ET - AMZA: 4 Reasons I'm Not Buying It

2023-05-25 12:50:42 ET

Summary

- AMZA has a long track record of underperforming in terms of both share price, total return, and dividend growth.

- We can't blame this on the industry alone because most MLP stocks are performing much better.

- You can probably do a lot better by simply buying and holding some MLP stocks.

InfraCap MLP ETF ( AMZA ) is a somewhat popular fund among investors seeking high dividend yields who want to get exposure to MLPs (Master Limited Partnerships) while avoiding the hassle of K-1 forms. I think investors should mostly avoid this ETF and pick their own MLPs if they want exposure to this sector. Below I will list the reasons.

Reason 1: Terrible underperformance

Since its inception and in the last decade, this fund had a pretty bad performance overall. The stock is down -87% and its total return (after reinvestment of dividends is down -50%) even before counting the effects of inflation. The fund has been doing a bit better since bottoming in 2020, but still it could take many years for it to regain its losses.

Some investors will object to this and say that the reason for this fund's underperformance is because the whole MLP industry suffered a lot in the last decade and most MLP stocks haven't performed that great either. While this is true, this fund underperformed most of its holdings. Below, you will see the performance of top 5 current holdings of this ETF, combination of which account for more than 50% of its total weight. Notice that 4 out of 5 holdings actually had positive results in the last decade with total returns ranging from 24% to 84% during this time, while the ETF itself was down -50% in total returns during this time. In the last decade, the ETF performed as bad as its worst holding out of the top 5 holdings ( MPLX ). There is no excuse for this type of underperformance.

Reason 2: Shrinking dividends

Many times, investors buy funds with declining value and say that they are in it for the dividend and don't care for the fluctuations in the share price, but this fund's dividends have also been shrinking along with its stock price and NAV. If you bought the stock 10 years ago because of its high dividend of ~10% at the time, you will be shocked to see that your current yield on your original investment will be only about 2% because of how much the dividends shrank over time.

Again, people will say it's because the whole industry was cutting dividends for a big part of last decade, but we are not really seeing it when we look at the fund's top 5 holdings which account for more than 50% of its total weight. Notice that Western Midstream Partners ( WES ) hiked dividends by 330% in the last decade, MPLX hiked dividends by 171% and Energy Transfer ( ET ) hiked their dividends by 87% during this time. Even the worst performer of the top 5 ( PAA ) only dropped its dividends by 54% as opposed to AMZA, which reduced its dividends by more than 90% since inception.

So what kind of fund underperforms its top 5 holdings (accounting for +50% of its total weight) both in share price and dividend growth by such a huge margin? If the fund just held its top 5 holdings and didn't actively trade in and out of positions, it would have performed much better than it did

Reason 3: Investors can easily pick their own stocks

At the end of the day, there aren't that many big players in MLP industry, and investors can simply pick 4-5 that they feel comfortable with. You only need to add a few criteria such as dividend history (both in terms of consistency and growth), share price trends (either appreciation or at least holding steady), management's philosophy in terms of managing their balance sheet, relatively low debt and strong margins.

If you are not big on picking stocks, you can just go ahead buy the top 5 holdings of this fund that are shown above, and you will likely outperform the fund itself as it actively trades in and out of positions and uses leverage to make things even worse.

Sure, you will have to deal with K-1 tax forms, but it's better than suffering a terrible underperformance and losing your money.

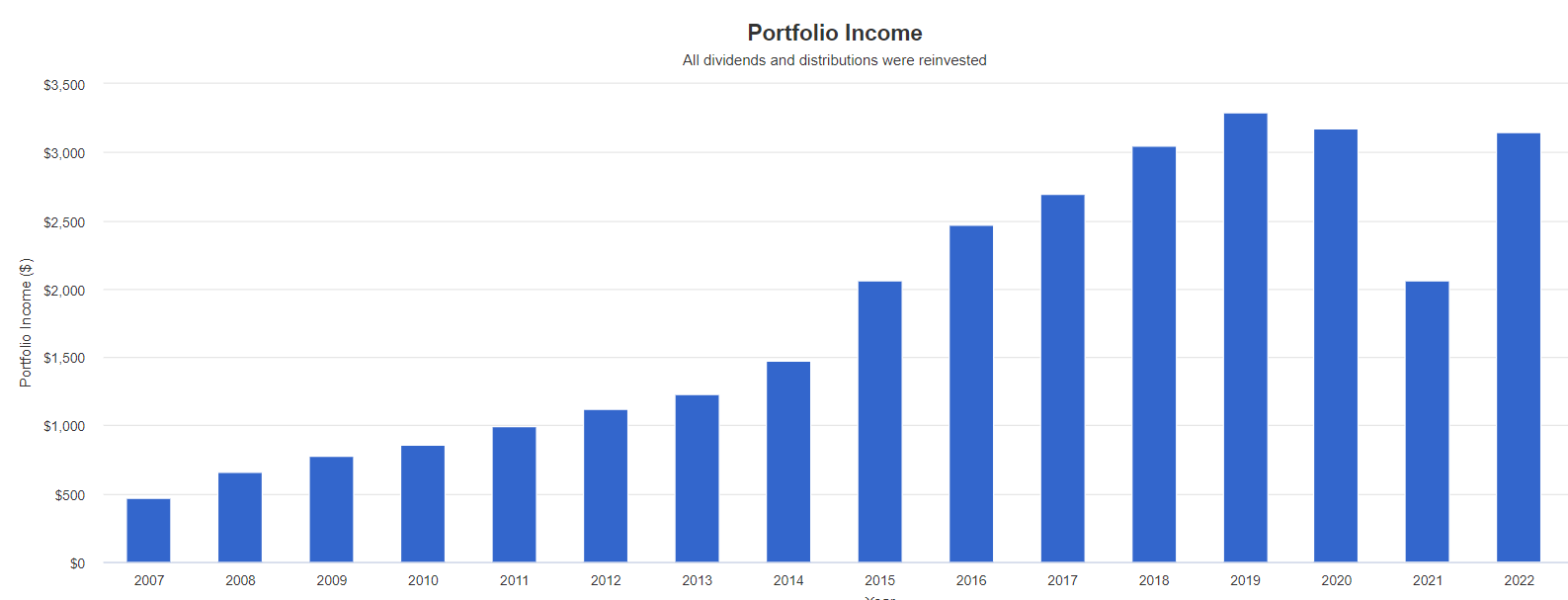

Let's take Energy Transfer (ET) for example. The stock has a low P/E of 9 and high dividend yield of 9.64%. Its history of dividend payments is mostly stable with some growth. If you had bought $10k worth of ET in 2007 when it became public, your money would have grown to $40k by now and if you reinvested your dividends along the way you'd be generating a dividend of $3.1k per year right now which represents a yield of 31% on your original investment.

{kind=link}

If you are in MLPs mostly for dividends, another metric you want to pay attention is their cash flow, especially cash from operations. Typically, this is where dividends and stock buybacks come from. Notice that most major MLPs were able to grow their operating cash flow nicely in the last decade, ranging from 88% to 3000% of growth. The industry as a whole has been doing very well, and you can do a lot better than how this ETF has been performing.

Since this industry tends to be capital intensive, another metric to pay attention is return on capital. This tells you how much money each company makes for each dollar they spend. The higher this number, the better it is because it means the company will be able to return more capital to you since it is able to gain more capital from its investments. Notice that this number generally ranges from 8% to 20%, and it can also fluctuate wildly depending on oil prices. For example, in 2020 many of these companies had negative return on capital, but this shouldn't surprise anyone since oil price dipped too much during the year as a result of shutdowns and lockdowns.

Reason 4: We could be headed towards recession

There are indicators showing that we could be headed into recession, and recently declining oil prices seem to agree with this assessment.

I am not saying you should sell your energy and oil stocks because of a possible recession, but you certainly don't want to be in a fund that uses leverage, actively trades and has a long track record of underperforming not only the overall market but even its largest holdings. Buying and holding individual MLP stocks through a recession could be ok especially if the company has a solid balance sheet and sustainable dividend but holding an underperforming and leveraged ETF during this time can lead to disaster.

Conclusion

AMZA attracts a lot of income focused investors due to its high dividend yield and lack of K-1 tax forms, but it has been underperforming for a long time both in terms of share price, total return and dividend growth. The fund even underperforms its own holdings by a vast margin. Investors would be better off by picking 3-5 MLPs and sticking with them instead of buying this fund. Even buying and holding top 5 holdings of this fund seem to be a better choice than buying this fund.

For further details see:

AMZA: 4 Reasons I'm Not Buying It