AMRS - Amyris: The Time Value Of Money

Summary

- Strategic transactions are a form of financing, and should be viewed as such when assessing their economics.

- Amyris is giving up a lot of value in the years ahead, but this makes sense when the cost of capital for Amyris and Givaudan is taken into account.

- Amyris will still likely need to access more outside capital in 2023, which could come from another licensing deal, brand sales or an equity raise.

Amyris ( AMRS ) needs access to outside capital due to a weak balance sheet and large losses, but their current situation makes obtaining financing difficult and expensive. As a result, Amyris may be willing to conduct deals with seemingly poor economics in order to obtain access to cash. Potential partners have no obligation to engage in a deal and hence will only be concerned with potential returns. This gives potential partners a strong negotiating position, although this is limited by the fact that a number of companies are interested in Amyris' assets.

There are ways that these transactions could create value for Amyris, but to a large extent they are a form of financing, and hence investors should not expect the terms to be particularly favorable. It is possible to agree to a deal that is beneficial to both parties though, due in large part to differences in the cost of capital. Amyris is on the verge of bankruptcy and has an extremely high cost of capital, whereas potential partners have a more normal cost of capital. Therefore, bringing cash flows forward is worth relatively more to Amyris.

Givaudan Transaction

The recently announced Givaudan ( OTCPK:GVDBF ) transaction appears to have disappointed most investors, but the terms are broadly in line with past transactions.

Givaudan will acquire a portfolio of cosmetic ingredients from Amyris, including Neossance Squalane, Neossance Hemisqualane, and CleanScreen (sun protection). Amyris will continue to manufacture ingredients for Givaudan to use in cosmetics, as well as provide access to their innovation capabilities. Givaudan will also become the commercialization partner for Amyris’ future beauty ingredients. The planned transaction remains subject to formal approvals from the relevant regulatory authorities, and the transaction is expected to close in the first half of 2023.

The asset purchase agreement appears to have been entered into on February 21, 2023. It is not really clear from the announcement, but it appears that Amyris is assigning certain distribution agreements, selling the relevant trademarks and granting a marketing license for the ingredients in cosmetics. The deal is for up to 350 million USD in near-term contributions, consisting of upfront cash and a three-year performance based earnout. The manufacturing portion of the deal is expected to bring the total value to approximately 500 million USD.

There is uncertainty in what manufacturing value means in these types of agreements as it could refer to gross profits or revenue and a discounted value or an undiscounted value. Presumably the reference is to undiscounted revenue to make the deal appear as large as possible. While this may make the deal appear bad, it is important to remember that gaining access to 350 million USD in near-term value is extremely valuable to Amyris. It is also a large amount of value when considering that the assets in question only generated 30 million USD revenue in 2022.

For Amyris, the deal comes down to a choice between continuing to market the ingredients themselves, or licensing to another party. While the cash flows for Amyris and Givaudan are equal and opposite, both can benefit from the transaction due to their vastly different cost of capital. Using reasonable discount rates for each company, cash flows in 10 years' time are probably worth twice as much to Givaudan as they are to Amyris. Amyris may also still decide to go through with a deal that has a negative NPV if they need the cash.

While the deal with Givaudan does not necessarily destroy value for Amyris, it is likely to significantly suppress ingredient margins in the future. After the earnout period, Amyris’ ingredient margins for Squalane and Hemisqualane are likely to be low or even negative, as Amyris are effectively repaying the loan from Givaudan. This is also problematic because it will tie up capital in a low margin business.

Management has previously guided to 10-20% ingredient margins after licensing deals, but this is hard to reconcile with the 150 million USD of manufacturing value in the Givaudan deal. Margins could be based on total costs and total downstream value (manufacturing + earnouts) over the contract period.

The above scenario only looks at how the “pie” is split between Amyris and Givaudan. It is also possible that by entering an agreement, the “pie” can be made larger, in which case Givaudan may be willing to pay a premium. For this to occur, Givaudan would have to believe that they are able to raise prices or increase volumes. Partners like Givaudan are likely to have significantly more sales resources and B2B relationships than Amyris, which could help them to drive volume. Givaudan also has a lot of product formulation expertise, which could be leveraged to increase demand.

The large amount of uncertainty around the deal highlights the poor communication with shareholders. Additional information required to understand the deal includes:

- Licensing period

- What does manufacturing value refer to?

- Assumed sales growth rate over the contract period

- Are there additional payments associated with access to innovation capabilities?

- Are there embedded options related to the commercialization of future ingredients?

Previous Transactions

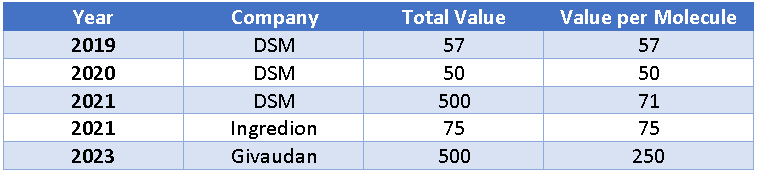

In 2021, Amyris signed an agreement with DSM Nutritional Products , a subsidiary of Royal DSM ( OTCPK:KDSKF ), for the exclusive rights to supply Amyris' product portfolio of flavor and fragrance ingredients, including seven intermediate products . The total transaction value was estimated at over 500 million USD, with approximately 1/3 attributed to an upfront payment, more than 1/3 attributed to potential earn-out payments based on milestones over a three year period from 2022 through 2024, and the remainder attributed to a 15-year manufacturing agreement and the expected value of developing and scaling a pipeline of new F&F molecules. The earnout is based on the EBITDA growth of certain activities, mainly products just launched and under development.

Amyris also entered into a deal with Ingredion ( INGR ) in 2021, where Ingredion, via its PureCircle subsidiary, became the exclusive global B2B commercialization partner for Amyris's sugar reduction technology that includes fermented Reb M. The parties also entered into an R&D collaboration agreement to create and advance the development of zero-calorie, nature-based sweeteners and potentially other types of food ingredients. As part of the deal, Ingredion became a minority partner in Amyris’ Barra Bonita facility. The transaction value was estimated to be worth 100 million USD, with 75 million USD of this attributed to the exclusive license to sell and market Reb M. Additionally, Amyris will earn a profit share from Reb M sales.

{kind=link}

Table 1: Past Amyris Transactions (source: Created by author using data from Amyris)

Based on past deals, Amyris could expect to receive around 125 million USD from Givaudan upfront. It seems likely that Amyris will receive a greater amount upfront in the current deal (~200 million USD), but in return will receive less downstream value.

{kind=link}

Table 2: Past Deal Breakdown by Component Contribution (source: Created by author using data from Amyris)

The deal valuation appears to be broadly in line with past deals, with a relatively large amount being received upfront and in return a smaller total amount. Valuation is difficult to assess without knowing expected growth rates and margins for the licensed molecules, and in some cases molecule revenue is not known for sure.

{kind=link}

Table 3: Past Transaction Valuations (source: Created by author using data from Amyris)

Amyris’ Cash Position

While the deal with Givaudan should have put investor concerns to rest, there is still uncertainty regarding when and how much cash Amyris will receive from Givaudan, and this raises questions about further financing needs. Cash burn has likely eased significantly in recent months due to:

- Reduced supply chain disruptions

- End of manufacturing in Europe

- Expansion of operations at Barra Bonita

- Insourcing of consumer manufacturing

- Optimization of shipping and fulfillment

- Continued growth

- Reduced management headcount

- Fit-to-win initiatives

Amyris can also temporarily reduce cash burn by using up existing inventory, delaying payments to vendors, accelerating payments from customers and pausing CapEx. This makes it difficult to say with any degree of certainty, how much cash Amyris has used over the past five months and how much they have remaining. It is possible that Amyris has sufficient cash to cover operations until near the end of March, although this would require a number of things to have gone right.

Regardless, Amyris does not have sufficient cash for the Aprinnova transaction. Amyris recently amended their share purchase agreement related to Aprinnova. The parties have agreed to extend the closing of the agreement until March 17, 2023 . This could indicate that Amyris believes they will receive payment before this date, or it could indicate an upcoming financing requirement. Amyris may also have generated cash from:

- Barra Bonita asset financing

- IP financing

- Receivables financing

- Asset sales

Another potential source of cash could be related to Givaudan announcing the availability of sustainably produced retinol. RetiLife is produced using a fermentation process, and while there has been no official announcement of who developed the technology, it is rumored to be Amyris. Retinol had previously been announced as part of Amyris’ product pipeline. At the J.P. Morgan Healthcare Conference in January, John Melo stated that production of a beauty ingredient at Barra Bonita would begin in the first quarter of 2023, although this could refer to ectoine or another ingredient. If Amyris developed or is producing retinol for Givaudan, there may have been an associated upfront payment.

Cost Cutting

Amyris appears to be closing Ecofabulous in an effort to prioritize profits over growth. This type of move should have been expected after Amyris announced at the J.P. Morgan Healthcare conference that they were segmenting their brand portfolio into "Category Leaders" and "Growth" brands. Costa Brazil, Onda Beauty, Olika and Purecane will also need to demonstrate growth and a viable path to profitability or will likely be shutdown as well. Support for Olika has already been pared back significantly, with Olika no longer available through the website or Amazon.

This may not reduce cash burn that much though, as Ecofabulous only has 11 employees on LinkedIn. In addition to this, Ecofabulous is likely sharing resources with other brands and would have had its own marketing budget.

{kind=link}

Figure 1: Ecofabulous Closing Notification (source: Ecofabulous)

At this point it seems quite likely that sizeable layoffs could be in the works, and it is somewhat baffling that this hasn't already been done. After missing guidance in 2022 and significantly reducing guidance for 2025, Amyris appears overstaffed for their current size and growth trajectory. Management may be reluctant to cut jobs, but it is better to let employees go during a strong labor market so they can find other opportunities, rather than to reduce headcount in the midst of a downturn.

Conclusion

Many investors have failed to appreciate that the licensing deals are to a large extent a form of financing for Amyris, and as such Amyris has to “repay” the upfront consideration over time. The deal with Givaudan may seem unimpressive, but it provides capital that will allow Amyris to move closer to profitability. The deal is unlikely to create value for Amyris, but it may not be particularly harmful. Amyris is not an ingredients business, and they continue to demonstrate a willingness to sacrifice the ingredient business in order to focus on their technology platform and consumer businesses.

Amyris is a business with ongoing problems, many of which are due to external factors. Most of these issues are likely to be addressed or resolve themselves in 2023, but Amyris remains risky due to its low cash balance. Investors should keep in mind that Amyris "turned the corner" months ago and still controls assets (Biossance, JVN, Rose Inc, Pipette, Stripes, Barra Bonita, 10 molecules ready to be scaled) that dwarf their current enterprise value.

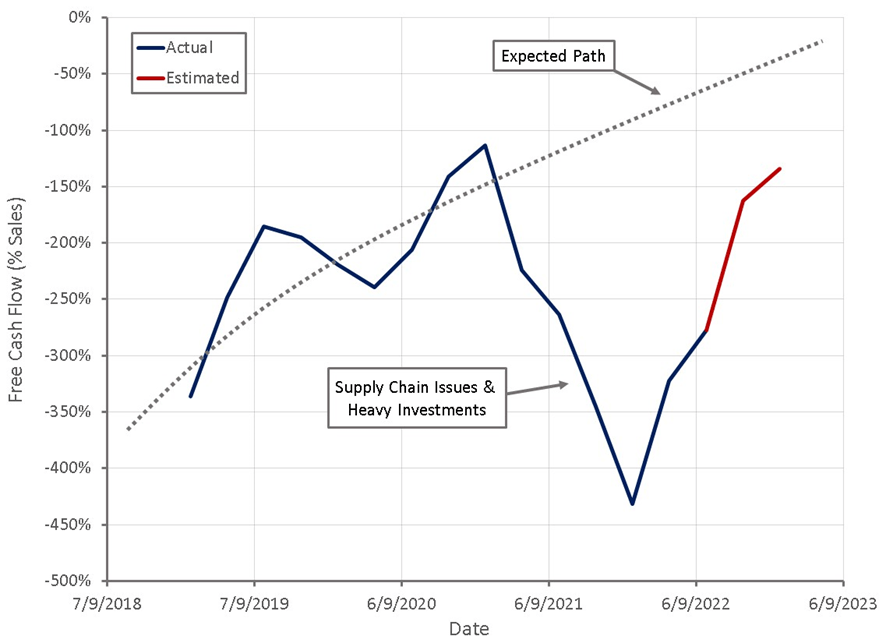

Figure 2: Amyris Free Cash Flow as a Percentage of Sales (source: Created by author using data from Amyris)

{kind=link}

For further details see:

Amyris: The Time Value Of Money