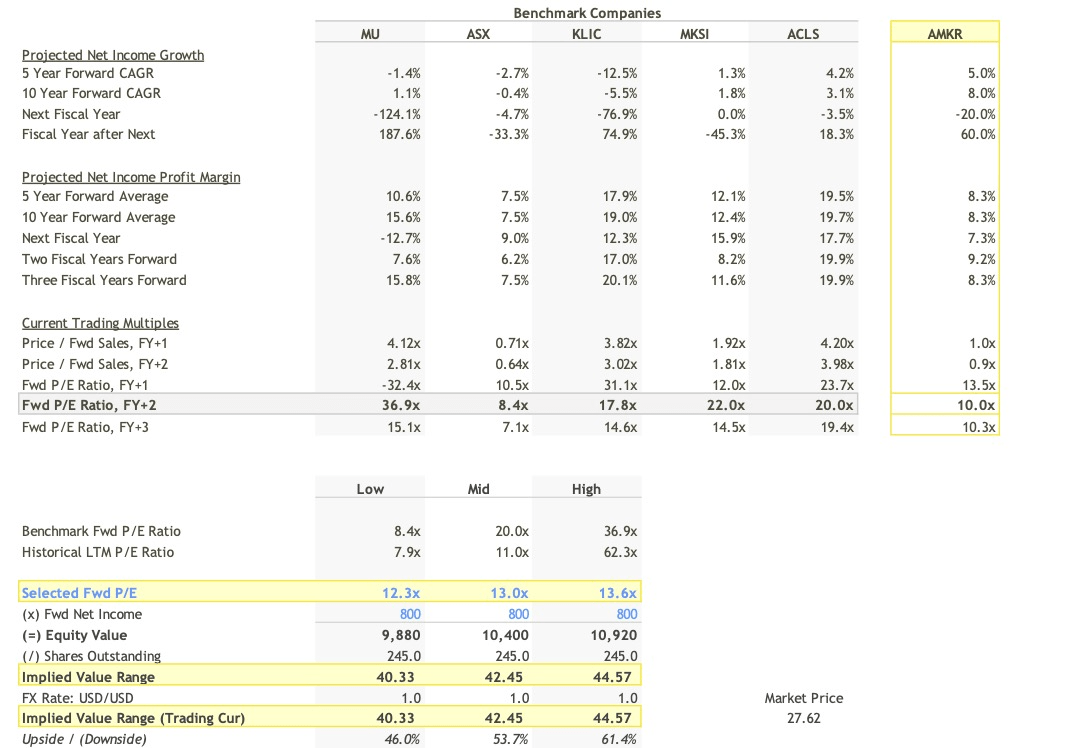

I do a comparable valuation, benchmarking the company against its peers on the P/E metric to understand whether it trades at a discount or a premium.

{kind=link}

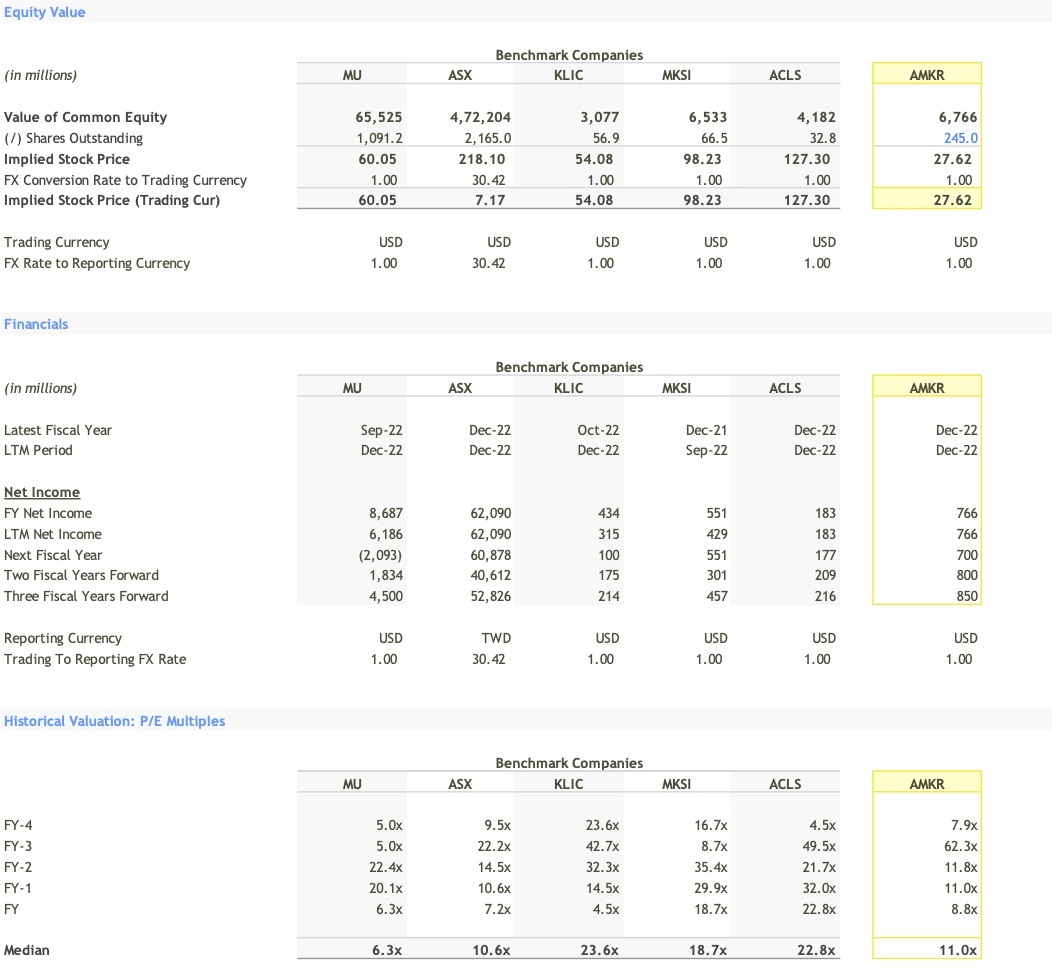

First, I look at the company's equity value and P/E multiples in the last five years and benchmark it against its peers. Then, I assume the company's net income will reduce in 2023 from $766 to $700 million but will rebound to $800 million and $850 million in 2024 and 2025.

{kind=link}

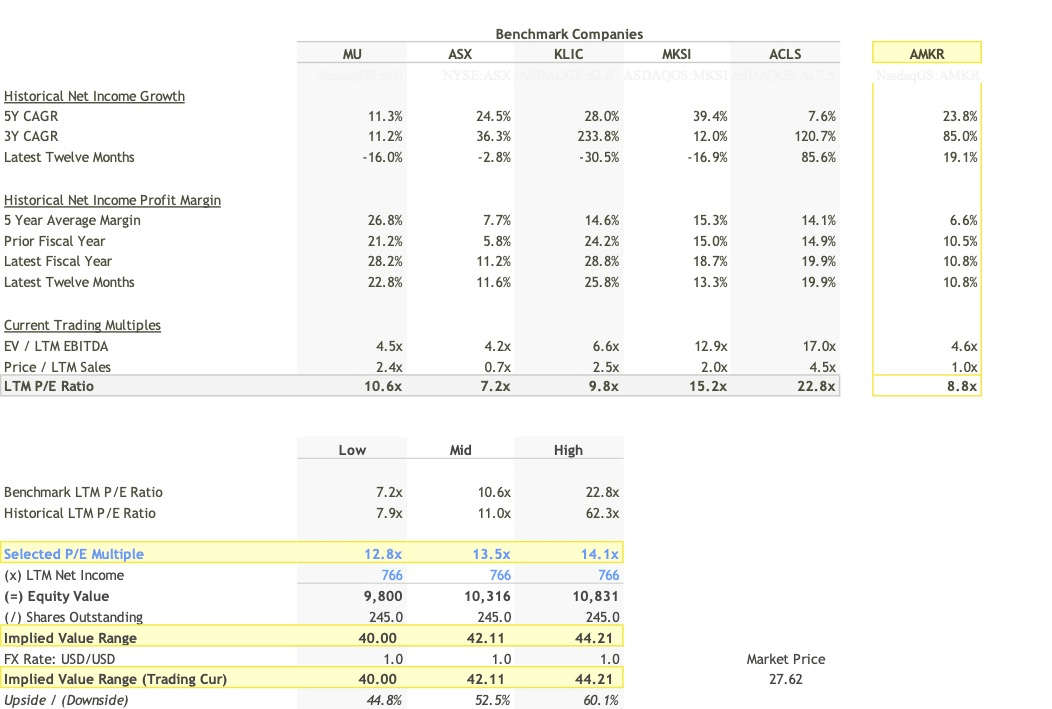

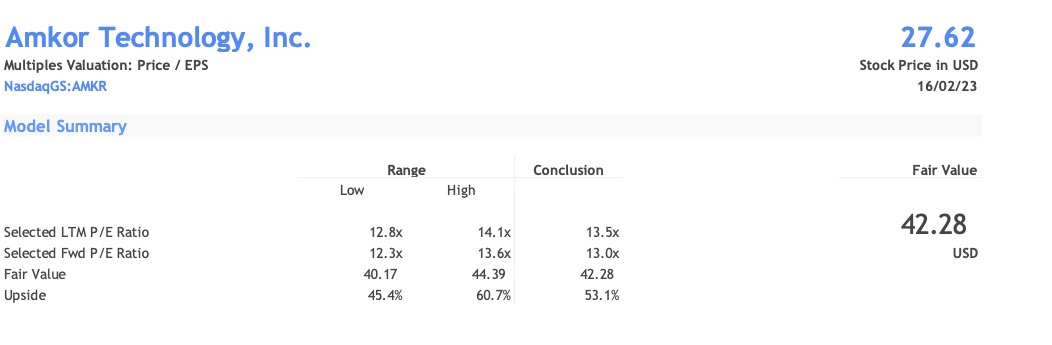

In the last three years, the company's net income grew at 85% CAGR and 23.8% CAGR in the last five years. Its five-year average net margin was 6.6% but improved to 10.8% in the last twelve months. The median P/E ratio for the industry is 24.9x, and I assume that at the multiple of 13.5x, the company's implied value is $42.1 giving it a 52.5% upside over the current trading price.

{kind=link}

For the forward P/E calculation, I assume that the net income will decline next year to $700 million but will rebound to $800 million in 2024. At 13x forward P/E and 2024 net income of $800 million, the implied value for the company is $42.45 giving it a 53.7% upside against the current trading price.

{kind=link}

I average the implied price derived from LTM P/E and forward P/E to arrive at the price of $42.2 per share for the company.

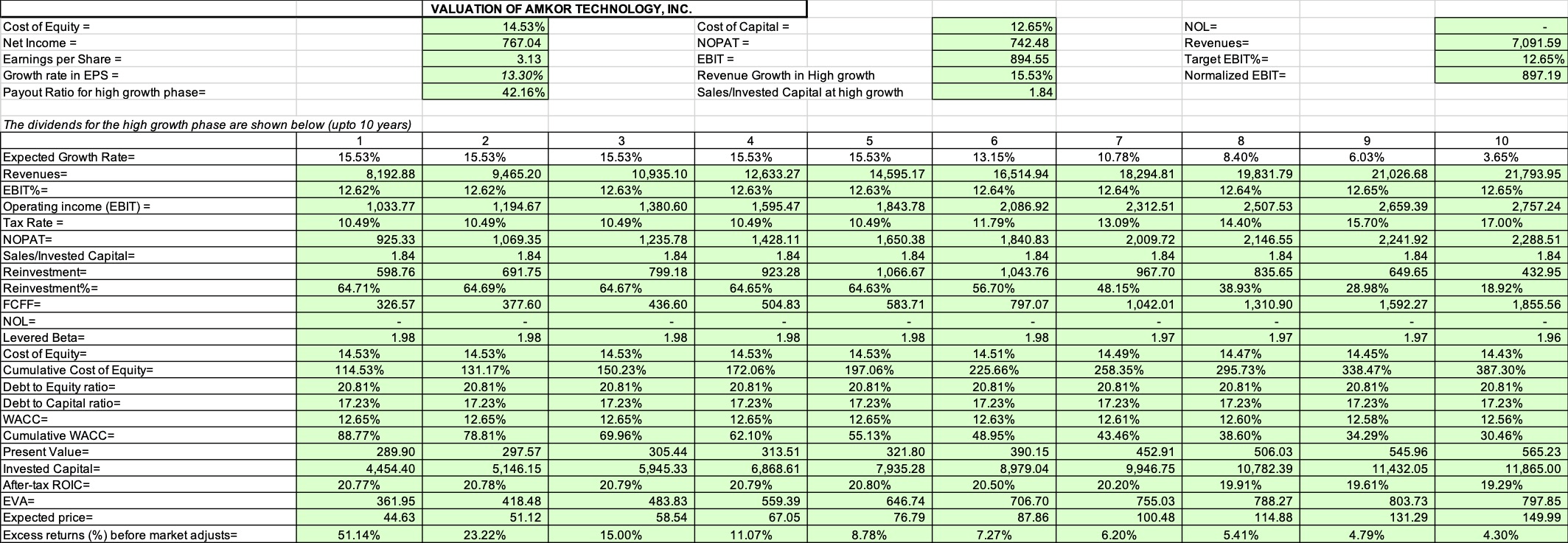

For my DCF calculation, I assume the following:

Revenues will grow at 15.5% CAGR for the next five years and 10.2% for the next ten years, as the semiconductor packaging and testing industry is expected to grow at 10% in the coming years. As a result, Amkor will outgrow the market.

The company will maintain its EBIT margin for the next ten years. The company's EBIT margin will stabilize at 12.5% over ten years despite being in the cyclical industry and having a high dependence on macroeconomic forces.

I assume the company will maintain its Sales/Invested capital at 1.84 as it has an excellent track record of higher asset turnover. Further, its new facilities in Vietnam will help the company maintain its asset turnover.

The company reported $149.5 million in R&D expenses. As R&D expenses generate future economic benefits, I capitalize the R&D expenses by amortizing them for three years.

| Year |

| R& D Expenses |

| -1 |

| 149.43 |

| -2 |

| 166.04 |

| -3 |

| 140.73 |

For each year, I add the R&D expenses to the operating income and deduct the amortization expense. I add the unamortized portion of the R&D expenses to the balance sheet .

| Year |

| R&D Expense |

| Unamortized portion |

| Amortization this year |

| Current |

| 149.43 |

| 1.00 |

| 149.43 |

| -1 |

| 149.43 |

| 0.67 |

| 99.62 |

| 49.81 |

| -2 |

| 166.04 |

| 0.33 |

| 55.35 |

| 55.35 |

| -3 |

| 140.73 |

| - |

| - |

| 46.91 |

I value the unamortized portion of R&D expenses at $304.3 million and the total amortization at $152 million.

To arrive at the Cost of capital, I assume the 10-year US treasury bond rate of 3.65% as the risk-free rate.

For equity risk premium, I use the US ERP of 5.5%.

As the company operates in the semiconductor industry, I take the bottom-up beta of 1.69, the current debt-to-capital ratio of 3.6%, and the levered beta of 1.98.

I get the company's Cost of equity as 14.53% and the Cost of debt as 3.6%.

Assigning the market weights of equity and debt at 82.77% and 17.23%, the company's WACC is 12.56%.

{kind=link}

| Estimating the value of growth |

| Value/Share |

| Value of assets in place = |

| 5,887.74 |

| 24.03 |

| Value of stable growth = |

| 237.69 |

| 0.97 |

| Value of extraordinary growth = |

| 3,614.25 |

| 14.75 |

| Value of the stock = |

| 9,739.67 |

| 39.76 |

I arrive at the company's enterprise value at $39.76 per share.

Adding cash and subtracting debt, the intrinsic equity value of the company is $9.54 billion or $38.97 per share. As a result, the company is undervalued by 44%.

Amkor Technology looks attractive at the current price on comparables and Discounted Cash flow valuation.

I conclude my analysis by stating that despite the challenging macroeconomic conditions in 2023 and low guidance for Q1 2023, the company will recover to its expected growth in the second half of 2023. Moreover, as a long-term investor, I believe that Amkor Technology, Inc.'s strength in advanced packaging technology, broad geographic footprint and strong presence in growing automotive electronics markets will help it to outgrow the semiconductor market in the future.

For further details see:

Amkor Technology: Strong Position In Semiconductor Supply Chain Offers Resilience