AON - Aon: United Business Model Supports Double-Digit Earnings Growth

2023-08-11 14:18:36 ET

Summary

- Aon is a well-managed company with mid-single-digit organic revenue and double-digit EPS growth, supported by share repurchases.

- Aon's United business model has driven sustainable growth and expansion into higher-growth areas like climate, intellectual property and cyber security.

- Aon's robust capital allocation policy, including substantial share buybacks, has resulted in decreased outstanding shares and strong EPS growth.

Editor's note: Seeking Alpha is proud to welcome Lighting Rock Research as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

I believe Aon ( AON ) is a highly recurring and well-managed company, with mid-single-digit organic revenue growth and double-digit EPS growth, accompanied by substantial share repurchases. Aon's United business model has proven to be effective and has delivered sustainable growth. Additionally, Aon is entering higher growth areas such as climate, intellectual property, and cybersecurity, which could potentially accelerate their organic revenue growth and margin expansion. I have owned Aon for a long time, and I am quite bullish about their future growth.

Business Overview

Aon serves as a corporate risk management and health and wealth solutions provider. Aon encompasses four main business lines:

Commercial Risk Solutions (54% of revenue) : Aon offers risk consulting and retail brokerage services to corporate customers. They earn both insurance commissions and professional service fees.

Reinsurance Solutions (18% of revenue) : This includes treaty and facultative insurance services for insurance companies. Aon is servicing insurance companies.

Health Solutions (17% of revenue) : Human capital and employee benefit services, akin to the Commercial Risk Solutions business, generating insurance commissions and service fees.

Wealth Solutions (11% of revenue) : Aon provides retirement consulting and pension administration, offering a highly recurring and reliable revenue stream.

All four businesses are predominantly recurring and non-discretionary. Aon boasts an impressive average retention rate of 95% across its product portfolios. Even during the challenging year of 2009, Aon experienced only a marginal 1% decline in organic revenue.

The management team aims for a 5% organic revenue growth in the long term and foresees moderate margin expansion driven by operational efficiency and the introduction of new services. Furthermore, Aon expects double-digit growth in free cash flow over the long run.

Investment Thesis

Well-Managed Aon United Business Model

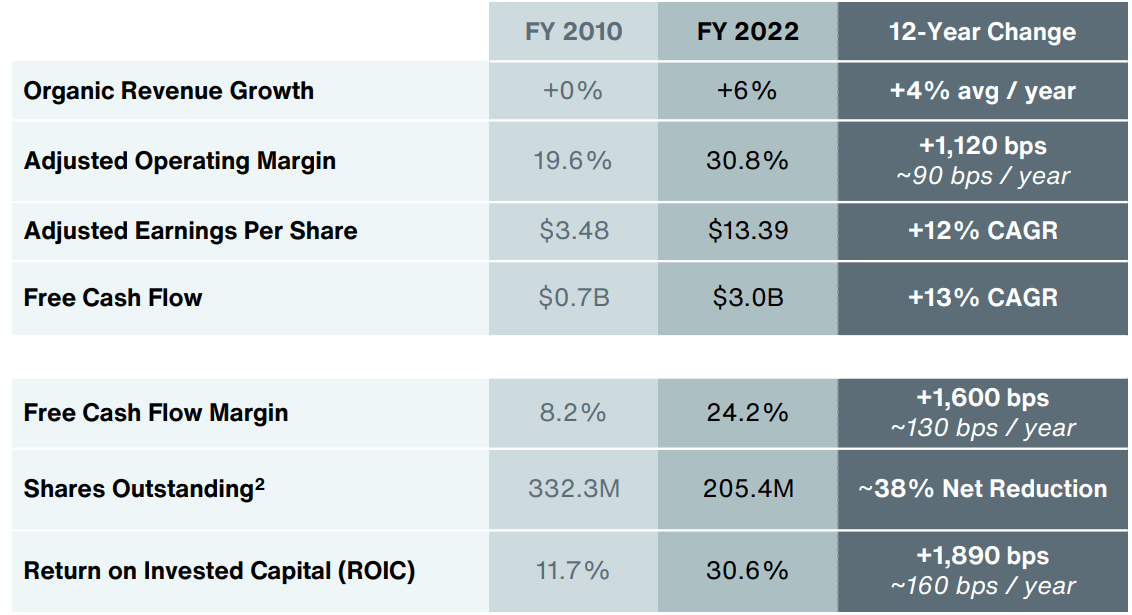

Aon has coined its business model as Aon United, emphasizing standardized operating policies and disciplined prioritization. This approach has made Aon more efficient, fostered innovation, and facilitated informed business decisions. Consequently, Aon has achieved remarkable financial results since 2010, witnessing accelerated growth in both top-line and bottom-line performance. Their free cash flow exhibited an impressive compound annual growth rate of 13% from FY10 to FY22.

Aon Investor Presentation in June 2023

{kind=link}

High Recurring Business Model

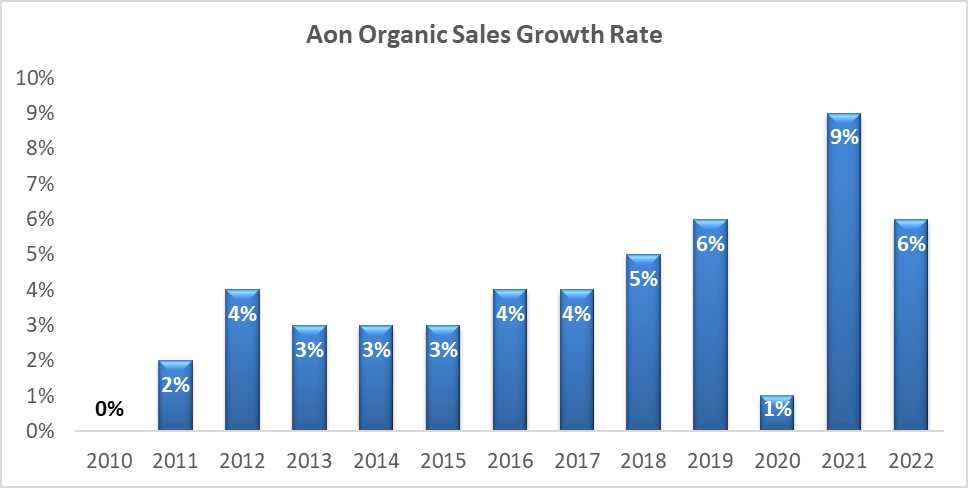

As depicted in the chart below, Aon has consistently maintained positive organic sales growth since 2010, attributed to their highly recurring business models.

Aon 10Ks, Author's Calculation

{kind=link}

I think the resilient business is straightforward to comprehend. For instance, within their Health Solutions business, Aon assists corporate clients in managing employee health benefit programs. Transitioning from one service provider to another would likely involve significant migration costs for corporations. Furthermore, many of the services Aon provides are obligatory for corporations, given the requirement to procure various insurance products to mitigate business-related risks.

Robust Capital Allocation Policy

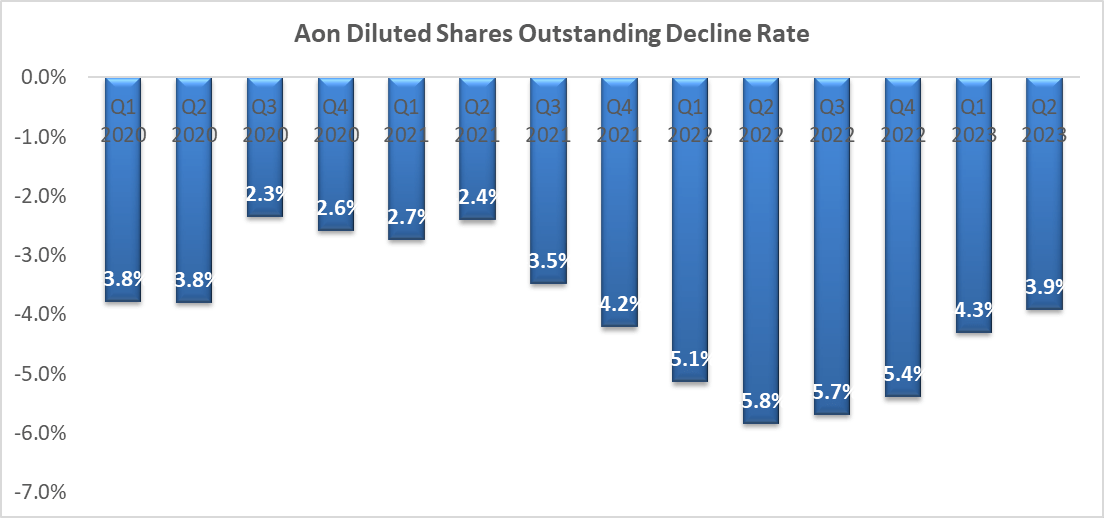

I admire Aon's capital allocation policy. Over the past five years, Aon generated $10.7 billion in free cash flow, distributing $2.1 billion in dividends and repurchasing nearly $12 billion worth of their own shares. Naturally, this required taking on some debts to fund the substantial share buybacks. As a result of these significant repurchases, Aon's outstanding shares have consistently decreased quarter after quarter.

{kind=link}

Major Market Misconceptions

One significant misconception prevalent in the market is viewing Aon solely as an insurance company. However, Aon is distinct from traditional insurance companies since it does not bear insurance underwriting risks. Moreover, Aon derives revenue from both insurance commissions and professional services. I think a comparison of forward P/E ratios between Aon and some insurance companies can be misleading, as comparing multiples across companies, especially those in diverse industries, is not a direct comparison.

Seeking Alpha Data - Author's Calculation

I believe it is invalid to assume that Aon should be traded at the same multiple as other insurance companies, as this could potentially underestimate Aon's fair value. Based on my analysis, Aon's business model doesn't solely revolve around generating insurance commissions; rather, they provide comprehensive risk consulting services to enterprises. I believe their primary value proposition stems from their profound expertise in risk management and mitigation.

Key Investment Risks

On the whole, I perceive Aon to be relatively free from substantial risks in their business operations. Nevertheless, investors should monitor a few key factors.

Firstly, concerns persist regarding Aon's operating margin. Aon has elevated its operating margin from 19.6% in FY10 to 30.8% in FY22. The upper limit of margin expansion remains uncertain. I believe that if Aon sustains mid-single-digit organic sales growth and continues product innovation, they can continue margin expansion. The growth rate of operating expenses need not mirror revenue growth. Moreover, Aon's foray into climate, intellectual property, cybersecurity, and workforce resilience businesses could contribute to margin expansion due to the higher pricing associated with these services.

Secondly, Aon has a history of pursuing significant M&A transactions. While Aon announced plans in March 2020 to merge with Willis Towers Watson (WLTW) and create the largest insurance broker, this $30 billion merger was ultimately abandoned due to government intervention. Such large transactions could potentially erode shareholder value if integration proves challenging.

Lastly, Aon's earnings might be affected by insurance underwriting cycles . Although Aon is not an insurance company and is not exposed to insurance underwriting risks, I believe that a portion of their earnings ((specifically insurance commissions)) could be linked to the overall underwriting cycles of the insurance market.

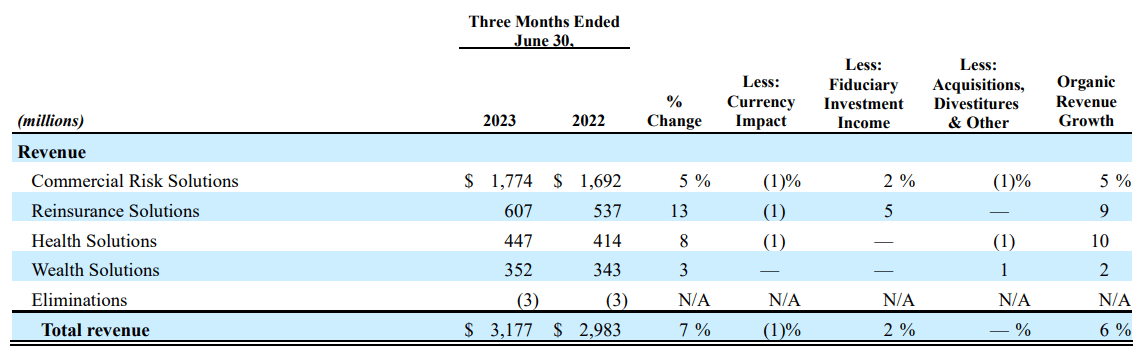

Q2 FY23 Earnings Review

In Q2 FY23 , Aon achieved 6% organic sales growth and a 110 basis point margin expansion. They repurchased 1.7 million class A ordinary shares during the quarter, leading to a 3.9% reduction in outstanding shares year over year. During the earnings call, Aon's management indicated that they consider their stock price significantly undervalued at its current level.

{kind=link}

In Q2 FY23, Aon issued the following guidance

- Organic Sales growth : mid-single-digit in FY23

- Operating Margin : expect to expand in FY23

- FCF : double-digit growth in FY23

- Capex : moderate in 2H, and project $220 million to $250 million in FY23

I think it was a quite normal quarter for Aon. As the company disclosed in their earnings call, cash from operations was flat year over year, and FCF dropped by 7%, primarily driven by increased capital expenditures. Aon expects their capex to moderate in the second half of FY23. Regarding the balance sheet, Aon's management team indicated that they will add incremental debt as EBITDA grows over time while maintaining the investment credit profile. Given that Aon is repurchasing their shares, I believe it makes sense to add some debt to finance the share repurchase. As they disclosed, their long-term debt is all fixed-rate with an average of 4% and an approximate maturity term of 11 years. Therefore, I consider their balance sheet quite solid, and the debt appears to be entirely manageable.

Aon - DCF Valuation

My DCF valuation model relies on the following assumptions:

Normalized Organic Sales Growth : 5%. Aon's guidance indicates mid-single-digit organic revenue growth in the long run.

Margin Expansion : Annual expansion of 10 to 20 basis points. Aon seeks to increase margins over time, primarily through operational leverage and higher pricing for new products.

Capex : I expect $226 million in FY23, closely aligned with their guidance. Aon is a capital light business, and their capex is representing less than 2% of total sales.

M&A : I assume a 1% growth in sales from acquisitions, given Aon's history of incorporating tuck-in acquisitions to expand its product offerings.

Tax Rate : 18%. This represents the average tax rate over the past five years.

WACC

Beta: 0.83. Data Source: Seeking Alpha’s 24-month beta.

Risk-Free Rate of Return: 4%. I am using 10-year US government bond yield .

Expected Market Return Premium: 7%. I am using the same assumption across my models.

Cost of debt: 10%. I am using the same assumption across my models.

With these inputs, WACC is calculated at 8.4% in my model.

The table below provides a summary of my DCF analysis.

{kind=link}

According to my model, free cash flow margin is anticipated to expand to 28.5% in FY32, accompanied by double-digit growth in EPS. After discounting all firm free cash flows to present value, my estimate places Aon's enterprise value at $89.5 billion, with equity value at $80 billion. This implies a fair value of $392 per share according to my estimations.

Conclusion

Aon's business strategy remains steady and consistent. Any company showcasing mid-single-digit organic revenue growth and double-digit EPS growth, while maintaining a lack of structural risks, holds strong appeal to me. Aon has been a longstanding component of my investment portfolio, and I wholeheartedly recommend a "Strong Buy" rating for Aon.

For further details see:

Aon: United Business Model Supports Double-Digit Earnings Growth