AMRS - Amyris: Show Us The Money

Summary

- Amyris is on the cusp of closing a record strategic transaction slated to generate ~$500mm in cash value.

- All indications point to a transaction closing in the next two to three weeks.

- Cash balances by year-end projected to be >$350mm after the strategic transaction close.

- Q4’22 revenue guidance for$100mm is achievable and on track for ingredients, licensing and D2C fronts; however, brick & mortar sales bears examination.

- Q4’23 revenue and operating income margins, while close, may be a bit of a stretch goal.

New to Amyris (AMRS)? I suggest you read my first and second Seeking Alpha articles as primers on the company.

Now, let's be honest. The Q3’22 earnings call (“EC”) was a complete disaster and a “deja vu” moment from exactly one year earlier.

Amyris is viewed by most investors (institutional and retail alike) as a very binary investment: Extremely risky balanced by an unknown speculative reward.

Our goal is not to rehash what happened (there are good articles for that), but to answer the pressing questions regarding the:

- Status of the Strategic Transaction

- Achievability of Revenue Targets

- Understanding of Cash Costs/Burn

Molecular Marketing Rights Deals

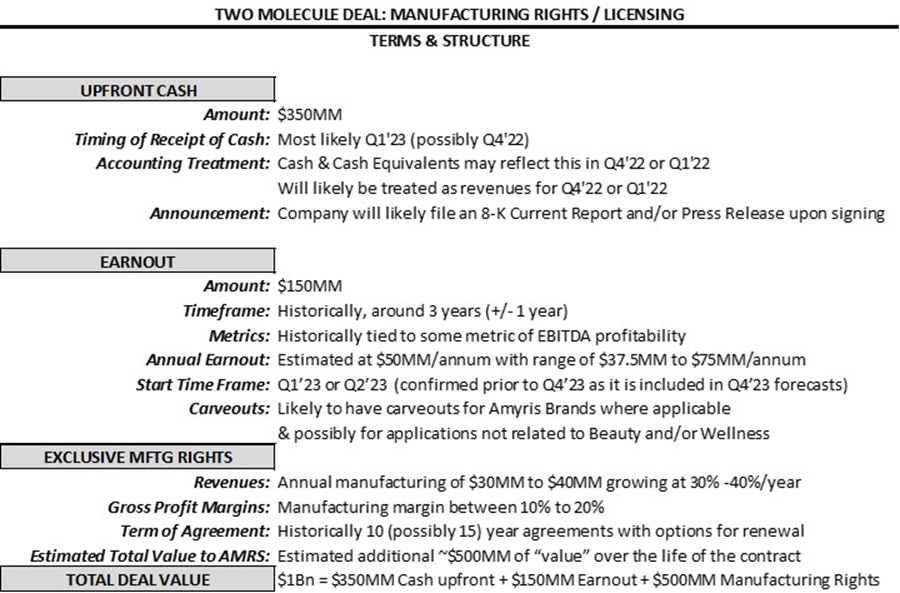

Amyris announced on their Q1’22 EC a $250MM Strategic Transaction (“ST”) involving the Marketing Rights for two Molecules through a multiparty competitive bid process. The structure and value of the transaction expanded over the next three quarters culminating in a $500MM ST value ($1Bn if you include the exclusive manufacturing rights). The ST is expected to close by year-end and represents the largest ST in the firm’s history:

{kind=link}

Author Compilation

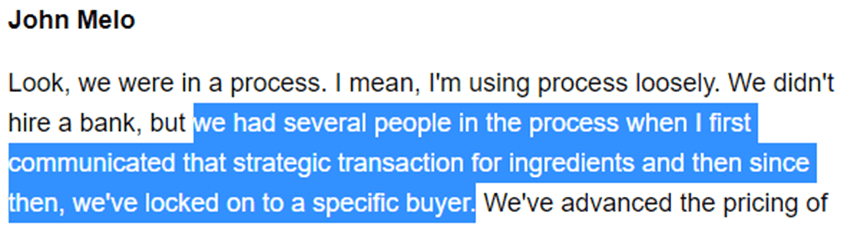

By Q2’22 EC , Amyris had locked on one buyer to proceed into deeper due diligence and deal structuring:

{kind=link}

/seekingalpha.com/article/4532027-amyris-inc-amrs-ceo-john-melo-on-q2-2022-results-earnings-call-transcript

Likelihood & Time Frame

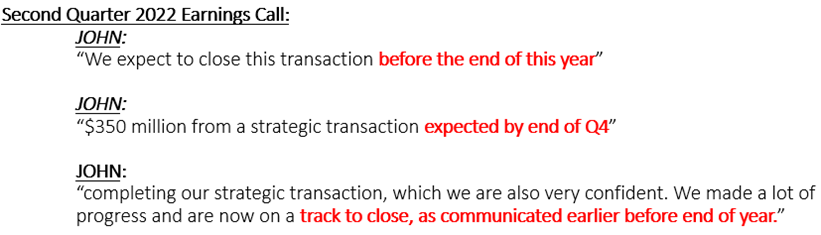

Many investors question the likelihood and authenticity of the ST despite management’s reiteration numerous times in press releases, filings, and verbal statements:

{kind=link}

investors.amyris.com/sec-filings

{kind=link}

amyris.com/newsroom

{kind=link}

seekingalpha.com/article/4554999-amyris-inc-2022-q3-results-earnings-call-presentation

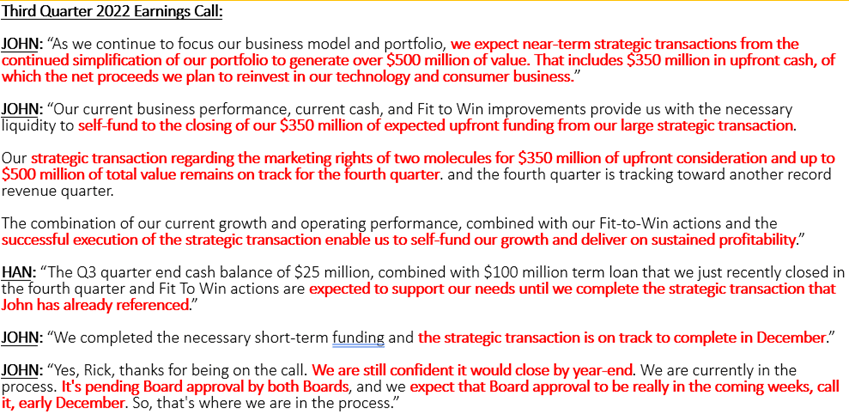

With the most recent Q3’22 EC , it was disclosed that the ST was pending approval in front of both Boards:

{kind=link}

seekingalpha.com/article/4555043-amyris-inc-amrs-q3-2022-earnings-call-transcript

Since then, John Melo (“JM”) reconfirmed the deal status in a 11/30/22 press release :

{kind=link}

investors.amyris.com/2022-11-30-AMYRIS-CONSUMER-BRANDS-DELIVER-80-CYBER-MONDAY-LIKE-FOR-LIKE-GROWTH

However, there seems to be confusion on the timing of the Strategic Transaction as to whether it would close in “early December” or by year-end:

{kind=link}

seekingalpha.com/article/4555043-amyris-inc-amrs-q3-2022-earnings-call-transcript

A Board Approval is not the same as a Closing Date (i.e., the date of ratification). Companies require time to review/edit/re-draft/ratify Definitive Agreements and/or binding Term Sheets.

To help narrow down an expected time frame, we can look to past STs. The last two that were executed in the fourth quarter were announced the week prior to the holidays (i.e., Monday, December 21 st , 2020 and Thursday, December 23 rd , 2021).

Our research indicates Amyris’ Board may likely have already met in mid-November and the next meeting may likely be one month from then (i.e., between 12/12/22 and 12/23/22) to ratify the deal. As such, we expect an announcement most likely during the week of 12/19/22 through 12/23/22 (or possibly the week before) in advance of the holidays.

What are the Two Molecules in Play?

Despite repeated reassurances, the market (as expressed in a share price effectively priced for bankruptcy) remains wary and skeptical with lingering questions:

- Which molecules are these?

- Who is the Buyer?

- Will the Buyer’s Board back out in this Macro environment?

We hope to address these questions below through deductive reasoning.

We have gathered the following ST information from various analyst conferences and earnings calls with management:

Author Compilation

“Existing”, “In Production”, and “One vs. Two” Molecules

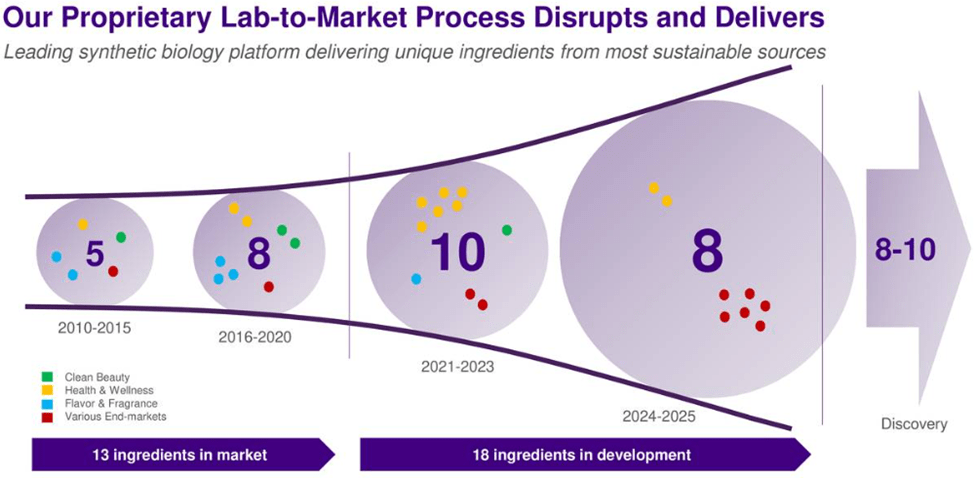

Amyris has a library of ~250 existing molecules and ~25 molecules in active development (~20% in collaborative partnerships; 80% developed and commercialized in-house).

Only 13 ingredients / molecules were in “existence” and “in production” as of the date of the deal announcement:

Author Compilation

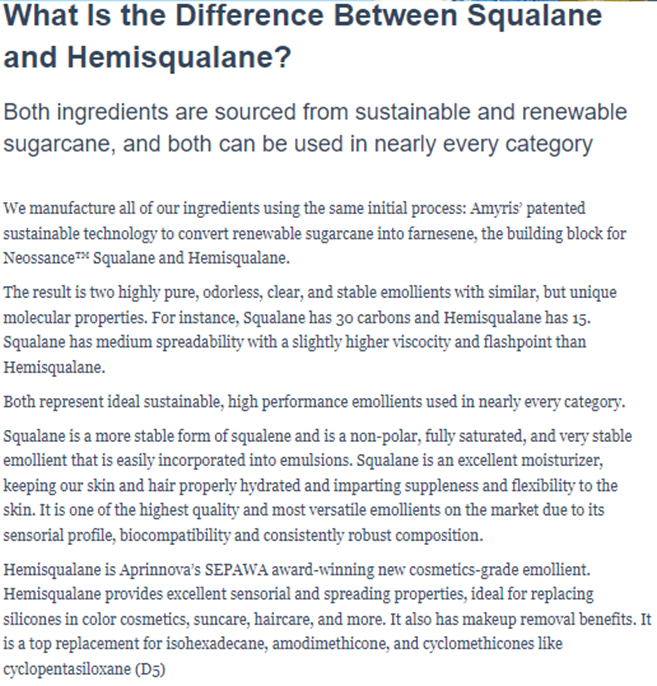

Of those, only three have a strong relationship with eachother:

‘Squalene’,

‘Squalane’

‘Hemisqualane’

We believe the relationship between two of the three molecules caused the correction made by JM initially when he initially identified one ingredient, and later adjusted his statement to two. To clarify, it helps to understand the distinction between all three ingredients:

- Squalene

{kind=link}

abeautyedit.com/hemi-squalane-vs-squalane/

- Squalane

{kind=link}

abeautyedit.com/hemi-squalane-vs-squalane/

- Hemisqualane

{kind=link}

abeautyedit.com/hemi-squalane-vs-squalane/

Since Squalene was not manufactured in large quantities at the time of the announcement, we can narrow the playing field to Squalane & Hemisqualane.

Let’s examine the differences between the two:

{kind=link}

aprinnova.com/knowledge/what-is-the-difference-between-squalane-and-hemisqualane

Production & Timeframe

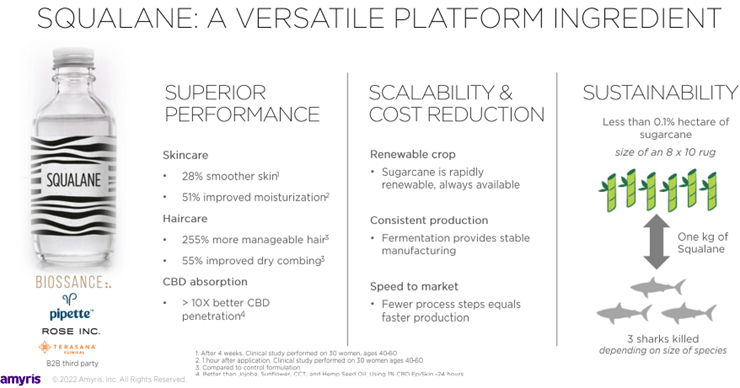

Amyris has disclosed that it has produced large quantities of Squalane for nearly a decade becoming a significant market share leader:

{kind=link}

seekingalpha.com/article/4509715-amyris-inc-amrs-ceo-john-melo-on-q1-2022-results-earnings-call-transcript

To quantify: According to Sunil Chandran (Chief Science Officer at Amyris), worldwide there is between 2,500-to-4,000 metric tonnes of Squalane produced , of which Amyris produces >2,000 metric tonnes.

Amyris, in recent quarters, has accelerated efforts to highlight these two molecules throughout its investor presentations/and earnings calls:

{kind=link}

investors.amyris.com/events-and-presentations#past

{kind=link}

investors.amyris.com/events-and-presentations#past

Both molecules appear to be on a significant growth trajectory and are the only two molecules that may be considered as “one set” out of the original thirteen. The volumes and growth estimates match the estimated volumes and 30% to 40% CAGRs referenced by JM earlier:

{kind=link}

seekingalpha.com/article/4532027-amyris-inc-amrs-ceo-john-melo-on-q2-2022-results-earnings-call-transcript

Complexity & Timeframe

This takes us to the final clue which is the complexity of the deal and why it required 7-to-8 months to complete. Both ingredients are derived from a beta-farnesene precursor (aka Biofene) and require “finishing” through a 50/50 Joint-Venture entity known as Aprinnova (established in 2017 and held in partnership with a third party entity, Nikkol Group ).

It is unclear whether the Buyer in this ST will assume Amyris’ interest in the Aprinnova, or Nikkol Group’s interest in the JV, or some alternative structure; however, it may explain why the deal was established from the outset for an end-of-year completion date while navigating a tri-party deal.

Buyer “Speculation”

Now that we may have identified the molecules, let us see if we can identify the Buyer using the same process of elimination.

JM has publicly stated that the winning buyer was an existing partner of Amyris, helping us to narrow the playing field to: DSM , Firmenich , Yifan , Nikkol Group , Takasago , Kuraray , or Givaudan .

JM has elaborated publicly it is not DSM, which, by extension, would eliminate Firmenich who is in the process of a merger with DSM.

JM further indicated publicly that this was a decade’s old partner which rules out Yifan who has been a partner with Amyris since 2018 .

Four potential partners remain: Kuraray (2011), Takasago (2012), Nikkol Group (2011), and Givaudan (2011)

Kuraray: Amyris has not been a major supplier to Kuraray, although there are developments underway for commercialization of liquid farnesene rubber . While Kuraray has its own synthetic squalane (using terpene-compound synthesis technology ), it is a competitor with Amyris, and does not appear to have worked with fermented Squalane/Hemisqualane in the past. The ST would not be a strategic acquisition for Kuraray as they are focused on the production and sale of functional resins, chemical products, man-made leathers, synthetic fibers, and textiles.

Takasago: Takasago has focused on fragrances and lacks both commercial familiarity with the Squalene molecule family (other than a patent filing from ~50 years ago ) and products in beauty care (i.e., skincare or haircare). Nor does Takasago have the financial strength to support a ST of this magnitude.

Nikkol Group: The Nikkol Group lacks the financial leverage to support a ST of this size.

Givaudan: This leaves us with Givaudan as the most likely candidate that matches all of the characteristics of the would-be buyer.

{kind=link}

Author Compilation

To understand how this relationship evolved, let us unpack the history of their partnership.

On June 23rd, 2010 Soliance and Amyris tied-up to produce Squalane:

{kind=link}

cosmeticsbusiness.com/news/article_page/Soliance_and_Amyris_tieup_to_produce_squalane/55259

Givaudan and Amyris began their own relationship on 2/24/11, through a collaboration with Beta-Farnesene to develop a key fragrance ingredient.

On 3/14/11, Amyris deepened this relationship by extending it into Squalane (matching the “decade” relationship JM previously referenced):

{kind=link}

hbw.pharmaintelligence.informa.com/RS017479/Renewable-Ingredient-Firm-Signs-Givaudan-Boasts-10-Mil-quotPipeline-Of-Interestquot

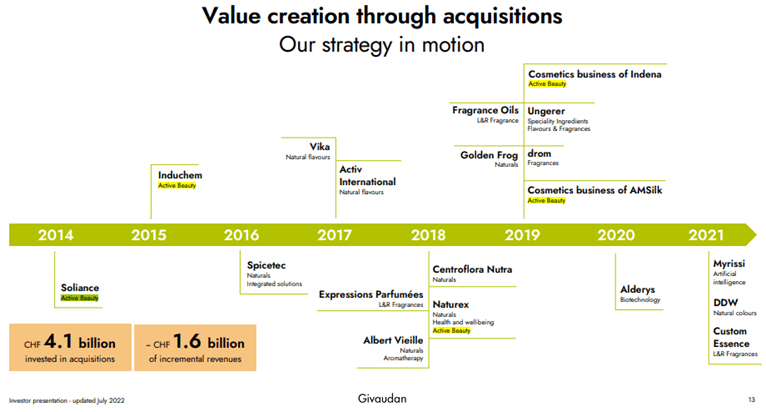

Givaudan went on to acquire Soliance on 12/9/14, along with their Amyris squalane relationship.

Since then, "Givaudan has been engaged in the research and development of proprietary fragrance ingredients with Amyris for several years" and sought to expand into the research, development and production of active cosmetic ingredients as an entrée into Active Beauty.

It has grown its Active Beauty business through strategic acquisitions with a focus on cosmetics…

{kind=link}

givaudan.com/files/giv-2022-investor-presentation-jul.pdf

…keeping an eye towards acquisitions in Fragrance & Beauty to expand product offerings that include natural ingredients and biotechnology:

{kind=link}

www.givaudan.com/files/giv-2022-investor-presentation-jul.pdf

Givaudan has indicated that “Health and Wellbeing” and “Active Beauty” are key priorities:

{kind=link}

seekingalpha.com/article/4524890-givaudans-gvdbf-ceo-gilles-andrier-on-q2-2022-results-earnings-call-transcript

Acquisitions are a primary method to grow strategic priorities for Givaudan:

{kind=link}

seekingalpha.com/article/4524890-givaudans-gvdbf-ceo-gilles-andrier-on-q2-2022-results-earnings-call-transcript

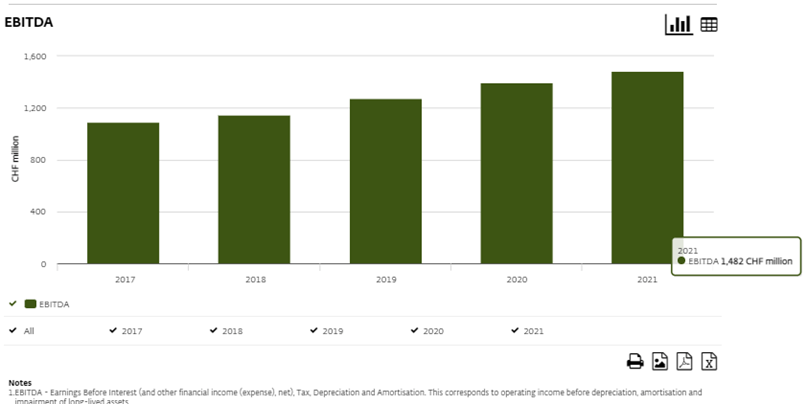

To understand if Givaudan has the financial capacity to handle an acquisition of this size, we can reference to the metrics noted above and examine Givaudan’s 2021 EBITDA performance to determine how much spare “capacity” they have remaining:

{kind=link}

www.givaudan.com/investors/financial-results/key-figures

From above, we can see that Givaudan generated ~1.57Bn USD in EBITDA for 2021. Using the 4x-to-4.5x Debt/EBITDA threshold levels vs. current level of 3.45x, this translates into 0.55x-to-1.05x 2021 EBITDA remaining spare capacity, corresponding to $864MM-to-$1.65Bn (more than enough to fund this ST).

Will Givaudan’s Board Oppose Management on the ST?

In my experience in dealing with Boards (e.g., Fortune 500, Academic, Private/Public, Domestic/International and Venture Backed), Directors often times serve as custodians/advisors but generally do not interfere or oppose management decisions. It can become dicey when there is a concentrated ownership among individual board members, (i.e., an “Activist Director”). As such, I thought it would be a useful exercise to investigate if there were any “John Doerr” equivalents on Givaudan’s Board:

integratedreport.givaudan.com/#/compensation-and-governance

Unlike Amyris, no single Givaudan Board Member owns more than 0.1% and the amounts owned by any member is <$5MM.

These are relatively small amounts (for a $30Bn Market Cap firm) and do not scream “red flags” among any of the Directors that may cause them to derail a 7-month process.

It is important to remember that Givaudan has been working alongside Amyris for over a decade and has their supply chain intertwined with Amyris’ supply chain as well. They need Amyris and the molecules in question just as much as Amyris will need Givaudan’s capital and sales & distribution support. Were Givaudan to walk, there are other bidders eager to step in and fill the void.

Given the above:

- As of 11/8/22, the deal was “pending Board approval” from both sides

- We believe the Boards have met in Mid-November

- As of 11/30/22, JM announced that the deal remained “on track”

…then one may infer that the deal has been reviewed and has likely been approved. We suspect that the deal is now in its final preparation for ratification.

What would the Transaction mean for Amyris’ Share Price?

We can look to the past for a glimpse into the future:

{kind=link}

Author Compilation

By examining the data from the past four STs above, we can try and gauge the impact on share prices based on the value composition of each deal:

{kind=link}

Author Analyses

From above, we can see that the % increase in share price is directly correlated with the increase in cash value of the ST as one may expect. It is notable that the cash value of the current pending ST (i.e., $350MM) is larger than the cash value of all four prior STs combined (i.e., $287MM).

However, a better way to refine that estimate, is to focus on the change in market cap relative to the actual Total Transaction Value (excluding manufacturing rights) to estimate a potential range for shares prices to climb.

We can infer a possible multiplier of ~5.5x to ~22x of the Total Transaction Value (although, the larger the ST, the smaller the multiplier applied). This is useful in understanding how powerful an impact a strategic transaction can have on market value (not so much in pegging an actual share price).

If these ratios were to hold, this would imply a forecasted share price of $6.6/share to $20/share (given today’s share price of $1.68 and 390MM fully diluted shares).

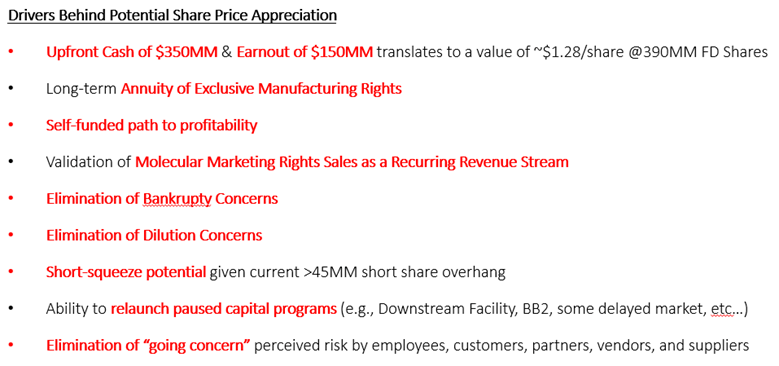

This appreciation in share price can be driven by a variety of factors:

{kind=link}

Author Compilation

This ST is one of many in the pipeline. Management has identified a second molecule that is slated to close in the next few months and we believe the second one is the Squalene molecule (for Adjuvant applications) based on references made by management regarding applications to the pharma industry and the value of Squalene.

The second ST will solidify four consecutive years of molecular sales and that the company has a powerful engine of recurring revenues with ~25 Active Development molecules in their pipeline and three to four others under consideration:

{kind=link}

seekingalpha.com/article/4414895-amyris-amrs-investor-presentation-slideshow

I see an evolution of thought on how to view/treat these deals as Analysts/Investors begin to classify them as recurring revenues, giving credit for the upfront cash components; followed by crediting the earnouts and then eventually finding real value in the annuity stream generated from exclusive manufacturing rights. The partners that Amyris is choosing are not just based on how much they can pay upfront but also how quickly they can scale the business over the years to come.

Revenues (Past, Current Quarter and Next Year)

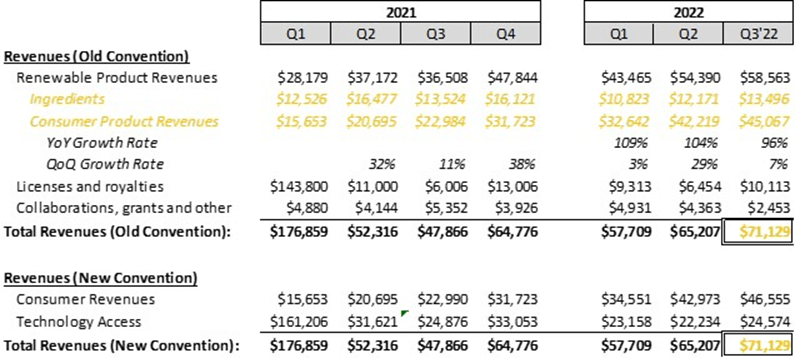

While Consumer Product Revenues have achieved record highs for six consecutive quarters, Ingredients have remained relatively unstable due to global logistics/supply chain issues.

{kind=link}

Author Analyses

The growth in Consumer Revenues has come at a tremendous cost due to the use of third-party manufacturers/CMOs which have led to gross profit losses (excluding earnout contributions).

{kind=link}

Author Analyses

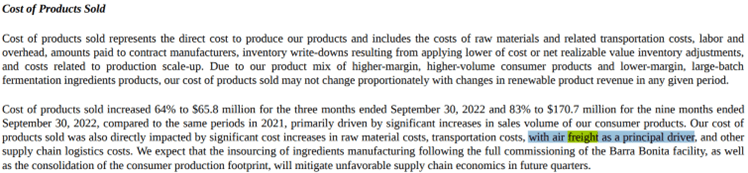

There are a variety of factors that led to the higher-than-expected Costs of Product Sold (“COPS”). Most notably were the use of third-party manufacturers/CMOs for both ingredients & consumer products as well as Airfreight Charges, resulting primarily from Inbound Airfreight used to ship consumer product parts from China (e.g., caps, pumps) and Ingredients from CMOs (e.g., S.A. Antibioticas from Spain whose cost of production is 3x that of Barra Bonita):

{kind=link}

investors.amyris.com/sec-filings

Reminiscent of the Q3’21 EC, and as a result of global disruptions (e.g., China lock-downs, Freight rate increases, high energy costs), Amyris had to make a hard choice between breaking contract obligations and foregoing earnouts or incurring large-unanticipated freight costs and increasing burn.

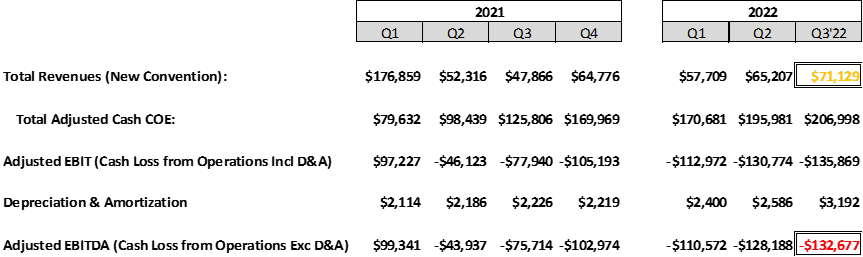

A portion of the costs however are non-cash stock-based compensation which can be stripped out to yield a better understanding of true cash burn…

{kind=link}

Author Analyses

…leading to a better understanding of Adjusted EBITDA over time:

{kind=link}

Author Analyses

There are a variety of non-recurring/savings opportunities from a Cash and Operating Expenses (“COE”) standpoint that have the potential for reducing Adjusted EBITDA on a go forward basis.

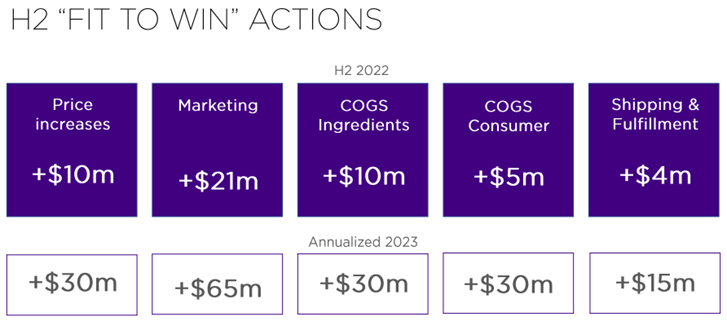

These are currently being implemented in phases through an internal program called “Fit to Win”. The original program, announced in the Q2’22 EC proffered the following savings opportunities:

{kind=link}

investors.amyris.com/events-and-presentations#past

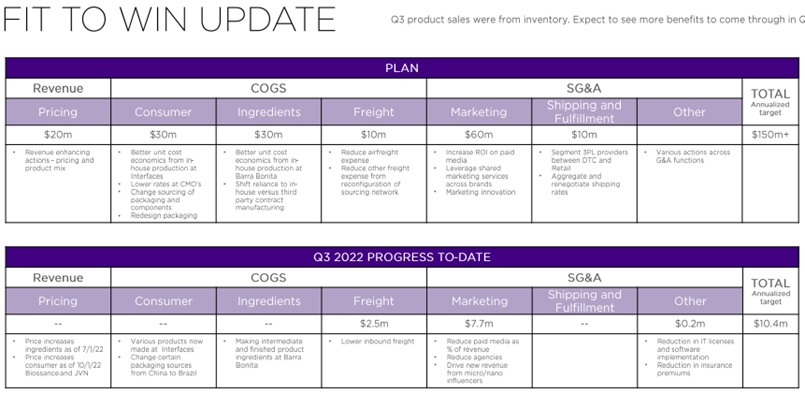

One quarter later, the opportunities were refined in the Q3’22 EC:

{kind=link}

investors.amyris.com/events-and-presentations#past

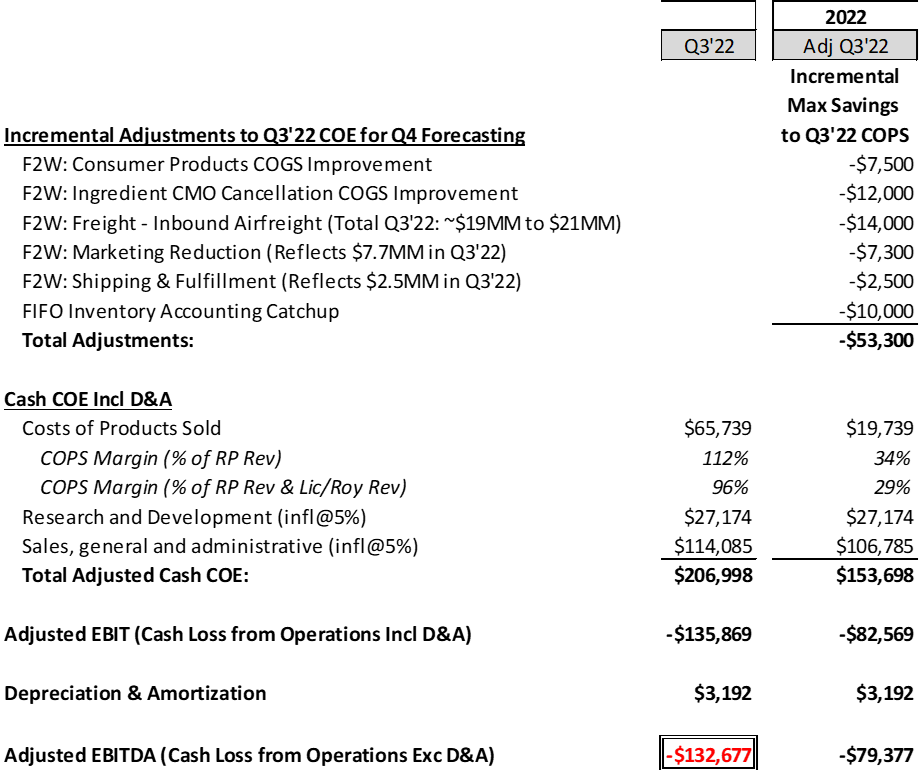

If we were to exclude those items from the Q3’22 results, we can understand what the improvement would have been to COPS and Adjusted EBITDA on a pro forma basis and can use this technique to forecast future quarters (using Q3’22 as a baseline):

{kind=link}

Author Analyses

Revenue Forecasts for Q4’22 and Q4’23

During the Q3’22 EC, Management provided $100MM Core Revenues guidance for Q4’22 and $200MM Core Revenues with $20MM Operating Income guidance for Q4’23.

We will discuss two Methods to triangulate first on forecasted Q4’22 Consumer Revenues.

Method 1: Management Guidance

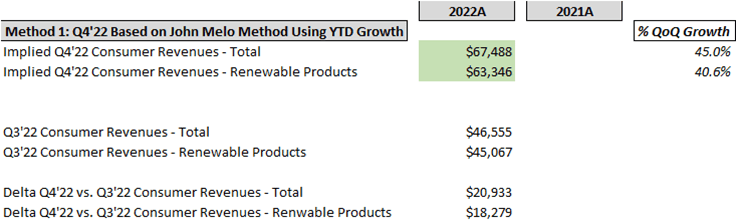

Management indicated Q4’22 Consumer Revenues will reflect the YoY growth seen in 9-month YTD Consumer Revenues for 2022. Using the implied growth-rate range we can forecast 12-month 2022E Consumer Revenues:

{kind=link}

Author Analyses

This provides us with an estimated range of $63.3MM to $67.5MM reflecting a 40.6% to 45% QoQ growth-rate:

{kind=link}

Author Analyses

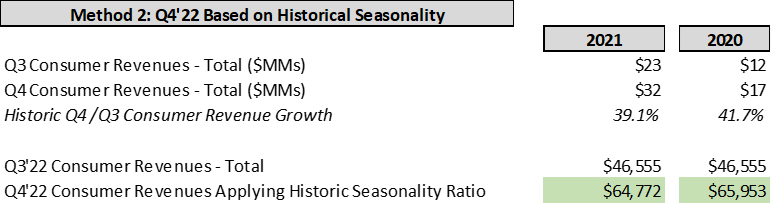

Method 2: Applying Historic QoQ Seasonality

We shouldn’t trust management’s guidance at face value. We can examine historic QoQ seasonal growth for the prior two years to sanity-check whether historical seasonal growth rates yield similar results (which they do: 39.1% to 41.7% derived below):

{kind=link}

Author Analyses

Both methods point to similar revenue range estimates and QoQ growth rates.

To help Amyris achieve those targets, there are elements this year that were not included in the Q3’22 Revenue base, which will lower the bar/hurdle:

- A preliminary review of cross-border (e.g., T-Mall) transactions in China reflect strong D2C Biossance Revenues: Estimated to be >$11MM for Q4’22 (driven in large part by a three-day ‘ Singles Day ’ event).

- 4U by Tia: Estimated Ship-to-Trade Walmart Revenues of between $2MM to $4MM in December.

- Stripes & Ecofabulous are expected to contribute ~$1MM in revenues for the quarter.

This will drive the QoQ Like-for-Like growth requirements on pre-existing brands down to ~25% (very achievable), given the already strong brand performance mentioned in recent press releases:

- 11/28/22 : AMYRIS CONSUMER BRANDS DELIVER RECORD BLACK FRIDAY WEEK SALES

{kind=link}

investors.amyris.com/2022-11-28-AMYRIS-CONSUMER-BRANDS-DELIVER-RECORD-BLACK-FRIDAY-WEEK-SALES

- 11/30/22 : AMYRIS CONSUMER BRANDS DELIVER 80% CYBER MONDAY LIKE-FOR-LIKE GROWTH

One area of uncertainty remains the Brick & Mortar component. While D2C outperformed expectations in many areas, we do not have clear visibility into Q4’22 B&M sales, and I believe this quarter the B&M share will underperform the D2C side and will not achieve record B&M sales.

Preliminary reviews of retail foot traffic indicate that this year is less than prior years and there are small signs of Q4’22 weakness. As a result, we expect the prior B&M/D2C ratio of 45/55 to flip this quarter in favor of D2C.

INGREDIENTS

Turning to Ingredients, we previously saw that Q3’22 ingredient revenues were only ~$13.5MM (significantly lower than guided).

Q3’22 Ingredients Revenue expectations on 8/9/22 had been set on all three main production lines (i.e., six 200k liter tanks) beginning production one week later:

seekingalpha.com/article/4532027-amyris-inc-amrs-ceo-john-melo-on-q2-2022-results-earnings-call-transcript

However, the reality was somewhat different as we discovered in the subsequent quarterly filing:

{kind=link}

investors.amyris.com/sec-filings?cat=2

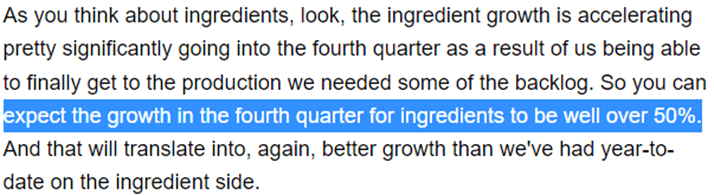

This was a disappointment relative to the original guidance resulting in a significant miss on ingredient revenues. However, as of 11/8/22, all three main lines are producing:

{kind=link}

seekingalpha.com/article/4555043-amyris-inc-amrs-q3-2022-earnings-call-transcript

{kind=link}

seekingalpha.com/uploads/2022/8/7/11765171-16598821362437603_origin.png

This has accelerated ingredient revenue growth by >50% QoQ going into the fourth quarter:

{kind=link}

seekingalpha.com/article/4555043-amyris-inc-amrs-q3-2022-earnings-call-transcript

Only one line was up and running at the start of Q3’22...

{kind=link}

investors.amyris.com/sec-filings?cat=2

...with the second up and running in the middle of Q3’22 requiring ramp-up time for that line to achieve full production. If you take the Q3’22 ingredients of $13.5MM and increase it by the “well over 50%” you get to >$21MM. As such, I have set our case range to between $22MM to $24MM.

We now have a relatively tight range forecast for Q4’22 and Q4’23 revenues with the following management assumptions:

- Consumer Revenues for Q4’23 will follow a similar growth trajectory as Q4’22

- Ingredient Revenues will have achieved max-capacity utilization at $30MM-to-$35MM by Q4’23

- There will be incremental earnout contributions from DSM, Reb M and the new ST Buyer

{kind=link}

Author Analyses

We can now forecast Q4’22 and Q4’23 COE by allocating a portion of the Adjustments to COE identified previously in various case scenarios:

{kind=link}

Author Analyses

This drastically reduces Costs of Products Sold (“COPS”) and, while the cash “burn” for Q4’22 is still significant (ranging from ~$95MM to ~$106MM), it remains a significant improvement over Q3’22 results and converges towards breakeven by Q4’23.

I struggle though to see how management will achieve a 10% operating margin for Q4’22 without higher top line growth or further reductions in SG&A (e.g., Marketing).

Working Capital Management

Investors are concerned with Amyris' management of working capital components:

- Payables

I noted a rapid increase in Accounts Payable balances for the firm:

Author Compilation

Investigation into this has confirmed that Amyris is extending its credit terms with vendors/suppliers to a 60-to-90 period, thereby providing more liquidity to Amyris. While this balance will shrink going into 2023, management expects levels to remain elevated going forward under the new structural shift in payment terms.

- Receivables

Amyris has a few receivables that are owed to them:

- DSM receivable of ~$20MM

- An Ingredion Working Capital Contribution estimated @$20MM-to-$30MM for its member interest in the RealSweet shell-entity related to the production of Reb M and the associated downstream finishing facility

- Inventory

Inventory levels have elevated to ~$129MM to maintain an estimated ~two quarters worth of safety stock in anticipation of seasonally high Q4’22 demand as well as potential further supply chain shocks (e.g., China).

{kind=link}

investors.amyris.com/sec-filings?cat=2

The high cost of that inventory, sourced from third-party manufacturers, will likely be depleted on a FIFO basis over time resulting in elevated COPS for a portion of the fourth quarter and possibly the first quarter of 2023. Once that inventory is cleared, margins will improve rapidly under the insourced manufacturing cost structure. Additionally, Amyris anticipates that they will be able to free up capital from the Inventory liquidation as they will not need to maintain as much inventory going forward and the cost of inventory for similar unit volumes will be significantly lower due to insourcing from their own consumer manufacturing facilities.

- Prepayments, Advances and Deposits

Amyris has approximately $25MM in prepayments to CMOs.

{kind=link}

investors.amyris.com/sec-filings?cat=2

As the transition to Barra Bonita nears completion, the cash conversion of the prepayments will free up additional capital over the next few quarters.

As a notable example of a large prepayment, a final CBGA production run of ~20 tonnes from S.A. Antibioticos (a Spanish CMO) was made shortly after the termination of its relationship with Amyris:

usimports.info/buyers-amyris/data-1.html

This volume of CBGA was impressive and likely one last advance production run to be used for future new formulations/SKUs contemplated across various skincare brands (e.g., Biossance, Stripes, and Beckham).

- Employee Headcounts

While not a working capital item, we thought it important to note that Amyris has entered into a hiring freeze in November for which no new non-critical hires will be allowed and should an employee leave, the vacancy will not be filled unless it is deemed critical in nature by Amyris. This policy is expected to continue for some time after the closure of the ST.

- Cash

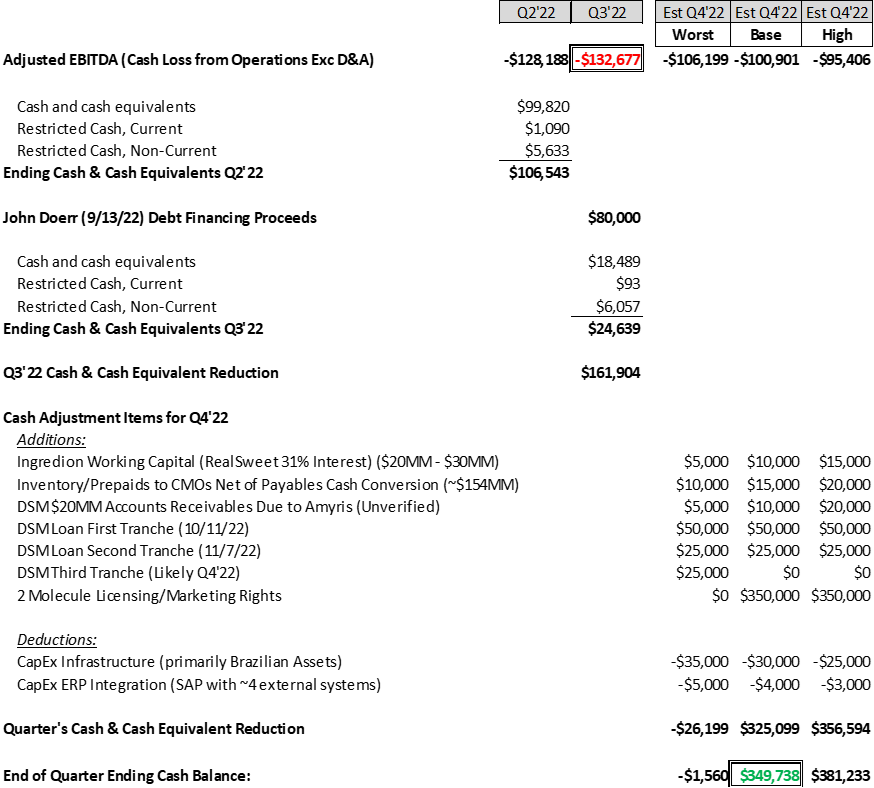

Using the earlier estimated Adjusted EBITDA forecasts, we can generate a waterfall of what the cash position of the company may look like over the near future:

{kind=link}

Author Compilation

One thing is clear, is that the ST is critical to maintaining a healthy Balance Sheet.

Strategic Transaction Slated for 2023 Molecule Marketing Rights

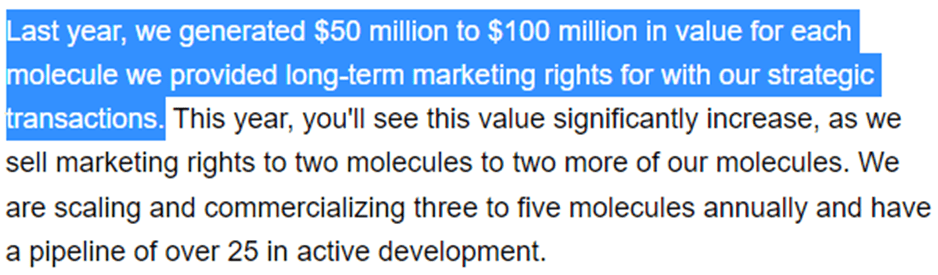

The typical value generated for molecules in early-stage development (i.e., unproven from a commercial standpoint) is $50MM to $100MM based on historical transactions:

{kind=link}

seekingalpha.com/article/4532027-amyris-inc-amrs-ceo-john-melo-on-q2-2022-results-earnings-call-transcript

RISK FACTORS

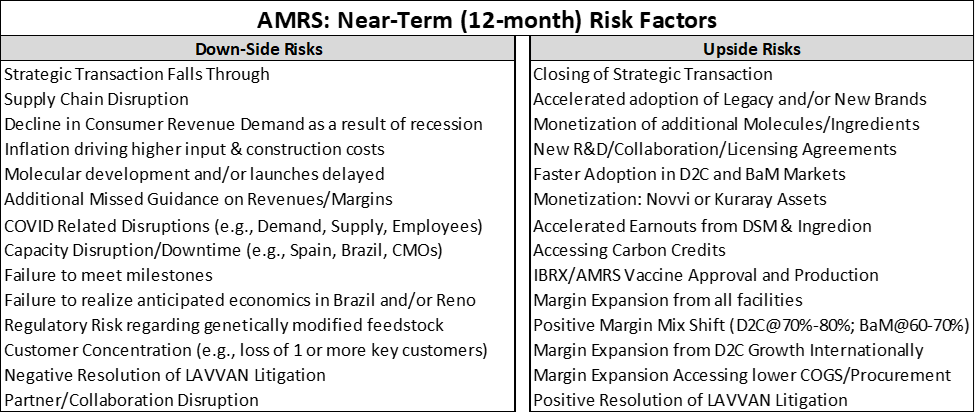

{kind=link}

Author Compilation

Conclusion

The market has priced Amyris for bankruptcy just as the Company lies on the cusp of closing the largest deal of its existence (i.e., $500MM in cash value).

The Company's track record in closing Strategic Transactions like these has been 100% over the past few years and historically, deals of much smaller sizes have catapulted the stock to lofty levels.

In the end, Amyris has put its shareholder base through a rollercoaster ride of emotion over the past twelve months and there is a sense of fear and distrust. The firm has proven it can drive top-line growth but ignored the convergence to the bottom line, in my opinion.

I believe t his p ivotal deal will eliminate concerns of bankruptcy and dilution and turn the conversation back towards achieving profitability.

Management will be scrutinized intensely for the quarters to come, as investors seek confirmation that management is truly focused on cost management. I remain optimistic that in the next two to three weeks we will have good news and I look forward to that day.

For further details see:

Amyris: Show Us The Money