ET - AMLP: Wait Until Magellan-ONEOK Deal Resolution Before Buying

2023-06-19 05:54:18 ET

Summary

- The Alerian MLP ETF offers a convenient way to gain MLP exposure without the hassle of a K-1.

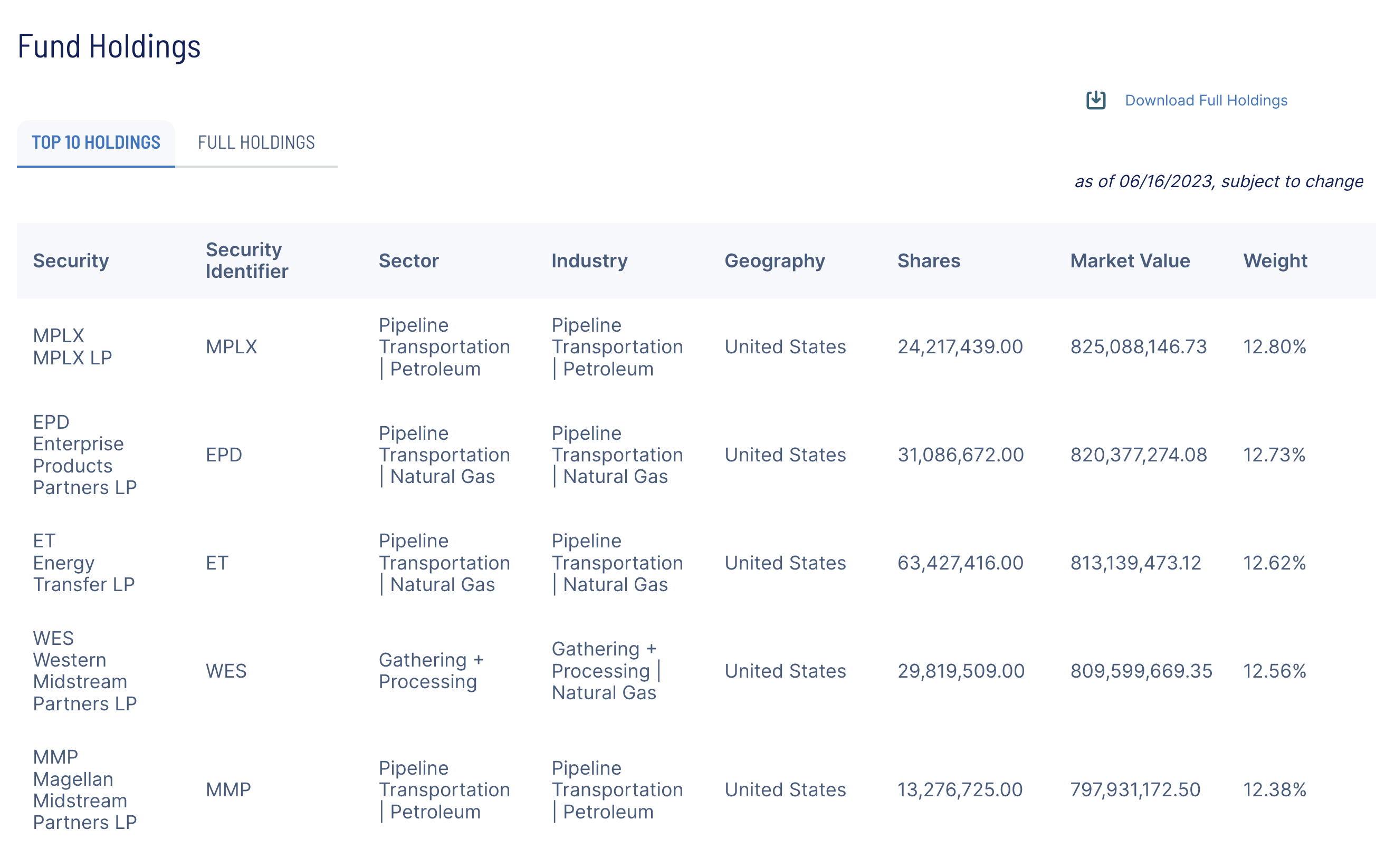

- Top holdings include MPLX, Enterprise Products Partners, Energy Transfer, Western Midstream, and Magellan Midstream, all of which the author views as top-quality names.

- The ETF is rated a "Hold" due to potential tax impact from the ONEOK-Magellan Midstream deal but will return to a 'Buy' once the deal closes or is rejected.

Back in March, I placed a buy rating on the Alerian MLP ETF ( AMLP ), saying it was a nice way to get MLP exposure without the hassle of a K-1. The ETF has returned a solid 8.8% since then, although that has trailed the overall return of the S&P 500 over the same time period. Let's take a closer look at the ETF and its top holdings.

{kind=link}

MPLX ( MPLX ) - 12.8%

Diversified midstream operator MPLX moves up to be the top holding in the AMLP ETF, up from #2 when I initially looked at. This is a great top holding in my book, as MPLX has been one of the most consistent midstream companies over the years. The company reported strong Q1 results and its outlook remains solid.

To me, MPLX offers one of the best combinations of yield, defense, and growth potential. The stock has a very attractive yield of over 9%, and its distribution is well supported with a coverage ratio of 1.6x and strong contracts anchored by its parent Marathon Petroleum ( MPC ). Meanwhile, it has a solid balance sheet at only 3.5x leverage, which is very good for the space, and it generates a lot of cash. In addition, while some midstream companies don't have many growth projects, MPLX has a very solid backlog.

For more on MPLX, see my recent article on the name.

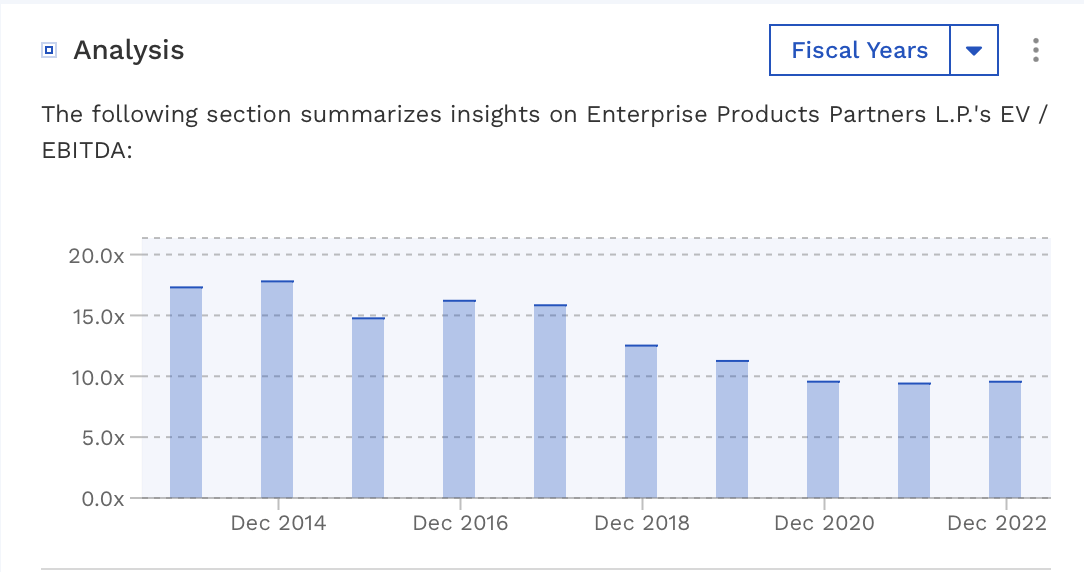

Enterprise Products Partners ( EPD ) - 12.73%

The granddaddy of midstream companies, there has arguably been no better-run midstream company over the past two decades than EPD. When other midstream companies had to cut their distributions during the most-recent energy crash, EPD was still able to boost its payout and is on track to raise it for the 25th consecutive year.

The first quarter was once again a strong one for EPD, with its distributable cash flow rising 5.5% to $1.94 billion. Its coverage ratio was a robust 1.8x, while its leverage was only 3.0x. With $3.8 billion in projects set to come online the rest of this year, EPD also has solid growth as well, although it has benefited from outsized spreads that should eventually normalize when more natural gas takeaway comes online in the Permian.

EPD is a core holding for any income-oriented investor.

Energy Transfer ( ET ) - 12.62%

While it doesn't have the consistency of MPLX or EPD, ET may have the best assets in the midstream space. Former CEO and current Chairman Kelcy Warren hasn't always played nice with LP holders in the past and has been accused of empire building. However, given the current structure of ET, unitholders are now aligned and investors are set to benefit from the midstream empire that Warren has built.

After cutting its distribution in 2020 to help repair its balance sheet, ET's latest distribution increase puts its a penny ahead of its prior $1.22 distribution on an annualized basis. With a yield of about 9.6% and trading at about 7.5x 2023 EBITDA (adjusting for the Lotus acquisition), this is a great company trading at a very attractive price.

Western Midstream ( WES ) - 12.56% Weighting

A new entrant to AMLP's top-5 holdings, WES is a gatherer and processor (G&P) primarily for its parent and Warren Buffett's favorite Occidental Petroleum ( OXY ). The company operates primarily in two basins, with about 55% of its EBITDA stemming from the Delaware Permian and nearly 30% from the DJ Basin in Colorado.

Over 93% of WES' contracts are fee-based, so it doesn't have much commodity or spread exposure. Meanwhile, over 80% of its cash flows are supported by minimum volume commitments (MVCs) or cost-of-service contracts.

WES' Delaware assets are solid and should continue to see good growth from the best basin in the U.S., while the DJ is seeing some declines. As the Permian sees some of its natural gas takeaway constraints eased, the basin should see growth pick up.

The stock looks undervalued in my view at under 8x EBITDA. For more on WES, see my earlier write-up from late March .

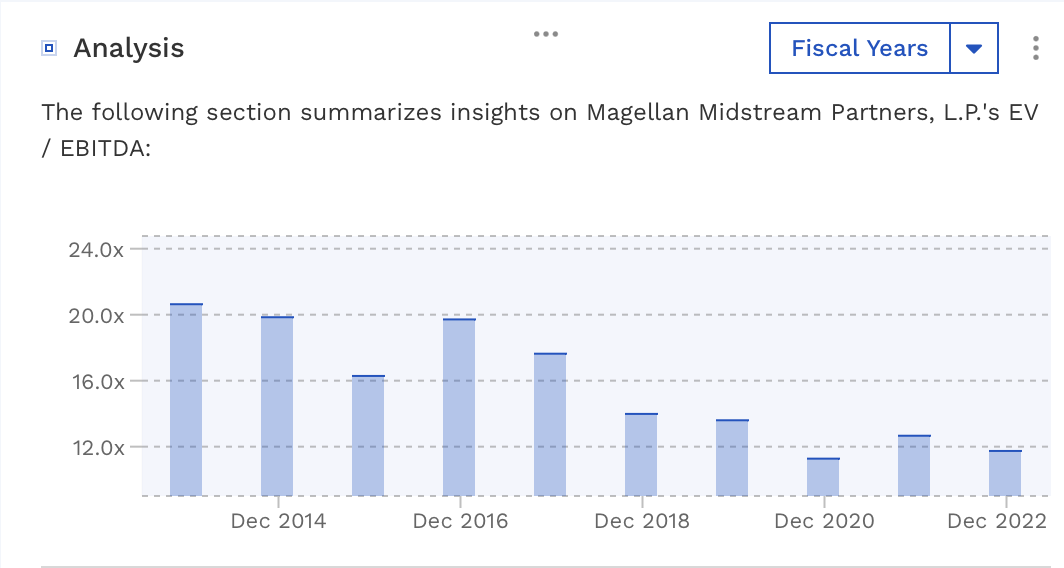

Magellan Midstream ( MMP ) - 12.38%

The big news out of MMP is that it has agreed to be acquired by ONEOK ( OKE ) in a deal that represented a 22% premium when it was announced. OKE will pay MMP unitholders 0.667 OKE shares and $25 per share in cash.

I recently wrote an article on why I believe long-term MMP holders should reject the deal. If the deal goes through, the ETF will also feel the tax impact and since OKE is not an MLP, AMLP will be forced to sell those shares.

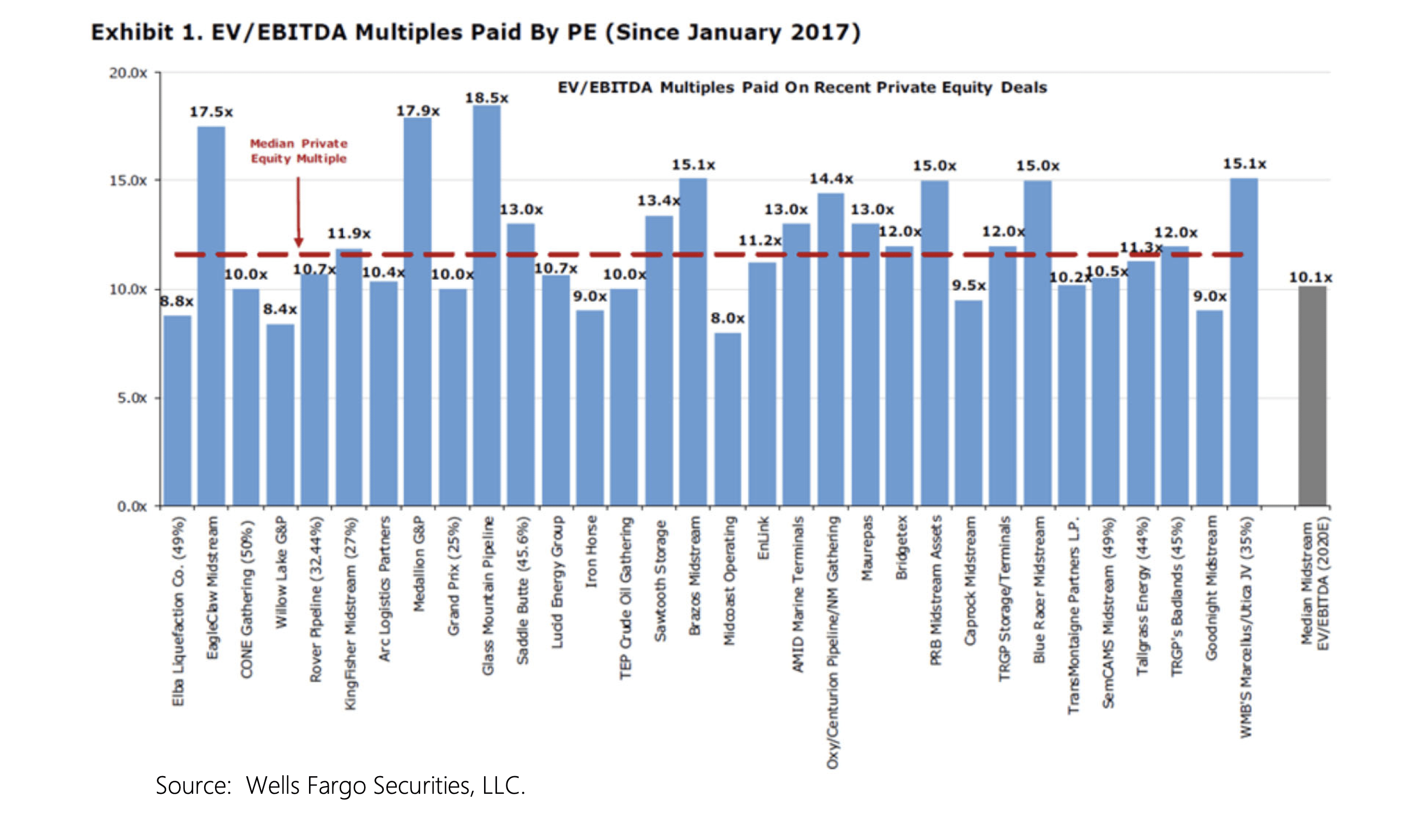

MLPs Remain Undervalued

I continue to believe midstream companies, whether structured as MLPs or C-corps, remain undervalued as a group. Quite simply, the stocks trade at lower valuation today than in the past, despite the fact that they no longer face many of the issues that the group has dealt with in the past.

{kind=link}

Before the pandemic, midstream companies would often be valued around 12x in the private markets and over 10x in the public markets. Valuations were even higher a few years before that. For example, it wasn't uncommon to see EPD or MMP trade at over 15x pre-2017.

{kind=link}

{kind=link}

Perhaps the oddest thing about the valuation compression is that midstream companies are just in much better shape today than there were several years ago when their valuations were considerably higher. Gone are the days of IDRs, which were like a huge tax (transfer of wealth) on LP investors every time a company increased its distribution when it was in the high splits. Today, most companies have eliminated their IDRs.

The IDR era also led to a period of rapid expansion, where MLPs would consistently dilute unitholders to grow. At the same time, balance sheets would also balloon, and it wasn't uncommon to see MLPs be leveraged 4.5x or even 5.0x or more. Coverage ratios were also generally paltry, barely covering the distribution and growth CapEx was solely paid for with equity and debt.

Today, leverage is typically below 4x, and in some cases lower than 3.5x or 3.0x. Coverage ratios are now generally robust, and companies look to generate free cash flow after distributions to lower debt or buy back stock. Despite that, good quality midstream companies can often be found at below 8.5x EV/EBITDA multiples.

Conclusion

While I like picking individual stocks, given the annoyance of K-1s, I think AMLP is a great option for income-oriented investors looking to avoid the hassle. The ETF has some of the best MLPs in the space as its top holdings, and I think the space in general is attractive. It currently has an 8.8% yield, and its dividend was recently raised to 86 cents from 77 cents in May.

I continue to like the AMLP ETF, but will now rate it a "Hold." The reason is that the tax impact of the OKE-MMP deal could adversely impact its NAV. The fund has been around since 2010, so it likely has been a holder of MMP for a long time. Once this is resolved, I would move it back up to a "Buy."

For further details see:

AMLP: Wait Until Magellan-ONEOK Deal Resolution Before Buying