AMRS - Amyris: Dependent On Charity

2023-05-22 11:53:54 ET

Summary

- Amyris' fate is no longer in its own hands, with the company dependent on investors for the ongoing provision of capital and third parties who will enter into strategic transactions.

- This situation is being exacerbated by a management team that refuses to acknowledge the gravity of the situation and begins making the radical changes necessary to ensure Amyris' survival.

- It would be easy to create an argument for why Amyris is undervalued, but until the company acts in the interest of shareholders, this value won't be realized.

Amyris' ( AMRS ) first quarter results show that the company is still moving towards bankruptcy and doing little about it. Gross profit margins remain near zero, employee costs remain similar to revenue, and Barra Bonita appears to have made the situation worse. While Amyris has a number of options that should stave off bankruptcy in the near term, this matters little if the underlying problems with the business are not addressed.

Potential Sources of Cash

Amyris’ financial position is becoming more precarious as management has failed to significantly move the needle on losses. Unlike in previous periods, Amyris is now highlighting the doubt around its ability to remain a going concern over the next 12 months. While management plan on addressing this, they have been trying to stem losses and shore up the balance sheet for the better part of a year, with limited progress. Each day that Amyris fails to enact radical changes, including large scale layoffs, the company’s long-term viability becomes more questionable.

Potential sources of cash include:

- A manufacturing JV that would provide Amyris with 50-100 million USD , as well as provide CapEx for future facilities and reduce working capital requirements.

- Consumer brand sales that management hopes will bring in up to 100 million USD (planning to retain 5-6 consumer brands).

- Advancing the proceeds of up to 350 million USD from future earn-outs and milestone payments.

If Amyris can secure these transactions within the next few quarters, the company should be able to continue operating for the next 1-2 years, but this isn’t particularly positive. Amyris continues to put itself in a position where it is forced to give up significant long-term value in order to secure access to near-term cash.

Molecule Pipeline

Amyris has over 30 molecules in its pipeline, although it is unknown how many of these are ready for commercialization. This pipeline is an important part of Amyris’ value and could be used as a source of cash to continue financing ongoing losses. The value of this portfolio is somewhat debatable, though, which is evidenced by the recent squalene transaction. Amyris’ management has aggressively touted the increasing value of licensing deals, but this has largely been the result of Amyris licensing more mature molecules. Future licensing deals will generally involve less proven molecules that command lower valuations.

On the first quarter earnings call, management highlighted ectoine and hydrogenated difarnesene as high potential molecules. Ectoine is a humectant and the hero ingredient of the Stripes brand. Ectoine could eventually develop into a valuable molecule, similar to hemisqualane, but this will require time, something that Amyris does not have.

Hydrogenated farnesene could find use in the skin care, hair care, color cosmetics and personal care markets as a palm oil alternative. It is more viscous than squalane and has a favorable combination of moisture retention, gloss and cushion properties. HDF could also result in lower cost formulations and is expected to be commercialized within the next 12 months.

It is not really clear how Amyris is going to monetize is molecule pipeline, despite its potentially large value. Management seems reluctant to outright sell molecules, and potential buyers may not want to take on the burden of manufacturing. Amyris is yet to demonstrate that it can consistently produce molecules at a profit, and doesn't currently have access to the necessary fermentation capacity to increase production.

Molecule Licensing

Amyris recently entered into a licensing agreement with Croda for the supply of squalene for use in vaccines, drug delivery systems and nucleic acid delivery systems. Amyris’ squalene is molecularly identical to shark derived squalene, but reportedly offers higher purity and a more predictable cost profile. Management’s choice of words here would seemingly suggest that Amyris’ squalene has a higher cost, though.

Amyris will receive an upfront payment of 4 million USD and potentially an additional 4 million USD milestone payment. Amyris will also share in the profits from the sale of squalene excipients and formulated products incorporating Amyris' squalene technology for use in the vaccine field. Given that Amyris is yet to commercialize squalene and that there is still significant risk associated with the molecule, it is not surprising that squalene failed to bring in a substantial amount of cash. This is a problem that Amyris is likely to face with future licensing deals.

Financial Analysis

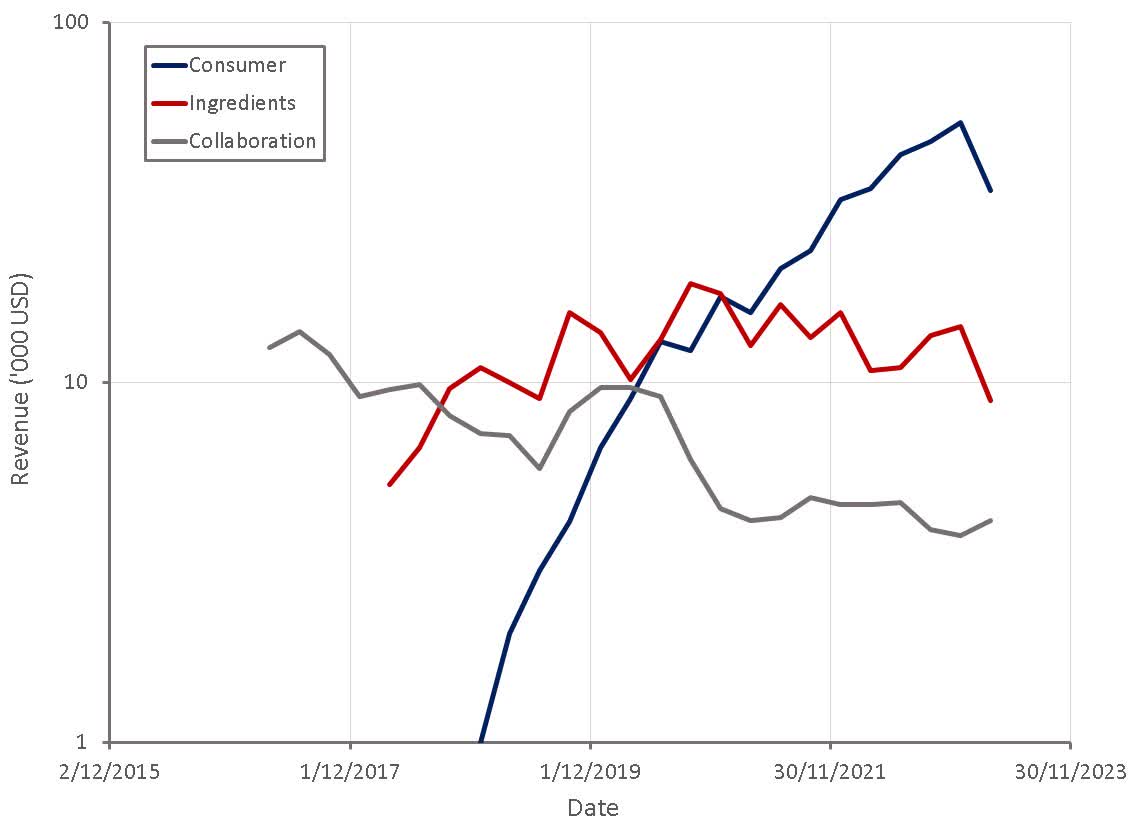

Growth ground to a halt in the first quarter as Amyris essentially found itself in a position where it didn’t have sufficient cash to operate the business normally. Core revenue decreased by 3% YoY, with the consumer business declining by 1% and ingredient revenue decreasing by 18%. Consumer revenue was impacted by dramatically reduced marketing spends and out of stock products. Management suggested the out-of-stock issue was due to vendors waiting for payment before releasing finished products to Amyris, with an impact of something like 10 million USD in the first quarter.

Ingredients revenue was lower due to ongoing supply and working capital constraints as Amyris continues to bring production in-house. Ingredients revenue has essentially trended downwards over the past two years, despite the startup of Barra Bonita, which would appear to be due to a desire to minimize losses from a negative gross margin business.

Management has suggested that with the Givaudan deal providing access to cash, Amyris’ largest brands have returned to double-digit growth. Ingredients revenue would also presumably be expected to rebound, but this part of the business is an unmitigated disaster and there is no real clarity as to what is happening. Barra Bonita is something like a 200 million USD facility that has been operating for close to 12 months and yet is probably only producing something like 5 million USD revenue a quarter.

{kind=link}

Figure 1: Amyris Revenue (source: Created by author using data from Amyris)

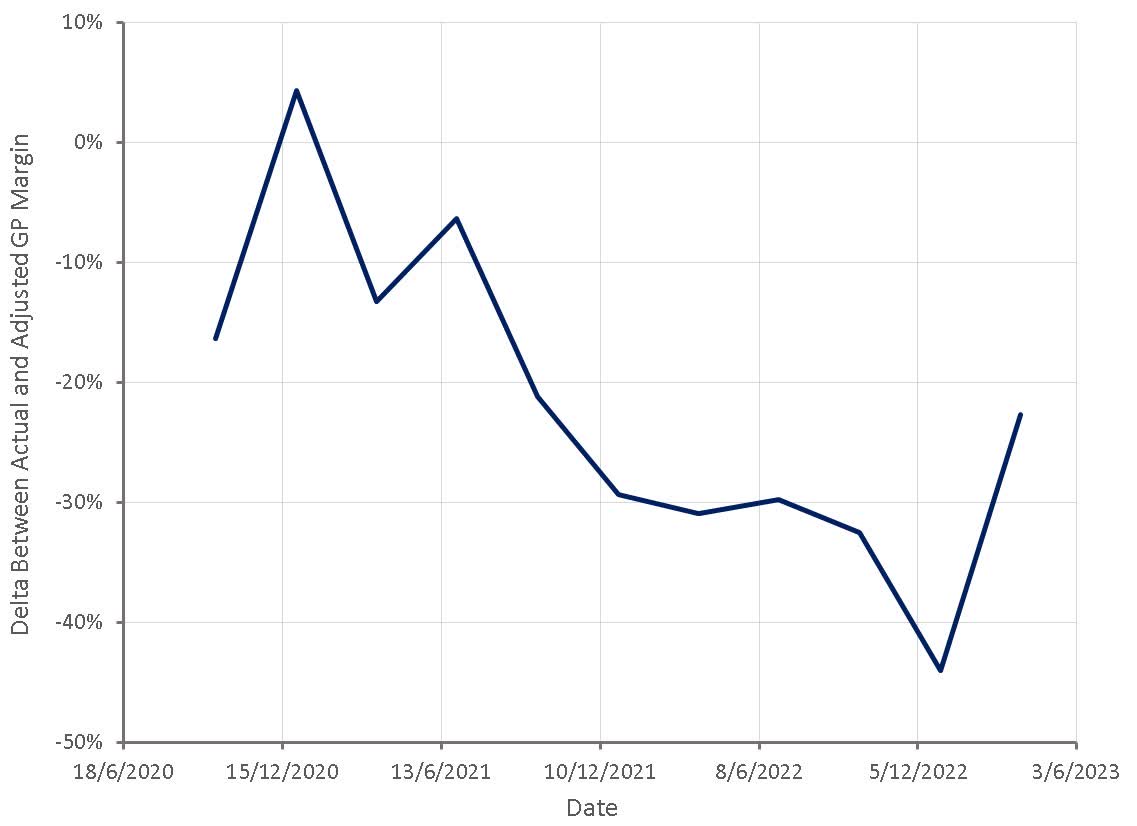

Despite a significant easing in supply chain pressure over the past 6-12 months, in addition to insourcing production, Amyris’ gross margins remain depressed. On a positive note, inbound freight expenses declined significantly YoY, including a 6.1 million USD reduction in air freight expenses. This is reflected in the convergence between actual and adjusted gross profit margins.

{kind=link}

Figure 2: Difference Between Actual and Adjusted Gross Profit Margins (source: Created by author using data from Amyris)

Non-GAAP consumer gross margins were 56% in the first quarter, declining YoY as a result of product and channel mix. Management expects that this will improve over the course of 2023 as roughly 60% of consumer goods are expected to come from the Interfaces facility by the middle of the year and around 80% by the end of the year.

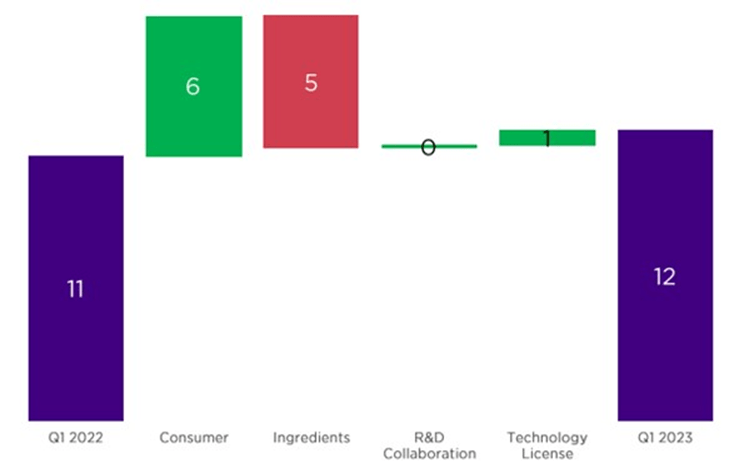

Ingredient gross margins continue to be truly awful, and this is not receiving the attention it deserves. The ingredient business caused a 5 million USD YoY decline in gross profits in the first quarter, despite only providing 8.9 million USD revenue.

{kind=link}

Figure 3: Sources of YoY Change in Gross Profits (source: Amyris)

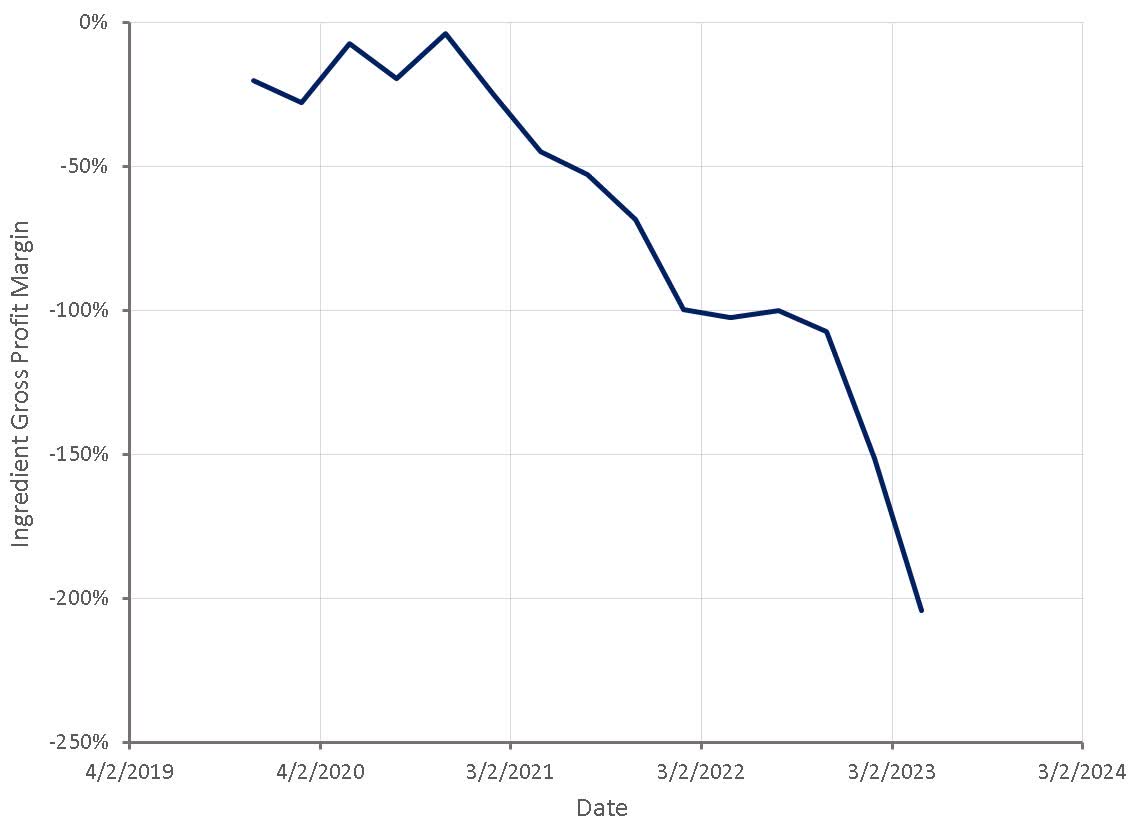

While management has given no insight into the cause of this, it would appear to be the result of a combination of elevated feedstock costs, high CMO costs and operating Barra Bonita at sub-scale. Management recently stated that around 50-60% of Amyris’ farnesene was still coming from Brotas and that 90% of the production of other molecules was occurring at Barra Bonita. The contract facility in Spain is still reportedly being used for the production of 1-2 molecules this year. This is concerning as Barra Bonita is seemingly not producing that much, despite all three main lines now being operational.

{kind=link}

Figure 4: Estimated Ingredient Gross Profit Margins (source: Created by author using data from Amyris)

Amyris began to make some progress on reducing overhead expenses in the first quarter, although this appears to have been forced onto the company due to a lack of cash and may not be sustained going forward. Headcount reduction initiatives reduced costs by around 1 million USD in the first quarter, and consumer marketing expenses were roughly 14 million USD lower. Media spend in the first quarter of 2023 was about 25% of media spend in the prior year quarter.

Management suggested that each dollar of media spend in the first quarter generated around 10 million USD revenue. This may sound impressive, but it is really just a function of marketing spend approaching zero. It does highlight that Amyris has a viable consumer business, though. While the consumer business has stopped growing, a dramatic decline in marketing spend did not result in a collapse in revenue.

Amyris discontinued the EcoFabulous brand and reorganized the Beauty Labs business in the first quarter, resulting in:

- A 28.5 million USD favorable non-cash change in acquisition related contingent considerations

- A 95.4 million USD asset impairment

- A 4.2 million USD inventory write-off

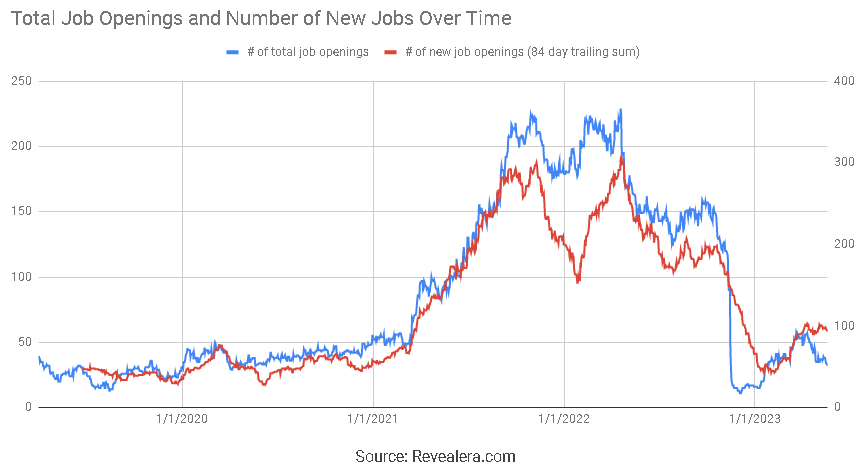

While this is a step in the right direction, there continues to be a lack of urgency. Amyris should be aggressively exiting or spinning off non-core brands and reducing headcount. So far there appears to be no will to enact the necessary layoffs though, and without this, Amyris is left needing to at least triple its revenue with a weak balance sheet and limited access to cash.

{kind=link}

Figure 5: Amyris Job Openings (source: Revealera.com)

For further details see:

Amyris: Dependent On Charity