AMRS - Amyris: Sub-Scale With High Fixed Costs And Limited Growth

2023-04-19 09:33:20 ET

Summary

- Amyris' margins continue to deteriorate due to input cost inflation and inefficiency.

- Growth has slowed significantly, which is problematic given the introduction of large fixed costs over the past 12 months.

- Amyris has limited runway in which to resolve its current issues, and yet management is taking little action.

Amyris’ ( AMRS ) fourth quarter earnings were a disappointment on every level. Growth has slowed significantly and costs continue to increase, despite efforts to reduce spending and easing inflationary pressures. Management is now being forced to take actions that should have been made 12 months ago, but it is no longer clear that Amyris has the assets to finance losses until profitability is achieved.

Amyris still has a number of valuable assets (brands, molecules etc.), which should stave off bankruptcy for at least the next few years, but management needs to take far more drastic actions than they have planned if they are to turn the company around.

Growth

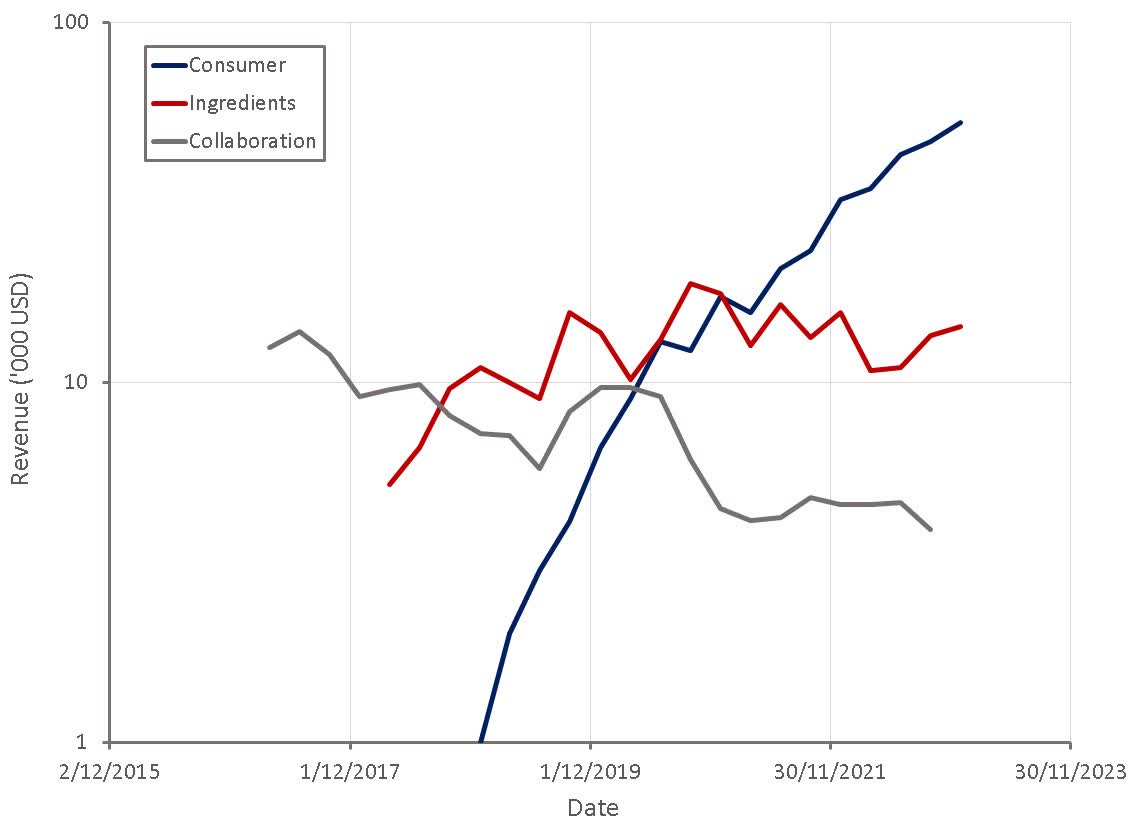

Amyris’ consumer revenue growth slowed to approximately 64% YoY in the fourth quarter, and ingredients revenue continued to be fairly flat, despite Barra Bonita supposedly debottlenecking production.

Management suggested that their larger brands performed well and that much of the consumer business weakness was the result of a slowdown in investments in new brands and ship to trade due to a lack of cash. Growth from existing brands was only 50% YoY in the fourth quarter though, suggesting that there has been a broad based reduction in growth investments or consumer demand.

Figure 1: Amyris Q4 2022 Core Revenue (source: Amyris)

Management has suggested that ingredient production has been challenged by capacity, access to feedstock and working capital. As a result, Amyris has 14 million USD of unfilled ingredient orders, which are mainly related to farnesene and RebM. These issues are expected to be resolved in the first half of 2023.

Real sales growth may also have been even weaker than it appears on the surface given that Amyris was planning on raising prices. Price increases as part of management’s fit-to-win initiative were supposed to drive a 5 million USD quarterly improvement in profits. Assuming that these price increases have been implemented, revenue growth in the fourth quarter was even weaker than it appears.

{kind=link}

Figure 2: Amyris Revenue (source: Created by author using data from Amyris)

Unit Economics

While continued strong growth is necessary for Amyris, due to the high cost structure that management has put in place over the past two years, a failure to make progress on unit economics is more concerning. The unit economics of both the ingredients and consumer business are negative and don’t appear to be improving.

Figure 3: Amyris Q4 2022 Non-GAAP Gross Margin (source: Amyris)

Taking into account elevated freight expenses, Amyris’ ingredients gross margins could be below -200%. Despite energy and shipping costs easing, and Amyris insourcing production at Barra Bonita, ingredient gross profit margins have continued to slide.

Table 1: Amyris Ingredient Business Unit Economics (source: Created by author using data from Amyris)

While consumer gross profit margins are quite robust, marketing expenses have been high in order to drive growth, and shipping and handling costs have been extraordinarily high. Marketing expenses will decline as growth moderates and the business scales, particularly if weaker brands are divested, but the DTC business needs significantly lower shipping and handling costs to be viable.

Table 2: Amyris DTC Business Unit Economics (source: Created by author using data from Amyris)

Feedstock

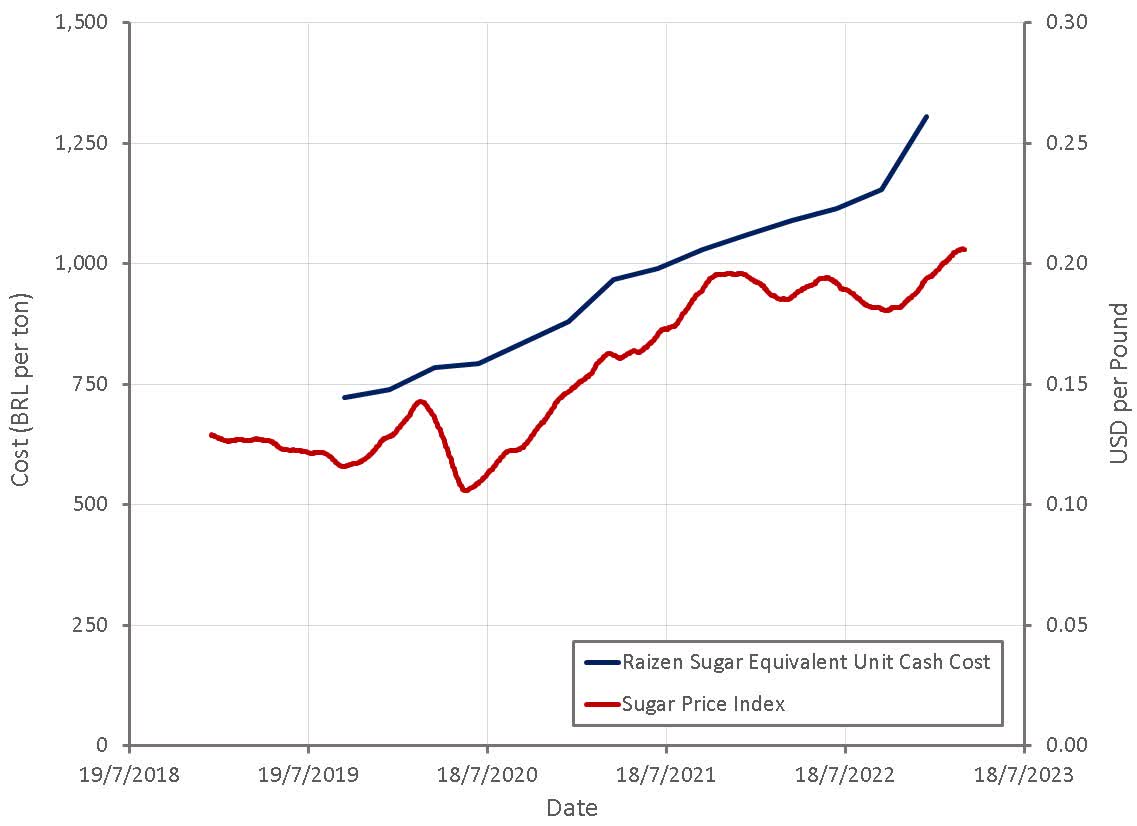

While Amyris’ ingredient gross profit margins should have improved in the fourth quarter due to the ramping of production at Barra Bonita and an easing of inflationary pressures, this may have been undermined by rising feedstock costs. The price of sugar has been trending up over the past few years, and feedstock is one of the main drivers of cost in the fermentation of low value molecules.

{kind=link}

Figure 4: Indicators of Rising Feedstock Costs (source: Created by author using data from Raizen)

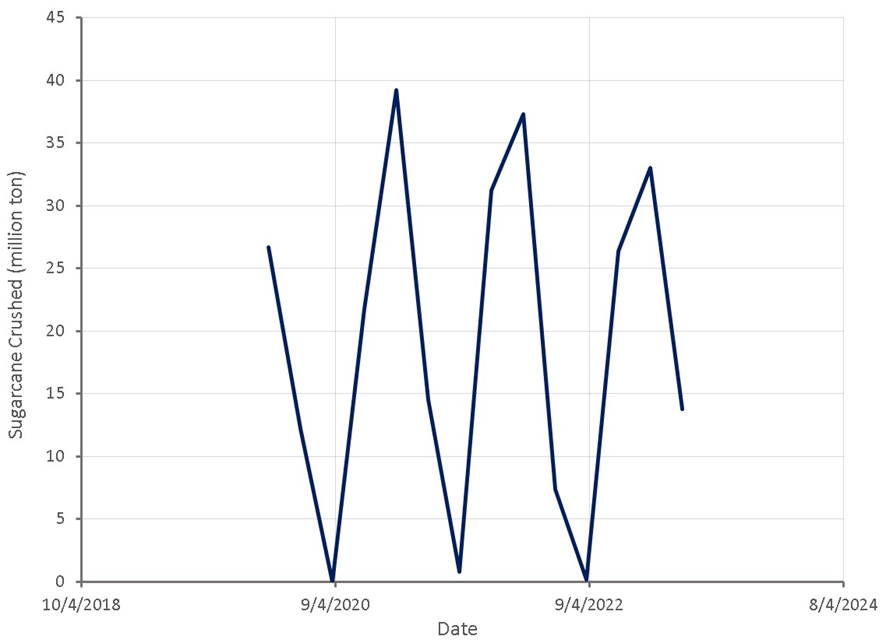

Amyris' fourth quarter also falls outside of the sugarcane harvest peak in Brazil. Sugarcane in Brazil can be harvested from April to December in the south-central area, which can impact production costs. In the past Amyris has based facility maintenance around the sugarcane harvest season in an attempt to avoid elevated production costs. During the offseason Amyris has had to use raw VHP sugar crystals as feedstock, rather than concentrated cane syrup. Amyris has previously estimated the cost of switching feedstock as somewhere around 0.6-0.75 USD per liter , which is quite large relative to the production cost of farnesene.

{kind=link}

Figure 5: Raizen Sugarcane Crushed Volumes (source: Created by author using data from Raizen)

Barra Bonita

The ramp of Barra Bonita was expected to contribute to significant improvements in the economics of the ingredients business in 2022, but so far this has not been the case. Management has provided essentially no commentary on the facility or how it is performing versus expectations. Given that the three large lines were expected to be operational in August, and yet the third line was only commissioned in the fourth quarter, it seems likely there have been significant issues. Reading between the lines on management’s commentary it also seems like commissioning caused issues in the fourth quarter, reducing production at Barra Bonita.

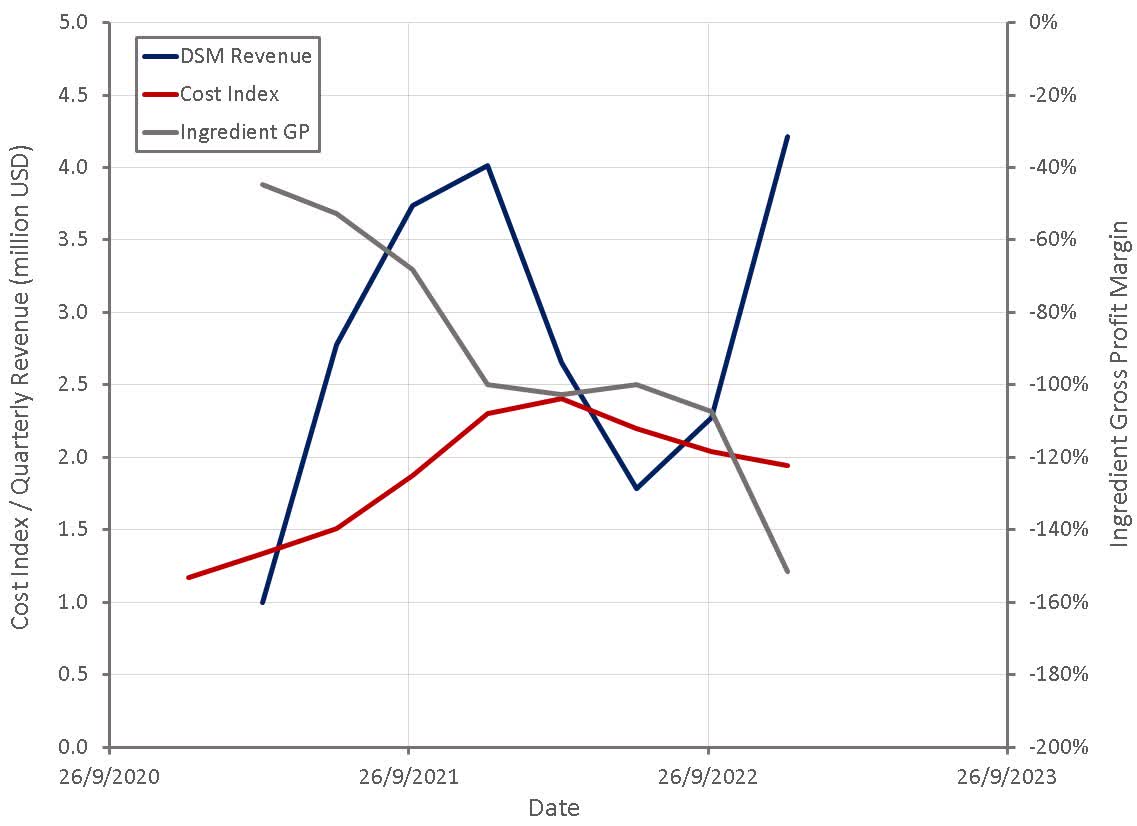

Amyris has given little detail on what or how much is being produced at Barra Bonita, but product revenue from DSM may be indicative. In early 2022, Amyris reduced production for DSM, presumably due to cost pressures. This production ramped up again later in the year as the Barra Bonita facility came on line, suggesting that the facility is largely being used to support F&F production for DSM. This seems to align with management commentary and shipping data.

This would be problematic though, as it would suggest that Barra Bonita has dragged margins lower, rather than improving them. As production ramped in the second half of the year, ingredient gross profit margins declined, even as cost pressures began to ease.

{kind=link}

Figure 6: Amyris Product Revenue from DSM (source: Created by author using data from Amyris)

While all three large lines are now fully operational, and Amyris managed to produce four different products in the fourth quarter, the facility is far from finished. The two smaller lines are apparently not even connected and downstream processing is not in place. Management has suggested that Barra Bonita will lead to performance improvements that are spread out over the year as the facility ramps, but without additional capacity or DSP, gains may be limited.

Consumer COGS

Management continues to give limited information about the profitability of the consumer business, although it did suggest that DTC gross margin increased 6% YoY in the fourth quarter. This is not a surprising result given supposed price increases and the in sourcing of production.

The Interfaces facility is reportedly leading to better than expected production costs. For example, the COGS of Biossance bestsellers has reportedly been reduced by an estimated 50% . It is anticipated that 60% of consumer volumes will be manufactured at Interfaces by the third quarter of 2023, which is expected to deliver a 3-4% improvement in consumer business gross profit margins. This is neither here nor there though, as consumer COGS are not a particularly important cost driver for Amyris.

Unknown COGS

Amyris excludes a number of costs in calculating an adjusted gross profit. Other costs and provisions are excluded from the adjusted gross profit calculation and is reportedly largely made up of certain freight and manufacturing expenses. Prior to the fourth quarter it seemed likely that this line item was being driven by air freight, elevated shipping costs and elevated CMO expenses, but this is now less clear. Other costs and provisions have continued to increase, even as the use of air freight and CMOs has declined and shipping expenses have fallen. Management has given no commentary on why this line item exploded in the fourth quarter, or what it primarily consists of.

{kind=link}

Table 3: Other Costs and Provisions Component of Non-GAAP COGS - Percentage of Product Revenue (source: Created by author using data from Amyris)

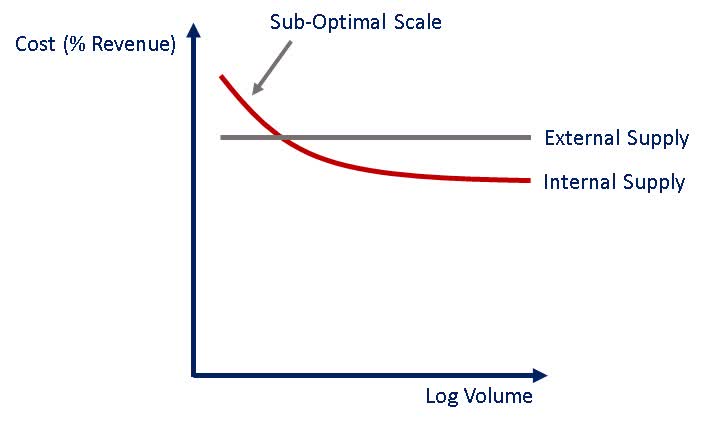

Fixed Costs

The deterioration in gross profit margin is difficult to understand given easing supply chain issues. In addition to rising feedstock costs, Barra Bonita, Interfaces and Reno may be operating below the minimum viable scale, causing their start up to increase costs rather than reduce them.

{kind=link}

Figure 7: Potential Impact of Vertical Integration on Production Costs (source: Created by author)

While it is difficult to say that vertical integration has undermined Amyris’ profitability, there clearly has been limited benefit so far. With Amyris’ current business mix and revenue, COGS should probably only be around 20-25 million USD a quarter. For comparison, quarterly lease expenses, depreciation and employee costs related to production in Brazil are probably in the vicinity of 8 million USD. The introduction of these fixed costs will need to expand capacity and reduce variable costs significantly to be worthwhile.

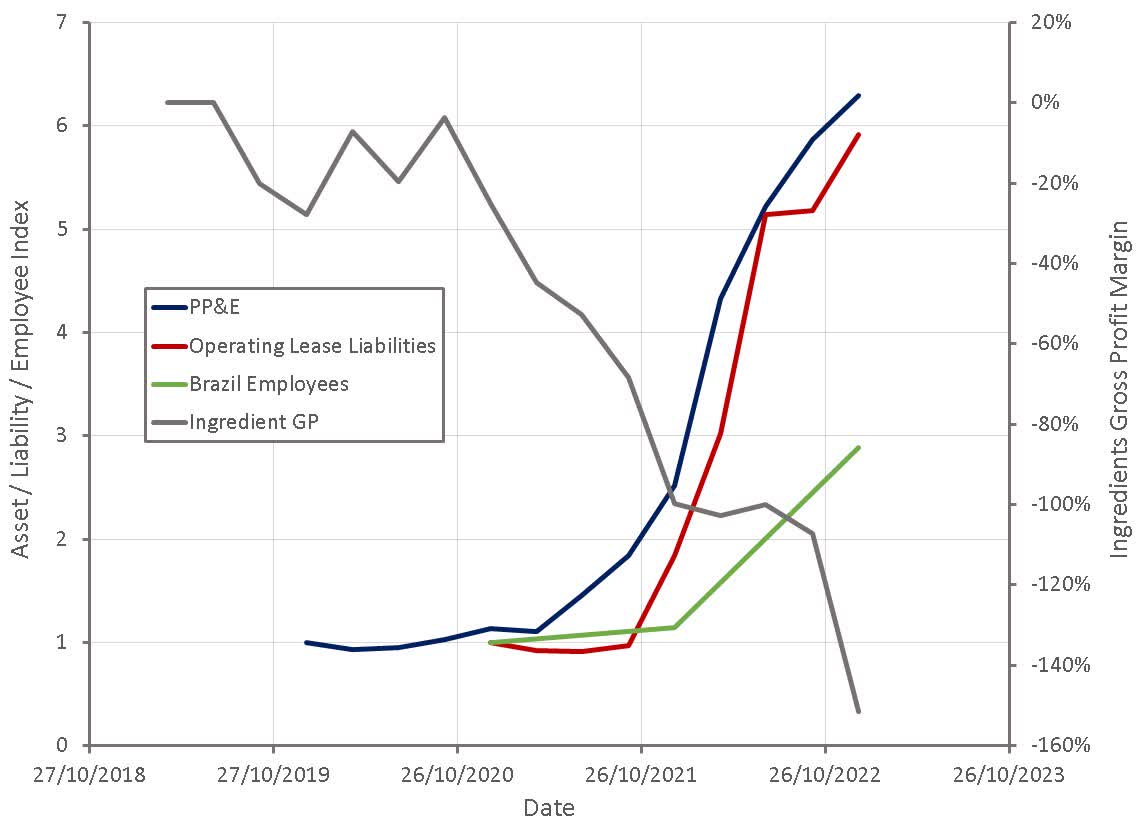

{kind=link}

Figure 8: Amyris PP&E, Operating Lease Liabilities and Employees in Brazil (source: Created by author using data from Amyris)

Logistics

Amyris' air freight costs declined from 12.7 million USD in the third quarter of 2022, to 3.5 million USD in the fourth quarter. Freight and logistics expenses are expected to continue to decline as production at Barra Bonita is ramped and consumer manufacturing and component sourcing is transitioned to Brazil.

Shipping and handling expenses increased by 5.5 million USD YoY though, a 68% increase. This is an unsustainably large cost, and it is not clear why Amyris has not been able to control this line item at all over the past year. Amyris recently negotiated a new shipping and parcel agreement with a large global provider, which is expected to save 15-20 million USD over the 3-year life of the contract.

{kind=link}

Table 4: Amyris Shipping and Handling Expenses (source: Created by author using data from Amyris)

Headcount

Amyris has hired aggressively over the past two years, causing a dramatic increase in headcount. The increase in headcount is perplexing, even if Amyris was managing to meet its own ambitious growth targets, but given recent actual growth and expected growth in 2023, the increase in headcount appears suicidal.

{kind=link}

Table 5: Amyris Employees (source: Created by author using data from Amyris)

The CEO has eliminated 30% of his direct reports , and the executive team has reportedly been reduced by 60%. There were 1.2 million USD of restructuring charges incurred in the fourth quarter related to these layoffs.

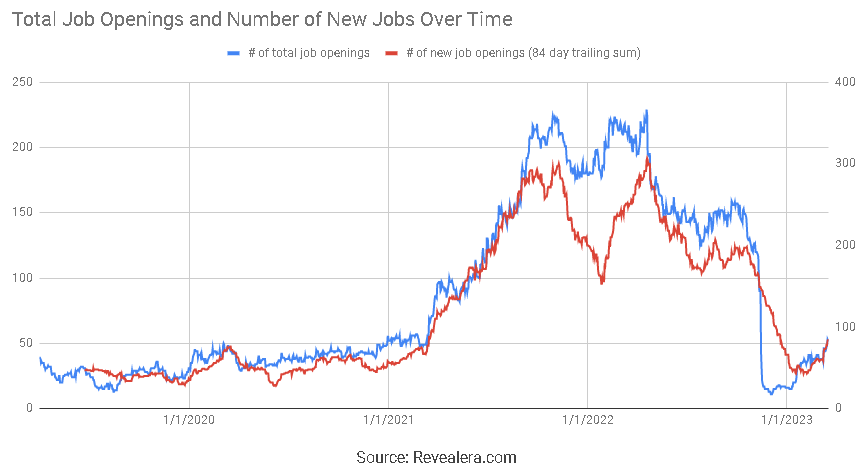

There was also a hiring freeze in the fourth quarter, but so far no large layoffs have been announced, and job openings have begun to creep up again in recent weeks. Amyris expects 9-10 million USD of savings in 2023 from staff reductions and workforce attrition.

This is completely insufficient if management is serious about achieving profitability any time soon. Given growth expectations for 2023, Amyris should be trying to cut around 900 people rather than continuing to hire. If there is a lack of resources within Amyris at the moment, it is due to inefficiency and not insufficient headcount.

{kind=link}

Figure 9: Amyris Job Openings (source: Revealera.com)

R&D

Amyris' management has stated that they are committed to R&D , and hence this is an area that may not be subjected to cost cutting. This is questionable though, as R&D is a large contributor to losses and molecule commercialization has become a bottleneck rather than molecule development. Amyris currently has around 10 molecules that are ready to be scaled, and management has previously stated that they are developing 4-5 new molecules annually.

Without access to additional manufacturing capacity, Amyris may not be able to commercialize new molecules for the next few years, at which point they could have something like 20 molecules awaiting scale-up. This makes little sense given Amyris' losses and liquidity constraints. Either molecules should be monetized through outright sales or R&D investments should be scaled back until the company finds its financial footing.

Brands

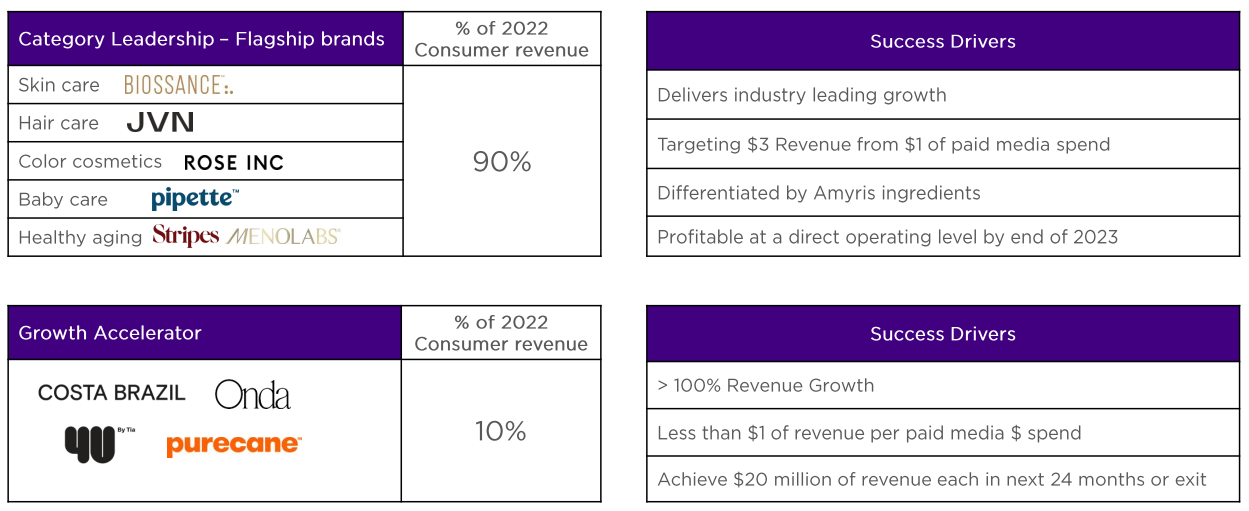

Management plans on reducing the number of consumer brands in 2023 to 5 or 6 . The brands that are kept are likely to make extensive use of Amyris’ ingredients and have a clear path to profitability. Divested brands are expected to bring in 150 million USD of cash proceeds this year and Amyris is reportedly in active discussions with potential buyers for these non-core assets.

Presumably Amyris is planning on keeping Biossance, JVN, Rose Inc, Pipette, Stripes and possibly MenoLabs. There is also 4U by Tia to consider, and the planned David Beckham fronted brand.

{kind=link}

Figure 10: Amyris Brands (source: Amyris)

Cash Needs

While management tried to paint the fourth quarter as an improvement in cash usage, not paying vendors is delaying cash use, not reducing it. In doing so, Amyris has also likely soured relationships, which will result in vendors refusing to do business in the future or only doing business on punitive terms.

After ridiculously suggesting several months ago that Amyris would be profitable by the end of 2023, management is now projecting a negative 200 million USD operating cash flow run rate in the fourth quarter of 2023, which is probably still optimistic unless more serious efforts are made to cut costs. Strategic transactions, manufacturing JVs, brand sales and earnouts will help finance losses in the short term, but may not be sufficient.

Amyris recently entered into a loan and security agreement for an aggregate principal amount of up to 50 million USD . The loan is to be repaid at the earlier of the closing of the Givaudan transaction or by June 8, 2023. The terms of the loan were fairly punitive, with a 12% annual interest rate and a repricing of previously issued warrants.

Amyris is currently in the process of negotiating another strategic transaction in the human health and pharmaceutical space. This is a competitive bidding process that will include squalene for adjuvants, and is expected to close in 2023. This will likely be a far smaller deal than the squalane / hemisqualane transaction, and without the complications, putting the timeline at less risk.

Amyris is now also considering JVs to reduce the burden of operating manufacturing facilities. Management has suggested that one of the world’s top four sugar producers is considering entering a JV that would involve the Barra Bonita facility, a future facility and downstream processing equipment. Amyris would receive 50-100 million USD and the partner would fund the next facility, which would be dedicated to farnesene production, and the installation of DSP equipment. The deal would also free up roughly 50 million USD of working capital, as the ingredients business has a long cash conversion cycle. If the deal progresses as expected, the next facility would be under construction by the end of 2023. From the details given, it is not really clear what the deal will involve, but there is a significant risk that after making a large investment over the last few years, Amyris will be forced to sell a stake at a significant discount.

Table 6: Amyris 2023 Sources of Cash (source: Created by author using data from Amyris)

At this point it is extremely difficult to estimate Amyris' cash usage. Losses will decline at some point as inflationary pressures continue to ease, particularly if management gets serious about cutting costs and improving efficiency. Amyris' cash usage in 2023 will likely exceed 500 million USD, leaving a financing gap that will need to be filled by equity or further asset sales.

Conclusion

The fourth quarter highlighted the fact that Amyris is yet to demonstrate that the ingredients business is viable. The last time Amyris tried to scale ingredient production they almost went bankrupt, and there is a risk that this will happen again.

While Amyris is clearly undervalued on a sum of the parts basis, there is little chance that the company’s assets will be liquated so that current investors can benefit from this value. Instead, it seems more likely that Amyris will continue to sell assets to finance losses.

For further details see:

Amyris: Sub-Scale With High Fixed Costs And Limited Growth