AON - Aon plc: Too Expensive Despite Financial Outperformance

2023-06-30 04:50:00 ET

Summary

- Aon plc is a company I wrote about a few months back. I went neutral/'Hold' on the company due to valuation-related challenges above a share price of $300/share.

- While the company has performed well, I still hold my stance that this company is too expensive for the meager yield and the questionable upside it offers.

- I remain at 'Hold' - and here is why. There are better alternatives in the sector out there.

Dear readers/followers,

AON plc ( AON ) was a company I wrote about a few months back, going in with a "HOLD" rating, which was not uncommon at the time, and still isn't uncommon for the business and the analysts that follow it. In this article, I'll showcase the underperformance we're able to see from the company at this time - at least relative to the index, and I'll showcase why I believe there to be better investments at this time, despite the company's quality and stability.

Seeking Alpha AON RoR (Seeking Alpha)

Let's look at what this company can offer us here. My latest article was back in December of 2022, so it's been some time since I've revisited the business - we have 1Q23 results, and estimates for the 2023E.

AON plc - Upside exists at a valuation we currently do not have

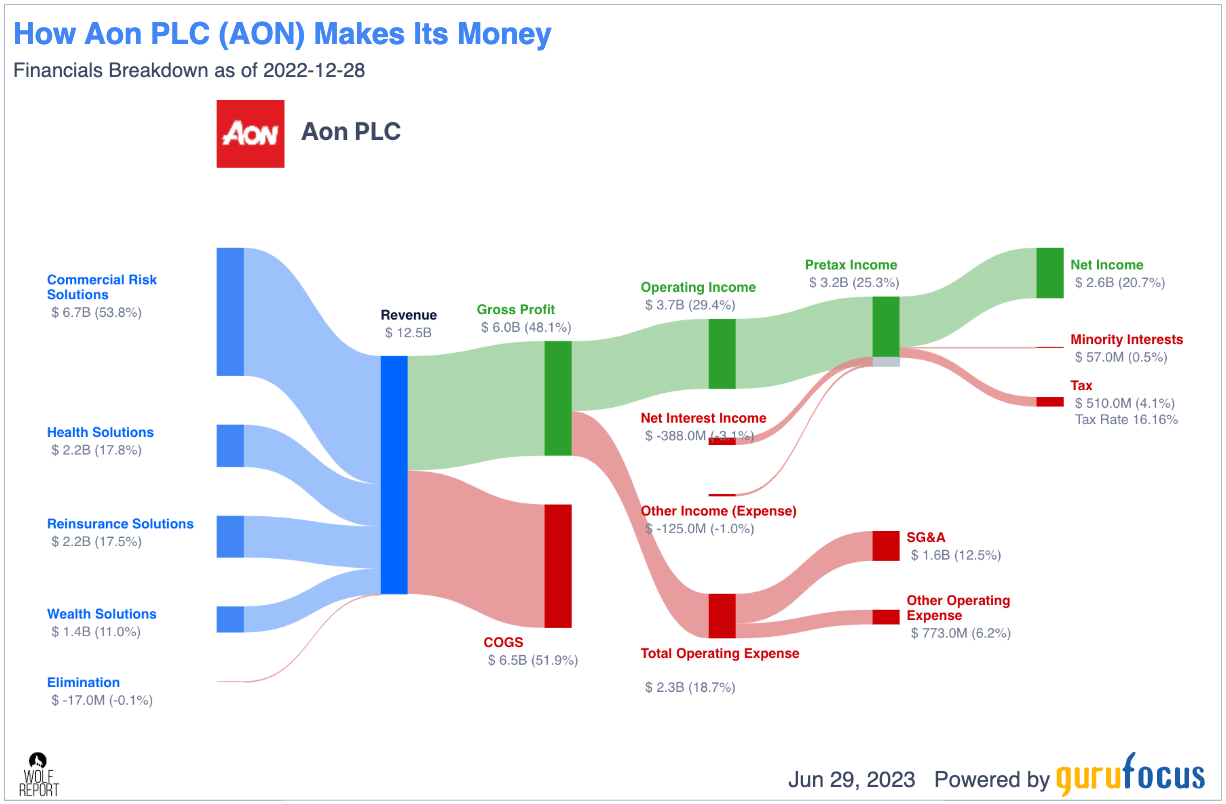

The company is an interesting business - because it works to help other companies make better decisions. They do this in 4 segments, each key to specific markets, including Reinsurance solutions, Health Solutions, Commercial Risk solutions, and Wealth solutions. With 50,000 employees across the globe and 120+ countries with clients found in AON, the company is one of the biggest at what they do.

Not only that, AON is very good at what they do.

I justify this by looking at the company's profitability in terms of the broader sector. We find Gross margins of 48%, operating margins of nearly 30% and net margins of over 20%. Very few companies manage 20%+ margins on the net side of things, and that's before going into some of the best return-related metrics, such as RoE, ROA, ROIC, and ROCE, that exist in the sector (Source: GuruFocus).

Despite not being a strictly-oriented insurance business, the company is most often compared to insurance businesses. That means that the comps of which I speak when I talk about AON outperforming the sector, include great businesses like Marsh & McLennan ( MMC ), Arthur Gallagher & Co ( AJG ), Willis Towers Watson PLC, Brown & Brown ( BRO ), others. Not traditional line/multi-line insurers, but more companies that are brokers or do higher-level consulting.

The company's core business and areas are focused on Risk, reinsurance, health, and wealth solutions, where it does retail brokering, specialty solutions, reinsurance, capital markets, consulting, and brokerage for health, retirement, pensions, and investments.

Like most such companies, the income is in turn a result of a mix of commissions, comp from collaborators, and customer fees. Attractive incomes do vary over time and with the overall macro, but not as macro-sensitive as some other areas.

The closest comparable peer is MMC - it's no stranger to me, this segment, and it's an attractive one. But if bought at the "wrong" value, it can stagnate for years.

For instance, if you had bought mid-late summer of 2021, your current RoR on an annual basis for the company is around 3% including dividends, and around 2% without. In the same timeframe, my own portfolio is up more than 15x. So holding onto expensive stocks can cost you money - and AON plc is one of those companies.

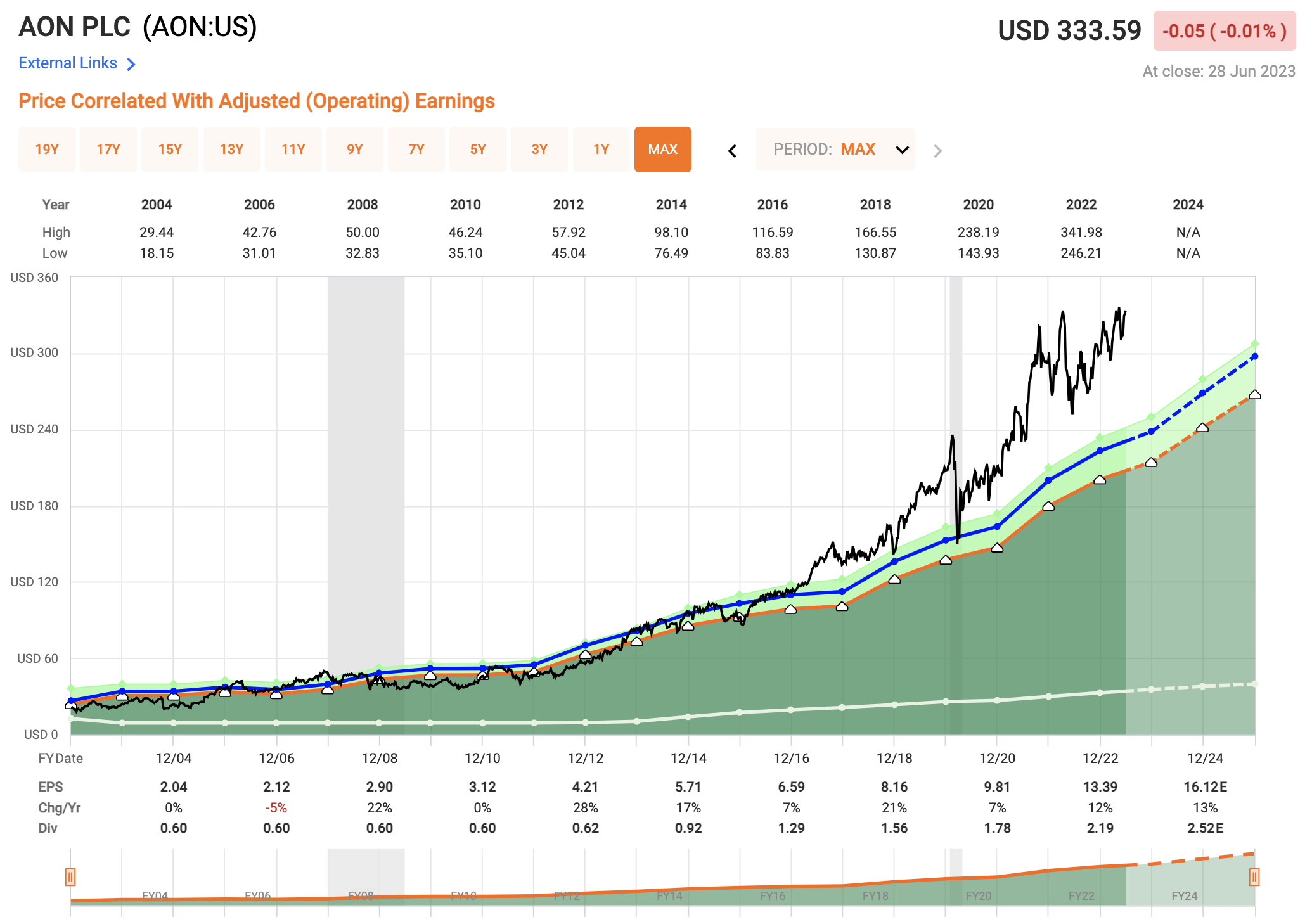

F.A.S.T graphs AON (F.A.S.T Graphs)

{kind=link}

AON is likely to continue to grow. As I said, the company has one of the best profitability in the entire industry. Its ROIC is close to sector-leading.

{kind=link}

Quality warrants premiumization - I don't have an inherent issue with this, but when that premium grows as I see it, beyond what I would consider rational, then the question becomes how much more can be expected.

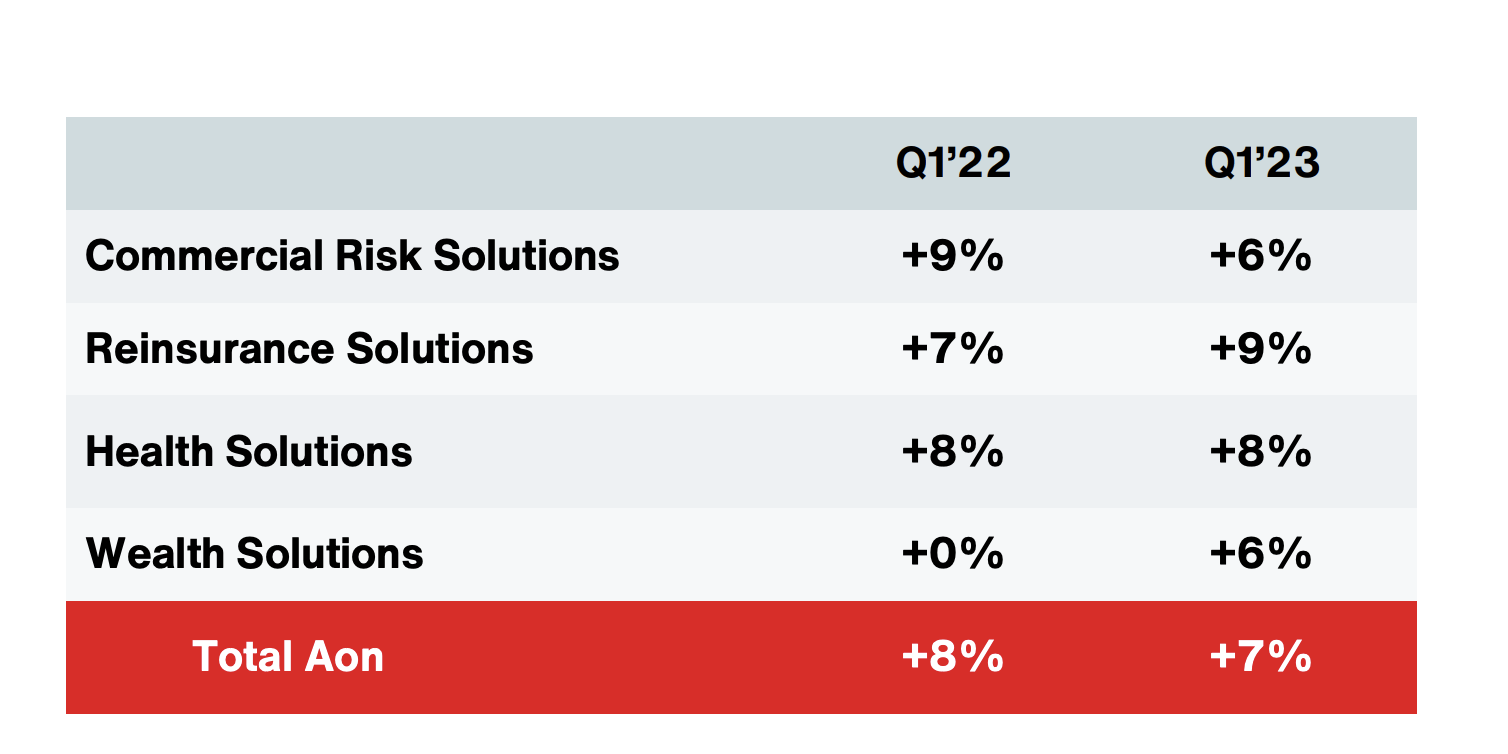

The latest quarterly results are nonetheless good and indicative of continued growth. We can clearly see things like continued revenue growth, well over 35% in company-wide operating margin, and almost half a billion dollars in quarterly cash flow from operations. The revue growth was 7% organic, driven by both strong retention of existing customers, as well as new overall generation of business. The company managed margin expansion despite ongoing inflation and cost pressures - and not a rounding error either, but a 70 bps margin improvement. Adjusted EPS growth came in at 7%, due to that organic growth and strong overall capital management on part of the company.

The company's forward target is managing mid-single digit or above in terms of organic revenue growth over the long term, while sustaining the current solid operating margin expansion, as well as ongoing FCF growth over the longer term.

AON is also not expecting a negative 2023E. The company expects to deliver its long-term mid-single-digit revenue growth, and expects to deliver operating margin expansion for the full year. As with any international company though, the primary risk to AON that I can clearly see is the foreign FX impact due to the relative strength of the dollar and other currencies like it in relation to currencies like the SEK or other, smaller currencies which are currently not doing well.

{kind=link}

As you can see, organic growth was present in all business lines - and the reasons are the same for most of the segments, and can be translated into that the company simply knows well what it is doing.

It's been a long time since the company has not or failed to deliver organic revenue growth - since 2016, as a matter of fact. Since then, the company has delivered on average 4-6% organic revenue growth every year.

The company has a number of market-leading or close-to-market-leading positions in relevant industries. Among other things, AON is the #1 issuer of insurance-linked securities in its reinsurance solutions segment, where it helps businesses, governments, and communities to navigate these uncertain times.

Its Wealth Solutions arm has over $4T of pension liabilities valued, with over $3.8T of assets under advisement (not AUM). The company also supports 3M retirement participants.

Things to keep an eye on going forward is the company's globalized and international structure. In many ways, this makes the company more diversified and safer, but it's also in some ways what makes the company go up and down a bit. But the international growth/decline patterns is really the sole risk I see for the company. Beyond that, the company's own guidance and analyst guidance is telling us that AON is set to expand revenue and earnings further going forward. Management characterizes the environment, at this time, as "foundationally very strong". The company is looking at M&A possibilities to deliver more tack-on growth. Margin expansion is the company's calling card here - and that is set to continue.

So what we would say is we grow margins each and every year. And our margin expansion for the last 12 years has been 1,120 basis points or approximately 90 basis points a year. And that 90 basis points a year over the last 12 years has been a gross margin expansion higher than that, and then it nets to 90 basis points, net of the investments we're making in long-term growth. So that is consistent with the way we drive margins each and every year.

(Source: Christa Davies, 1Q23 Earnings Call )

With that, I consider risks to AON to be very few - and the potential for the company to continue to grow is very good. That does not, however, take away from the fact that the company is currently quite expensive.

Let me clarify.

AON plc Valuation - Expensive, despite good growth prospects

The only part that AON doesn't fulfill is the valuation and price portion of my investment criteria - everything else is either "fine", or more than fine. That Aon deserves some kind of premium, there is no doubt or argument about. The company is too good to trade at a simple 14-15x P/E, too big, and too much of a moat in a global market.

However, the company is an A-rated insurance broker (technically) with a less than 0.75% dividend yield in a high-inflation environment trading at an average P/E of 24-25x, depending on where you forecast it. In an environment where it is easy to find single-digit P/E valued A-rated insurance companies with over 6% yield, that's a tough pill to swallow, as I see it - and I'm fairly certain that I do not want to invest in it until it drops below 20x P/E. It was about a year back since we last saw such a valuation.

Thanks to the company's very limited yield, a forecast here even with a double-digit EPS growth rate comes to no more than a 6-7% annualized RoR at a 21-22x P/E on a forward basis. The simple fact is that I do not consider that good enough - I want 8-9% at least, and I certainly want the possibility of reversal, which we do not have in this business at this valuation.

Other analysts mostly agree with my cautious stance here. 17 S&P Global analysts forecast AON, and their average from $275 on the low side to $360/share on the high side comes to an average PT of $331/share, with a total upside therefore of negative 0.5% based on the current share price. Out of those 17 analysts, only one has the company at a "BUY". We have 4 underperform or "SELL" and 15 analysts at "HOLD". The street sentiment for AON is very clear here.

Even if the company were to outperform even more, I do not view this as reason enough for the company to trade even higher here. Because there is such a very limited upside here based on the sector and valuation, I find it very hard to give any bullish thesis any credence for this company.

Take an EPS without NRI DCF-based example. You could forecast this company with a 10% discount rate with a 10-year long 11% per year growth rate, going to 5% in the terminal period, and you'd still not get higher than a $230/share fair value. That's a negative 44% margin of safety at a stock price of over $333/share. In order for things to go positive here you'd have to go for a DCF with a 15% growth rate in the growth stage, and 9% in the terminal stage, again with a 10% discount rate. That gives you a fair value that gives a 2.71% margin of safety at today's valuation.

I neither view this as likely nor as a scenario that I want to forecast - and for that reason, I remain at my current thesis for AON, which is as follows.

Thesis

- AON plc is a superb, fundamental company in financial services and insurance, and risk brokering. It's one of the leaders in its field and deserves your attention at the right price. That price is around $250/share, as I see it.

- The company has grown more since my last article and now trades at over $330/share.

- A mix of near-term challenges related to macro, inflation, and premium headwinds calls into question how high an upside on a 3-year basis the company actually has, despite recent growth.

- AON plc is a "HOLD" to me for the time being - even with the bullishness we see from results and management. It's above what I would want to pay for a company like this.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company does not fulfill my valuation criteria - and therefore it warrants no more than a "HOLD".

For further details see:

Aon plc: Too Expensive Despite Financial Outperformance