VZ - Another Year In Review With Some Thoughts For 2024

2023-12-06 10:45:00 ET

Summary

- In this review, I take a look at what themes worked well in 2023. I also give some advice on how to prepare for the upcoming year.

- Higher interest rates are not likely to have a significant impact on US corporations in the near term, as most of their debt doesn't mature until 2026 or later.

- The bond market is showing signs of stabilization, with positive returns expected in the future, making bonds a worthwhile investment.

- The market rally in 2023 has been driven by a handful of stocks known as the "Mag 7," masking weakness in other sectors.

Main Thesis / Background

The purpose of this article is to take some time and reflect on the year we just had. I will discuss some successes, some failures, and how I will be approaching 2024. I find these exercises useful because it allows me to take a broader perspective on where we are (as an investor in the market) and where things may be going from a macro-view - rather than on any specific sector, fund, or stock.

My reflections will often lead to making better investment decisions in the future as long as I understand the why behind why some moves worked well and some did not in any calendar year. While short-term moves can be difficult to reconcile sometimes, a longer range view will often reveal themes that are time-tested. Therefore, my objective here is to highlight some moves I will be making in the coming months and why I believe these will be successful. Hopefully readers will find this informative and useful as they begin to plan ahead for the upcoming new year themselves.

A Year For The Bulls - If You Loved The Mag 7

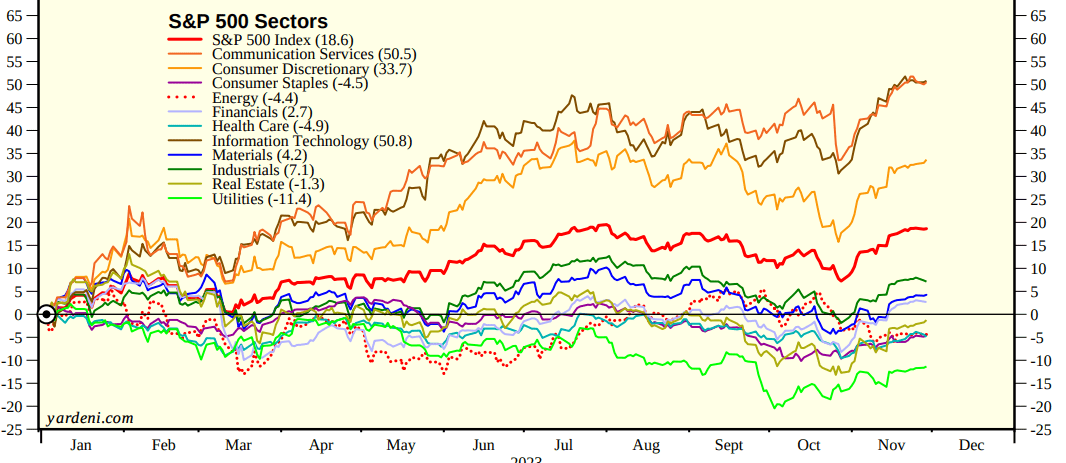

To begin, let us take a look at sector performance for large-cap U.S. stocks. Suffice to say - it has been a great year. After a poor showing in 2022, Technology stocks in particular roared back and many other sectors are heavily in the green as well. The exceptions are Utilities and Real Estate, both of which tend to be inversely correlated with interest rates. So their decline was not much of a surprise given the continuation of Fed rate hikes:

2023 YTD Performance (By Sector, through November) (Standard & Poor's)

{kind=link}

On the surface this looks very healthy. Some sectors have modest losses but the S&P 500 is in bull market territory. Further, many sectors - such as Tech, Communication Services, and Consumer Discretionary are all posting gains in excess of 50% and 33%, respectively. So this looks like a broad, across-the-board rally that investors should be welcoming with open arms.

But there-in lies the problem. On the surface this looks broad, but if we dig in to why these sectors are all out-performing we see that a lot of it has to do with just a handful of names. These stocks, dubbed the "Mag 7", have been leading the market and pulling up a variety of sectors with them. While the majority of stocks in the S&P 500 sit with either modest gains or losses, the Mag 7 is pushing this index in to bull market territory as investors have piled in overwhelmingly to these select companies.

To reiterate, the Mag 7 consists of the following: Alphabet ( GOOG ), Amazon ( AMZN ), Apple ( AAPL ), Meta ( META ), Microsoft ( MSFT ), NVIDIA ( NVDA ) and Tesla ( TSLA ). These have been big winners this year and the implication is they are bringing up the S&P 500 - and a handful of sectors - as a result. This is masking some of the weakness in other corners of the market because their weightings are very high.

But, wait, you say. Aren't these just "Tech" firms? Shouldn't they only be driving the Tech sector higher? If that was the case, then the gains in Communications or Consumer-oriented sectors are the results of strong performances elsewhere, right?

There-in lies the rub. These sectors are not what they used to be. Take Communication Services as a great example. Since I have been investing for about twenty years, this sector to me means the likes of Verizon ( VZ ) and AT&T ( T ) - two stocks that have actually performed very poorly this year:

YTD Performance (Google Finance)

{kind=link}

This begs the question - how can this be? The answer is that these legacy telecom firms do not make up the bulk of this index anymore. With some reshuffling over the past few years, sectors like Communication Services actually are dominated by members of the Mag 7. In fact, two of the largest components of the sector, GOOG and META, represent roughly 50% of the sector’s market capitalization. This explains the correlation between how the Mag 7 performed and this sector. A similar story (albeit with different tickers AMZN and TSLA) emerges when we look at the Consumer Discretionary arena as well.

The point I am trying to emphasize here is that the boon of 2023 is being driven by a handful of names. This isn't inherently "bad" - it depends on one's perspective (and one's holdings!). But it does mean that readers should be mindful of why the market is registering such strong gains - even in different sectors. While it looks like an "everything rally", it is anything but. This could have implications for the new year if the Mag 7 slows down. Will other stocks emerge to lead the charge, or will a broad pullback be the story. It will be interesting to watch which plays out in the months ahead.

**I own the Invesco QQQ ETF ( QQQ ) and the Vanguard S&P 500 ETF ( VOO ) to capture the "Mag 7". I also own the Invesco S&P 500 Equal Weight ETF ( RSP ) to balance out my large-cap US holdings.

US Corporations Can Survive "Higher for Longer" - For A Time

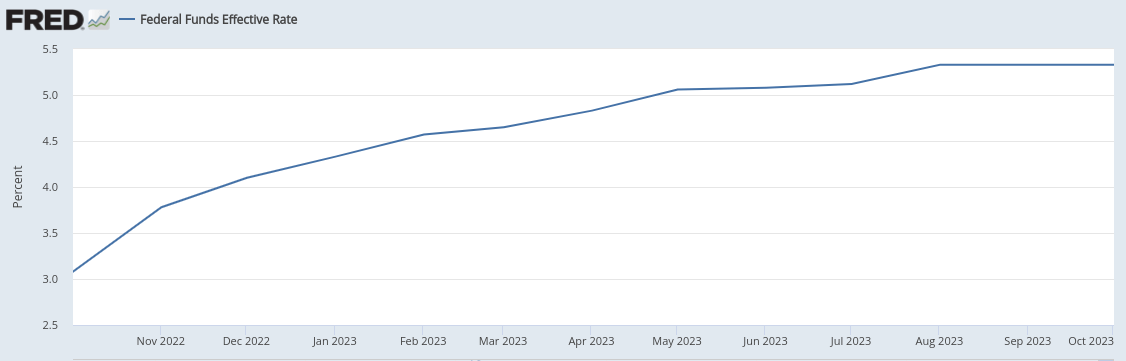

The next topic I want to cover is interest rates. This has certainly been a theme for 2023 as the Fed has embarked on a relatively hawkish path. While the rate was put on-hold at the last meeting , the slope of the curve shows how far we have come:

Fed Funds Rate (St. Louis Fed)

{kind=link}

This has made interest rates (and forward expectations for interest rates) a key talking point for this year and next. So we should consider what this means for any investment strategy in the new year, as I am certain it will remain headline news for the foreseeable future.

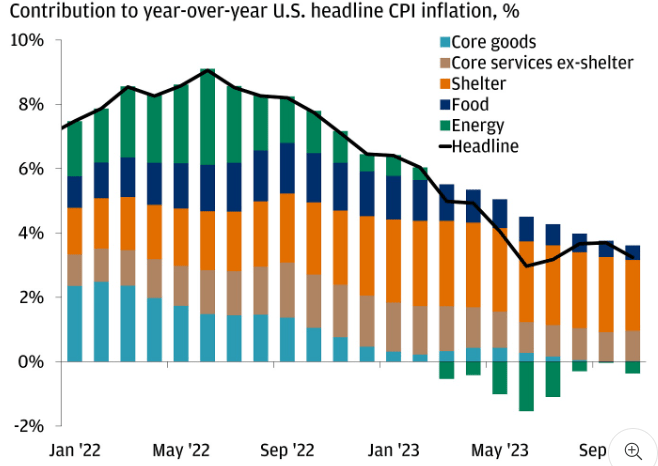

On the one hand, investors are hoping for a decline in rates to be a catalyst for stock gains in 2024. This has some merit, as inflation is finally cooling and the Fed has paused from hiking rates further in the short-term:

CPI (US) (Bureau of Labor Statistics)

{kind=link}

This has been considered "good" for US-based stocks and is part of the reason why the Q4 rally has had some legs. The risk to this bull run in the minds of many is that if inflation does not continue to decline and/or the Fed does not cut rates, then stocks are going to be in for a marked correction next year.

At this point we should acknowledge that forecasts are helpful but not always predictive of the future. I can give my opinion for how I think 2024 will play out, but I could easily be wrong as so many "professionals" have been in 2023 (and in the years before it). Knowing how the S&P 500 is going to perform or where it will finish 2024 is really a fool's errand. Nobody knows for sure, so we have to maintain a balanced and disciplined game plan that we are comfortable riding out if times get tough. That is the most practical advice you are going to get for the long-term.

But we should also acknowledge that after such a big run-up in share prices, the market will likely be ripe for a fall if negative catalysts emerge. If sentiment is sour and the Fed disappoints, downside could be limited. But the bulls are firmly in control at present and this suggests to me that there is plenty of downside potential if rate hikes continue, inflation stays hot, or corporate earnings fall short. This risk-reward dynamic seems to have shifted in this regard given where the major indices sit.

The good news, despite this reality, is that how share prices perform and how large-cap companies are performing is often different. What I mean is, if US corporations are still earning money, managing expenses, and growing their revenues, then short-term fluctuations in the stock market are less of a concern. If the underlying strength is there, I can handle some downturns in my portfolio because I will have confidence that those shares will bounce back.

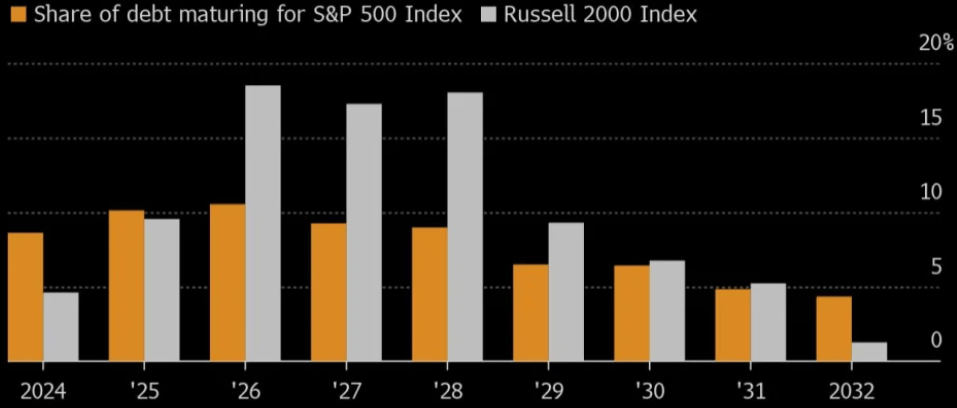

And I do have that confidence now. One reason is that I don't believe higher interest rates are the death blow to earnings power that some seem to think it will be. The reason is that the lion's share of debt maturing for both small-cap and large-cap US companies is a few years out. In fact, a small percentage is maturing next year, with a slight bump in 2025:

Debt Maturity Schedule (US Corporates) (Bloomberg)

{kind=link}

What this is showing is that it won't be until 2026 (and later) that small-cap companies see a spike in maturing debts, and large-caps have a fairly stable path for the foreseeable future. While higher interest rates will certainly hurt net profits - all other things being equal - I don't see the immediate impact as overwhelming.

My conclusion is that the headline risk of higher rates - while important - should not be overblown. While stock prices may overreact to the downside, I see it as just that - an overreaction. Companies here in the US, both big and small, are positioned to keep riding out the storm for the next few years given that a significant share of their debt doesn't mature for a while. This means that investors are wise to flee some of the riskier, junk-rated companies that have debt profiles that are concerning. But the stronger firms that make up the major indices should do just fine.

**I own a stake in the Vanguard Small-Cap Index Fund ETF ( VB ).

Bond Market Is Unlikely To See Another Big Drop

I will now shift over to the bond market. This has been a source of quite a bit of pain and angst among investors this year! After a terrible 2022, bonds continued to take it on the chin in 2023. This challenged the sector's usefulness as a "safe" play or an equity hedge as bonds continued to fall with Fed rate hikes as the main catalyst.

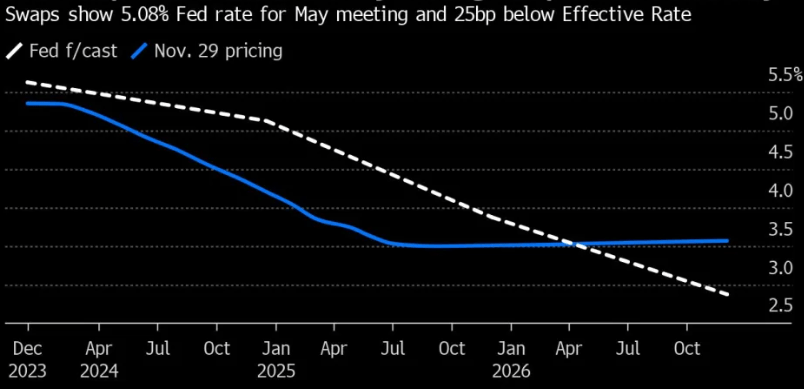

While this story continued for most of the year, the past few months have seen a complete reversal. The Fed pumped the brakes (for now) and the outlook for rate cuts began to dominate investor's minds:

Fed Rate Forecasts (Bloomberg)

{kind=link}

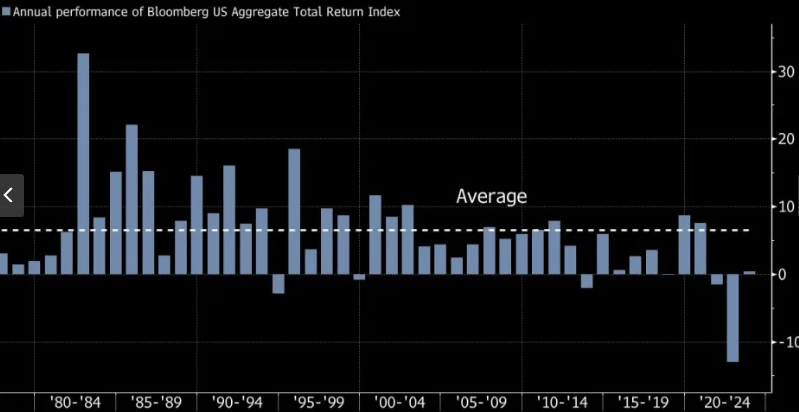

This clearly shows the consensus is for lower rates in the future. The net result has been a surge in bond buying across corporates, munis, and treasuries. It has been enough to push the Agg index (a common bond benchmark) in to positive territory for the calendar year:

Agg Index's Calendar Year Return (Yahoo Finance)

{kind=link}

To me this represents a bit of a return to normalcy in the bond market. While positive returns are never guaranteed, bonds have a history of delivering consistent and moderate gains. Losses do occur, but what we saw in 2022 (and the first half of 2023) are historically unusual and not something to plan on next year.

Could it happen? Sure. But a lot of things "could" happen that won't. I see the recent push higher for bonds across the board as a restoration in confidence in this asset class and I expect that to continue next year. If rates ease off the current levels, then I see returns on the horizon that make holding bonds worthwhile.

**I own the Invesco Taxable Municipal Bond ETF ( BAB ) and the VanEck High Yield Muni Bond ETF ( HYD ).

US Consumer Isn't Out Of The Woods

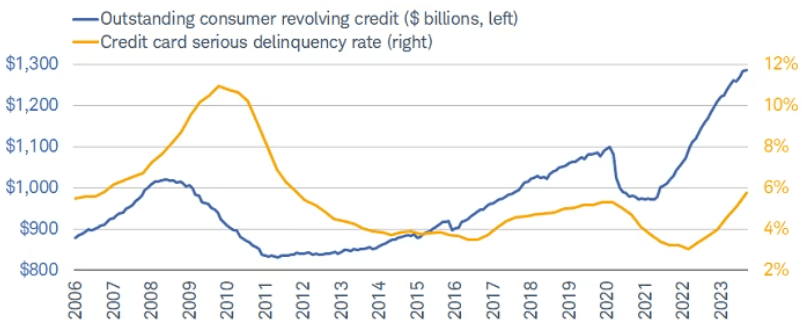

Now for some of the risks. One area that is particularly concerning to me is the consumer backdrop. After a few years of stimulus, hunkering down and building savings, and an uneven job market, American households are starting to feel a pinch that is a bit of a new reality for many. I am referring to the much higher borrowing costs facing consumers (and businesses).

For a while, excess savings and government checks shielded many from the impact. After all, if you have plenty of cash sitting around you either don't have to borrow or can absorb those higher interest rates. Now, with stimulus drying up and American's savings tapped out, the pressure is on. This is leading to cracks in the consumer borrowing market, with revolving credit lines up markedly and credit card delinquency levels also rising off their lows:

Consumer Credit Backdrop (Charles Schwab)

{kind=link}

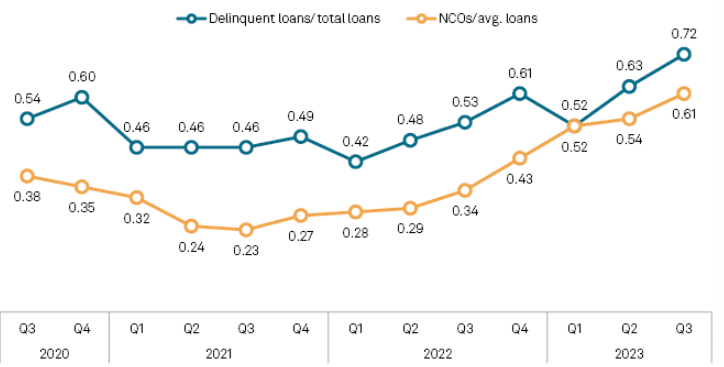

And it isn't just consumer credit cards. Taking a holistic look at borrowing we see that broader delinquencies and charge-offs are also increasing at an almost uninterrupted rate over 2023:

Delinquency Rates and Charge-offs (S&P Global)

{kind=link}

It seems clear to me that the consumer picture is a red flag that investors need to keep a keen eye on. I would personally focus on some of the higher-end brand names that cater to wealthier consumers that aren't reliant on borrowing to make ends meet. This is different that broad consumer plays that are "big box" focused or primarily cater to the masses. Those "masses" are going to have to make tough choices as interest rates pressure their discretionary spend - and that clouds the investment case for many retail names.

The Case For Diversifying Couldn't Be Stronger

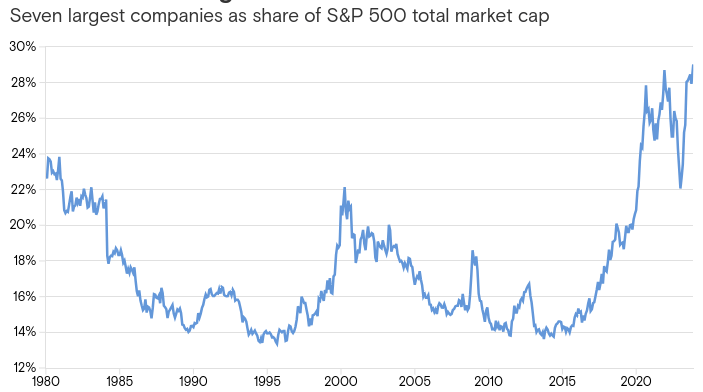

Another point I want to highlight is a trend that started to really accelerate in 2020 and really spiked this year. This is the ever-growing concentration of the largest companies in the make-up of the S&P 500. I alluded to this point earlier when I discussed how the Mag 7 are dominating performance across the market. But the net result of this is what I want to focus on here. This is how these select companies have gotten to be almost 30% of the entire S&P 500 index. This is high in both isolation and compared to history pre-2020:

Mag 7 and the S&P 500 (FactSet)

{kind=link}

In my view this is a bit alarming because it really represents how much concentration risk there is in the market. When I was a young investor starting out, I plowed my entire 401k distributions in to the S&P 500. I used my personal investment portfolio outside of work to pursue other strategies: dividend investing, stock picking, and sector allocations. But I saw the S&P 500 as a smart index for the long-term and had no qualms about continuing to allocate pre-tax money to that index twice a month. I figured the index was large enough that it provided enough diversification on its own.

There is still some truth to that, but the case is getting harder to make. The S&P 500 is beginning to look like a bet on just a handful of companies and that warrants an approach beyond just that large-cap U.S. index. This may sound obvious, but if we look back at prior decades we see that this stark concentration is not really the norm. This means some investors may need to adjust their mindset in this regard because "S&P 500 investing" is not the same as what it used to be.

The action I would recommend from this is to make sure your portfolio is diversified away from these mega stocks. A large-cap US portfolio can be plenty diversified, but not if it is just the S&P 500 that is dominated so heavily by these names. Consider dividend funds, such as dividend "aristocrats", that don't have a large weighting in the S&P 500. Other ideas are REITs, Utilities, and Energy, all of which are under-represented in this index too. There is a plethora of options for those sectors and can balance out a portfolio very well.

**I own the Vanguard Utilities ETF ( VPU ) and the BlackRock Utilities, Infrastructure, and Power Opportunities Trust ( BUI ). I have oil/gas exposure through the Vanguard Energy ETF ( VDE ). I also own Mid-America Apartment Communities, Inc. ( MAA ) as my preferred REIT.

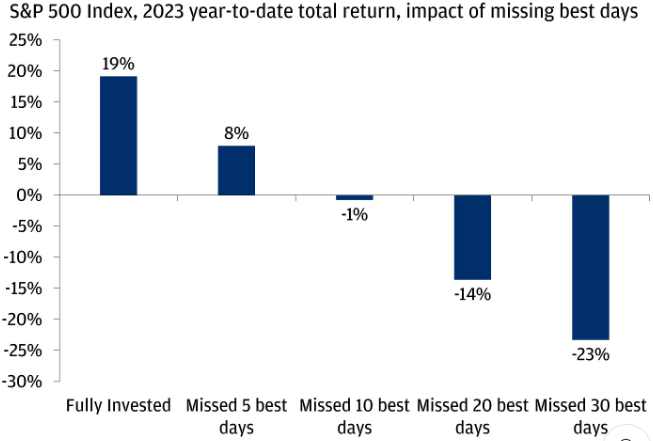

Remember Not To Be Too "Active"

I have used this review to discuss some strategies in the year ahead and I stand by those suggestions. But I do want to caution readers from getting too busy. What I mean is, once you have a strategy, stick to it if you believe in it and nothing has fundamentally changed. Don't trade too much or make massive adjustments due to short-term volatility or headline noise. The market is always going to see ups and downs or ebbs and flows, but the general trend has been up over time. Staying invested is key - whether it is through the S&P 500, foreign stocks, bonds, or any other sector/stock I discussed here.

To emphasize this strategy, let us look at how being too creative and/or staying out of the market can impact total return. While 2023 has been a great year for US equities (so far), there has been plenty of volatility and down days. If one had rotated out of the market too much, or simply timed their buys and sell poorly, the net result could be in stark contrast to what someone would have earned if they had just stayed invested the whole year:

YTD Returns (S&P 500) (JPMorgan Chase)

{kind=link}

The takeaway for me is that sometimes retail investors can be too smart for their own good. It does make sense to monitor valuations and concentration risk, I would never suggest otherwise. But don't get too passive or lose focus when making these adjustments because, as the graphic above shows, there is plenty of risk to being out of the market.

Bottom-line

My year-end review this time around has a more upbeat tone than it did last year. Plenty of that has to do with performance. While stocks and bonds took a beating in 2022, the net result through November 2023 has been one of increased wealth and satisfaction!

For me, the big themes of this year is that bonds are finally starting to turn the corner, the equity market (as measured by the S&P 500) is getting increasingly concentrated, and geo-political events (i.e. Russia/Ukraine and Israel/Hamas) are largely being ignored. This means investors should take the time to readjust their portfolios to make sure they are too exposed to just a handful of mega-cap stocks, have their hedges in place, and are prepared for some inevitable flare-ups in early 2024. But if the past few years has taught us anything, America and the American economy are resilient, so I head into the new year full of optimism. I hope all my followers are able to feel the same.

For further details see:

Another Year In Review, With Some Thoughts For 2024