REIT - Apartment REITs: Rents Are Rising Again

2023-06-15 10:00:00 ET

Summary

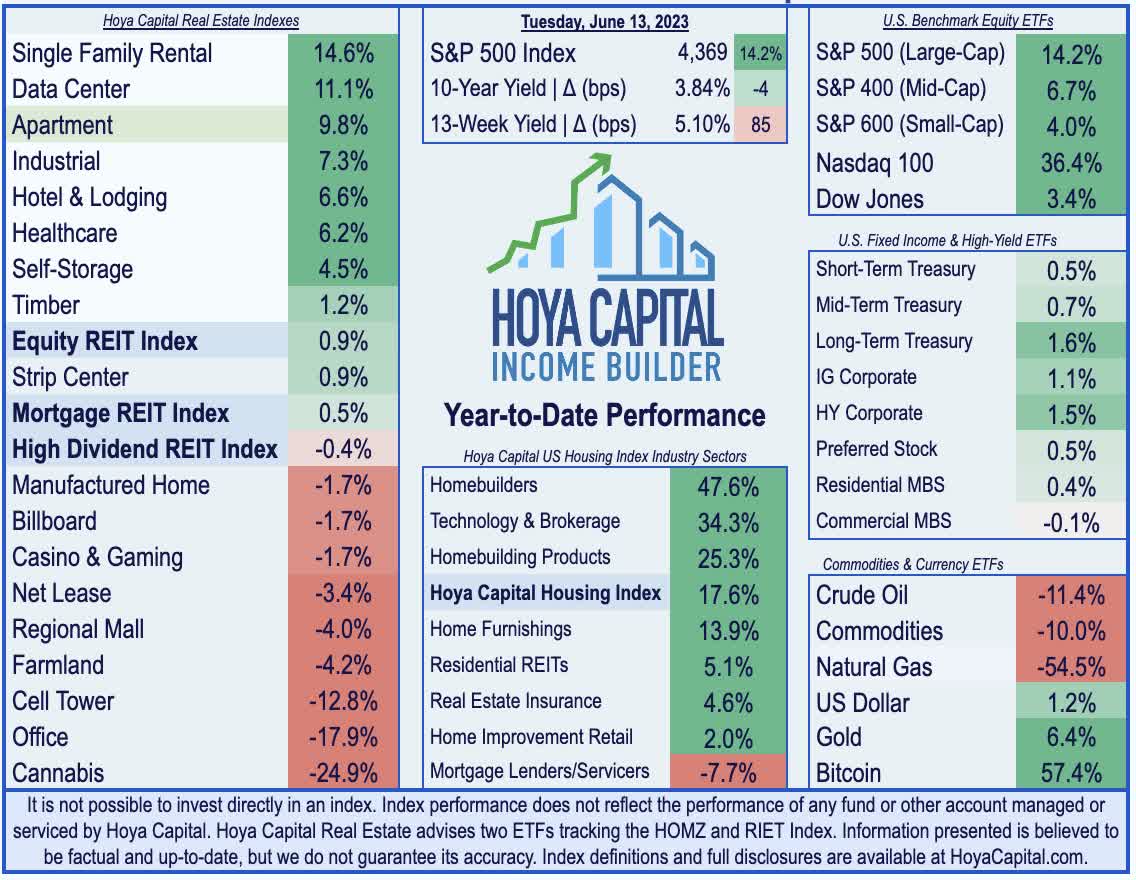

- Left for dead in late 2022 on expectations of a "hard landing" across rental markets, Apartment REITs are the third-best-performing property sector this year, lifted by surprisingly buoyant property-level fundamentals.

- Recent industry data has shown a reacceleration in rental rate and occupancy trends since bottoming in January, with rent growth appearing to stabilize in its typical "inflation-plus" range between 4-5%.

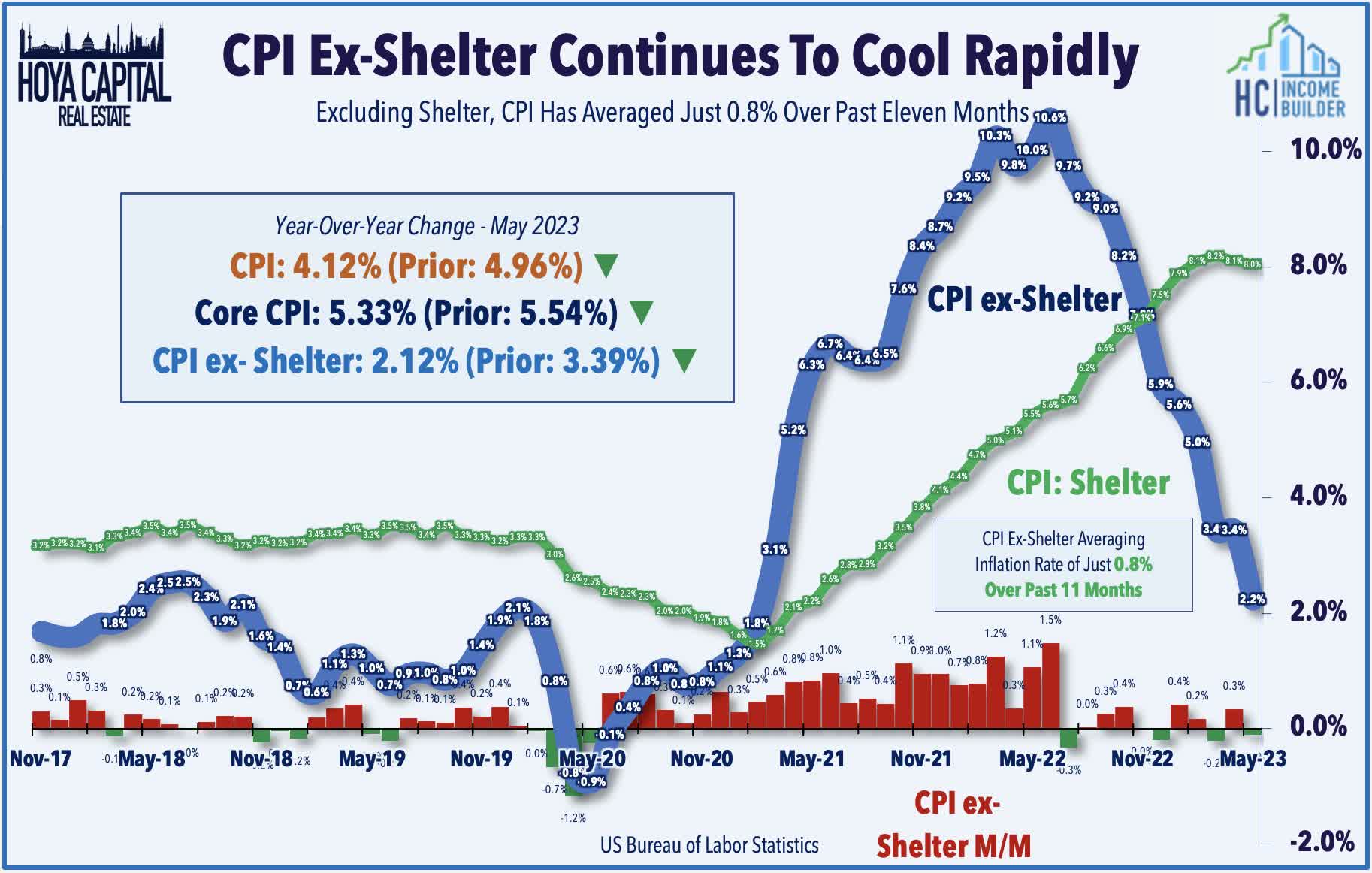

- This "inflation-plus" level of rent growth was the norm in the pre-pandemic era as housing demand outpaced new home development. Housing is back to being the primary driver of inflation.

- Supply concerns have been the unabating refrain from 'bears' over the past decade of outperformance. While the multifamily pipeline is historically large, overall housing development remains below equilibrium levels, and tighter financing conditions have curbed groundbreakings.

- We continue to employ a 'Sunbelt skew,' which worked exceptionally well throughout the pandemic as Sunbelt REITs delivered cumulative FFO that more than doubled their Coastal peers. We see a handful of mid-cap REITs as prime M&A targets from several large-cap REITs that have the balance sheet firepower to accretively consolidate.

REIT Rankings: Apartments

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on June 14th.

{kind=link}

Left for dead in late 2022 on expectations of a "hard landing" across rental markets, Apartment REITs are the third-best-performing property sector this year, lifted by surprisingly buoyant property-level fundamentals. Within the Hoya Capital Apartment REIT Index , we track the fifteen largest apartment REITs, which collectively account for roughly $130B in market value and own over a million rental units across the United States. Apartment REITs were the second-worst-performing property sector in 2022 - barely outperforming the troubled office sector - despite delivering a record year of operating performance underscored by 20% growth in Funds From Operations ("FFO") but have rebounded this year as calls for a "hard landing" in rental markets have so far proven to be incorrect. Instead, recent industry data has shown a reacceleration in fundamentals since bottoming in January, with rent growth appearing to stabilize in its typical "inflation-plus" range.

{kind=link}

Relief may be in sight for renters across the nation that, for several years, were receiving an unwelcome surprise at the end of their lease term with double-digit percentage increases on their renewal offer and even higher effective rent increases on new lease offers. Consistent with a broader cooling of inflationary pressures, the historic pace of rent growth has moderated significantly since peaking at around 20% nationally in late 2021, but recent apartment REIT earnings results and forward guidance have pushed back on the dire narrative depicting a " crash " in rental markets. While rent growth on new leases have cooled to around 3.5% thus far in 2023, renewal spreads remained firm at above 6%. Buoyed by these firm renewal spreads, Apartment REITs expect average same-store NOI growth of nearly 7% and FFO growth of roughly 4% in 2023 - among the highest in the REIT sector.

{kind=link}

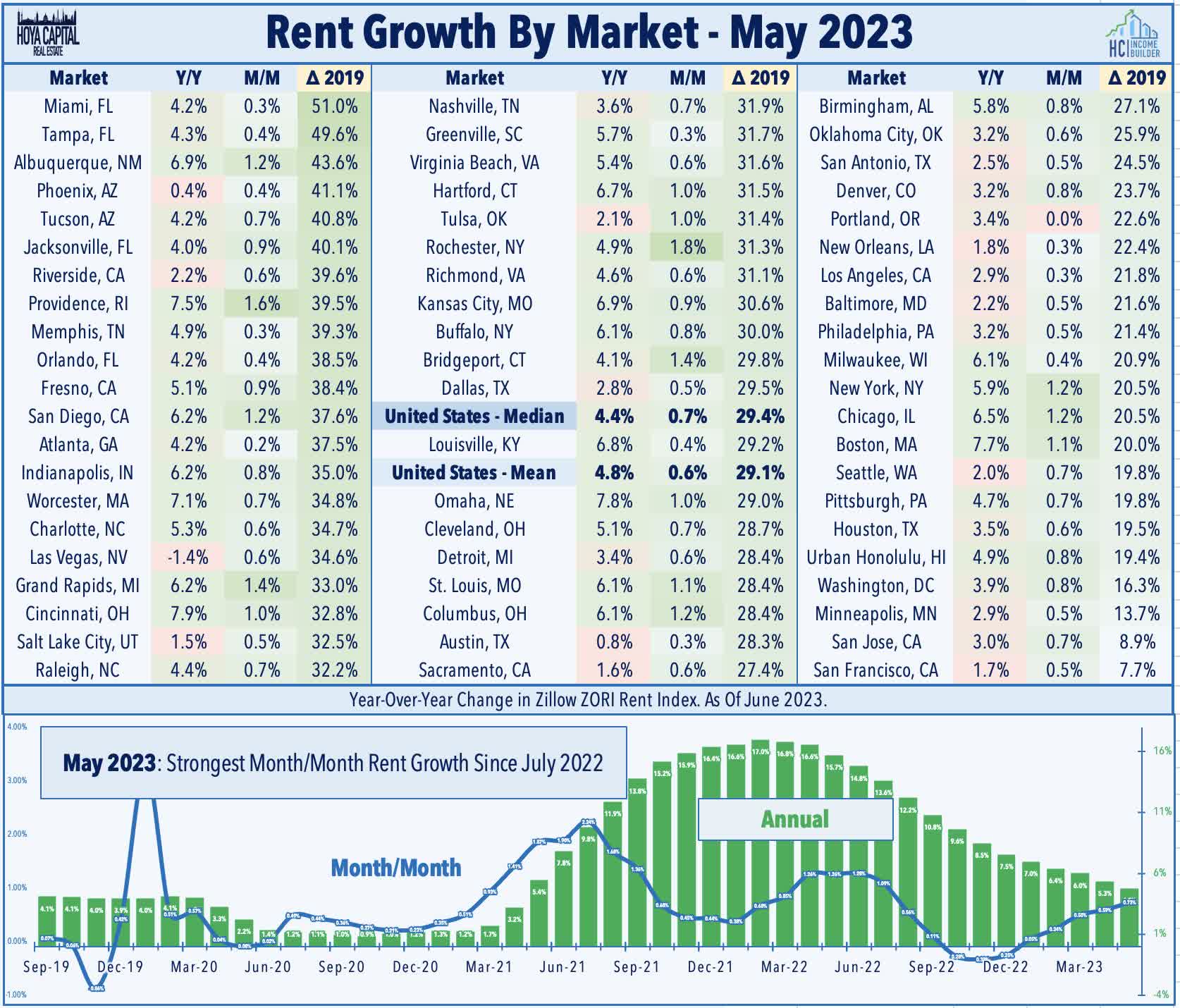

While market valuations still indicate that investors haven't given up on the "hard landing" narrative, recent data and forecasts from the leading multifamily data providers confirm our "soft landing" prediction of a steady normalization in rent growth and a modest uptick in vacancy rates back towards historical averages, but not the outright steep declines in rental rates that are currently being seen in prices off other pandemic-affected commodities and goods. Notably, the latest data from Zillow ( Z ) shows that annual rent growth for the median U.S. market moderated to 4.8% in May - down from the 17.0% peak in early 2022 - but recorded a sequential month-over-month increase for a fifth straight month following a stretch of three-straight declines in late 2022. Consistent with apartment REIT reports, we've seen more variation in market-level performance this year, with some Northeast and Midwest posting the strongest rent growth in recent months, while some previously-soaring Sunbelt markets have been pressured by pockets of supply growth. West Coast markets have remained weak.

{kind=link}

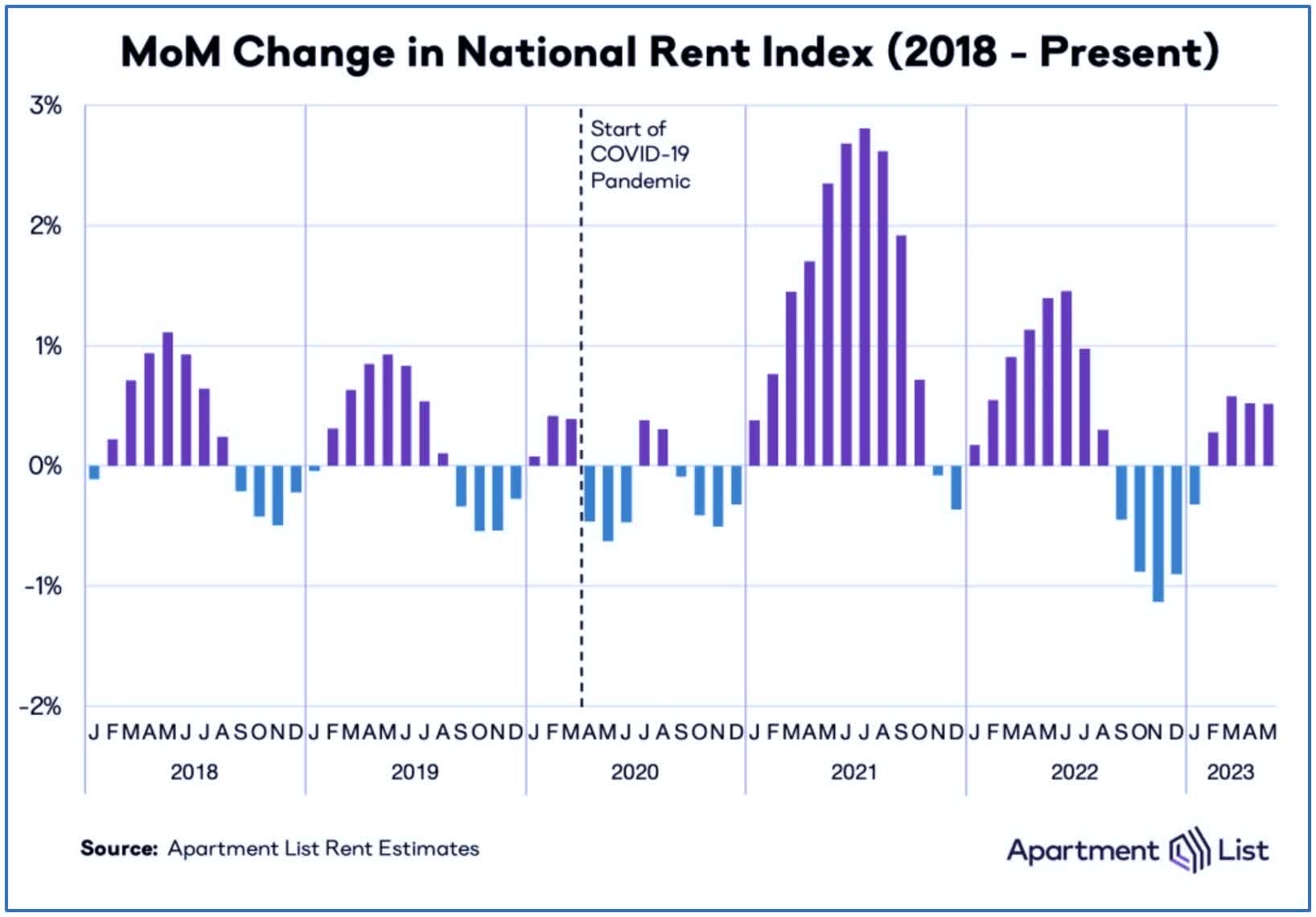

Apartment List data shows similar trends in its National Rent Report, noting that while the year-over-year rent growth cooled to 0.9% in May, rents have increased in each of the past four months beginning in February. Their forecast for the balance of 2023 remains more pessimistic than those provided by apartment REITs, however, commenting that the apartment market "remains sluggish even as rents continue on an upward trajectory... and even if demand rebounds over the summer, a strong construction pipeline should temper rent growth for the remainder of the year." Its report also noted the emerging market-level variations, highlighting strength in Midwestern markets, commenting that "markets in the Midwest may now represent some of the last bastions of affordability" and noted that California remains a persistent soft spot, pointing out that San Francisco and San Jose are the only two large metros where the median rent is currently cheaper than it was at the pandemic’s onset. Elsewhere, Yardi's 2023 forecast calls for 2.6% rent growth in 2023 while Real Page Analytics sees rent growth at 2.9% for 2023.

{kind=link}

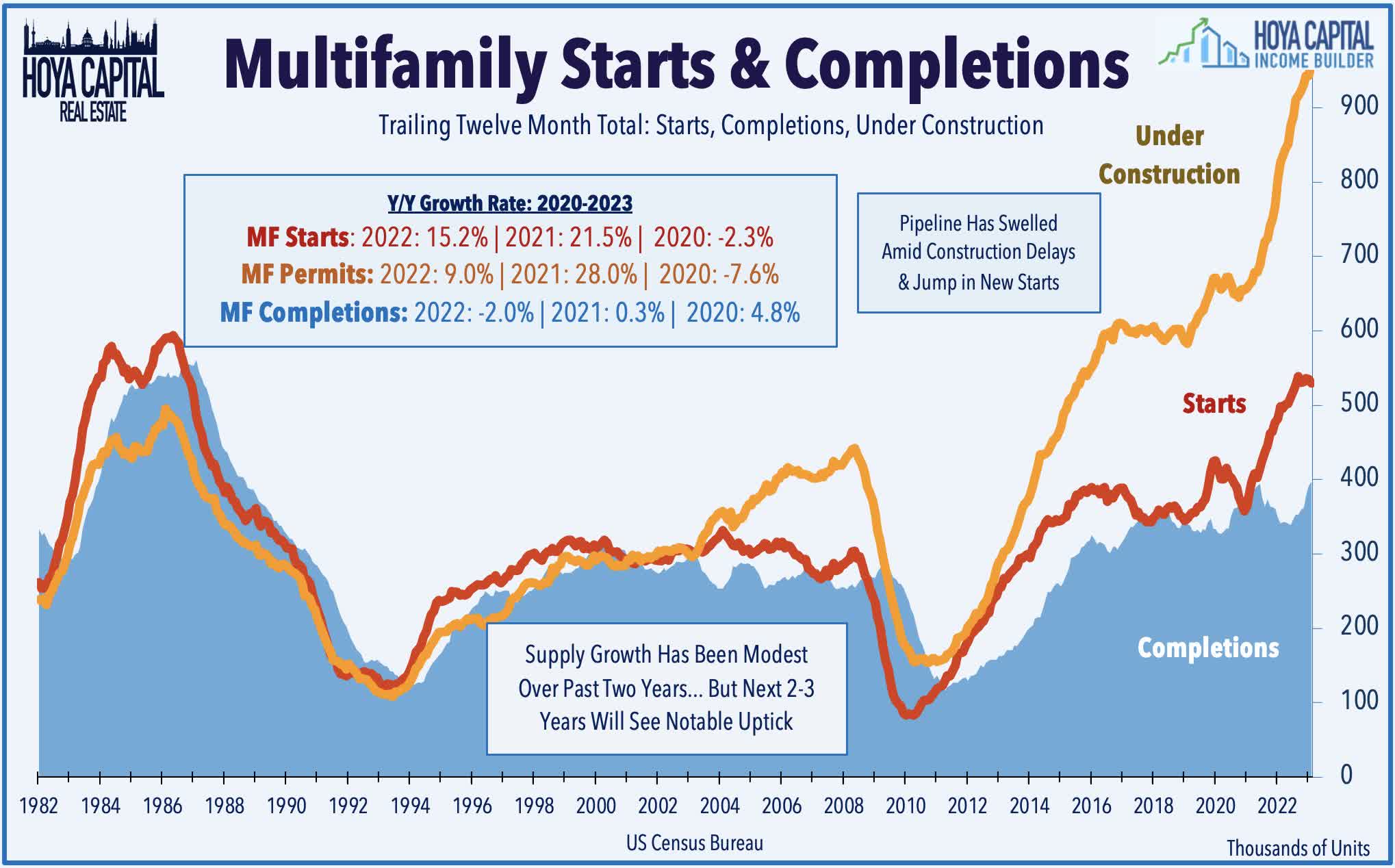

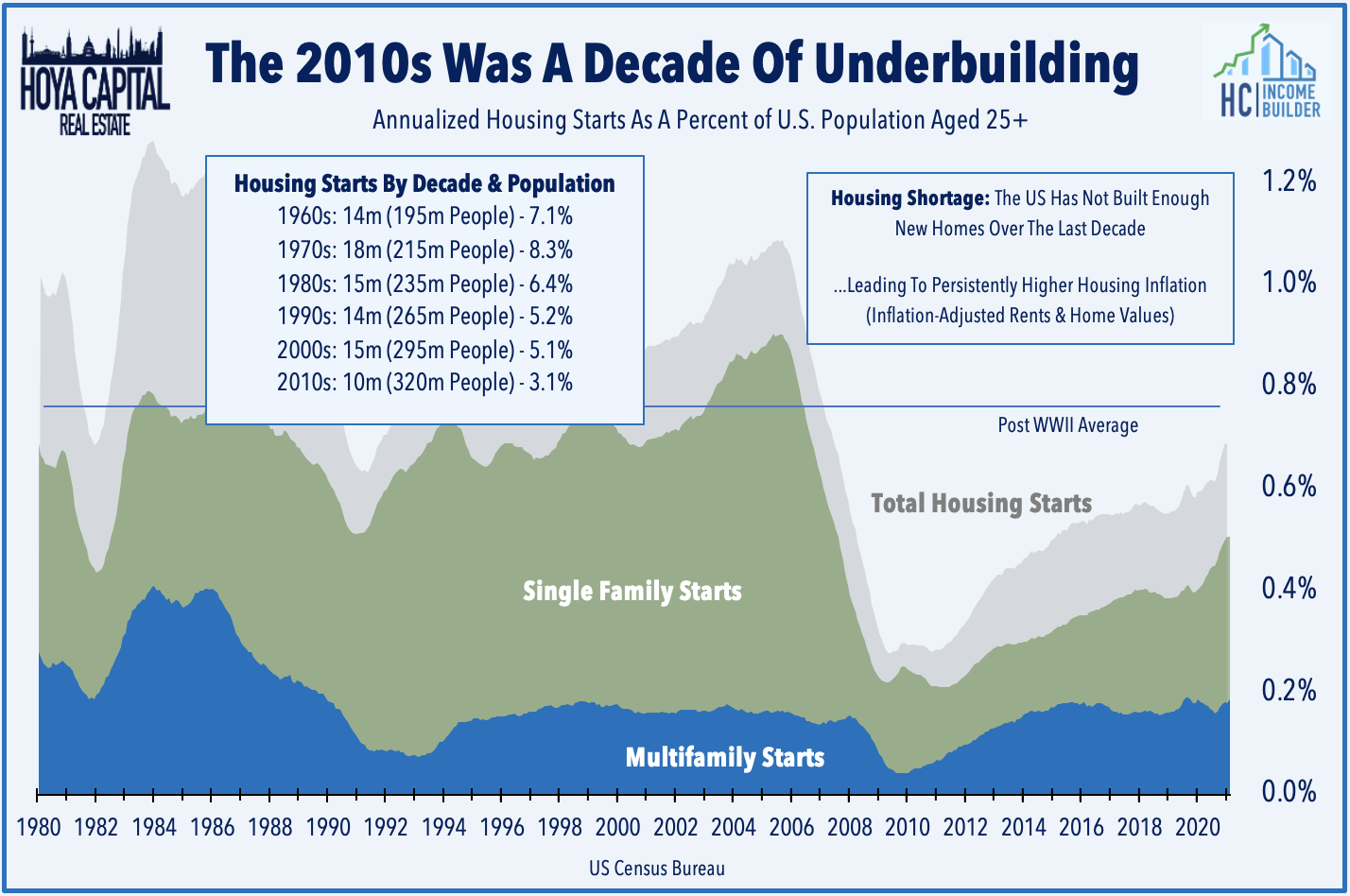

Supply concerns remain the root of the market pessimism as soaring rents sparked a wave of new development that will come to market over the next 18 months, but we believe the often-cited metrics look more menacing than reality. After several years of muted supply growth, multifamily starts jumped 20% in 2021 and another 15% in 2022, but this acceleration in apartment development was offset nearly one-for-one with a pull-back in single-family development. Driven largely by the effects of the elongated development timelines resulting from supply chain disruptions and labor constraints, the pipeline of under-construction units has swelled to nearly 1 million units in early 2023, up considerably from the roughly 450k peak during the prior two development peaks in 1985 and 2007. Yardi expects 440k units to be delivered in 2023 - up from the 325k in 2022 - representing a 2.9% increase in stock which roughly matches levels seen in 2018 and 2019.

{kind=link}

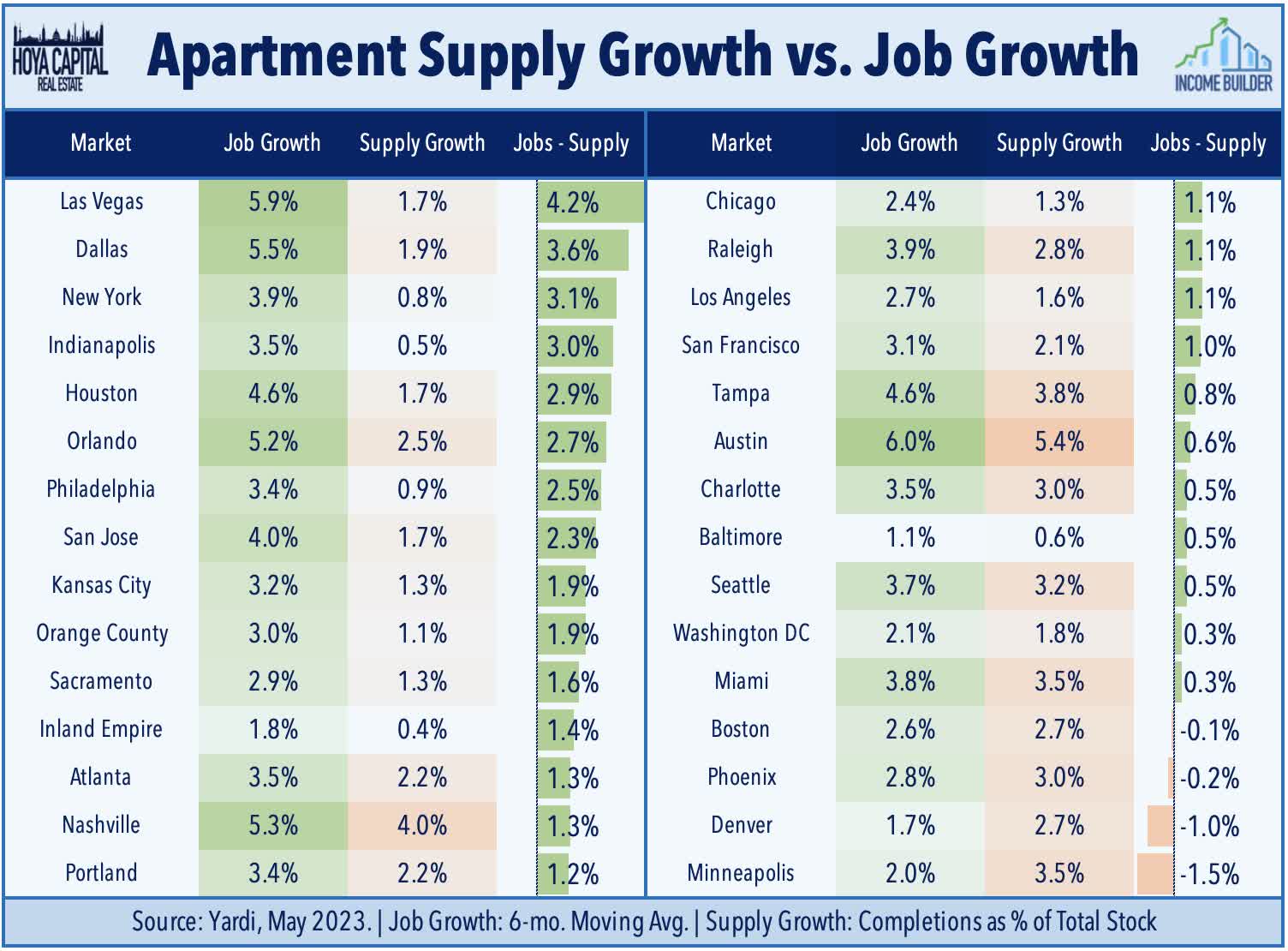

While the overall level of supply growth appears manageable - serving as a moderate headwind but not the looming disaster that some would suggest - Yardi does predict supply growth of over 4% across a handful of markets - primarily in the Sunbelt region - including Austin, Charlotte, Phoenix, Miami, and Nashville - markets that have generally seen the strongest population growth and cumulative job growth over the past three years. Yardi projects that deliveries will begin to wane by mid-2024, however, due to lingering or worsening impediments to new development, including the difficulty of getting construction financing, ongoing delays in labor, and challenges in getting entitlements from local planning and zoning boards. These supply headwinds require an even more discerning approach, but it's important to avoid putting too much weight on the supply factor alone - which would otherwise suggest that markets like Baltimore and the Inland Empire are poised to become top markets. Instead, supply growth should be balanced against job growth - the best available proxy for apartment demand - which shows that some of the more supply-heavy markets actually remain undersupplied relative to demand.

{kind=link}

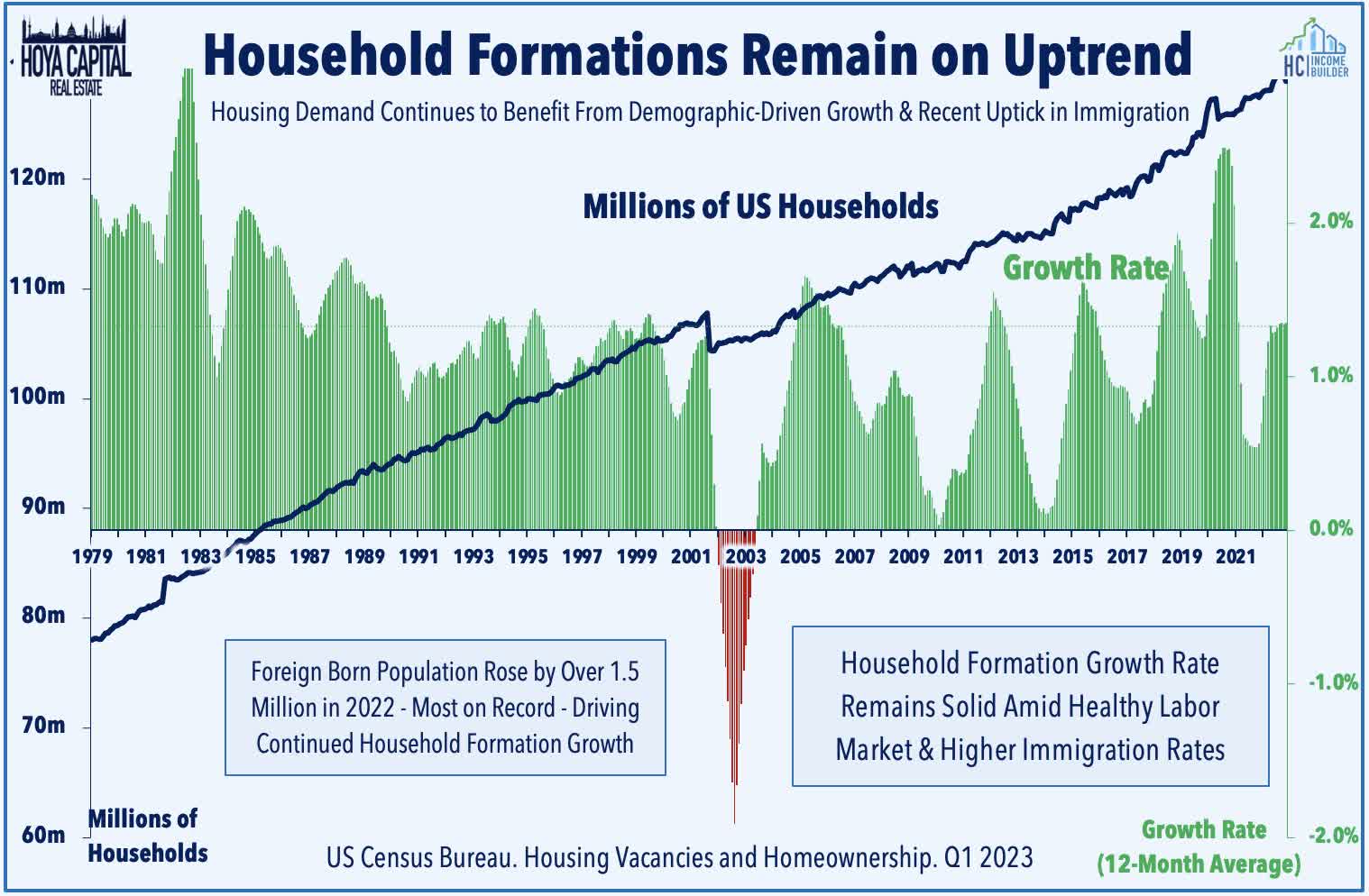

As we've discussed at length over the past decade, demographics suggested the 2020s were already poised to see historic levels of housing demand as the millennial generation - the largest cohort in American history - comes full-steam into a severely undersupplied U.S. housing market. What we could not foresee, however, was the added acceleration provided by the pandemic-driven "Work From Home era" which has begun to unleash millions of extra "deferred" formations among adult children, in particular. Additionally, stronger-than-expected household formations trends are consistent with our long-held theory that population estimates and - and thus U.S. population growth - have been materially understated by Federal statistical agencies over the past several administrations due primarily to the undercounting of immigrant populations, an undercount that the Census Bureau confirmed in a report last year. Net international migration added more than a million people to the U.S. population between July 1, 2021 and July 1, 2022 - a 168.8% increase from the prior year - marking the largest single-year increase since 2010. Net international migration added 1,010,923 people between 2021 and 2022.

{kind=link}

Apartment REIT Fundamentals

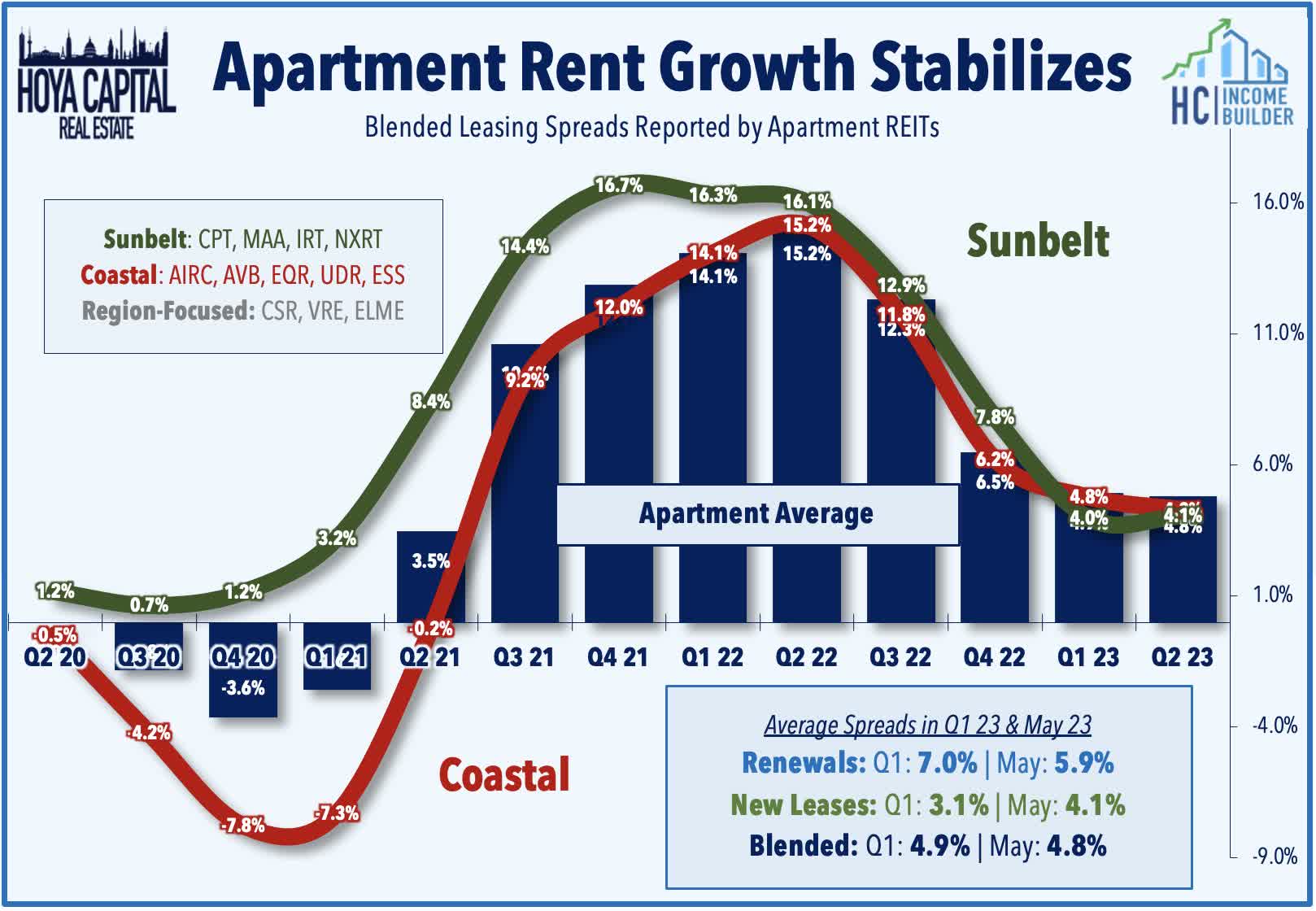

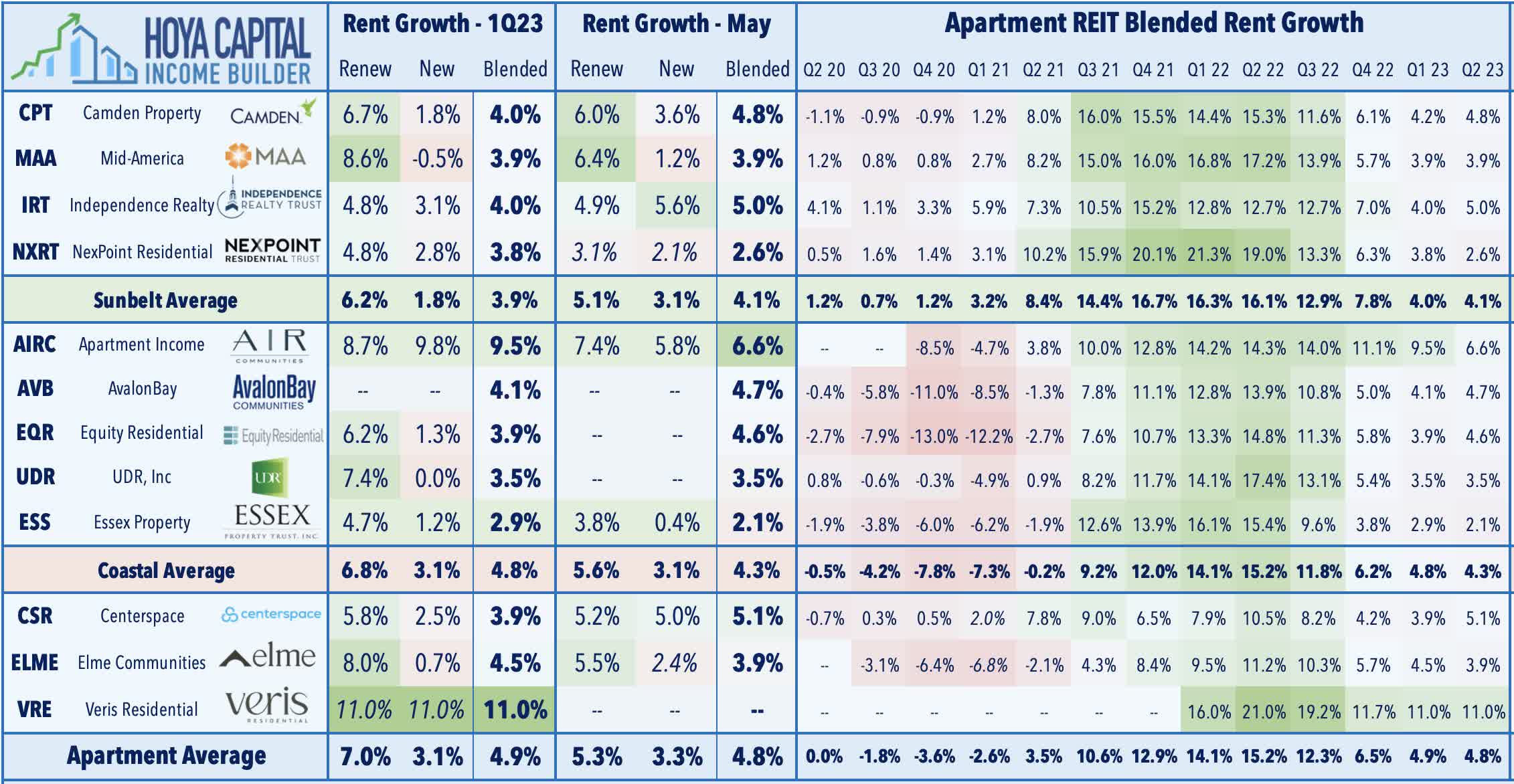

As discussed in our REIT Earnings Recap, apartment REIT earnings results and subsequent REITweek updates were solid across the board, showing similar "stickiness" to rental rate trends and underscoring the embedded rent growth that is still being unlocked from existing renters even as new lease rent growth cools from historic highs. Four apartment REITs hiked FFO estimates during Q1 earnings season and a fifth raised its outlook during REITweek - two Sunbelt-focused REITs and three coastal-focused REITs - while REITs across both regions reported nearly identical 4% blended rent growth in Q1 with a slight acceleration in April and into May, consistent with industry data showing that rental rate trends have firmed in recent months following a sharp deceleration in late 2022. While commentary indicated expectations of supply headwinds later this year, most REITs have seen a material slowdown in new ground-breakings given tighter credit conditions, providing reasons for optimism heading into the back half of 2023 and into 2024.

{kind=link}

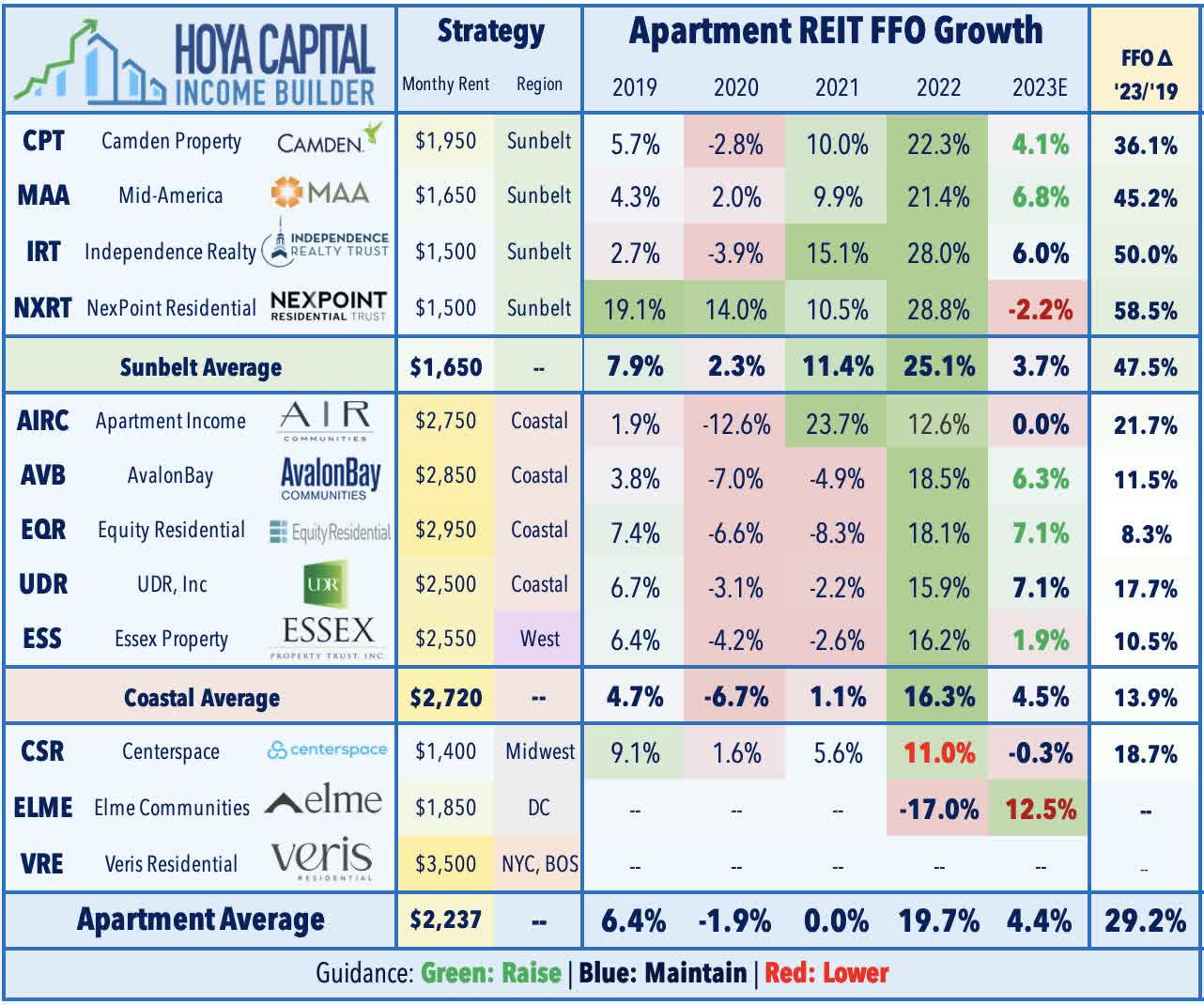

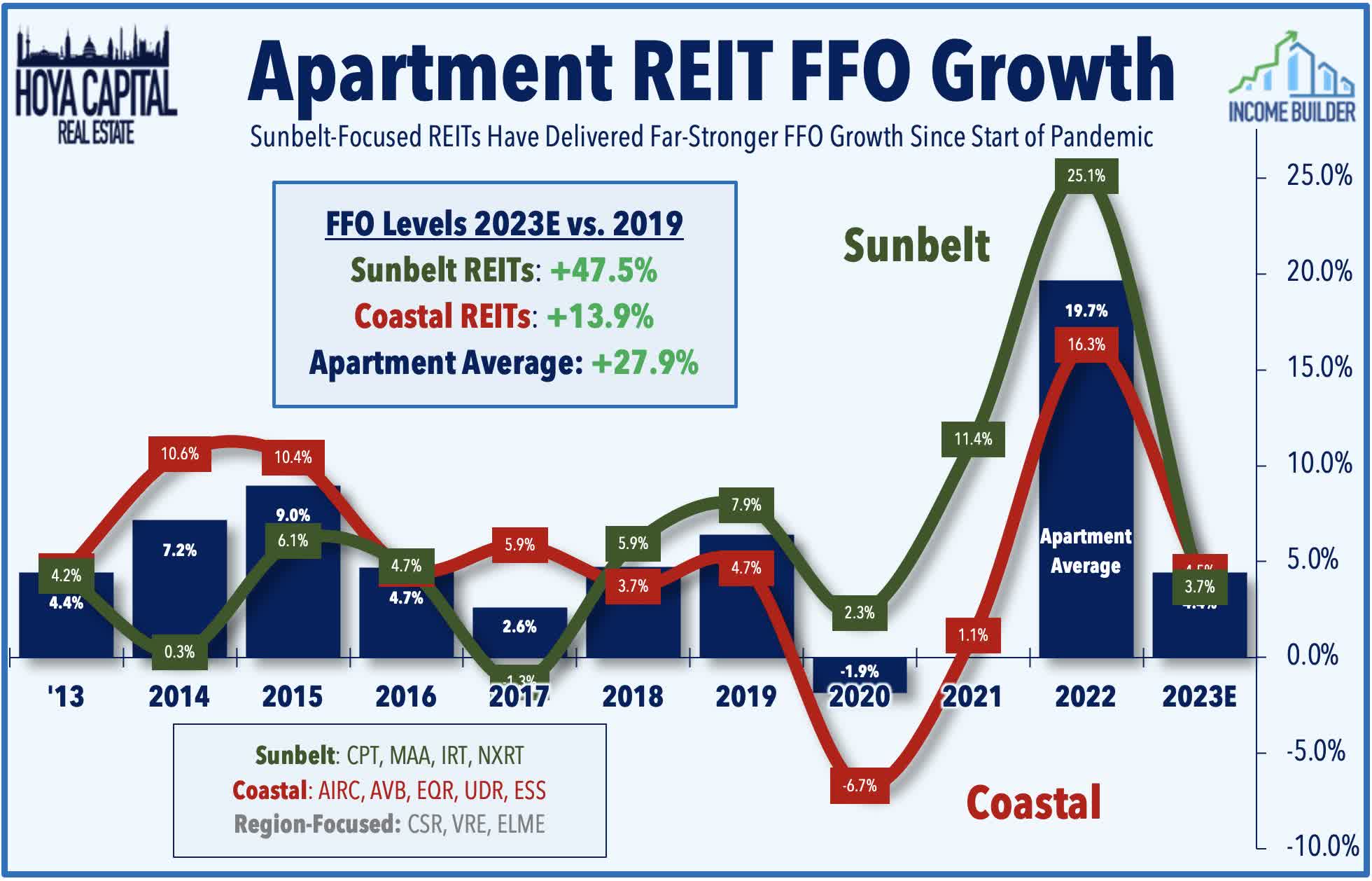

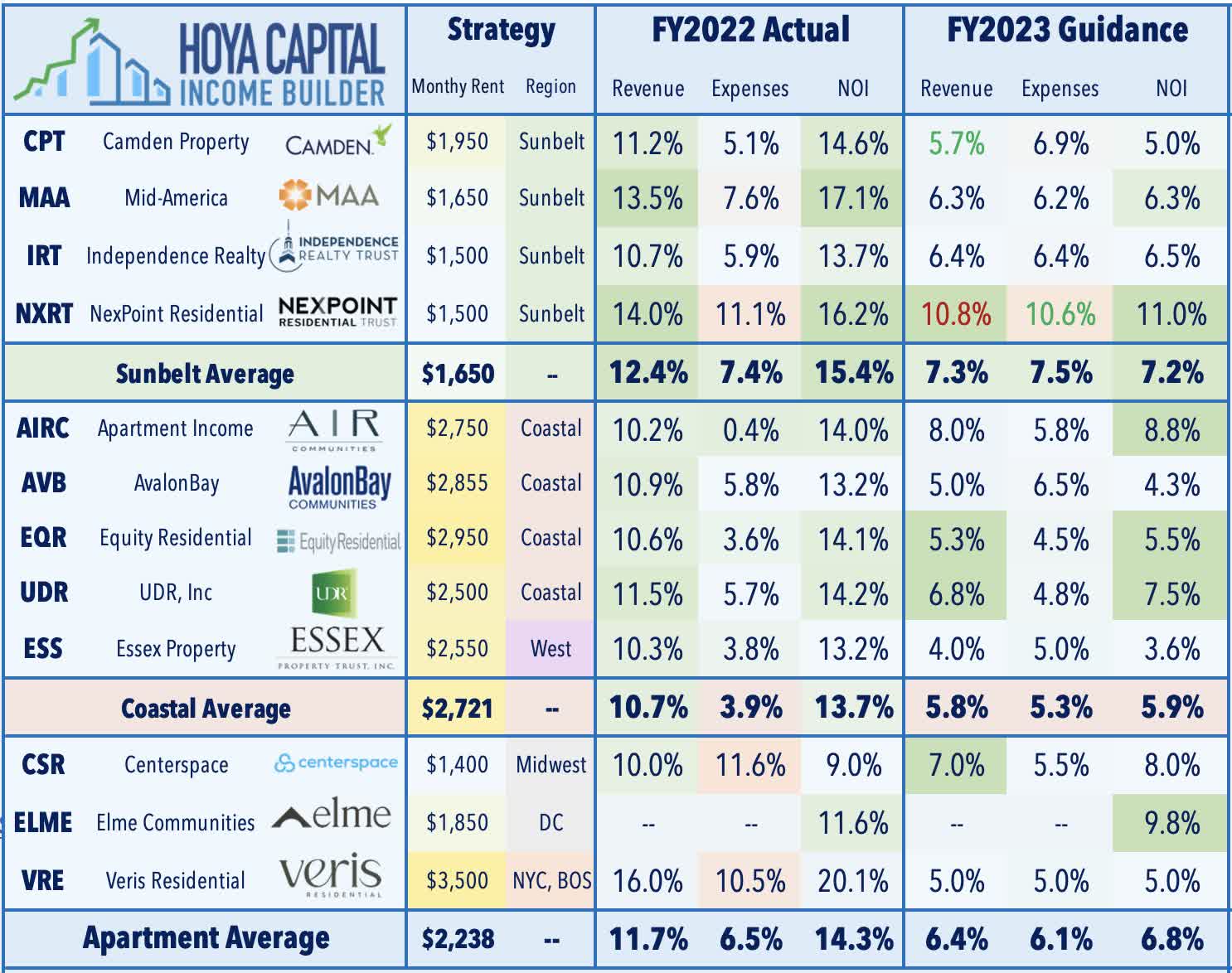

Apartment REITs delivered average FFO growth of 19.7% for full-year 2022 - the strongest year ever for the sector and the second-highest earnings growth rate across the real estate industry behind the roughly 23% growth from the storage REIT sector. The upgraded outlook for 2023 now calls for FFO growth of 4.4%, on average, which would likely trail only the industrial and manufactured housing sectors for the strongest across the REIT industry. If these full-year outlook targets are met, apartment REITs will have delivered average cumulative FFO growth of 27.7% since the start of the pandemic. Sunbelt REITs never skipped a beat during the pandemic and now expect 2023 FFO levels to be 47.7% above their pre-pandemic rate from 2019 while Coastal REITs now expect 2023 FFO levels to be 13.5% above 2019-levels.

{kind=link}

The strength of renewal rent growth was perhaps the most significant takeaway from these results. While new lease rates have seen a rather sharp sequential slowdown since peaking in Q2 at 17.5% and slowing to 3.1% in Q1, renewal rates held relatively steady in the high-single-digits over the past three quarters, averaging 7.0% in Q1 and over 5% in January. Among the coastal-focused REITs, Apartment Income ( AIRC ) reported the strongest rent growth metrics with 9.5% and 6.6% blended spreads during these periods, while NYC-focused Veris Residential ( VRE ) also reported impressive results with blended spreads of over 11% in the first quarter. Notably, seven of the eleven REITs that provided REITweek leasing statistics reported a sequential acceleration in blended leasing spreads in May compared to Q1.

{kind=link}

Among the recent highlights, Equity Residential ( EQR ) boosted its full-year earnings outlook during REITweek, citing strong demand in New York and lower than previously anticipated delinquency in southern California. EQR now expects full-year FFO growth of 7.1% at the midpoint - up 80 basis points from its prior outlook provided in April - and expects to report 2023 same-store net operating income (NOI") growth of 6.5% at the midpoint, up 100 basis points from its prior midpoint of 5.5%. EQR commented that its "benefiting from limited new apartment supply in most of our markets as well as the high prices and low availability of single family housing in these markets." AvalonBay ( AVB ) raised its full-year FFO growth outlook in Q1 and commented that its recent leasing activity is "materially exceeding expectations." NexPoint Residential ( NXRT ) was one of two apartment REITs to lower its FFO outlook - a revision driven by higher interest expense - but the small-cap REIT also reported perhaps the strongest property-level metrics.

{kind=link}

Deeper Dive: Apartment REIT Portfolios

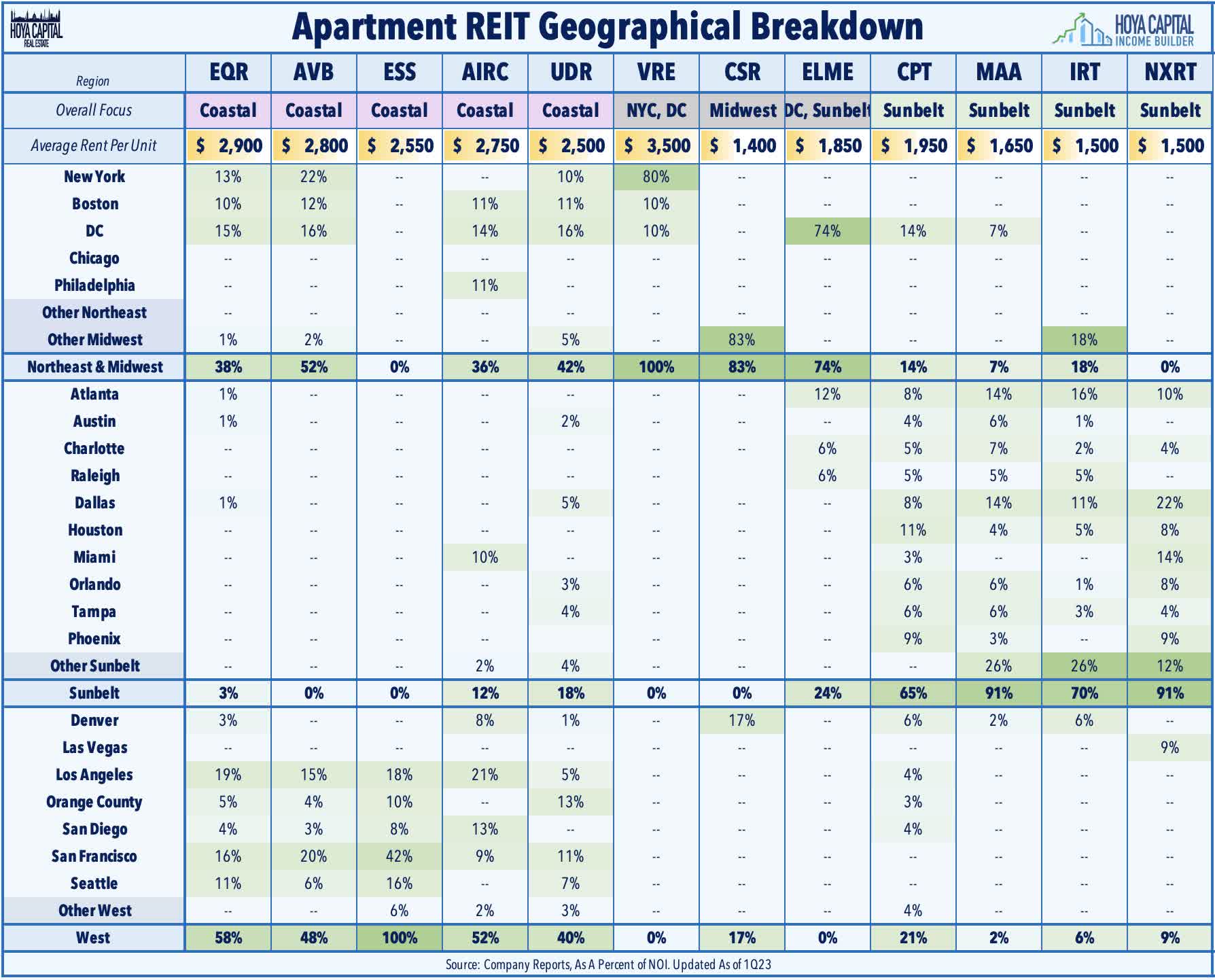

As a sector, apartment REITs collectively have fairly balanced geographical exposure across most of the major U.S. markets. Individual apartment REITs tend to focus on either coastal markets or sunbelt and secondary markets and own portfolios that typically include a blend of luxury high-rise, mid-rise, and garden-style apartment communities. Several of the newer apartment REITs are more geographically concentrated, including Veris Residential ( VRE ) - formerly known as Mack Cali - which derives around 80% of its revenues from the New York City metro region, and Elme Communities ( ELME ) - formerly known as Washington REIT - which is primarily based in Washington, DC. Equally as important as their regional distribution is the composition of portfolios towards either urban or suburban assets and towards the Class A or Class B segment. Secondary and tertiary markets have generally seen lower levels of new development in recent years, with much of the new supply growth concentrated in the luxury segment.

{kind=link}

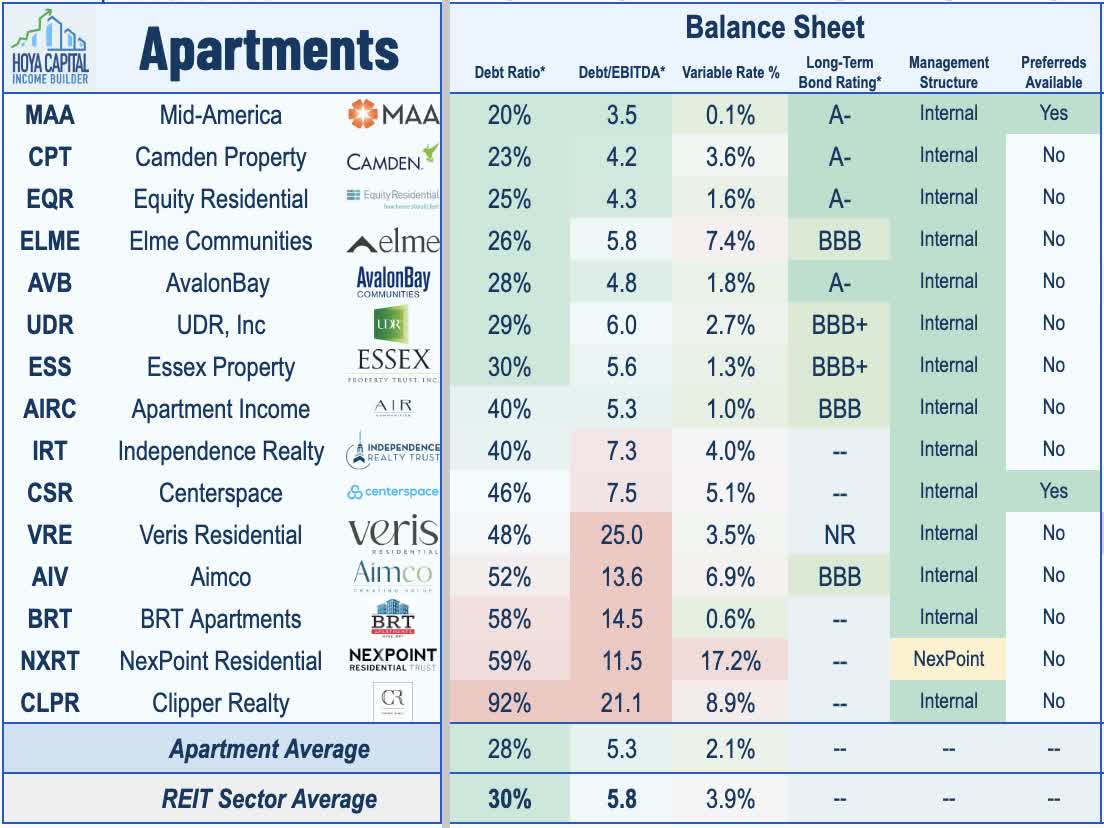

The larger apartment REITs are generally some of the most well-capitalized companies across the REIT sector - a critical attribute during the pandemic-related turbulence - but several of the small-cap apartment REITs do operate with elevated debt levels with more exposure to variable-rate debt. Among those is NexPoint Residential , but we've been pleased with NXRT's recent progress in reducing their variable rate exposure through asset sales, refinancings, and the use of interest rate locks. The seven largest apartment REITs command investment-grade credit ratings from Standard & Poor's, led by A- ratings by AvalonBay , Equity Residential , and Camden . The larger REITs in the sector also tend to rank high on the corporate governance scale with shareholder-friendly governance structures.

{kind=link}

Apartment REIT Stock Performance

The Hoya Capital Apartment REIT Index has rebounded in 2023 on recent reports and industry data showing buoyant rent growth and occupancy trends, gaining nearly 10% so far in 2023, outpacing the 0.9% advance from the broad-based Vanguard Real Estate ETF ( VNQ ) and the 6.7% gain from the SPDR S&P MidCap 400 ETF Trust ( MDY ). Apartment REITs have been some of the strongest-performing REITs over most long-term measurement periods. From 2010 through 2022, Apartment REITs delivered average annual returns of 15.0%, outpacing the 10.4% annual total returns from the broad-based REIT average during that time. Six apartment REITs are higher by double-digit percentages on the year, led by the coastal-focused REITs including AvalonBay , Equity Residential , and Essex .

{kind=link}

Apartment REIT Dividend Yields

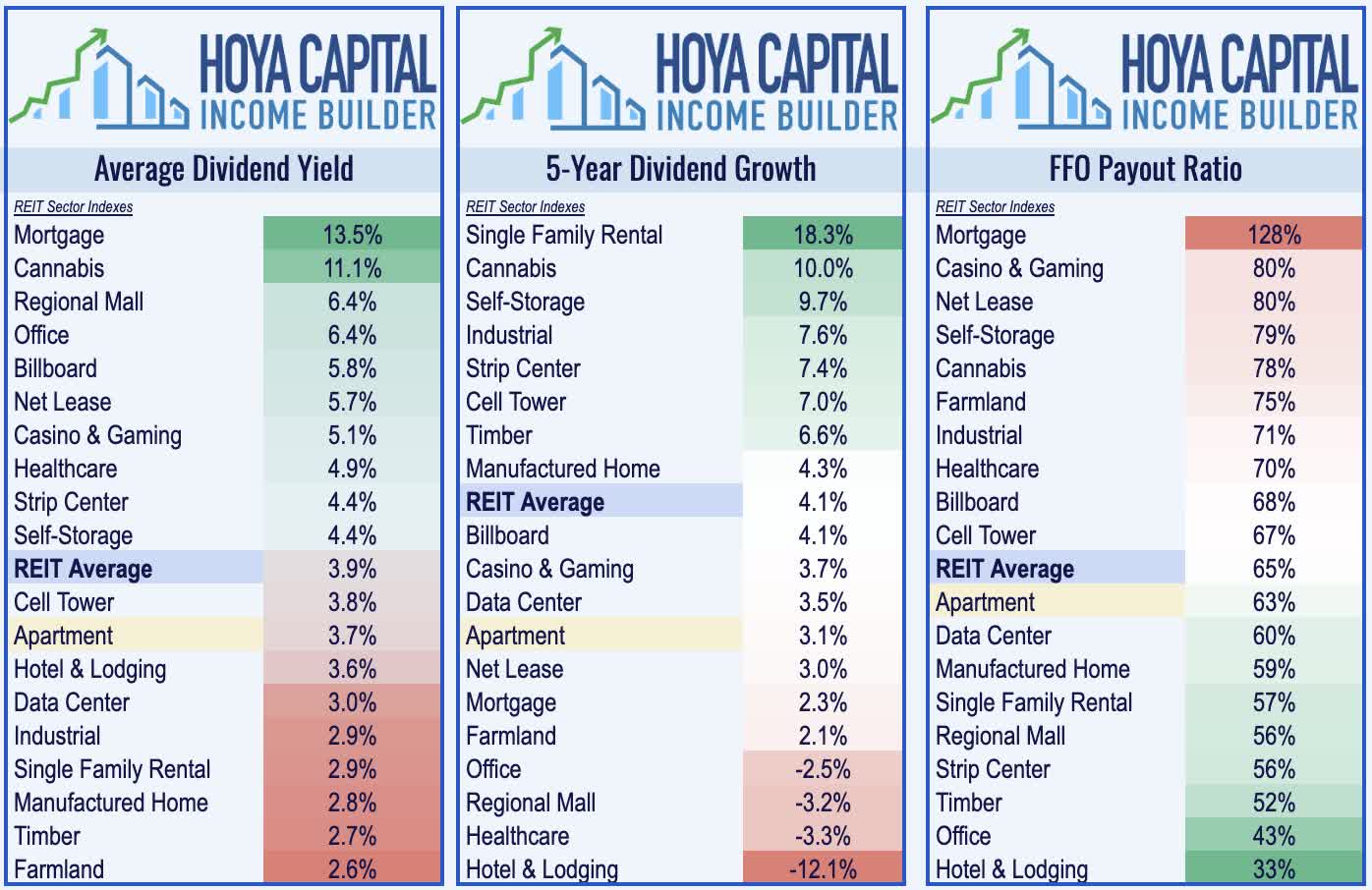

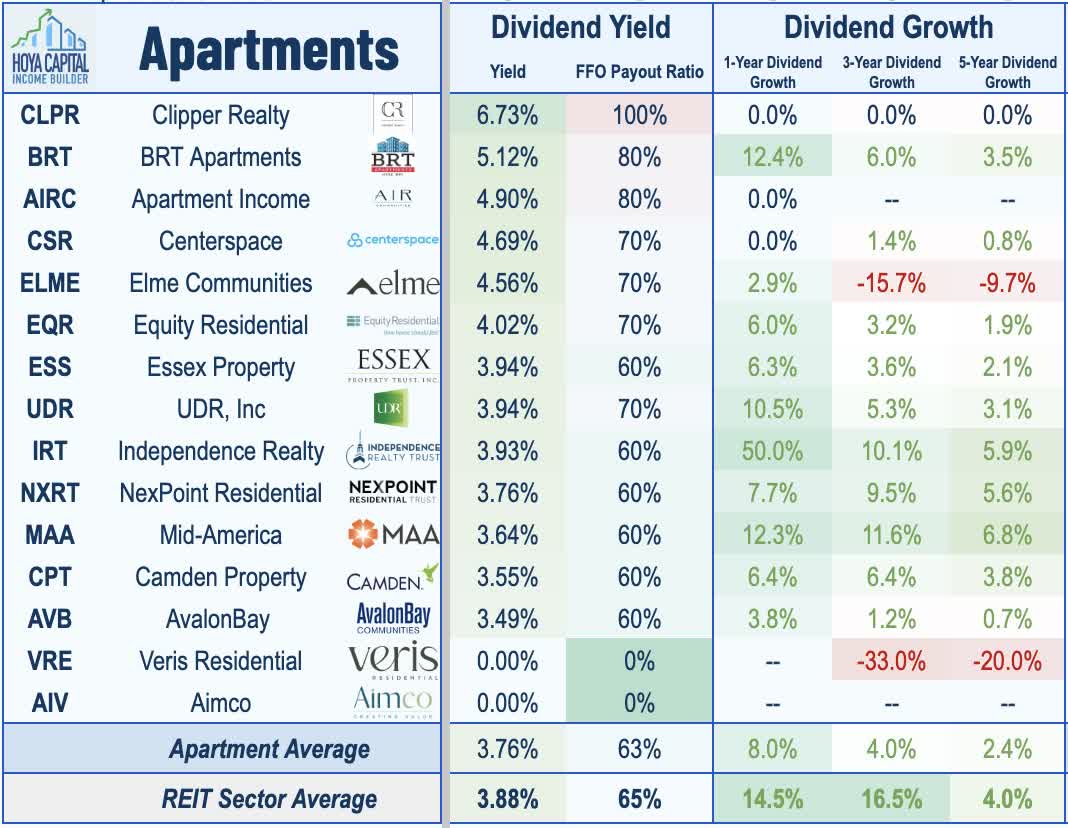

Near-perfect rent collection throughout the pandemic allowed apartment REITs to not only avoid the wave of dividend cuts that swept through the REIT sector during the early stages of the pandemic but also to be among few REITs to raise their distributions in during the depths of the pandemic in 2020 - a trend of dividend raises that continued in 2021 and 2022. Apartment REITs pay an average dividend yield of 3.8%, which is slightly below the REIT market-cap-weighted sector average of 3.9%. Since the start of 2015, apartment REITs have delivered average annual dividend growth of roughly 3% as near-double-digit growth from Sunbelt-focused REITs has offset the more muted dividend growth delivered by Coastal-focused REITs.

{kind=link}

Apartment REITs only payout around 60% of their available cash flow, giving these companies the flexibility to take advantage of external growth opportunities or to increase future distributions. Seven apartment REITs have raised their dividends so far in 2023, including a 14% dividend hike from Independence ( IRT ) last week and a pair of 10% dividend hikes from NexPoint Residential ( NXRT ) and UDR ( UDR ) earlier this year. Camden ( CPT ) and Elme Communities ( ELME ) each raised their dividends by 6%, while AvalonBay raised its payout by 3%. Small-cap Clipper ( CLPR ) tops the charts with a dividend yield of 6.73%, followed by BRT Apartments ( BRT ) at 5.12% and Apartment Income at 4.90%.

{kind=link}

Takeaway: Return of 'Inflation-Plus' Growth

Renting or owning - housing has become significantly more expensive over the past three years as pre-existing secular tailwinds related to the lingering housing shortage were given an added pandemic-related accelerant. The historic surge in mortgage rates since early last year cooled the once-red-hot housing market, but the secular tailwinds couldn't be held back indefinitely. Consistent with our contrarian prediction in late 2022 when apartment REITs were left for dead by analysts and pundits, multifamily fundamentals have remained surprisingly buoyant in recent months - even accelerating into the peak leasing season - and have been among the top-performing property sectors this year. While fundamentals remain more favorable on the single-family side - where the lack of supply is perhaps the bigger issue - we're also maintaining our overweight positioning on the multifamily side.

{kind=link}

Following two years of historic rent growth, there was little doubt that growth would moderate over the coming quarters - but the question was 'how much?'. Recent industry data has shown a reacceleration in rental rate and occupancy trends since bottoming in January, with rent growth appearing to stabilize in its typical "inflation-plus" range between 4-5%. This "inflation-plus" level of rent growth was the norm in the pre-pandemic era as housing demand outpaced new home development/ Elevated rent growth and stretched affordability metrics are perhaps the most obvious indication of a lingering undersupply of housing, as Freddie Mac estimates that the U.S. housing market is still more than 3 million housing units short of what's needed to meet the country's demand. We continue to employ a 'Sunbelt skew,' which worked exceptionally well throughout the pandemic as Sunbelt REITs delivered cumulative FFO that more than doubled their Coastal peers. We also see a handful of mid-cap REITs as prime M&A targets from several large-cap REITs that have the balance sheet firepower to accretively consolidate.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Apartment REITs: Rents Are Rising, Again