AMRS - Amyris: Consumer Business Cost Breakdown

Summary

- Supply chain problems appear to have caused elevated COGS and shipping and handling expenses, a problem faced by many beauty brands and DTC companies.

- Insourcing production and changing packaging will resolve some of these issues and help improve profitability.

- Amyris has invested heavily in their consumer business over the past few years and must scale revenue to realize the benefits of these investments.

Amyris’ ( AMRS ) consumer business is scaling rapidly, but the economics are not currently clear. Elevated expenses, due to supply chain issues, and heavy investments in new brands have created extremely poor consumer margins. This should begin to change going forward, as existing brands continue to scale and three new brands are launched in Q4 2022. Amyris is controlling costs by insourcing production, reducing packaging costs and moderating marketing spending. In addition, the pace of hiring has slowed which will result in operating leverage as revenue continues to grow. The consumer business should become profitable over the next 12-18 months, which could dramatically change Amyris’ share price, provided they can access the cash to reach this point.

Consumer COGS

Amyris' consumer COGS are driven by a mix of ingredients, freight, packaging and channel specific distribution costs, with fermented ingredients a relatively small component. Packaging currently accounts for two thirds of COGS for Biossance and ingredients less than a third. Amyris is in the process of simplifying packaging, which they expect to remove 30-40% of packaging costs. Amyris has stated that this change should reduce consumer COGS by 5 million USD in the second half of 2022 and 30 million USD in 2023. Changes have already been implemented for Biossance, with John Melo stating that COGS have been reduced by 50% .

It is unclear how much Amyris’ consumer COGS have been impacted by packaging material inflation, but a range of materials like glass, paper and plastics have witnessed large price increases over the past 1-2 years. This is an industry wide problem, with many beauty brands and DTC companies suffering a deterioration in gross profit margins due to cost inflation. For example, Revlon (REVRQ) has had difficulties meeting customer demand, due to an inability to source a sufficient and regular supply of raw materials. Procter & Gamble ( PG ) and Unilever ( UL ) have passed through higher prices to consumers in a number of categories, including grooming, skincare, and feminine care. e.l.f. Beauty ( ELF ) has also had to raise prices in response to higher costs.

Amyris’ focus on ESG extends to the choice of packaging for their consumer brands, which may be contributing to margin problems. They have worked to replace non-recyclable materials with recycled plastics and bottles manufactured using sugarcane ethanol instead of petroleum derived energy sources. The outer boxes of many products are also made from sugarcane pulp. Amyris also makes extensive use of glass in packaging and in some cases designs containers to be refilled. It is unclear whether this focus on sustainability has contributed to elevated costs, but Amyris’ focus on the prestige segment has certainly led to higher costs through packaging design and materials. This provides an easy opportunity to cut costs, provided that consumer perception of the brands is not affected.

It is unknown how much input costs and freight have impacted consumer margins in recent quarters, but Biossance is likely indicative. In the past, Amyris has suggested that Biossance’s blended gross margins were fairly constant at around 70%. In the second quarter of 2022, Biossance’s gross margins were in the mid-60s , and while this deterioration may be at least in part due to channel mix, it is also likely the result of inflation.

Amyris is in the process of insourcing manufacturing for their consumer products, with the goal of reducing costs and making their supply chain more resilient. Consumer manufacturing is expected to be at least 70% in Amyris controlled factories by the fourth quarter of 2022. The combination of this, and moving to Amyris controlled fulfillment, is expected to add 5-10% to consumer gross margins. At the end of the first quarter of 2022, Amyris already had 10% of their highest volume products in production at their facility in Reno. This facility has a capacity of 50 million units a year on one shift.

Amyris has a 10-year manufacturing partnership agreement with Renfield Manufacturing to provide manufacturing services and third-party logistics processes, including inventory management, warehousing and fulfillment at the Reno facility. Amyris will pay Renfield a series of fixed payments totaling 37.4 million USD and variable payments for products manufactured and/or fulfilled on a cost-plus basis. This arrangement introduces operating leverage into the consumer business, and could cause elevated expenses during the start-up phase, when the facility is operating sub-scale.

Amyris is also insourcing consumer manufacturing in Brazil, with an expectation of lowering costs. Amyris acquired Interfaces for a total of 6.7 million USD in 2022. Interfaces specializes in the production of cosmetics for skin care, hair care, and makeup. The acquisition of Interfaces will support growth, add operational resilience to Amyris' supply chain, reduce its dependency on third-party manufacturing, and increase the ability to source strategic components. The Brazilian facility has an annual capacity of 36 million units on one shift.

Amyris plans to consolidate production of a large part of its consumer portfolio at its two plants, in addition to simplifying components and packaging. This is expected to reduce consumer COGS by 5 million USD in the second half of 2022 (2.5% improvement in gross margins) and 30 million USD in 2023 (5% improvement in gross margins). Amyris is not insourcing all consumer manufacturing though, as some products are unique and their volumes do not justify the required capital investments. These two facilities should be sufficient to support Amyris’ consumer business for the foreseeable future.

Channel mix is likely to be a drag on gross margins going forward as Amyris is in the process of dramatically expanding its brick-and-mortar presence and wholesale gross profit margins are typically around 20% lower than direct-to-consumer margins. While this may appear to be a headwind, the overall impact is likely to be muted as DTC causes relatively high shipping and handling expenses, which are currently captured under SG&A.

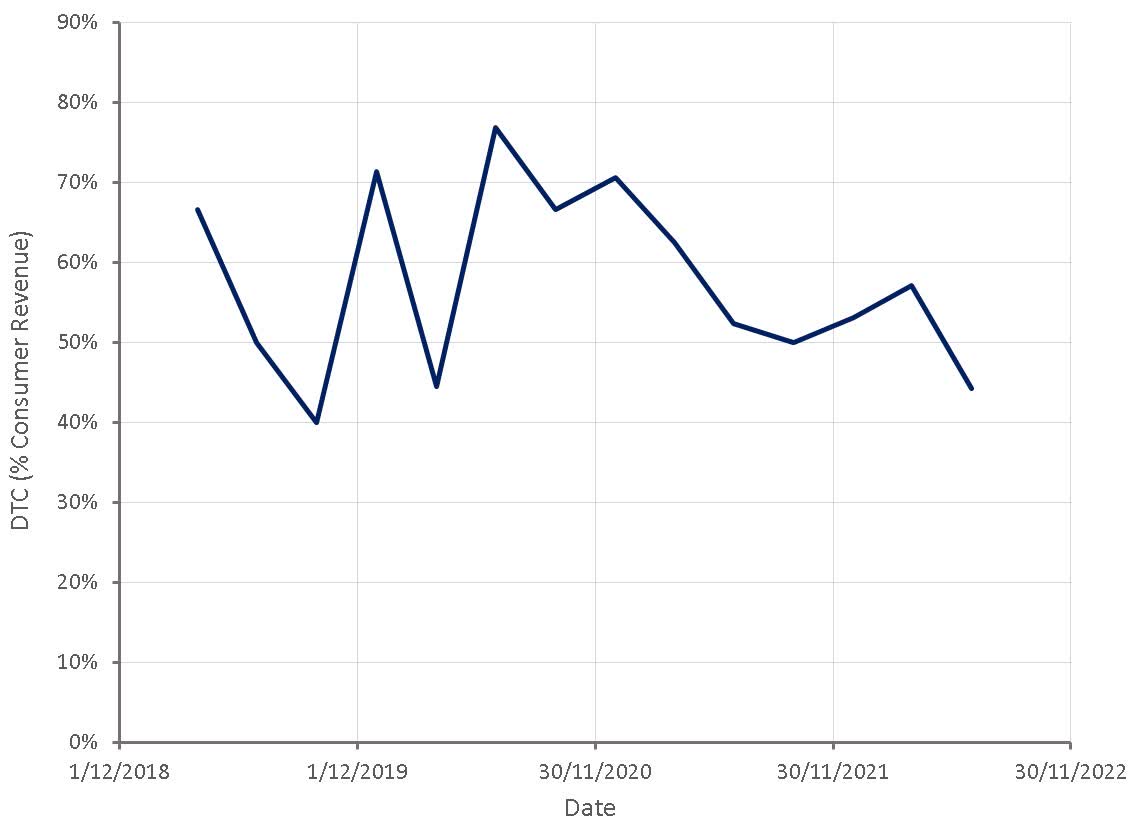

Figure 1: Amyris Retail Doors (source: www.reddit.com/r/Amyris) Figure 2: Amyris DTC Revenue (% Consumer Revenue) (source: Created by author using data from Amyris)

{kind=link}

Amyris has a mix of brands in their portfolio, ranging from luxury to prestige and mass market. Each of these segments will have their own margin profile and hence their mix in Amyris’ brand portfolio will also impact consumer gross profit margins. Most of Amyris’ revenue currently falls into the prestige segment, but with the launch of 4U by Tia and increasing distribution for Pipette and Purecane, this could change over time.

Table 1: Typical Gross Profit Margins by Market Segment (source: Created by author)

Freight

Consumer gross margins have also been negatively impacted by higher freight rates, due to Amyris primarily sourcing packaging from Asia. Lockdowns in China and supply chain issues appear to have forced Amyris to air freight packaging at considerable expense over the past 12 months.

An analyst on the Q3 2021 earnings call suggested that Amyris could air freight the materials required to meet previous earnings guidance, with a potential 20% hit to margins on those sales. Melo responded that they had looked into leasing 747s for this purpose, and that the impact would be more than the suggested 20%. According to The World Bank , air freight is typically priced 4–5 times that of road transport and 12–16 times that of sea transport.

Despite the massive impact to Amyris’ bottom-line, they have utilized a significant amount of air freight in each of the past 3 quarters. There appears to have been a reluctance to forgo sales, regardless of the cost, with inbound air freight used to ensure the supply of components, packaging and intermediate products. Amyris has built inventory, and supply chain constraints are easing, meaning air freight should be less of an issue going forward.

Table 2: Amyris Air Freight Expenses (source: Created by author using data from Amyris)

{kind=link}

Shipping And Handling

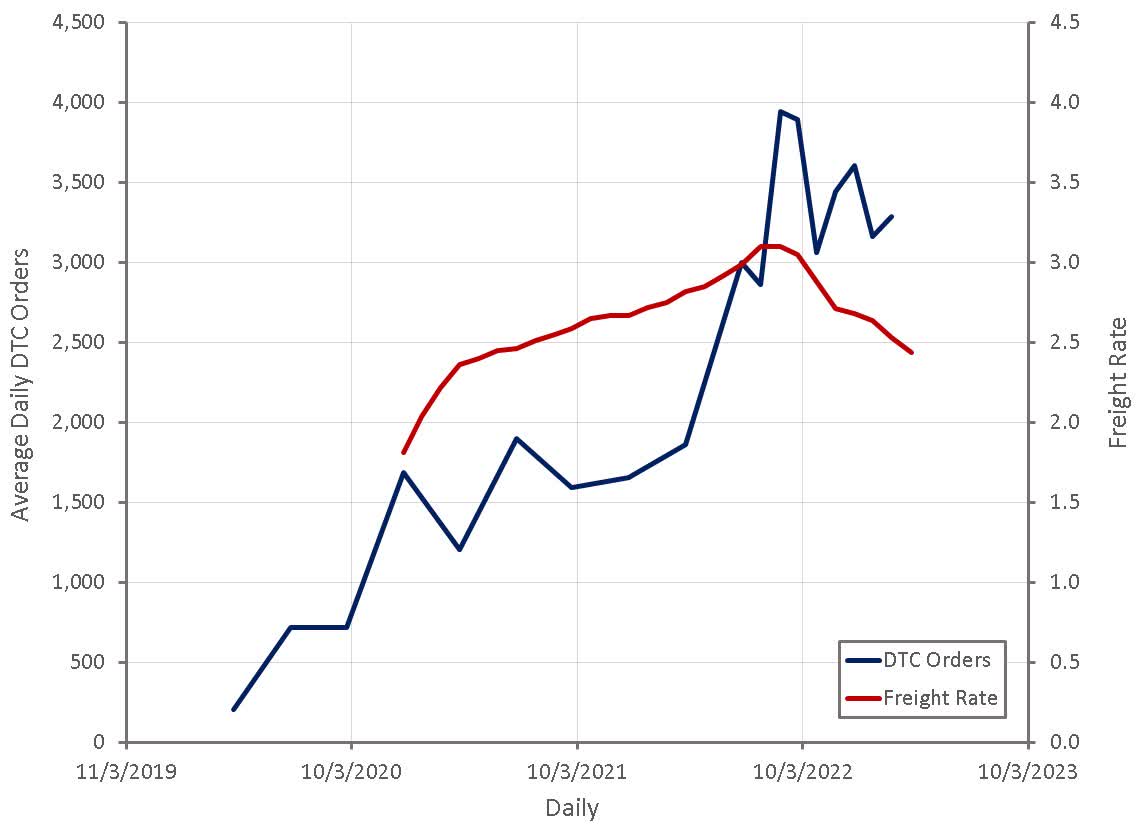

Shipping and handling expenses are primarily related to the DTC business and have exploded due to a combination of higher third-party costs, higher freight costs and a dramatic increase in volumes.

Figure 3: Amyris DTC Orders and US Freight Rates (source: Created by author using data from Reddit and www.dat.com/trendlines)

{kind=link}

Data indicates that the last mile of product delivery can account for 53% of total shipping expenses , and costs an average of 10 USD per package. Shipping and fulfillment expenses often amount to 15-20% of net sales , even without supply chain issues.

Amyris has not given total shipping and handling expenses, but in Q2 2022 indicated that shipping and handling costs had increased by 6 million USD versus the same quarter of the previous year. This cost is primarily associated with the DTC business, which increased revenue by approximately 8 million USD over the same period. Assuming a 30% increase in freight rates and a 120% increase in volumes over this period, shipping and handling expenses would have increased from 3.2 million USD to 9.2 million USD. A return to normal freight prices could therefore result in something like a 3 million USD per quarter cost saving. This is somewhat difficult to assess though, as the cost drivers for the pick and pack component of expenses will be different to those for the shipping component. Shipping is likely to constitute the majority of shipping and handling expenses though.

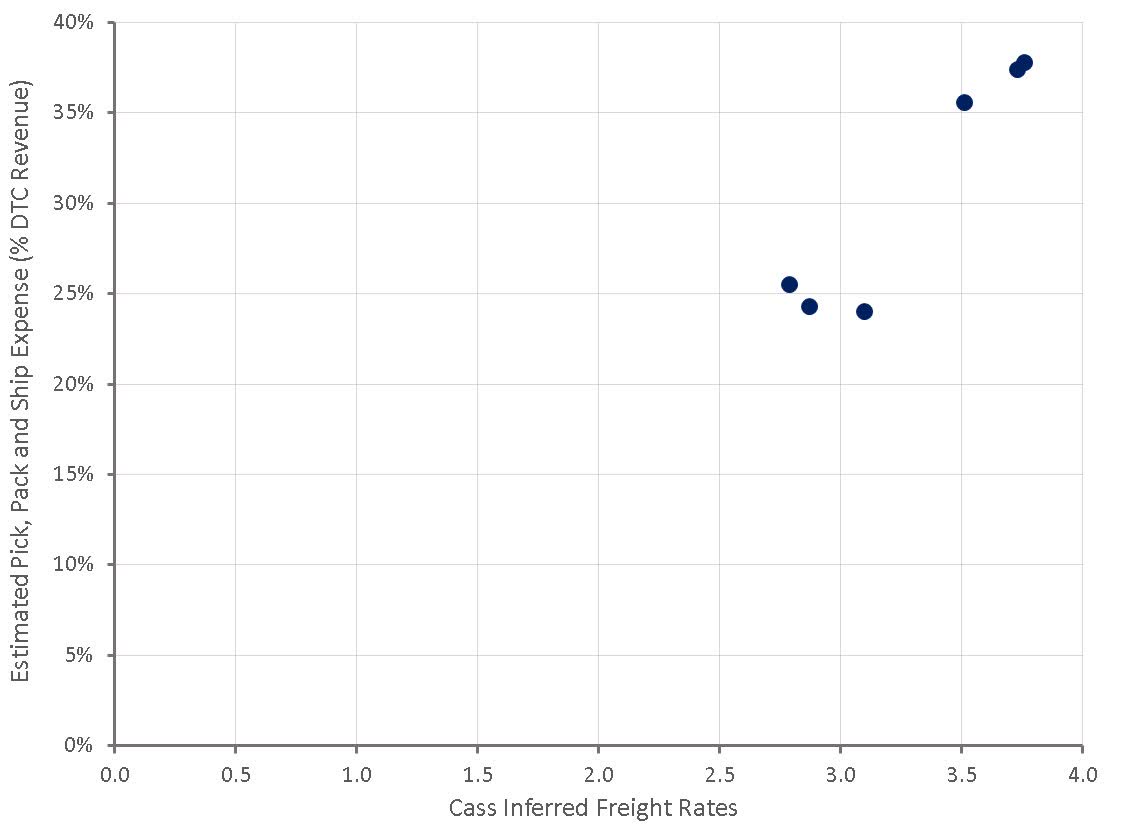

Figure 4: Estimated Amyris Pick, Pack and Ship Expenses (source: Created by author using data from Amyris and Cass)

{kind=link}

Amyris is in the process of optimizing their distribution footprint to control shipping and fulfillment expenses. A 4 million USD benefit is expected in the second half of 2022 (2% improvement in operating profit margins) and a 15 million USD benefit is expected in 2023 (3% improvement in operating profit margins). John Melo recently mentioned that a 30% reduction in fulfilment costs for Biossance has already been achieved.

Marketing

Amyris plans on rationalizing their marketing efforts to contain costs without impacting growth. This is expected to yield a 21 million USD improvement in the second half of 2022 (11% improvement in operating profit margins) and a 65 million USD benefit in 2023 (11% improvement in operating profit margins).

Reasonable customer acquisition costs are key to the success of the consumer business, and the lack of data on marketing expenses is likely a major cause of concern for many investors. With Amyris rapidly expanding their brand portfolio and investing aggressively to build those brands, marketing expenses are likely very high relative to revenue. John Melo has suggested that in a brand’s first year, marketing expenses are approximately equal to sales, with the number closer to 12.5% for a strong mature brand.

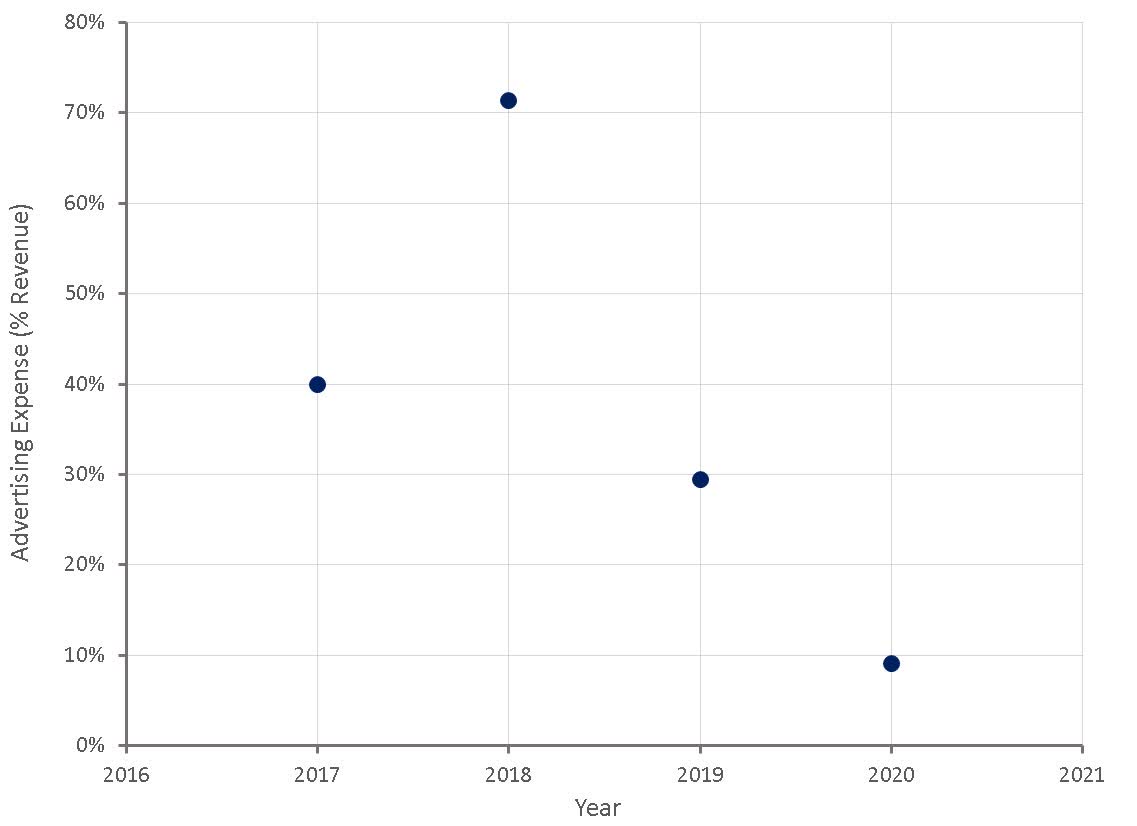

In the past, Amyris has given return on advertising spend figures for Biossance, with a trend toward fairly impressive figures as the brand has matured. The last estimate given in 2020 was potentially impacted by a surge in consumer spending though, and may not be indicative of performance under normal circumstances.

Figure 5: Biossance Advertising Expense (% Revenue) (source: Created by author using data from Amyris)

{kind=link}

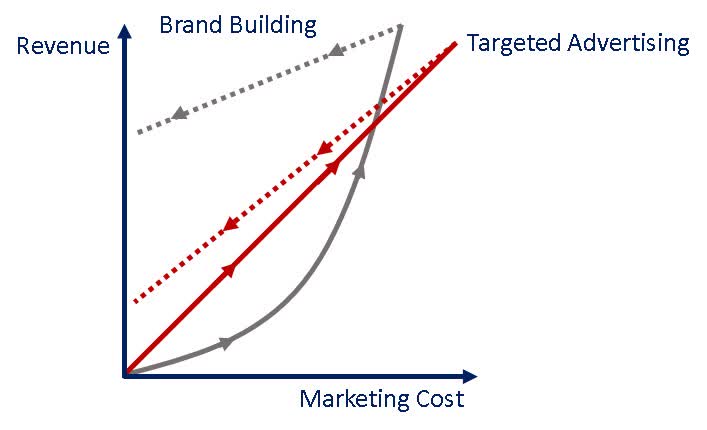

This data supports a concept I had previously discussed , where high marketing expenses are acceptable, provided they are able to drive brand awareness and consumer loyalty in the long-run. With Amyris’ differentiated product formulations and strong messaging around sustainability and clean chemistry, it does not make sense to lump their brands in with undifferentiated DTC companies competing on the ability to effectively target customers.

Figure 6: Illustrative Impact of Brand Advertising Versus Targeted Advertising (source: Created by author) Figure 7: Biossance Advertising Spend (source: Created by author using data from Amyris)

{kind=link}

{kind=link}

In Q3 2019, Amyris stated that they were achieving continued growth with less discounting and better returns on advertising spend. The percentage of repeat customers also grew from 15% in Q1 2018 to 48% in Q3 2019. In the second quarter of 2018, Amyris stated that approximately 50% of purchases were from repeat customers and 17% from brand loyalists who were purchasing more than three times a year. The lifetime value of Biossance customers was estimated to be approximately 1,200 to 1,400 USD in 2019 and increasingly rapidly. These figures compare favorably to benchmarks for the beauty industry.

Table 3: Ecommerce Benchmarks for Beauty Brands (source: Created by author using data from Metrilo) Table 4: Customer Acquisition Sources for DTC Beauty Brands (source: Created by author using data from Metrilo)

{kind=link}

Another indication of Biossance’s improving brand strength is the increasing number of end caps at Sephora. Stores with full end caps have about 2 to 2.5 times the sales of stores where they have wall only formats. At the end of Q3 2019, Biossance had end caps in 219 out of 480 stores , with plans to expand to 247 by the end of the year. Productivity in Sephora has also been well above average, with productivity calculated as Biossance’s revenue per square foot in Sephora stores relative to peers.

Table 5: Biossance Productivity in Sephora Stores (source: Created by author using data from Amyris)

Like many DTC companies, Amyris has probably faced significant customer acquisition cost headwinds over the past 12 months, due to competition and an increasing focus on privacy impacting the efficacy of digital advertising. Part of Amyris’ response to this has been to utilize pop-up retail stores to build brand awareness in key markets. This initiative appears to be going well, as Amyris is planning on opening flagship stores in New York, Miami, London and Los Angeles. At the Biossance showcase store in Miami, Amyris has witnessed conversion rates of over 60% along with a boost in website traffic in the Miami area. The Rose Inc. pop-up store saw conversion rates of over 90%. Research shows that the average conversion rate for brick-and-mortar stores is around 20-40% . Amyris’ stores currently compare favorably to this, but this is not surprising for newly opened showcase stores.

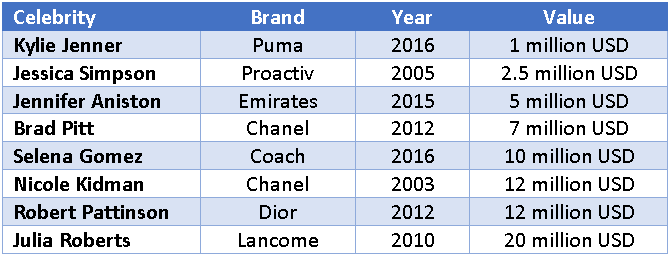

Another consideration is Amyris’ heavy use of brand ambassadors and their compensation arrangements. It is not clear how this is accounted for, but it would seem reasonable for these expenses to fall under SG&A. Amyris have used equity, royalty, or consulting arrangements to remunerate these ambassadors. Based on other celebrity deals it would not be unreasonable to expect that Amyris is paying millions of dollars a year to brand ambassadors.

Table 6: Example Brand Ambassador Deals (source: Created by author)

{kind=link}

New Brands

Some of the confusion related to the effectiveness of Amyris’ marketing spend likely comes from the investments they are making in launching new brands. Amyris has stated that it costs 5-7 million USD to develop a new brand and another 20-30 million USD to make it profitable. Presumably much of the initial cost is in market research, product formulation, brand design, etc. The remaining cost is likely related to sales and marketing to scale revenue to the point where overhead costs are covered. Management have stated that much of the investment is in the supply chain, packaging and new ingredients, and that these costs are expensed rather than capitalized.

Julie Fredrickson, CEO and co-founder of Stowaway Cosmetics, believes that at least 1.5 million USD in capital is required to successfully launch a beauty brand, despite ecommerce and social media lowering the barriers to entry. It should be noted that this type of figure is relative though, and that the cost to launch a global brand targeting 100 million USD in revenue will be very different to a national brand targeting a few million USD in revenue.

Table 7: Estimated Contribution to Beauty Brand Launch Costs (source: Created by author using data from Vogue Business)

There have been conflicting estimates given by Amyris regarding launch costs though, which may be a reflection of their capabilities evolving. More recent estimates are that it typically costs less than 3 million USD to build and launch a new brand, with a follow up 8-10 million USD cash investment required to reach operating break-even. Amyris stated that their investment in developing and launching JVN was approximately 2.7 million USD . Costs may have been lower due to Amyris’ extensive experience with hemisqualane and lessons learned from previous brand launches.

Biossance was Amyris’ first consumer brand and was likely launched with little conviction. The brand initially had a single SKU and limited resources were placed behind the brand. Amyris believe their investment in Biossance was about 50% lower than what is typical for a skin care brand. In Q3 2020, Amyris stated that their total investment in Biossance over 4 years was approximately 45 million USD .

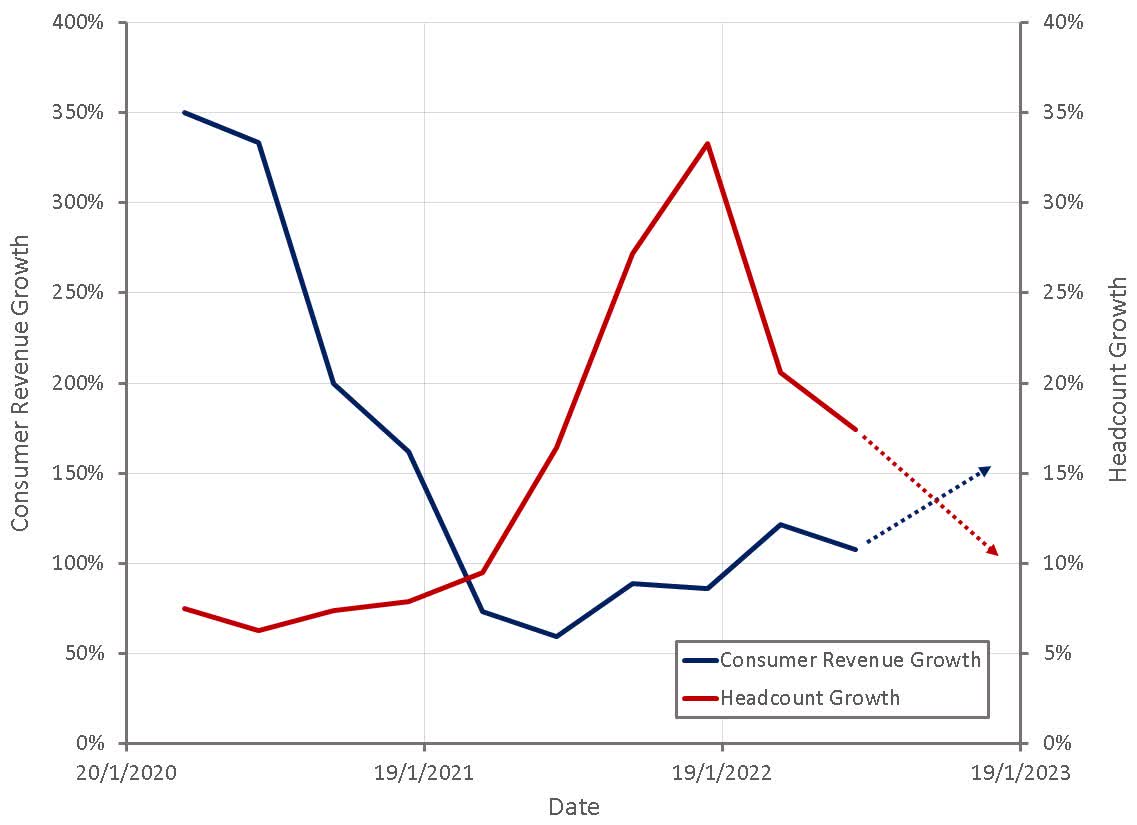

The wide range in estimates makes it difficult to draw conclusions, but it seems likely that each new brands causes cash outflows of tens of millions of dollars in the first year. This has been problematic for Amyris over the past 18 months, as they have rapidly expanded the number of brands in their consumer portfolio. The rapid increase in headcount in 2021 also indicates that brand investments begin long before those brands begin to generate meaningful revenue.

Figure 8: Amyris Headcount Growth and Consumer Revenue Growth (source: Created by author using data from Amyris and Revealera.com)

{kind=link}

Each new brand launch therefore causes a temporary decline in profitability until it reaches a sufficient scale. Amyris’ transition from 3 consumer brands in early 2021 to 13 consumer brands at the end of 2022 has caused a tremendous drag on the company’s bottom-line, but as these brands scale and some of them begin to approach breakeven, Amyris’ margin profile will change dramatically.

Figure 9: Typical Profit Profile when Scaling a New Business (source: Created by author)

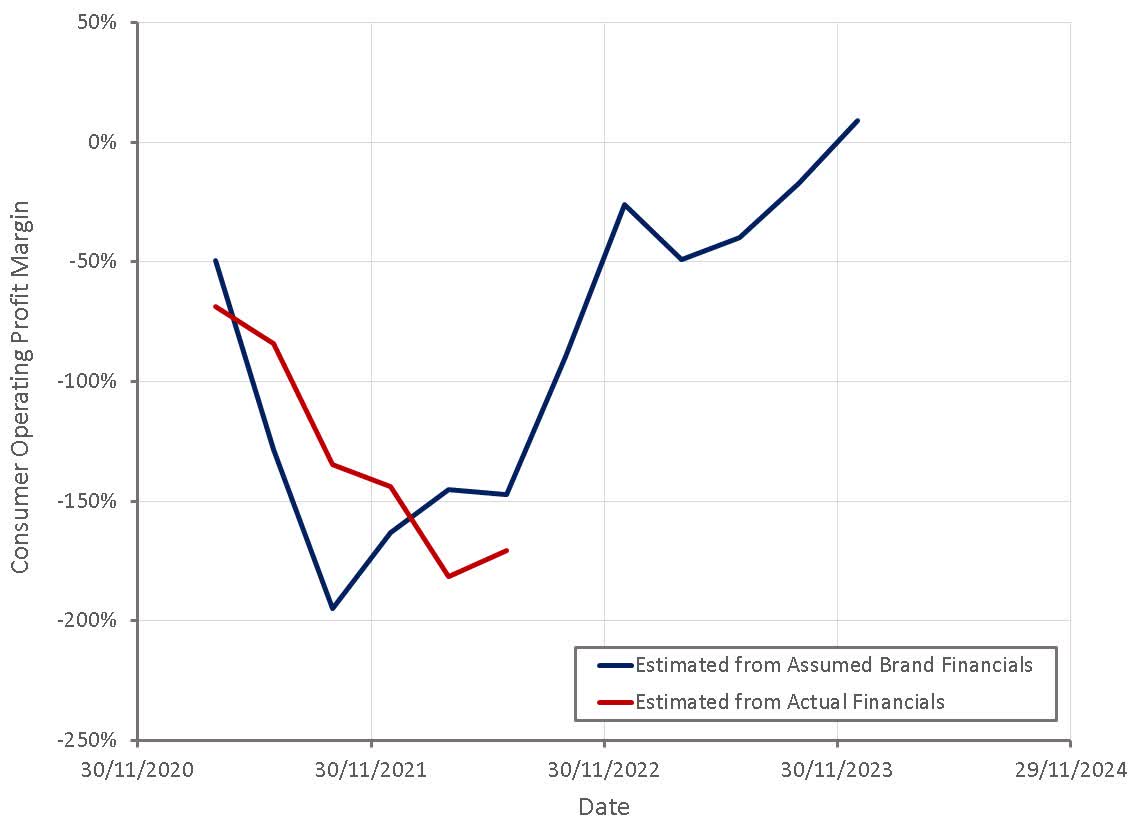

Amyris does not breakdown financial performance by segment, but indicative financials for the consumer business can be estimated by assuming that most of the variation in gross margins comes from the ingredients business and most of the variation in OpEx comes from the consumer business. Consumer operating profit margins declined significantly in 2021 as tailwinds from the pandemic subsided, inflation accelerated and Amyris invested aggressively in new brands. Consumer margins have likely bottomed though, and should begin to improve going forward as consumer revenue increases, particularly with the launch of 3 new brands in Q4 2022.

This dynamic can also be modeled by aggregating assumed financial performance for each brand. This is obviously difficult given the lack of public information, but by assuming marketing expenses based on public statements and overheads for each brand, using LinkedIn as a guide for headcount and calculating revenue and pick, pack and ship expenses from DTC order tracking, reasonable estimates can be made which show a similar trend.

Figure 10: Estimated Amyris Consumer Operating Profit Margins (source: Created by author using data from Amyris)

{kind=link}

The burden of new brand launches should be significantly reduced going forward due mainly to the size of the existing portfolio. There is also potential for economies of scale when adding new brands, which Amyris should benefit from over time. Amyris’ formulation organization is utilized by all brands, as is the creative organization, DTC channel management and brick-and-mortar partner management. Similarly for international expansion, where each country basically only requires one point person. The primary cost that is brand specific is marketing spend.

DTC

The DTC business model was in the right place at the right time during the pandemic, with many companies benefiting from increased demand and improved economics. Much of this benefit has proven temporary though, and many companies now face weak growth, elevated costs and declining investor faith in the business model.

Amyris’ consumer brands also benefited from the pandemic, and it seems likely that management over extrapolated this growth and has found it difficult to meet expectations over the past 12 months. It is also likely that the pandemic encouraged Amyris to focus on their consumer brands and led to the large investments undertaken over the past 12 months.

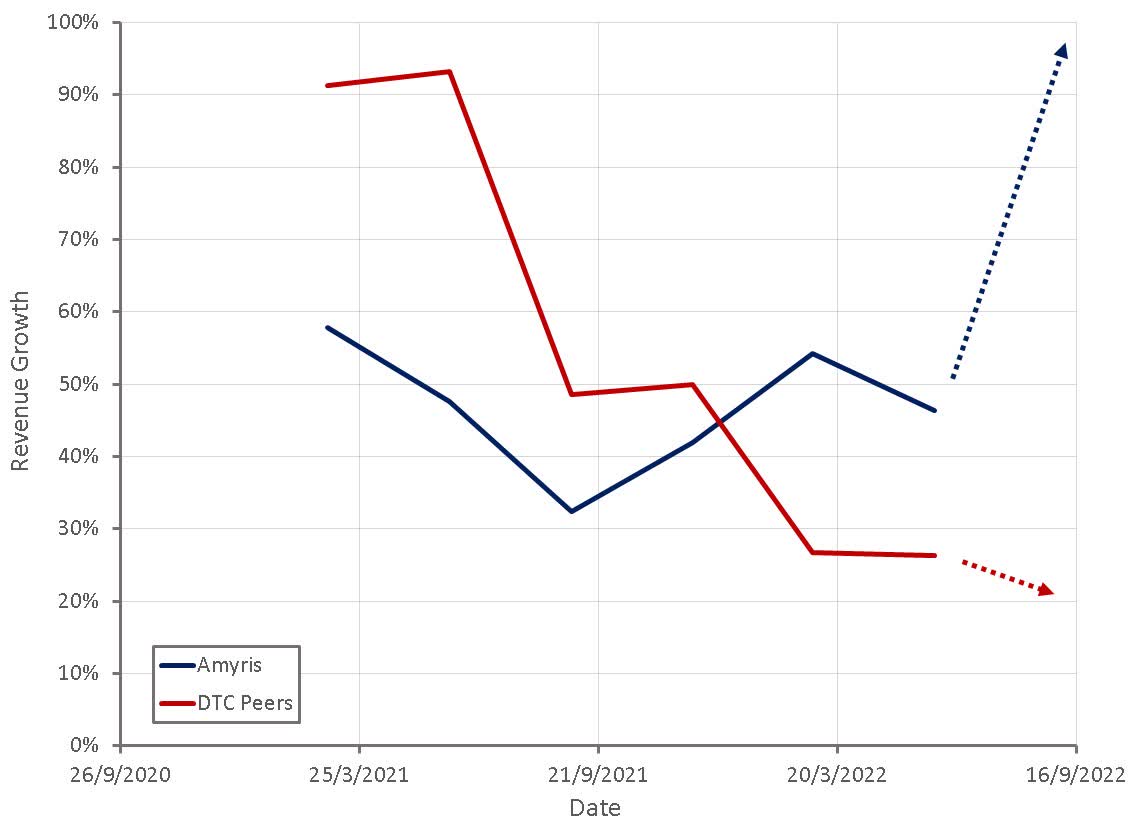

Amyris’ differentiated product formulations, excellent consumer reviews, strong brand performance and rapid expansion of retail doors should make it clear that Amyris is not just a DTC company though. With Barra Bonita debottlenecking ingredient production and the launch of three new brands, Amyris’ product revenue growth will accelerate substantially later in the year, further differentiating the company from DTC peers that will likely continue to struggle.

A number of DTC companies pointed to softening demand in their latest earnings calls, particularly in Europe and China. A number of companies have also slowed their pace of hiring, supporting expectations of a decline in growth.

Figure 11: DTC Company Revenue Growth (source: Created by author using data from Seeking Alpha)

{kind=link}

In the past, the DTC business model has been characterized by outsourced supply chains, online distribution and social media marketing. This minimized start-up requirements and allowed businesses to scale rapidly, but was only really feasible while taking advantage of low customer acquisition costs. As competition increased, brands have been forced to vertically integrate to preserve their margins and differentiate their products.

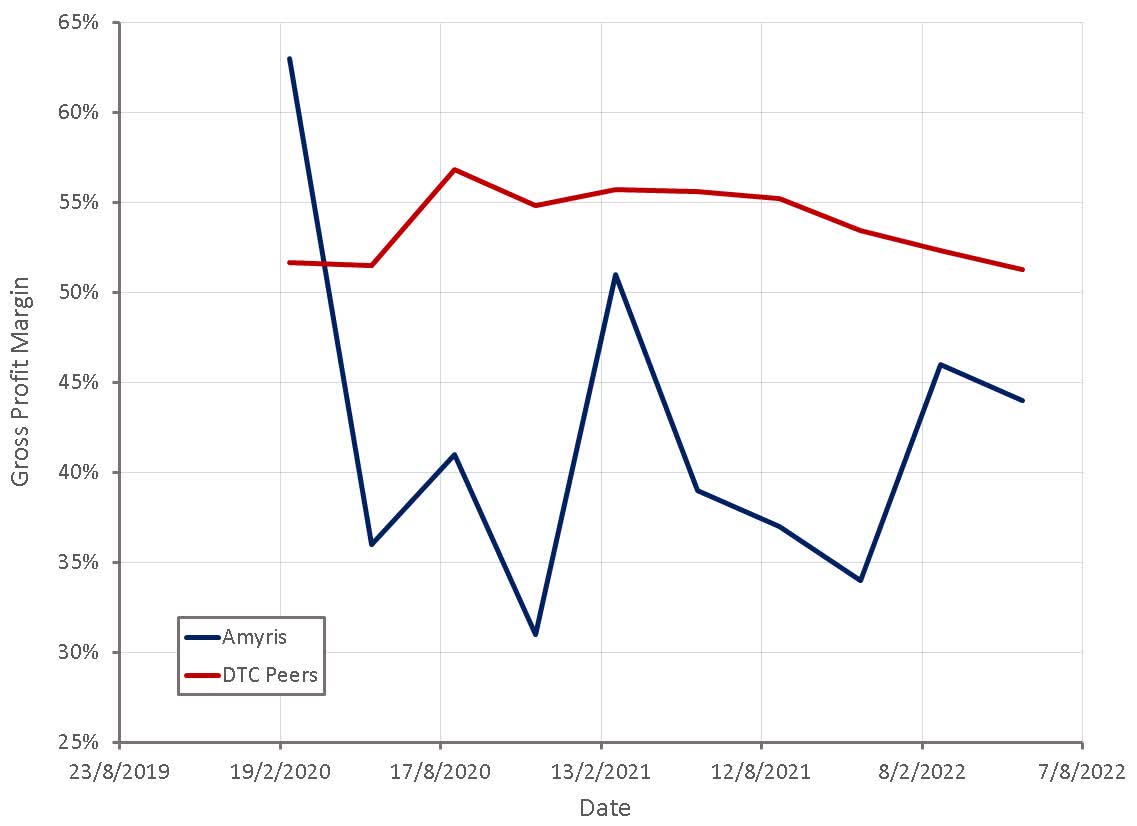

Over the past 12 months increasing competition has been exacerbated by supply chain issues and Apple’s ( AAPL ) privacy initiatives impacting the efficacy of targeted advertising. Gross profit margins have generally declined due to inflation, despite many brands increasing prices.

Most companies have had to deal with significantly higher shipping expenses, and a number of brands have had to manage factory closures in China. Allbirds ( BIRD ) estimate that supply chain issues have caused 4.5-5% decrease in their gross profit margins. Olaplex ( OLPX ) stated that logistics and input cost headwinds have caused a 3.3% decline in their gross profit margins (20% increase in COGS). Revolve ( RVLV ) incur fuel surcharges on every package they ship to their customers and on return packages. Fuel surcharges in the second quarter of 2022 were more than 4x times what they were in the prior year. Longer lead times have also led to lower inventory turnover, increasing the working capital requirements of most companies.

Figure 12: DTC Company Gross Profit Margins (source: Created by author using data from Seeking Alpha)

{kind=link}

Most of the DTC companies considered are relatively small and growing rapidly, and hence should be realizing operating leverage. The fact that operating expenses have generally increased faster than revenue over the past 2 years points to significant headwinds (demand, supply chain, marketing). Most companies have called out higher customer acquisition costs, for example Solo Brands ( DTC ) stated that their customer acquisition costs have increased by 20% .

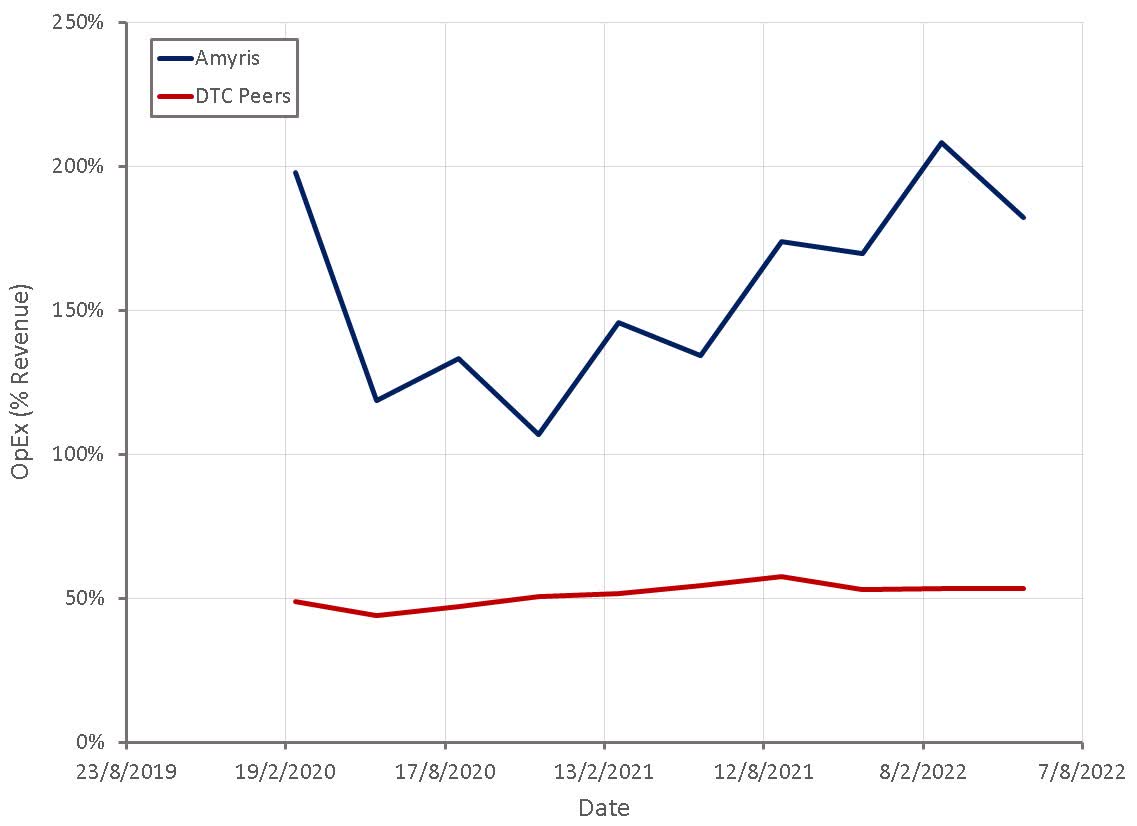

Figure 13: DTC Company Operating Expenses (source: Created by author using data from Seeking Alpha)

{kind=link}

Many DTC companies are responding to competition and supply chain issues in the same manner as Amyris:

- Insourcing production and / or fulfillment (Warby Parker ( WRBY ), Hims and Hers ( HIMS ), Revolve)

- Automated distribution centers (Allbirds, Revolve)

- Reduced headcount (Allbirds, Warby Parker)

- Expanding omnichannel distribution (Allbirds, Solo Brands, Olaplex, Hims and Hers)

- Opening retail stores (Allbirds)

- International expansion (Solo Brands, FIGS ( FIGS ), Olaplex)

Headcount

Much of Amyris’ expense growth over the past 18 months has been due to increased headcount, primarily building out their sales and marketing organization. The pace of hiring has moderated substantially from its peak, although remains relatively high.

Table 8: Amyris Headcount (source: Created by author using data from Amyris)

The impact of this increase in headcount on revenue has been somewhat muted so far, as the ingredients business has been supply constrained and revenue from licenses and royalties and grants and collaborations has been flat. In the second half of 2022, growth will accelerate substantially though, as Amyris begins to reap the benefits of the investments they have made over the past 2 years.

Figure 14: Amyris Hiring Trends (source: Revealera.com)

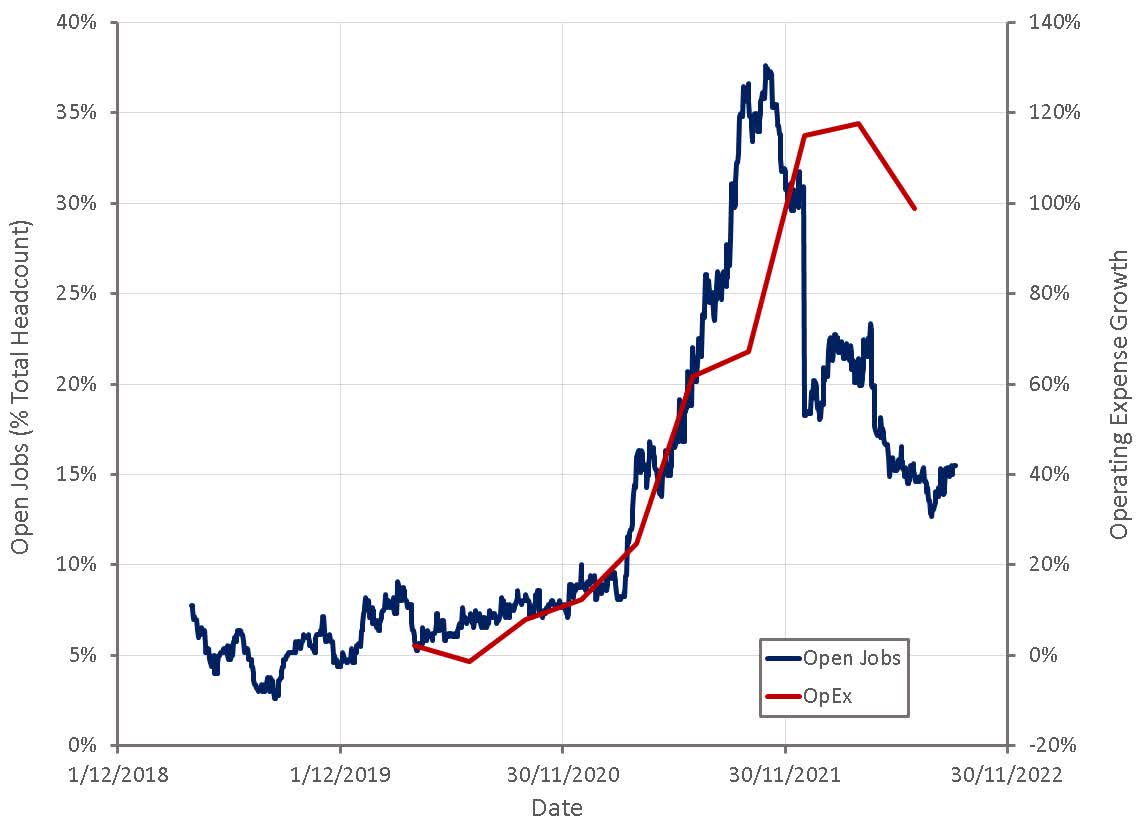

With inflationary pressures and Amyris’ headcount growth moderating, operating expenses should begin to level out somewhat over the next few quarters. With continued strong consumer revenue growth and Barra Bonita enabling an increase in ingredient revenue, Amyris should begin to realize operating leverage. Absent a reduction in headcount, operating leverage realized through revenue growth is the most important contributor to Amyris’ transition to profitability.

Figure 15: Amyris Hiring Trend and Operating Expense Growth (source: Created by author using data from Amyris and Revealera.com)

{kind=link}

Conclusion

Amyris’ consumer business is at an inflection point and should start progressing towards profitability over the next 12 months as revenue grows and expenses stabilize. This is contingent on successful launches for the 3 new brands in the fourth quarter of 2022 and the new brand in the first half of 2023.

For further details see:

Amyris: Consumer Business Cost Breakdown