AON - Aon plc: The Company Remains A 'Hold' In The Face Of Valuation

2023-10-23 21:21:14 ET

Summary

- Aon plc remains overvalued compared to other companies in its segment despite its high-level business ideas and focus on helping companies improve decision-making.

- Aon has consistently grown its results and maintained high operating and net margins, making it one of the more profitable businesses in the segment.

- The company's performance in 2Q23 was impressive, with organic top-line growth, increased operating margin, and effective capital management leading to a 5% increase in EPS.

- The company's current valuation dictates that the business is a "HOLD" here, however.

Dear readers/followers,

Aon plc ( Aon) is a company that remains, despite the recent underperformance since about June when I posted my last article, interesting. This article can be found here. The problem is that based on the current situation we're in, we're looking at a company that remains overvalued by most metrics to other companies in the segment.

I like companies with high-level business ideas - and Aon certainly is that. Its focus on helping other companies improve their decision-making process is a good one. I categorize it to other insurance/business services businesses due to the company's Reinsurance and risk solutions business, which comprises large portions of the company's end markets and customers.

With 50,000 employees across the globe and 120+ countries with clients found in Aon, the company is one of the biggest at what they do.

All in all, there are many arguments as to why this company should be on your list - it's just that it falls short in some others.

Aon - Tricky despite an 8% drop since my last piece

Aon is certainly safe, and it's also one of the more profitable businesses at what it does, on a comparative basis. What do I mean by this?

I mean that a 28.6% operating and 20.7% net margin is one of the best in the entire segment. The company is in the 90th percentile in both of these comparisons. This is likely one of the reasons why the company has not underperformed during a time when many other financial and insurance-related businesses have been not only performing negatively but well worse than the market average.

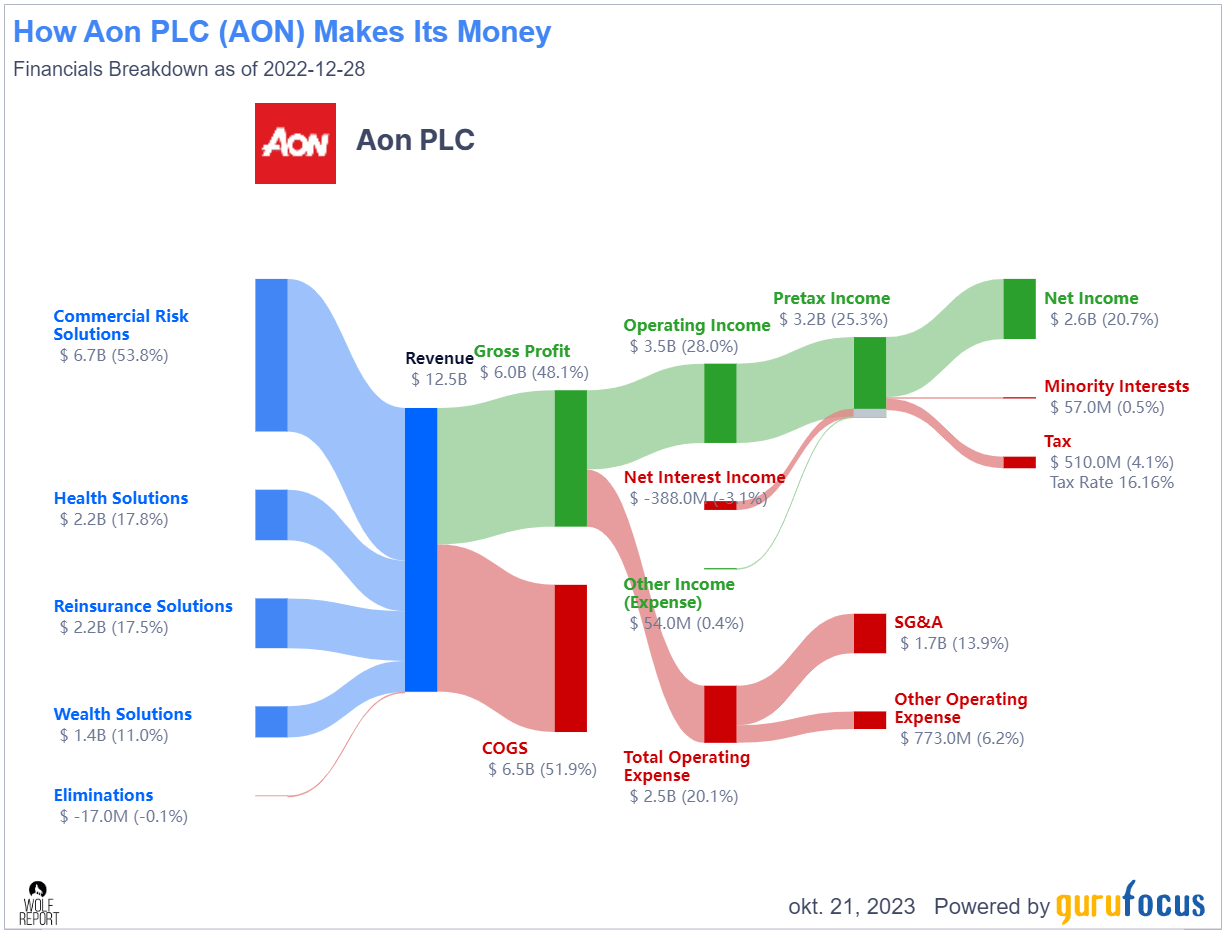

The way this business model looks is very impressive - but don't take my word for it, check this out for the 2022 results.

Aon plc Business model (GuruFocus)

{kind=link}

This also isn't a fluke. The company has been growing its results for years and has been on an almost-constantly growing results basis since the 2015 fiscal. The company has also held a positive ROIC since 2016.

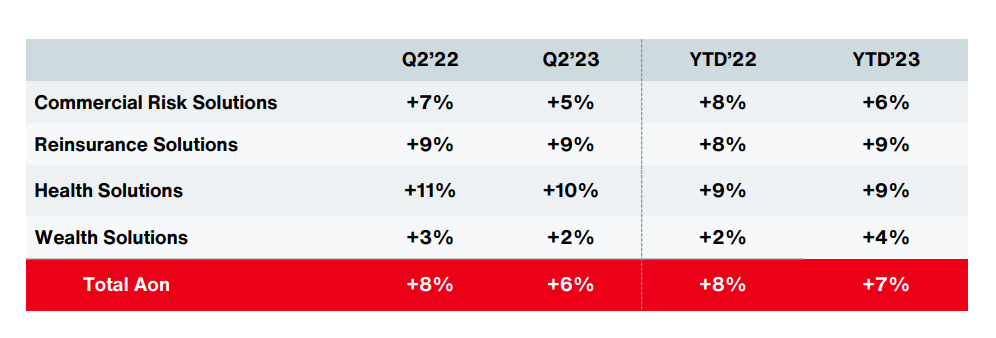

The latest set of results we have are the 2Q23. The main thing that I want to look at when it comes to Aon is whether the company's margins in any way are worsening. Top-line growth can occur in many companies here, but margin retaining and similar trends are rare. Good news there, because the 2Q23 margins remain firmly above 26% when we look at the operating margin.

The company's Commercial Risk solutions segment remains the largest for the company in terms of bound premiums, at over $110B - more than Reinsurance and Health together, while the Wealth solutions go by AUM instead of premiums, with currently $3.8T of assets under company management.

The company's performance during 2Q23 was actually good. Top-line results continued to grow organically due to strong business retention as well as new business coming to the company. Operating margin was up 110 bps, far from going down, only slightly offset by increased expenses and investment costs. EPS was up 5% due to effective capital management and effects from revenue growth. All in all, these results are impressive.

Where are we going from here?

Aon is targeting continued revenue growth on an organic basis of 4%+ per year. This expectation is based on continued expansion in faster-client growing areas, data-driven solutions, and expansion due to TAM increases. I view Aon's operating margin as sustainable for the long term, and I believe this has been proven based on operating margin improvements since 2010 of 11,20%, or 1,120 bps, which averages out to just around 90 bps per year. This growth has come from top-line growth, higher margin business focus, and increased operating leverage.

In short, Aon knows very well what it is doing, and improvements are not yet finished - as we can see from improvements this year alone during 2Q23.

Aon is unfortunately not a high dividend payor. The company has a very disciplined history of capital management and allocation. Instead, money is used to grow. Aon has finished 164 M&As over the past 12 years , as well as divesting 141 business units/segments. This implies just how laser-focused the company has been in improving its operations and streamlining things.

All of the company's capital decisions over the past decade seem to have an ROIC focus - in that ROIC stabilization or improvement is the goal here. Share repurchases, rather than dividends, are something that you need to be okay with here - that's how the company rewards its shareholders rather than dividends. That's because company dividends here are less than a 0.8% yield, which is one of the lowest yields I am currently considering. It's well below any sort of money market fund or solid dividend-paying stock and means that everything here (with the exception of 0.8%) is based on forward capital appreciation.

I would characterize the company as continuing to grow. Buybacks are expected to continue as well, thanks to continuing increases in FCF. Given that the company is performing like this, in one of the worst environments you can work in, things are likely to improve even more when the macro starts turning around.

{kind=link}

The company is working in accordance with its Aon united strategy, which includes standardizing operations and the company's operating platforms even further.

Things to keep an eye on going forward is

the company's globalized and international structure. In many ways, this makes the company more diversified and safer, but it's also in some ways what makes the company go up and down a bit. However, the international growth/decline patterns are really one of the few current risks I see for the company. In the last quarter, the company also saw a slight decline in deal volumes. Despite the positive results for 2Q23, the company is seeing this quarter as a bit of a downturn, where pressure is expected for 3Q23 as well, with continued soft outlooks in terms of demand.

This is also likely the reason why the company is down over 8% since my last article.

One of the key segments where the company is growing, and where the company has been growing since it started in the field back 7 years ago, is the IP business. This segment is likely to continue growing.

We love this business. It is a phenomenal opportunity for us. If you think about intellectual property overall, this is just hugely significant. This is representative -- we talked before, 85% of the value of the S&P 500, which really tied back to intangible assets. And if you go back to 2016, we started with an amazing investment, bringing in 601West to Aon, it's 20, 25 colleagues. We've now invested in hundreds of colleagues with a truly unique market-leading platform to really help understand this opportunity and these risks and the value of these assets.

(Source: Aon plc 2Q23 earnings call )

This is despite the fact that when looking at revenues for this particular segment, this market is very much still in its infancy. The role here shouldn't be overstated yet, but given the trends since the company started in the field, I expect Aon to grow it as they have been growing other parts of its business.

Let's now look at the valuation and why, unfortunately, I don't see the company as a compelling buy here.

Aon plc - The company's valuation is prohibitive in this market

In my last article, I gave the company and retained my original price target of $250/share. I still remain uninterested in investing in the company above a $300/share price, and despite trading lower now, Aon is still trading at almost $315/share as of the time of writing here. This is not good enough for me.

Why is this the case?

Because at this valuation, even estimating the company at its 5-year average of 21.6x, that upside is barely 10% per year. And I do not invest at 10% annualized upside, especially not when that upside is based on a significant premium which the company has been below several times in the last year.

If the company were to slightly underperform here, the RoR would quickly go below 8%, which given the company's very limited yield makes any of the currently available debt investments at 7-9% a better choice in my book - those prefs or high-yielding energy companies at least trade at a significantly lower multiple than 20x+ as we're seeing here.

The analyst averages here is an interesting story. You would expect analysts to be relatively positive, and indeed they are. The current analysts following the company estimate Aon at a range of $291/share on the low side and $362 on the high side, with an overall average of $339/share. Despite this, only one analyst has a "BUY" rating on the company. 17 are either at a "HOLD" or an "underperform" rating, despite almost every analyst being above the current company's trading level of $314.12.

If the company is such an amazing deal at this level, which clearly some of the analysts believe given their PT of $360+, then their ratings should reflect this, but it does not. My own rating of around $250/share is actually where I would start adding the company's shares despite the overall low yield of sub-1% even at that share price.

So, for now, my PT continues to reflect my rating on the business. I say that Aon does not deserve anything except a "HOLD" here.

Here is my thesis for the company as it stands today.

Thesis

- Aon plc is a superb, fundamental company in financial services insurance, and risk brokering. It's one of the leaders in its field and deserves your attention at the right price. That price is around $250/share, as I see it.

- The company has grown more since my last article and now trades at over $330/share.

- A mix of near-term challenges related to macro, inflation, and premium headwinds calls into question how high an upside on a 3-year basis the company actually has, despite recent growth.

- Aon plc is a "HOLD" to me for the time being - even with the bullishness we see from results and management. It's above what I would want to pay for a company like this.

- This thesis has been updated for the 2Q23, and I continue to view the company as too expensive.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansions/reversions.

The company does not fulfill my valuation criteria - and therefore it warrants no more than a "HOLD".

For further details see:

Aon plc: The Company Remains A 'Hold' In The Face Of Valuation