AMRS - Amyris: Abysmal Quarter Weak Outlook Insufficient Capital - Sell

2023-03-19 21:34:56 ET

Summary

- Last week, Amyris reported another set of abysmal quarterly results, with revenues missing consensus expectations by a mile and GAAP gross margin deteriorating to new multi-year lows.

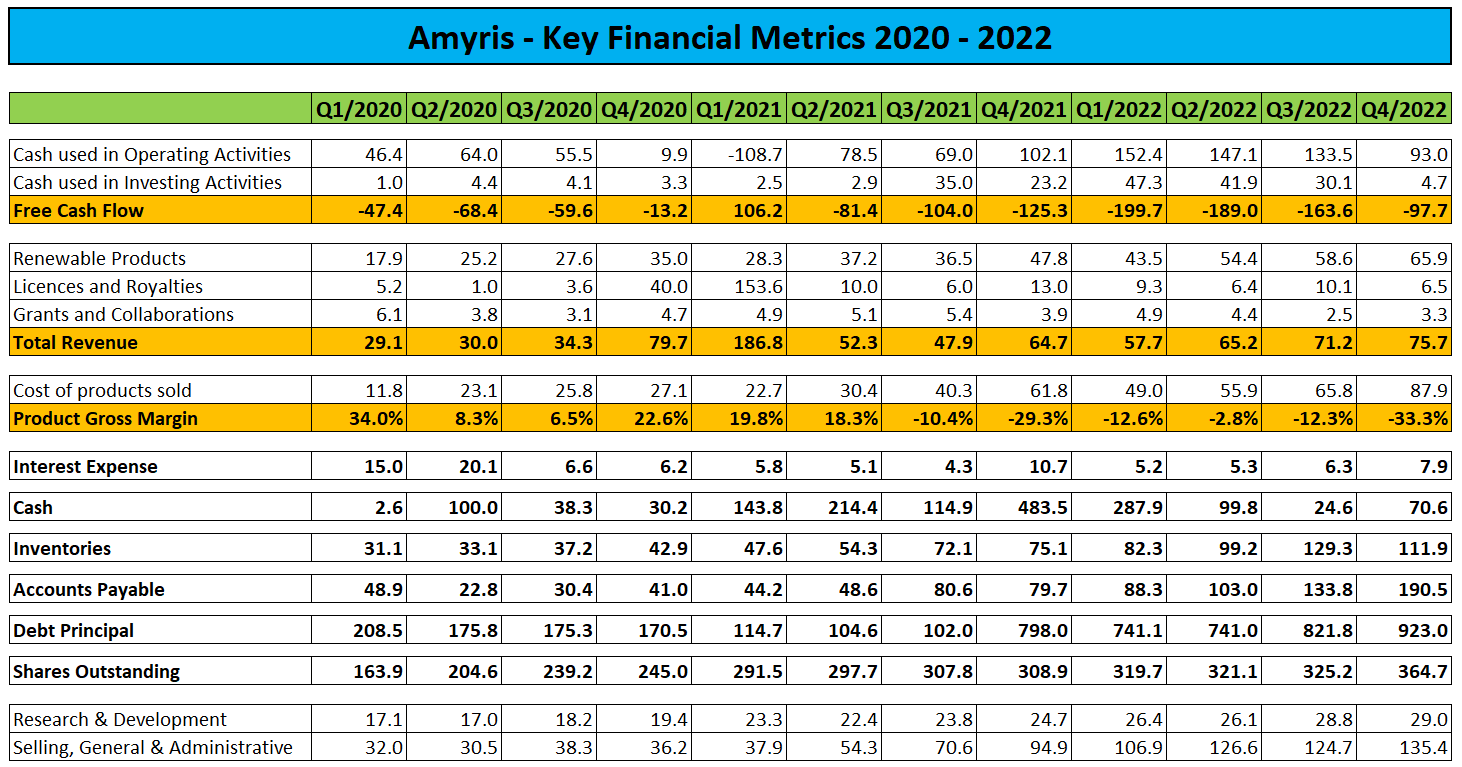

- Sequential cash burn reduction was mostly a result of ballooning accounts payable balances. For the full year, negative free cash flow amounted to $650 million.

- Annual cash usage is likely to exceed $350 million this year, substantially above management's most recent projections of between $150 million and $200 million.

- Management expects to raise substantial amounts of cash from the sale of non-core consumer brands and the contribution of ingredient manufacturing assets to a new joint venture but investors should take these projections with a huge grain of salt, particularly in the current market environment.

- Given the likely requirement to raise more capital over the course of this year, investors should continue to avoid the shares or even consider selling existing positions.

Note:

I have covered Amyris, Inc. ( AMRS ) previously, so investors should view this as an update to my earlier articles on the company.

Last week, cash-strapped specialty renewable products developer Amyris reported another set of abysmal quarterly results with revenues missing consensus expectations by a mile and gross margins deteriorating to new multi-year lows.

{kind=link}

That said, on the conference call management claimed year-over-year progress in " non-GAAP gross margins " when adjusted for the impact of license revenues:

Non-GAAP gross margin was $21.4 million or 28% of revenue compared to $22 million or 34% of revenue in Q4 2021. Excluding the impact of technology license revenue in both periods, non-GAAP gross margin increased by nearly $6 million and was 400 basis points higher as a percent of revenue than in the prior year. This was primarily due to consumer revenue growth and improved consumer margins.

Company Presentation

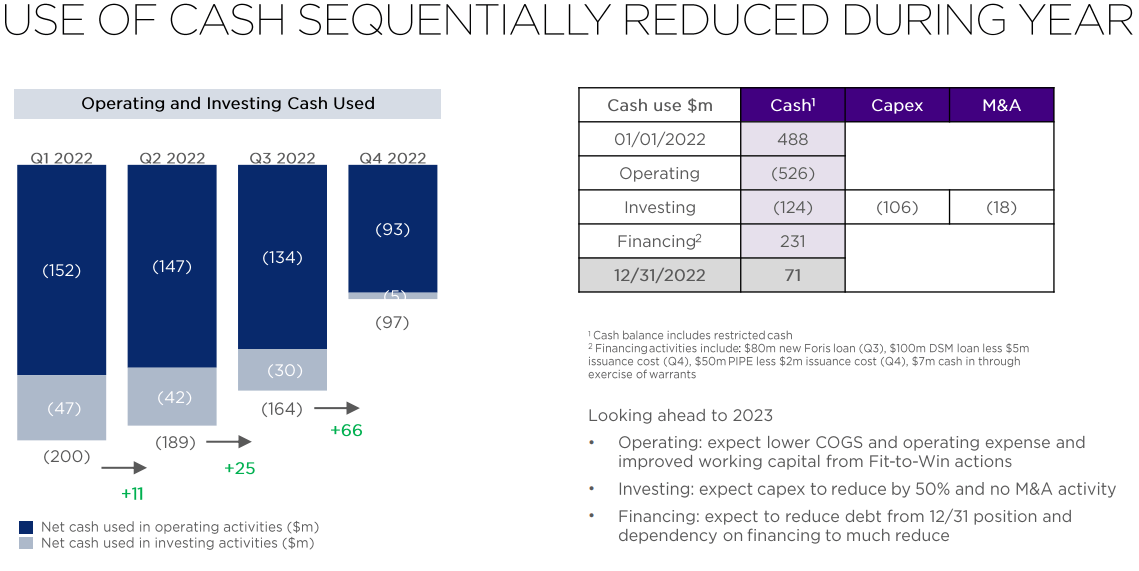

In addition, management touted a substantial reduction in quarterly cash burn, but this was almost solely achieved by increasing accounts payable more than 40% quarter-over-quarter. In addition, cash usage benefited from a meaningful sequential reduction in inventories:

{kind=link}

For the full year, negative free cash flow was an eye-catching $650 million.

Following a $50 million emergency capital raise on December 29, Amyris finished Q4 with $64.4 million in unrestricted cash and $923 million in outstanding debt principal.

On the conference call, management cut back on its recently stated target to reduce 2023 cash burn to a range of $150 million to $200 million (emphasis added by author).

We intend to bring our operating cash use in 2023 to around $200 million run-rate by the end of 2023 (...).

We are delivering this reduction in cash use through our Fit to Win agenda, portfolio rationalization of non-core assets along with ensuring we have the right size organization for supporting our lean and focused future. We are also expanding our gross margin this year through the manufacturing cost savings in the Fit to Win agenda, but also through the Givaudan earn-out and the underlying growth of our Flavors & Fragrance business and the impact this has on the DSM earn-out. Taken together, we expect these actions will enable us to meet our objective of ending 2023 as a growing self-sufficient enterprise with a capacity to fund its growth.

Please note that this guidance does not take into account $55 million in projected capital expenditures. Assuming $100 million in cash use from operating activities in Q1 and cash usage gradually declining to $50 million in Q4, cash burn from operations would amount to $300 million this year.

Adding the above-discussed $55 million in capital expenditures would result in negative free cash flow of $355 million for 2023.

Given the likely requirement to bring down elevated accounts payable balances, my cash burn assumptions could easily prove too generous.

While management expects to receive a $200 million upfront cash payment from the recently announced strategic transaction with Givaudan within the next 30 to 45 days, approximately $50 million will have to be utilized for acquiring an additional 49% in the company's Aprinnova joint venture from subsidiaries of Japanese Nikkol Group as the joint venture's manufacturing facility in North Carolina is required for converting Biofene into squalane and other final products.

Applying my above-discussed $355 million cash burn estimate and considering the company's year-end cash position of close to $65 million as well as approximately $150 million in net upfront cash proceeds from the Givaudan transaction, Amyris would have to raise at least $140 million in additional capital to make it into next year.

However, this number does not yet account for $128.7 million in short-term debt maturities and an additional $15 million recently borrowed from an entity affiliated with key shareholder John Doerr.

On the conference call, management projected around $150 million in cash proceeds from the sale of non-core consumer brands (emphasis added by author):

We are narrowing our investments to where we have and can’t extend market leadership and sustainable predictable growth, which includes the gross margin increase I mentioned earlier. We are further focusing our consumer brand portfolio and expect to end with 5 to 6 brands that our market leaders represent over 90% of our current revenue and growth, use a lot of our ingredients and their formulations and have a clear path to profitability. This additional rationalization of non-core assets in our consumer portfolio is expected to generate around $150 million of cash proceeds this year. The brands that remain in our portfolio have a current market value of around $2 billion. We are in active discussions with potential buyers for these non-core assets that we are in the process of selling. In parallel, we will reduce and eliminate all other spend through further divestments and deep prioritization of where we invest our limited dollars.

In addition, management hinted to a potential joint venture with one of the world's top four sugar producers which I would assume to be Raízen given the fact that the company's sugar mill is also located in Barra Bonita and provides feedstock to Amyris' newly-constructed ingredients manufacturing plant (emphasis added by author):

(...) We have been approached and are in active discussions regarding a manufacturing joint venture. We are exploring this opportunity with one of the world’s top four sugar producers, a mill about the size of Barra Bonita. The proposed JV structure would combine some of our biomanufacturing assets would we lease a significant amount of cash from our current production assets and the partner would fund the next biomanufacturing facility and downstream processing facilities. They have completed initial diligence and are impressed with what we have built at Barra Bonita and the quality of our teams and overall capability. (...)

Biomanufacturing consumes the most significant amount of our working capital and has a long cash cycle time. (...)

In addition to fully funding our much needed next production facility, this opportunity can also help generate $50 million to $100 million in new cash to our balance sheet in the short-term and free up $50 million of current working capital that is used to support our ingredients business. If discussions continue as planned, then we expect this facility to be in construction by the end of this year and be the 100% farnesene dedicated biomanufacturing facility.

Reading between the lines, the company is likely to contribute its new Barra Bonita facility against an upfront cash payment of up to $100 million with the joint venture partner taking over responsibility for working capital and expansion capex requirements. Including the anticipated working capital release, Amyris expects up to $150 million in near-term cash benefits from this transaction.

But given what happened to the much-touted strategic transaction with Givaudan in recent months, investors would be well-served to take these projections with a huge grain of salt.

To be perfectly honest, I would be surprised to see Amyris generating material cash proceeds from the sale of non-core brands which in aggregate accounted for just 10% of the company's consumer revenues this year.

Considering the current market environment and Amyris' very weak bargaining position, I do not expect proceeds from the upcoming consolidation of the company's consumer brands portfolio to be anywhere close to the " up to $150 million " envisioned by management.

In addition, investors shouldn't bet on the advertised manufacturing joint venture to be up and running anytime soon as negotiations and subsequent paperwork finalization will take time. Moreover, with Amyris being desperate for cash, the joint venture partner appears to hold all the aces.

Given these issues, I do not expect material near-term cash benefits from the above-discussed transactions which would likely result in the requirement to raise a substantial amount of new capital over the course of this year.

During the quarter, ongoing liquidity challenges resulted in further delays to the commissioning of the Barra Bonita plant and inability to fulfill over $14 million in ingredient product orders.

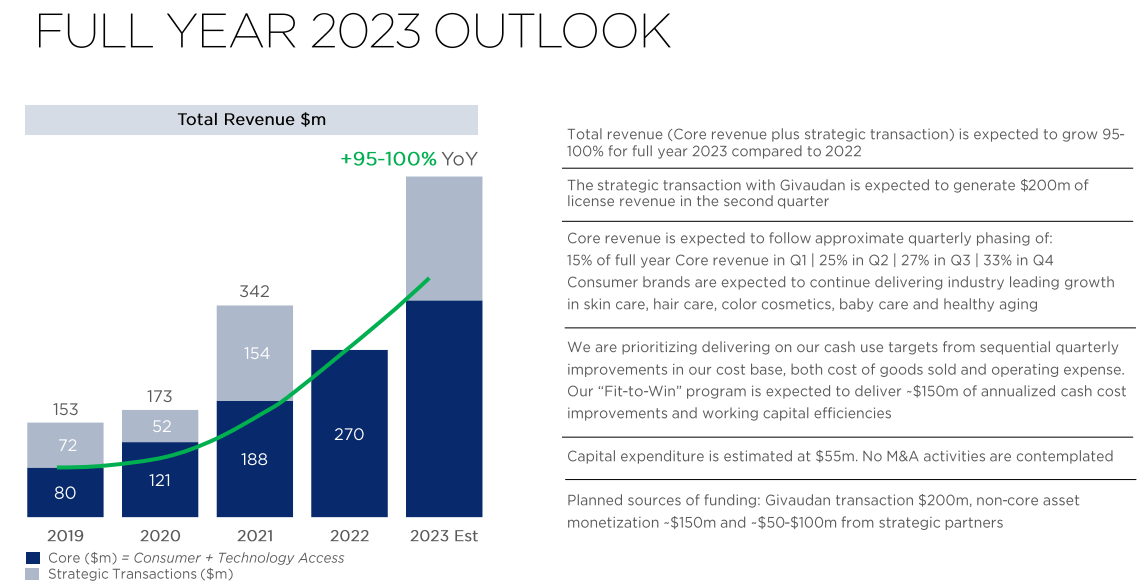

As Amyris is looking to sell non-core assets and cutting back on marketing spend, core revenue growth going forward will be a far cry from management's previous projections:

{kind=link}

Please note that the 95% to 100% projected revenue growth in the slide above includes the $200 million upfront payment from Givaudan.

Adjusted for the strategic transaction, 2023 core revenue guidance translates to just $325 million to $340 million or 21% to 26% year-over-year growth as compared to these projections provided by CEO John Melo on the company's Q3 conference call in November (emphasis added by author):

Our goal is to deliver 10% operating income on an estimated $200 million of revenue in the fourth quarter of 2023. We expect this to be our first solid quarter of operating profitability for our core business based on maintaining our current growth rate and delivering on our Fit to Win initiatives.

We expect over 10% operating income for full year 2024 and expanding that to over 20% operating income by 2025 with a goal of more than $1 billion in revenue during 2025.

Suffice to say, Q4/2023 revenues won't be anywhere close to $200 million, not to speak of profitability. Generously assuming 25% core revenue growth going forward, Amyris' 2025 core revenues would come in around $530 million.

Not surprisingly, analysts have cut price targets across the board citing substantially reduced growth expectations.

Bottom Line

Following an abysmal 2022, renewed capital constraints have forced Amyris to focus on consolidating its customer brand portfolio and cutting back on marketing spend.

As a result, the company's growth trajectory is expected to take a major hit going forward.

In addition, Amyris' 2023 cash usage will be substantially above the $150 million to $200 million number provided by management on the J.P. Morgan Healthcare conference in January, thus likely requiring the company to raise additional capital later this year.

While management expects up to $300 million in cash proceeds and working capital relief from the sale of non-core brands and the potential formation of a new ingredient manufacturing joint venture, investors would be well-served to take these projections with a huge grain of salt, particularly given the current market environment.

As the company's distressed financial condition is limiting access to the capital markets, Amyris is likely to remain on life support by 30% shareholder John Doerr for the time being.

After initially dropping to new all-time lows below $1, shares rallied approximately 30% over the course of Thursday's session as market participants apparently cheered management's stated decision to no longer sacrifice profitability for growth going forward.

Unfortunately, Amyris' management has never delivered upon any sort of financial guidance provided in recent years and I do not expect this pattern to change going forward.

Given the likely requirement to raise a substantial amount of capital over the course of this year, investors should continue to avoid the shares or even consider selling existing positions.

For further details see:

Amyris: Abysmal Quarter, Weak Outlook, Insufficient Capital - Sell